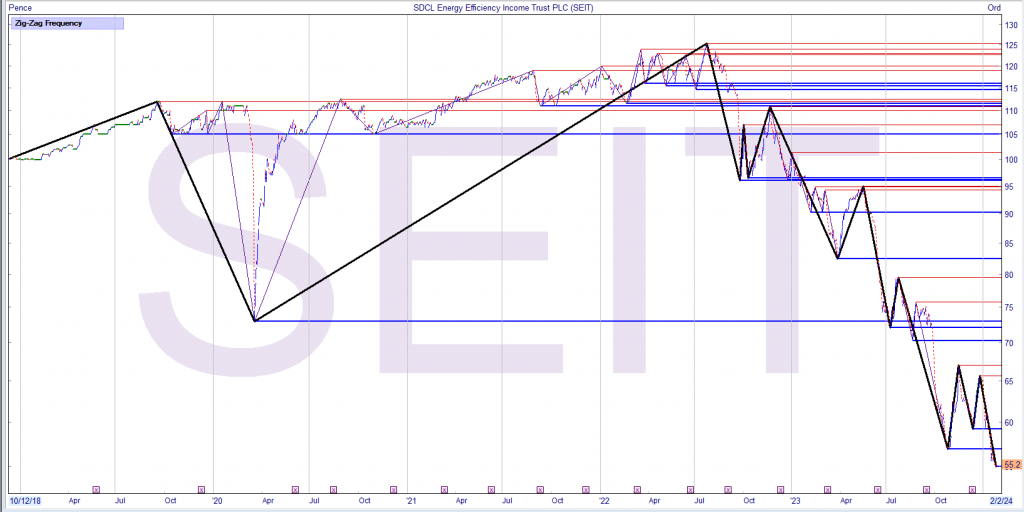

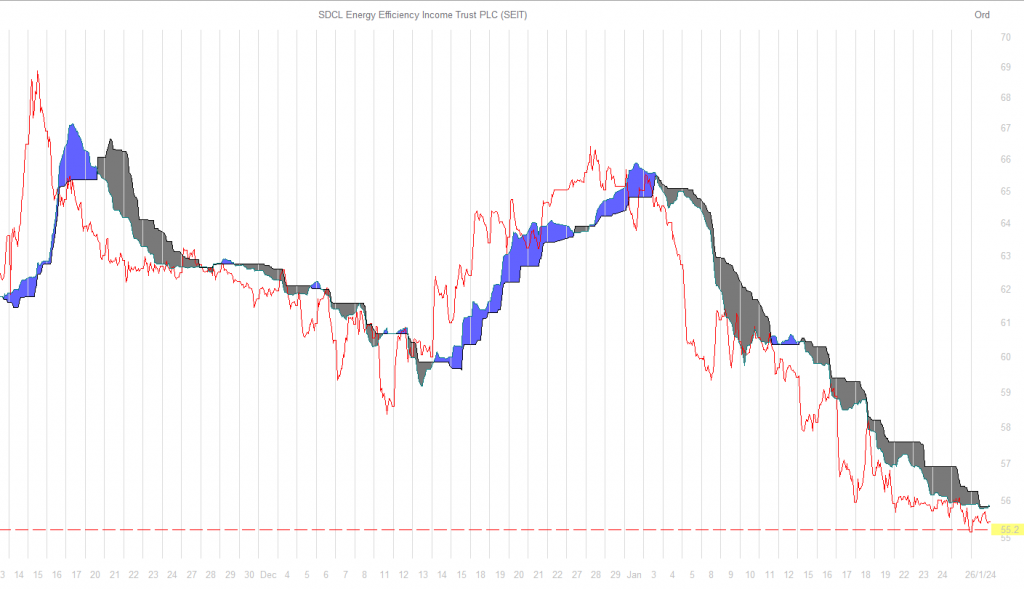

The reality of trading, it’s usually not easy. Currently yielding 11%

which may differ from your buying yield.

If I was a holder, I would hold for the dividends but I am not

so no decision needed.

Investment Trust Dividends

The reality of trading, it’s usually not easy. Currently yielding 11%

which may differ from your buying yield.

If I was a holder, I would hold for the dividends but I am not

so no decision needed.

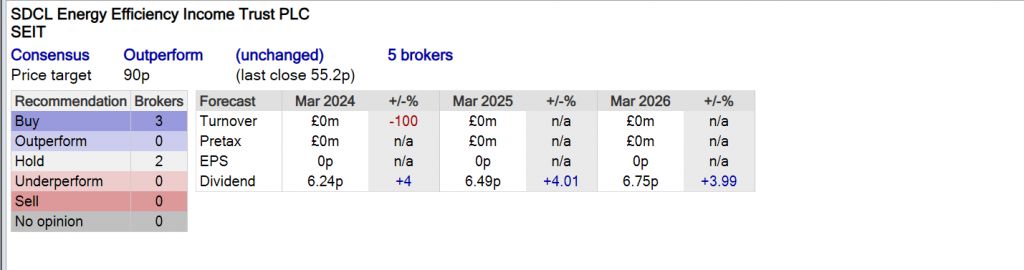

SEIT

Doceo Insights

By all accounts, London’s investment companies appear to have banished the discount blues that plagued them for much of the second half of 2023.

