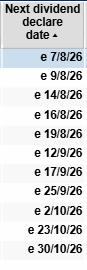

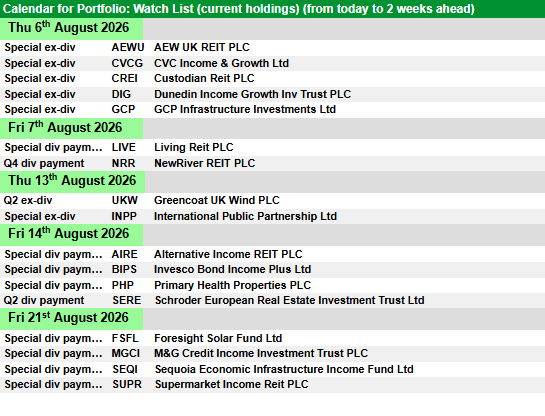

Below are the estimated xd dates for the SNOWBALL.

I prefer not to detail the holdings in the SNOWBALL as your snowball should be different to the SNOWBALL as it’s dependent on the number of years before your drawdown date.

The current target is to earn blended income of 1k a month which the SNOWBALL will earn this year but next year it’s doubtful that figure will be equalled.

Could your pension last to your 100th birthday? Here’s how

Friday, July 31, 2026

Sarah Coles

Related news

The number of people aged 100 or more has doubled over the past 20 years, raising the point that as life expectancy continues to grow so to must our pension calculations.

According to the latest government figures, there were 15,172 people who were at least 100 years old, two thirds of which were women.

When you’re planning for retirement, it’s easy to consider your own parents or grandparents as a benchmark, and assume you’ll live roughly as long.

However, this could mean you vastly underestimate how long you’ll live for – and how long your retirement income needs to last. This means that we all need to consider how we would keep paying the bills if we lived longer than average.

Let’s do the pension math’s

The first step is to use a pension calculator to see what you may be able to build by retirement and how long the income is likely to last. If there’s a shortfall, it’s worth considering boosting your pension contributions, planning for a longer working life, or rethinking your income expectations in your later years.

Most of these calculators will give you the option of factoring in the state pension. It’s worth doing the calculations both with and without, to see where you stand.

Nobody is suggesting that the state pension will disappear, but there’s always the chance the state pension age will rise or the triple lock will be replaced. When you’re forecasting so far ahead, you can’t guarantee state benefits will remain completely unchanged.

How you take retirement income matters

Drawdown offers real flexibility over how much you take from your pension, and when. It also gives you the opportunity to leave the pot invested for more growth throughout your retirement.

Plus, when you die, you can leave any unused pot to your family. However, as retirements get longer, it will be essential to ensure the money doesn’t run dry if you make it into your 90s or beyond.

It’s worth using an online drawdown calculator to see whether the withdrawals you want to make are likely to be sustainable. However, this can only ever be based on estimates, and you’ll face what’s known as sequencing risk.

This is where disappointing investment performance in the early years, coupled with larger withdrawals, can mean your pension doesn’t last as long as you had expected.

One way around this is a variable withdrawal strategy. The idea is to determine how much you can afford to withdraw from your pension in any given year – weighing up things like how the fund has performed, the value of the portfolio and your remaining life expectancy.

The idea is to adapt to market performance, so at times of market losses, you don’t end up eating into the capital. Then at times of better performance, you can afford to dip further into your funds.

This strategy can be complicated, so you may want to seek out some formal financial advice. Alternatively, some people will opt for a hybrid approach, with higher and lower limits over how much they take from the pension, based on performance and income needs. Others will opt to take a fixed percentage of the pot, but will revisit it regularly to make sure they’re not eroding their pot.

A variation on this theme, which can work for those with large pension pots, is to take just the natural yield from your investments. This is where you take the income from dividends produced by your investments, so you don’t eat into the capital itself.

This means the pot continues to grow and has the potential to keep up with inflation. You will need a substantial pot, with enough savings and investments elsewhere to give you flexibility over how much income you can take, but it’s a great way not only to protect an income for life, but also to give you flexibility if you need to dip into the pot for care needs.

If you opt for an annuity, you will have an income for life – regardless of how long you live. However, with a longer retirement it will be particularly important to consider inflation.