Or have they?

For while a dramatic drop in the tally of year-high discounters from those autumn peaks is undoubtedly a positive, before sounding the all-clear, a look beyond the headline numbers is called for, specifically at those investment companies with share prices trading close to year-high discounts. As Doceo Insights’ The 10%ers, the discount doldrums and a search (for positives) noted back in November 2023:

“Not much difference, after all, between a trust trading at its widest discount of the year and one trading a basis point or two off its widest discount of the year. To measure the extent of the discount issue, a more complete picture is needed, one that takes account of all investment companies trading at or close to their 52-week high discounts…” The article goes on to ask, and then answer, the following question: “But how close is close? A cut-off is required. For the purposes of this exercise, the cut-off will be set at those trusts trading at discounts that are within 10% of their respective 52-week highs – the 10%ers. Next step, totting up the 10%ers to see just how big London’s discount issue is.”

Three months on, seems only one thing for it – another roll call of the 10%ers needs to be taken to gauge if the discount doldrums have been well and truly blown away. First though…

A comparator is needed

Helpfully, the above Doceo Insights provides one. As at Friday 27 October 2023, the height of the discount doldrums when a total of 56 investment companies were trading at 52-wk high discounts, another 57 funds were trading within 10% of the then year-high discounts. That makes a grand total of 113 funds, more than a third of the investment company space covered. How does that compare to the situation today?

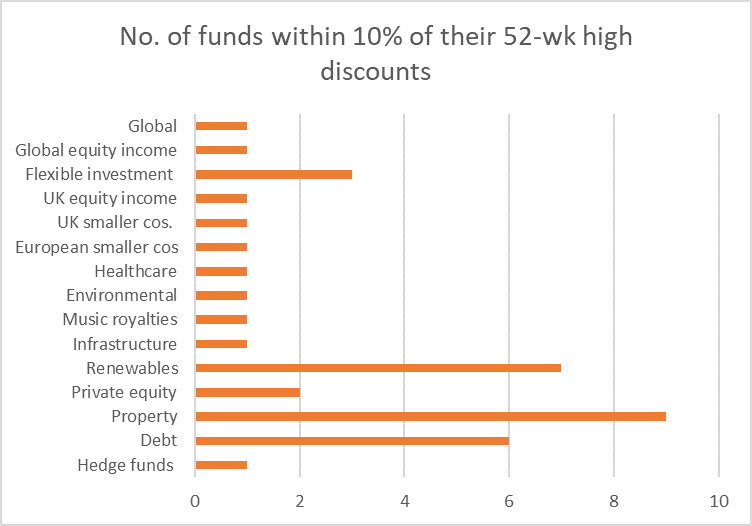

A quick count followed by a triple check of the results and the number of investment company share prices trading within 10% of their 52-wk high discounts currently stands at…

37

A little over 10% of the sample. A significant drop then. As the headline numbers over the past four weeks have been suggesting, the discount doldrums appear to be on the wane. Certainly, at the overall level. But…

What about individual sectors?

For all might be heading in the right direction at the headline number level, but that doesn’t mean a sector or two can’t still find themselves stuck in the doldrums. After all, there are 37 funds currently suffering from the discount blues. Question is, are they spread evenly across the sectors or do certain ones account for the lion’s share of the 37 names?

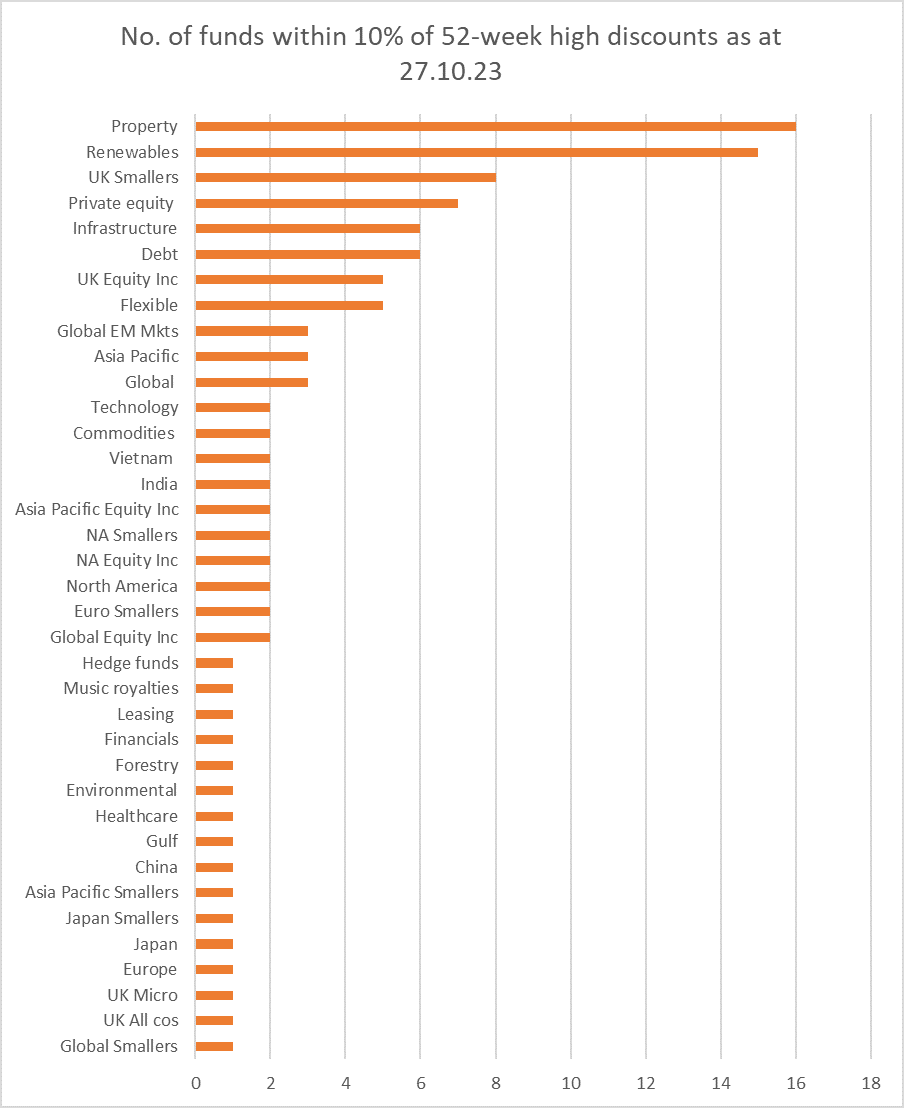

The below graphic provides a breakdown of the 37 funds by sector:

Three standouts catch the eye:

• Property tops the list with nine companies trading within 10% of their year-high discounts. That’s almost a third of the funds that are listed among the various investment company property sub sectors.

• Renewables, not far behind in second with seven names. 22 renewable energy infrastructure companies in the space so, as with property, almost a third of renewables still in the discount doldrums too.

• In third spot, debt – accounting for six of the total. Six out of 23 debt funds or around a quarter.

Shouldn’t be a surprise that the above 22, almost two thirds of the grand total, are alternatives. As Doceo Insights The 10%ers, the discount doldrums and a search (for positives) noted at the time: “With interest rates where they are, no surprise to see interest rate sensitive alternative sectors such as property, renewables, private equity, debt and infrastructure at the top of the pile, and by some margin.” Alternative investment company sectors still stuck in the discount doldrums then.

As with the Friday 19 January 2024 list, property and renewables occupy the top two spots, while debt, lying in sixth, still comfortably makes the top ten.

As with the Friday 19 January 2024 list, property and renewables occupy the top two spots, while debt, lying in sixth, still comfortably makes the top ten.

Has to be said though that, while there has been no change at the top, the number of property and renewable 10%ers is still noticeably down on the 27 October level. Currently:

• Nine property cos as opposed to 16 as at 27 October; and

• Seven renewables compared to 15 three or so months ago.

So, while the two sectors may still be in the doldrums, it’s not as bad as it was.

AERI, FSF, SHIP, ORIT, BNKR, CREI, API, IEM, MRC, SSON, SST, JMI

Welcome to this week’s Watch List where you’ll find golden nuggets on trust discounts, dividends, tips and lots more…

Frank Buhagiar

22 Jan, 2024

Doceo

BARGAIN BASEMENT

Discount Watch: seven

Our estimate of the number of investment companies whose discounts hit 12-month highs (or lows depending on how you look at them) over the course of the week ended Friday 19 January 2024 – four more than the previous week’s three.

Two of the seven were on the list last week: JPEL Private Equity (JPEL) from private equity; and Digital 9 Infrastructure (DGI9) from infrastructure.

That leaves five new names: Lindsell Train (LTI) from global; SDCL Energy Efficiency Income (SEIT) from renewable energy infrastructure; STS Global Income & Growth (STS) from global equity income; ICG-Longbow Senior Secured UK Property Debt Investment (LBOW) from debt; and Third Point Investors (TPOU) from hedge funds.