Prices in general have more than doubled in the past 30 years, so you need to understand the impact on your quality of life. You can opt for an inflation-linked annuity to overcome this, but you need to accept that the initial income will be much lower.

Taking the annuity route offers certainty, but it removes flexibility over how much income you can take, so you also need to think about how you would cover the cost of any one-offs, like adapting your home as you get older or replacing your car. It’s one reason why people often combine annuities and drawdown, either at the same time or at different stages of life.

2026 has so far seen an improvement for UKW on a number of metrics.

William Heathcoat Amory

Updated 30 Jul 2026

Disclaimer

Disclosure – Non-Independent Marketing Communication

This is a non-independent marketing communication commissioned by Greencoat UK Wind (UKW). The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

The first half of 2026 has been a positive period for UKW, supported by strong cash generation and a modest increase in NAV. Total shareholder return for H1 2026 was +9.2% (or +4.4% based on NAV), with dividends contributing to the majority of that return.

UKW’s NAV increased modestly by 0.6p per share over the period, reflecting the conversion of strong operational performance into cash. Net cash generation for the period was ahead of budget at £221.6 million, resulting in dividend cover of 1.9x for the period. This derives from electricity generation of 3,003 GWh, being 4.9% above budget, as well as favourable realised power prices. Net cash generation is now on course to be towards the top end of the £350-410m guidance for 2026.

The share price discount to NAV, which has not appreciably narrowed over the period, does not in the Board’s view reflect the strength of the business. The discount persists mainly due to macroeconomic and sector-wide pressures, including higher interest rates, policy uncertainty and an oversupply of listed renewable infrastructure vehicles. We are beginning to see some of these pressures ease, notably with the shrinking of the listed renewable trust sector. At this year’s AGM, 97.1% of shareholders voted for the continuation of the company.

Over the interim period, UKW refinanced £200m of 2026 debt maturities with new long-dated facilities provided by its existing lending group, with maturities now extended across 2032-34. The continued ability to place long-term debt demonstrates the durability of UKW’s financing model and the strength of its relationships with lenders.

UKW’s Board retains a clear approach to capital allocation, prioritising dividends alongside reinvestment of excess cash. The board has a 2026 dividend target of 10.7p per share, the thirteenth consecutive inflation linked increase. Beyond the dividend, the Group has also continued to strengthen its balance sheet, and has repaid £53.5m of debt during the period. Looking ahead, the Board continues to emphasise the importance of reinvestment to further sustain the Company’s dividend over the long term; renewable infrastructure assets are inherently finite, and maintaining the long term cash generating capability of the portfolio requires ongoing reinvestment. In this context, the Investment Manager has continued to evaluate a range of opportunities on behalf of the Company, with a focus on selective transactions that enhance risk adjusted portfolio returns.

Lucinda Riches, Chairman of UKW, commented “The outlook for UK wind remains attractive…as one of the largest owners of operational UK wind farms, UKW’s portfolio is well positioned to continue delivering both secure electricity and long-term cash flows for shareholders.”

Kepler View

2026 has so far proved to be significantly more positive for Greencoat UK Wind (UKW) than 2025, and we note an undercurrent of quiet confidence from the manager’s presentation for the interim results. UKW has a simple model, which puts the trust in a strong position to be a survivor over the short term, and over the long term a valuable constituent of diversified portfolios – for institutions and retail investors alike. UKW’s long standing attributes that underpin its position are that the trust is an attractive proposition at scale (gross assets of c. £5bn), it has a self-sustaining financial model ( long term dividend cover of 1.8x forecast over 2027-31), and that there is low execution risk in the trust continuing to deliver returns into the future, given the strategy is to keep doing what the trust has done for the past 13 years, and does not require a transformational pivot to continue to deliver for shareholders.

Fundamentally, UKW’s proposition remains faithful to its original design, having paid a covered, inflation-linked dividend for the last 13 years. Dividend cover is the key to UKW’s attractions in our view, given it gives the board so much flexibility to deploy capital to the advantage of shareholders. With net cash generation +36% for the six months to 30/06/26 over the same period last year, dividend cover has significantly improved (1.9x for the six months to 30/06/26). Responding to higher energy prices, the managers locked in 20% of annual electricity production for the year ahead at the interim stage, meaning that around 66% of UKW’s revenues for the remainder of the year are now fixed. The team commented that since the half year end, prices for a further 10% of production had been subsequently locked in, mainly in 2027. The managers note that this is not a change in policy, but more a tactical move taking advantage of higher prices. In our view, this should give confidence to shareholders that the target dividend for the year is effectively ‘in the bag’, and that for the full year, there will be significant excess cash for capital allocation.