ON THE MOVE

Monthly Mover Watch: a swap

At the summit of Winterflood’s list of top-five monthly movers in the investment company space with last week’s number two HydrogenOne Capital Growth (HGEN) (+28.6%) overtaking previous leader Seraphim Space (SSIT) (+26.1%). Still no news out from the hydrogen investor since November 2023, so sticking by last week’s comment: “Put this one down to the positive effect of lower yields then or could there be a whiff of corporate activity in the air? HGEN has a sub £100m market cap after all and it’s not as if there hasn’t been any corporate activity in the renewables sector recently.” Similarly, no new news out from SSIT but shares have been reaching for the stars ever since the turn of the year – the space investor recently put out a monthly shareholder letter…

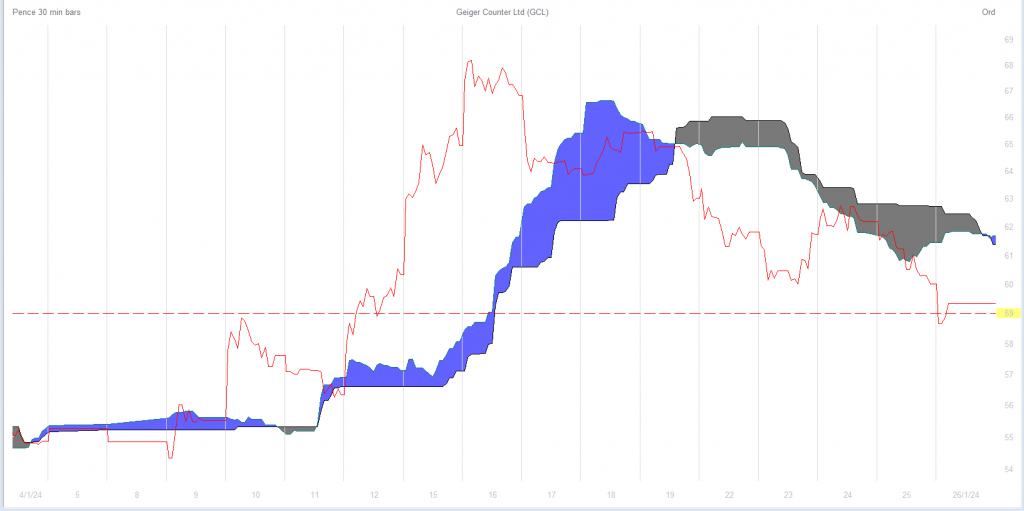

That leaves three newbies to report. In third, uranium investor Geiger Counter (GCL) (+17%). Strong share price run can be traced back to 11 January. No news out from the company, but take your pick in terms of uranium news out round about that day: the UK Government announced Biggest expansion of nuclear power for 70 years to create jobs, reduce bills and strengthen Britain’s energy security – Roadmap sets out how UK will increase nuclear generation by up to 4 times to 24GW by 2050; Reuters reported Saudi Arabia plans to use domestic uranium for nuclear fuel, and the Financial Times wrote a piece titled Uranium prices could power on after largest producer warns on supply. Small wonder that uranium prices have been well bid recently.

In fourth, Aquila European Renewables (AERI) (+12.6%). Shares still feeling the positive effects of December’s news that it has “…received unsolicited proposals from ORIT in relation to a possible combination on a to be defined formula asset value for formula asset value basis.” For ORIT read Octopus Renewables Infrastructure Trust. Finally, Foresight Sustainable Forestry (FSF) is in fifth (+12.4%) – the ongoing share buyback programme working its magic it seems.

Scottish Mortgage Watch: -4.5%

Scottish Mortgage’s (SMT) monthly share price loss as at Friday 19 January 2024 – last week the shares were up +2.9% on the month. Similar story with NAV – down -3.6% compared to the previous week’s +1.3% monthly gain. The wider global IT sector managed to finish down by only the tiniest of margins (-0.1%), although that was still a noticeable reduction on +2.6% seven days earlier.

THE CORPORATE BOX

Combination Watch: Custodian Property Income REIT (CREI) & abrdn Property Income (API)

Announced “that they have reached agreement on the terms and conditions of a recommended all-share merger pursuant to which CREI will acquire the entire issued and to be issued share capital of API…Under the terms of the Merger, Scheme Shareholders will receive: for each Scheme Share, 0.78 New CREI Shares…”

Comment from API Chair James Clifton-Brown: “Over the years, API’s manager, abrdn Fund Managers, has assembled an attractive portfolio on the company’s behalf, with a weighting to more favoured areas of the market, a diversified tenant base and a focus on ESG…The Merger will enable API Shareholders to retain exposure to the portfolio and its growth prospects at a significant premium to API’s share price, with the prospect of superior share liquidity and an enhanced and fully covered dividend. The API Board believes that, with increased scale and an enhanced capital structure, the Combined Group will be well positioned for the future.”