The team have guided their expectations are that UKW should throw off c. £120-180m of surplus capital for the current financial year. In terms of uses of this capital, we understand that the board and manager are focussed on disciplined reinvestment which is key to delivering long term cashflows to shareholders, having already repaid £30m of the RCF. UKW’s gearing, at 41.7% is marginally higher than the board’s sub-40% target. The successful refinancing of maturing debt is good news for shareholders, and the team highlight that they expect further refinancing activities will be announced later this year. Progressive debt reduction is one source of surplus cash, but with c. £45m re-paid each year from the Hornsea 1 specific loan, the team suggested achieving the sub-40% target may be a medium-term feature, reached through debt repayments but also through re-investment in the asset base to grow the GAV.

UKW’s target dividend yields 9.8% at the current share price. The portfolio discount rate, less annual charges, implies a NAV total return of c 10.7% per annum. As with any investment there are risks that anticipated returns will not be achieved, and one specific risk for UKW shareholders is the threat of politics. That said, with an anticipated doubling of electricity demand to 2050 (NESO Future Energy Scenarios 2025), wind farms are well positioned to make a strong contribution to an increase in supply, being lower cost and emitting zero-carbon at the same time. Any UK government must in our view be careful not to frighten off private capital, which is key to delivering transformational change for voters.

UKW is projected to have c. £1bn of surplus capital available to invest over the next five years, and so the trust could be a meaningful participant in helping to meet the UK’s future energy demands. At the same time, shareholders stand to benefit from any future price spikes caused by geopolitical instability, which the managers observe is becoming an increasing feature of markets. In this regard, UKW potentially offers an appealing package from a portfolio context: the prospect of attractive returns from a base-case scenario, potentially also offering a hedge to energy price rises in the future. With the shares trading on a discount to NAV of c 18% and corporate activity continuing within the sector, a further narrowing of the discount cannot be ruled out.

GCP Infra (LSE:GCP) reported a net asset value (NAV) of 98.60 pence per share as of 30 June 2026, supported by a diversified portfolio of 47 infrastructure investments with a combined value of £810.4 million. The portfolio delivers a weighted average annualised yield of 8.0% and has an average remaining life of 11 years, with many assets benefiting from partial inflation-linked income.

The company also confirmed that its online investor portal has been updated with the latest quarterly valuation data, giving shareholders greater transparency into the composition and performance of the portfolio.

Capital Recycling Enhances Liquidity

During the period, GCP Infra continued to strengthen its financial position through a series of capital management initiatives. Borrowings under its revolving credit facility were reduced from £24.0 million to zero, while the company repurchased more than 19 million of its own shares, leaving it with only a modest level of net debt.

The investment company also completed several portfolio optimisation transactions, including introducing third-party financing into its solar assets, which generated approximately £40 million in additional cash. It further completed the sale of an anaerobic digestion project and two onshore wind assets at prices above their previous carrying values, improving liquidity while crystallising value for shareholders.

Stable Financial Position Supports Outlook

GCP Infra’s outlook continues to be supported by a conservative balance sheet, improving cash generation and favourable technical market indicators. These strengths are complemented by shareholder-friendly capital allocation policies, including share buybacks and a stable dividend.

However, revenue trends have been mixed in recent periods, while the company’s valuation remains relatively demanding despite its attractive dividend yield. Even so, management believes the portfolio’s defensive characteristics and disciplined capital management provide a solid foundation for long-term returns.

About GCP Infrastructure Investments Ltd

GCP Infrastructure Investments Ltd is a FTSE 250-listed closed-ended investment company focused on infrastructure debt and related assets across the UK. Its portfolio primarily consists of projects backed by long-term public sector or availability-based revenue streams, with many investments offering partial protection against inflation.

The company has also been awarded the London Stock Exchange’s Green Economy Mark in recognition of the positive environmental contribution of its investment portfolio.

This article was written by the editorial team at InvestorsHub/ADVFN and is provided for informational purposes only.