Borrowing Watch: 2.7%

The cost of borrowing at Bankers Trust (BNKR): “The £15 million 8% Debenture Stock matured on 31 October 2023 and was repaid in full…Following repayment of the debenture, the Company’s overall cost of borrowing has fallen to 2.7%, in line with the dividend yield on the portfolio.”

Dividend Watch: 17.6%

The increase in Tufton Oceanic Assets’ (SHIP) annual dividend target to $0.10 per share. Comment from Liberum: “…the percentage increase in the dividend, reflecting a yield of 10.0%, is one of the highest across alternative funds over the past year. The increase in the target dividend reduces the prospective dividend cover marginally, from 1.6x to 1.5x.”

6.02p – the new full year dividend target at Octopus Renewables Infrastructure Trust (ORIT): “This increase of 4.0% over FY 2023’s dividend target is in line with the increase to the Consumer Price Index (CPI) for the 12 months to 31 December 2023, and marks the third consecutive year the Company has increased its dividend target in line with inflation. The FY 2024 dividend target is expected to be fully covered by cashflows generated from the Company’s operating portfolios.”

57 – the number of consecutive years Bankers’ (BNKR) payout has increased: “The Board is…recommending a final quarterly dividend of 0.66p per share, resulting in total dividends per share for the year of 2.56p (2022: 2.328p), an increase over last year of 10%…This will be the Company’s 57th successive year of annual dividend growth. For the current financial year, the Board expects to recommend dividend growth of at least 5%, which would equate to a full year dividend of 2.69p per share.”

MEDIA CITY

Tip Watch #1: This stock survived a backlash – and now it’s about to deliver

The stock? Impax Environmental Markets (IEM). The backlash? According to the above Questor article in The Telegraph: “Sceptical investors have pulled money out of funds investing on environmental, social and governance (ESG) grounds…the backlash in which investors withdrew almost £3.7bn from ESG funds in April-November last year has proved difficult for a £1bn global investment trust focused on companies contributing to a green, zero-carbon economy.” ‘£1bn global investment trust’? Enter IEM. According to Questor, “More than half its assets are invested in waste management, energy efficiency and water infrastructure, with the remainder split across alternative energy, sustainable agriculture, transport and digital technology providers…the trust’s fund manager…says that for each $10m (£7.9m) invested in the strategy, enough clean, renewable energy is generated to power 360 homes and the equivalent of 1,410 households’ water consumption and 240 tonnes of domestic waste are saved.”

And yet… “after two difficult years following the tech stock surge in the Covid pandemic, investors have not done well. The trust trails its benchmark, the FT Environmental Technology (ET) index, over all time periods – although since launch the gap is narrow, with an average underlying investment return of 7.6pc a year, just behind 7.8pc from the index…” Questor, however, believes “The outlook is more positive, particularly as the shares have fallen 9pc below the value of the trust’s 63 investments. The discount is double the 5pc average of the past year and makes the shares cheap in contrast to November 2021 when the shares peaked at 576p to trade above Nav…”

Questor adds: “To be fair, that the shares have tumbled…has less to do with ESG controversies and reflects the toll rising interest rates took on its collection of medium-sized and smaller growth companies…Any cut in interest rates will…reassure investors about the returns that solar and wind projects can make, while over-stocking pressures that have blighted the solar and natural ingredients sectors should ease…With the trust buying back its shares and the fund managers recently making a ‘material’ increase in their personal stakes, it’s time for investors to follow suit and back a fund about to deliver on its good promises.”

Tip Watch #2: Why I’m buying smaller companies

That’s the title of John Baron’s latest Investors Chronicle piece. Baron starts his article with a little context: “Last year was another challenging year for the investment trust investor. It is still the case that discounts on average remain at their widest since the financial crash of 2008-09…Of the categories that underperformed, the extent to which sentiment trails the fundamentals is perhaps at its most pronounced in the smaller companies sector. As we enter 2024, this sector is set to have its moment in the sun.”

Why? Well, firstly “An overweight exposure to smaller companies has been one of the more reliable investment strategies in generating higher returns over time, relative to the wider market…There is an inherent logic to this. Elephants do not gallop. Many smaller companies operate in niche and growing markets, are nimble and exhibit faster growth in part because they are benefiting from the advance of technology. This is not just helping to reduce costs and open new markets, but is better enabling them to embrace the disruptive practices needed to compete with their larger brethren. There is no reason to suggest this will not continue over time.” But, as Baron points out, “…investors need to be invested for the long term to capture this smaller company outperformance. The fact they exhibit greater volatility can then be embraced as an opportunity. This is such a moment.”

That’s because “Recent analysis by MSCI of US equity returns over the past 70 years show smaller companies usually perform strongly immediately after a recession. On each occasion, they have performed better than larger ones by a margin on average of over 15 per cent during the following year – again reflecting their ‘nimbleness’ when responding to the changing economic environment. Although global economies have tended to avoid recessions, slowing growth rates and perhaps modest ‘technical recessions’ of two negative quarters of growth should usher in something of a rebound from which these companies should particularly benefit.” Baron goes on to highlight four funds:

Mercantile (MRC): “The company has a solid and consistent track record of outperformance of its benchmark (the FTSE All-Share ex FTSE 100 and investment companies) over both the short and long term, while the current level of payout equates to a yield of 3.5 per cent when bought. Confidence in the future is perhaps illustrated by the management nearly doubling the company’s gearing to c14 per cent recently. Significant in-house resource adds to the investment case.”

Smithson (SSON): “The manager seeks to take advantage of the often greater disconnect between sentiment and fundamentals in this segment of the market, which is down to there being less research available. The company has performed well relative to the MSCI World SMID (£) index.”

Scottish Oriental Smaller Companies (SST): “The universe of smaller companies in Asia has come a long way in recent decades and is now much larger, with longer listed track records and the regulations protecting minority shareholders better established. This is providing a more favourable hunting ground for experienced stockpickers, and is reflected in the managers overseeing a higher-conviction portfolio than has historically been the case. Meanwhile, valuations are more attractive than they have been for a while.”

JPMorgan UK Smaller Companies Investment Trust (JMI): “…boasts a long-term asset performance that is among the best in its peer group…should the proposed merger with JPMorgan Mid Cap Fund (JMF) proceed, the company will introduce an enhanced dividend policy, which will target a 4 per cent yield (of NAV) as at the end of the preceding financial year.”

A 360 view of the latest results from USA, JEMA, TIGT, IAT, CCJI

Find out which investment company was created over a drink in a Wiltshire pub back in 2015 in the latest Weekly 360 round-up of results and commentary from the investment company space…

By

Frank Buhagiar

Doceo

Tribute of the week

“‘The big money is not in the buying and the selling, but in the waiting’, Charlie Munger. It feels only fitting to begin this Interim Report with a Mungerism. In part to mark the passing of a legendary investor but also to highlight its timeless relevance. The waiting, or a willingness to be patient, is an underappreciated skill set in investing.” Baillie Gifford US Growth (USA) Interim Management Statement.

Feels like a dream opportunity

Share price outperformance for Baillie Gifford US Growth (USA) over the latest six-month reporting period. According to the Interim Management Statement: “…the Company’s share price and NAV (after deducting borrowings at fair value) returned 12.3% and 4.1% respectively. This compares with a total return of 7.9% for the S&P 500 Index…(in sterling terms).” The statement goes on to remind readers that “We have a long-term approach and would ask shareholders to judge performance over periods of five years or more.” The investment managers add: “While share prices have shown strength over the past year, we continue to see opportunity in the dislocations between stock prices and the underlying valuations of companies. Future cash flows and earnings drive value, and a fundamental pillar of our investment philosophy is that price reflects value in the long run. However, price is driven by mood, momentum and broader sentiment in the short term, creating opportunity.”

The outlook kicks off with an admission: “When fundamentals will be better reflected in share prices is nigh on impossible to predict. Trying to predict the mood of the multitude of market participants is a fool’s game for the long-term stock picker. Instead, we must double down on what differentiates us – long-term, active, growth, bottom-up stock pickers focused on fundamentals. British physicist David Deutsch said, ‘We have a duty to be optimistic. Because the future is open, not predetermined and therefore cannot just be accepted: we are all responsible for what it holds’. We take that responsibility seriously. US Growth holds companies which are determining that future. But it will take time. Navigating storms is part of the process. We believe the portfolio is well-positioned to navigate and realise its potential. That feels like a dream opportunity.”

Numis notes: “Performance has improved in recent months, and although NAV total returns lagged the benchmark during the six months to November, it has outperformed post-period end. This is partly due to increased expectations of a Fed pivot…The fund has produced NAV total returns of 112% (13.7% pa), compared with 125% (14.9% pa) for the S&P 500 since its inception…Baillie Gifford US Growth is differentiated from its peers by a focus on disruptive growth stocks and the ability to invest up to 50% of the portfolio in unquoted securities, (31% of total assets at 31 December). The focus on high growth companies, in line with Baillie Gifford’s typical approach, means that the portfolio looks very different to any index. As a result, we would expect periods of significant out and underperformance versus the benchmark, which has been demonstrated since launch, and as the managers’ stress, investors need a long-term time investment horizon.”