Aberforth Smaller Cos Trust PLC ex-dividend date AEW UK REIT PLC ex-dividend date Custodian Property Income REIT PLC ex-dividend date CVC Income & Growth EURO Ltd ex-dividend date CVC Income & Growth GBP Ltd ex-dividend date Dunedin Income Growth Investment Trust PLC ex-dividend date EJF Investments Ltd ex-dividend date GCP Infrastructure Investments Ltd ex-dividend date Global Smaller Cos Trust PLC ex-dividend date Marwyn Value Investors Ltd ex-dividend date Monks Investment Trust PLC ex-dividend date Murray Income Trust PLC ex-dividend date Northern Venture Trust PLC ex-dividend date Polar Capital Global Healthcare Trust PLC ex-dividend date

Dividend heroes vs enhanced income: which approach is best?

Faith Glasgow compares two different investment trust approaches that look to appeal to income-seekers, particularly those approaching or in retirement.

29th July 2026

by Faith Glasgow from interactive investor

You might be approaching retirement and looking for an income stream, or keen to take a more “total return” approach to investing that incorporates dividends as well as capital gains; either way, investment trusts are a natural choice of collective investment.

That’s partly because of their listed company structure, which allows them to withhold some of the dividend distributions they receive from underlying companies and build up reserves; these can be used to supplement payouts to shareholders in years when there’s a shortfall of “natural” dividend income.

But it’s also because trusts are allowed, if they wish, to finance distributions from capital gains as well as natural income (and reserves). That ability has become increasingly popular with investment trust boards over the past decade or so, as trusts have become more attractive and accessible to retail investors managing retirement portfolios.

Some boards have taken the opportunity to introduce policies that will give shareholders greater certainty in regard to the income they can expect. This may involve trusts dipping into capital if necessary to meet their income ambitions.

and Murray International Ord MYI have no target yield but simply aim to keep annual dividend growth ahead of inflation.

At the same time, there’s a high-profile movement led by the Association of Investment Companies (AIC) in the shape of the “dividend heroes” – the rising number of trusts that have chalked up 20 or more consecutive years of dividend growth.

The longest-running heroes have almost 60 years of growing dividends under their belts. The AIC has further encouraged the trend with the “next generation” dividend heroes – those with between 10 and 20 years of payout growth.

Dividend hero status is highly prized, and trusts that achieve it are unlikely to cut a dividend if they can possibly avoid it, so investors in those trusts can feel pretty sure of continuing growth in distributions in the coming years.

However, both approaches to improving income security have their critics.

So, what are the pros and cons of each, and which strategy do the experts ultimately favour?

Enhanced dividends: ‘robbing Peter to pay Paul’?

The big plus about an enhanced dividend policy is that it frees up fund managers to invest in the best stocks for total returns, even if they have a low or no yield, rather than having to restrict themselves to those paying decent distributions.

Emma Bird, head of investment trust research at Winterflood, argues that the capacity to deliver “a higher level of income from an unconstrained investment approach” may in turn stimulate a benign investment circle. “It can help to attract new investors, which can support the fund’s rating.”

She points to JGGI as a good example of a successful enhanced dividend approach that has broadened the trust’s appeal for private investors. It pays out at least 4% of NAV a year, “while the investment approach remains unconstrained and style-agnostic, which has helped the fund to generate alpha in a range of market conditions”.

For Thomas McMahon, head of investment company research at Kepler Partners, such a policy really comes into its own across sectors that don’t traditionally pay dividends.

“For instance, investors can now draw an income while being invested in biotechnology, smaller companies and private equity, so the possibilities for diversification and generating growth as well as an income have expanded,” he explains.

trust, is among those who have criticised enhanced dividend policies as “robbing Peter to pay Paul” – effectively dipping into the capital gains prized by growth investors to ensure generous payouts for income seekers.

This could therefore deter growth investors, although James Carthew, head of investment company research at QuotedData, argues that it’s not an insurmountable issue if a dividend reinvestment plan is in place to enable them to roll up their gains within the trust.

McMahon makes the additional point that the process of moving away from an equity income strategy could in itself be a negative. “Equity income investing involves identifying some highly attractive characteristics: companies which can generate spare cash and grow that spare cash consistently could be attractive investments, particularly for those who are looking for steady compounding growth.”

There is therefore much to be said for a traditional approach in markets with a decent, diversified spread of high-yielding stocks, he suggests.