Weather forecast of the week

“It has been a better year. The storm is easing. We know we cannot assume that the sun will always shine, but we take comfort from the fact that the companies held in your portfolio are executing, and executing well.” Baillie Gifford US Growth (USA) Interim Management Statement.

A tilt towards value and income

First set of Finals from JPMorgan Emerging Europe, Middle East & Africa (JEMA) (formerly JPMorgan Russian Securities) since the investment objective (and name) change. As Chairman Eric Sanderson explains: “The operations, control structures and trading of securities under the new investment objective and using the Company’s new name were completed and commenced in the first half of this reporting period. The…completion of this process allowed the Company to commence measurement of the performance of its portfolio against its new reference index, the S&P Emerging Europe, Middle East & Africa BMI Net Return in GBP on 1st March 2023.” So, how has the fund performed? “…in the eight months…to 31st October 2023 the Company’s net asset value increased by 2.2%, an out-performance of 1.9% against the reference index…On a share price total return basis, the Company returned 10.0%…”

As for what’s in the new portfolio: “The Company’s new investments acquired in this reporting period are considered to be in high quality companies, with a tilt towards value and income and a focus on maximising total return for shareholders. The new investments have also changed the portfolio’s geographical focus with Saudi Arabia, South Africa and UAE representing 31.7%, 23.8% and 14.2% of the portfolio respectively…With little prospect of Russia’s invasion of Ukraine being resolved in the foreseeable future or limiting of the existing strict economic sanctions, the Company’s new investment objective at least helps the Company steer through this very difficult period. Although cognisant of the Company’s continuing holdings in Russian companies, the challenge for the Board is to use the new investment objective to grow the Company’s assets in a way that promotes the success of the Company for the benefit of the members as a whole.”

Winterflood writes: “JEMA will continue to participate in corporate actions regarding its Russian holdings…The Board noted that some institutions have identified sanction-compliant methods to sell Russian holdings at a substantial discount and will consider such actions where permissible and beneficial for shareholders.”

Numis adds: “…it is positive to see a period of outperformance, however we suspect that investors will be more focussed on the status of the Russian holdings, which are currently being valued at a nominal value. We note that Baring Emerging EMEA Opportunities, which also had Russian exposure prior to its invasion of Ukraine, has recently realised two of its Russian holdings which were held through global depositary receipts and is considering possible structures to enable it to separate Russian assets. The board of JEMA notes that the manager is considering its options with respect to its Russian holdings…There is currently c.£24m derived from dividend/tender proceeds held within the custody ‘S’ account…and an easing of sanctions/restrictions may unlock this value but ultimately it is extremely difficult to determine if or when this may occur.”

FAQ of the week

“We are often asked what the catalyst might be for a reversal of fortunes for UK equity valuations. We do not claim to have a good answer to this. That being said, and heading into a UK election year in 2024, we are hopeful that better long-term political thinking and prioritisation towards our home equity market will emerge.” Troy Income & Growth Trust (TIGT) investment managers.

UK equity valuations are compelling

Could this be the final set of Finals from Troy Income & Growth Trust (TIGT)? Will be if the proposed merger with STS Global Income & Growth Trust (STS) gets the green light from shareholders. In the meantime, according to Chair Bridget Guerin: “The Company delivered a…NAV…per share total return of +6.6% and a share price total return of +6.3% over the year to 30 September 2023. Over the same period, the FTSE All-Share Index produced a total return of +13.8%…The two most significant drags on performance were some of the Company’s holdings in large, low cyclicality Consumer Staples companies and the two holdings in the Materials sector. Sterling’s strong appreciation against the dollar was also a headwind, impacting the Company’s small number of US-listed holdings as well as the predominantly overseas earnings of the portfolio as a whole.”

Looking ahead, the Chair writes: “In the coming year, the UK market is likely to continue focusing on the path of interest rates, inflation, and the related impacts on corporate and consumer health. The Managers expect continued pressure on earnings, which resulted in a decline in aggregate UK dividends in 2023. In this environment, the Board sees clear virtues in an emphasis on quality, low cyclicality business models that can fund growing, comfortably covered dividends and we remain optimistic about this investment style for the future.” The investment managers point out that: “Despite our caution on near-term earnings, we believe that UK equity valuations are compelling. The UK is home to various world-class businesses and over the past year we have found exciting valuation opportunities on offer. These have been across a range of sectors and has resulted in six new holdings. We believe the Company has a strong portfolio and a high-quality list of potential stocks – we are well placed to take advantage as further opportunities arise.”

Winterflood writes: “TIGT has agreed terms for a proposed combination with STS Global Income & Growth (STS). If approved by each fund’s shareholders, this will result in the voluntary liquidation of TIGT and the rollover of its assets into STS in exchange for the issue of new shares of STS (on a FAV for FAV basis). Underperformance was a result of specific stock price movements, as well as the fund’s quality-orientated investment style, which faced headwinds compared to more value-orientated styles. Sterling’s appreciation against the dollar was also a headwind.”

Description of the week

“The investment backdrop during the past 12 months can be well summarised as ‘unsettled’.” Troy Income & Growth Trust (TIGT) full-year Manager’s Review.

Paid to wait

Half-year Report from Invesco Asia Trust (IAT). Chairman Neil Rogan has the numbers: “After a strong run of outperformance the Company’s NAV total return over the six months to 31 October 2023 of –5.9% was below our benchmark (MSCI AC Asia ex Japan Index) total return of –2.9%. The share price total return was –7.8% with the discount widening from 12.4% to 14.2% over the period.” But, “Despite the short-term underperformance, the NAV and share price performance remains superior to that of the benchmark index over one year, three years, five years and ten years…” And as the Chairman explains, the fund is currently something of an income play too: “A half-yearly dividend of 7.20p was paid on 23 November 2023 in accordance with our policy of paying two dividends over a year amounting to approximately 4.0% of NAV. This puts the annual dividend yield on the share price at 5.0%, based on the share price of 296.00p at 31 October 2023.”

In terms of outlook, it’s all about winds. Firstly, “Headwinds remain: China’s recovery is being hampered most notably by property oversupply and bad debts. Persistent inflation in the United States has led to American interest rates being higher for longer, which puts pressure on Asian currencies. Monetary tightening in the US and Europe will…further negatively reduce demand for Asian exports…” Then tailwinds, “The surprising thing is that favourable tailwinds have not yet appeared. There is the possibility of a rapprochement between the US and China…Dollar interest rates and US bond yields are close to peaking…Asian corporate governance is much stronger these days, so many companies can prosper even through harsh times. Asian economies are more resilient than in previous cycles…” And what if there is no wind at all? “If we are becalmed for a time, the dilemma becomes should you invest now or buy after things improve? If invested in Invesco Asia Trust, we would argue that you are paid to wait. Not only are the valuations of the underlying investments at unusually attractive levels but you have the double discount of the share price relative to the net asset value. On top of this comes a 5% annual dividend yield…”

Winterflood points out: “Exposure to China/Hong Kong was key detractor, alongside India underweight (now -7%). Stock selection elsewhere contributed, particularly in Korea and Taiwan. The managers believe that ‘the upside risk is now greater than the downside risk’ for Chinese equities. Lead manager Ian Hargreaves and deputy manager Fiona Yang will swap roles from 1 May 2024.”

Summer memory of the week

“One summer’s day back in 2015, conversations with Richard Cardiff in a Wiltshire pub, led to the creation of the Company.” CC Japan Income & Growth (CCJI) Chairman Statement.

Strong

That’s how Chairman Harry Wells described CC Japan Income & Growth’s (CCJI) full-year performance: “I am delighted to report a year of strong performance to 31 October 2023…NAV…total return of the Company which includes income, increased by 18.9% in sterling terms. The Share price, again measured by total return, rose 20.9%. This represents significant outperformance against the TOPIX Total Return Index, which rose 12.0% in sterling terms during the year.” And the outperformance is no one-off: “Since launch in December 2015 until the recent financial year end, the Company’s NAV total return, including dividend distributions, recorded a 117.4% increase, continuing to outperform the sterling adjusted TOPIX total return index, which rose 77.0%.”

And the Chairman believes there more to come: “Despite decent returns over the last decade, the Japanese equity market remains undervalued. The earnings yield dwarfs the negative return from cash. The Government and The Tokyo Stock Exchange are committed to cleaning up capital inefficiencies and boosting returns on equity. Companies are being forced to change their behaviour. TOPIX listed companies are still sitting on considerable amounts of cash estimated at the yen equivalent of over US $1 trillion. This should steadily be reduced through increasing shareholder distributions, share buy backs, management buyouts…and private equity deals…For now, BOJ monetary policy remains uniquely accommodating compared to other major Central Banks…Forecasts for corporate earnings growth are healthy…” And if that’s not enough, while “World equity markets tend to take a lead from the policy actions of the US Federal Reserve…Japanese equities now stand out on their own merits.” The result? “Our mandate is well placed to continue to provide solid total returns…”

Comment from Winterflood: “The Board ‘remains alert to any opportunities that could arise which could be incremental to our market capitalisation’, noting the ‘increased trend of consolidation within the investment trust industry not least the Japanese sectors’.”

i share FTSE whilst factual, if u bought 2/1/2013 the return

of 92.67% is more indicative, with the paid out yield.

Only a basis for DYOR

Remember the chart is in u$

As always it’s about timing and then time in.

Cleary retracing, will it reverse. ? If u took some money off the table

u would be looking for an opportunity to re-invest.

© 2026 Passive Income Live

Theme by Anders Noren — Up ↑