Bear market challenges

There are undoubtedly potential drawbacks to the enhanced dividend approach in some market conditions. The UK hasn’t seen a sustained bear market for a long time, but Carthew warns that “there are plenty of reasons why we might be approaching one”.

As Bird points out, an enhanced dividend policy in such a scenario would result in “either a reduction in dividends (based on a lower NAV) or a need to sell more holdings at lower prices to maintain or grow distributions”. That’s far from ideal, especially for growth-oriented shareholders.

An associated risk is that the sort of growth sectors that don’t pay dividends (but might be favoured for an enhanced dividend approach) may be more volatile and therefore lose more in falling markets. Income investors accessing these areas through trusts with enhanced dividend policies “need to think about their attitude to risk”, warns McMahon.

Dividend heroes: low yields and token increases?

The dividend heroes concept is a great piece of marketing and a valuable tool for investors to assess the likely reliability of a trust’s income stream.

As Bird explains: “We would expect most boards classified as dividend heroes to be keen to demonstrate their commitment to continued regular dividend growth, and to utilise revenue reserves when necessary to maintain this record as far as possible.”

However, one grumble around heroes is the fact that some have made only minimal increases to dividends in recent years, thereby ensuring their status is maintained but certainly not providing investors with inflation-beating income.

For McMahon, this could actually be a benefit rather than a detraction, as it indicates prudent housekeeping. “One justification for investing in dividend-paying stocks is that a regularly increased dividend is a sign of a well-run company. The same could be said of some of the investment trusts which make small increases each year,” he suggests.

Carthew agrees tokenism is a risk, but he too points to contrary arguments that indicate management strength, even at the expense of dividend hero status. “Temple Bar Ord TMPL

is a good example of the opposite stance,” he says. The trust cut its dividend to a more manageable level when management was taken over by Redwheel in 2020, losing its status as a dividend hero.

“But that move gave the managers more flexibility to buy recovery stocks on low to no yields. The reward has come in great performance and a rising dividend that surpassed the previous peak some time ago.”

In Bird’s experience, most dividend hero boards – certainly those with an income mandate – in practice “recognise the importance of delivering dividend growth ahead of inflation over the long term”.

Another, arguably more pervasive, concern is that uninformed investors may be confused by the fact that dividend hero status is based on growth rather than yield. Four of the 20 current dividend hero trusts yield under 2%, while eight of the 30 next generation heroes are yielding less than 3%.

In effect these are trusts with a focus on capital growth or total returns that are making modest but rising distributions to shareholders.

as a particular example. “It has 44 consecutive years of dividend growth, but its investment approach is purely focused on investment in growth companies, and its dividend yield currently stands at just 0.3%,” she points out.

That’s fine, so long as you understand that you’re buying long-term growth and a small but secure payout, not an income-oriented investment.

Importantly, if you’re seeking income from a fund, pay attention not just to its dividend hero status but also to its dividend yield, investment policy and approach, and long-term dividend growth rate.

Conclusion

So, is there a preference among the experts for dividend heroes or enhanced dividend policies? The consensus is that both are valuable approaches, but the best option will depend on the individual investor.

Carthew notes that value investing tends to outperform growth investing over the very long term, so for younger investors seeking long-term growth, dividend hero trusts make more sense. “A sensibly managed natural income trust without too high a yield target might deliver the best overall long-term returns.”

Income investors should consider where they plan to invest as a first step, points out McMahon. “Core income sectors with well-established dividend cultures are probably better invested in with a natural income approach, to benefit from the steadiness of operational performance underlying the income generation,” he says.

Dividend hero status is a valuable plus in this context. Conversely, enhanced dividend payouts can vary as NAV fluctuates, so they’ll be less reliable.

In the end, both strategies can work well for investors, but you do have to do your homework and delve beneath the alluring headlines to understand what you’re really investing in.

Octopus Renewables Infrastructure Trust (LSE:ORIT) announced an unaudited net asset value (NAV) of £454.7 million, or 86.18 pence per share, as of 30 June 2026, compared with £491.5 million, or 93.15 pence per share, at the end of March. The change represents a negative NAV total return of 5.8% over the quarter. The decline reflects lower long-term electricity price assumptions, a reduction of around 10% in projected energy production across the trust’s onshore wind assets, and higher discount rates, partially offset by more favourable macroeconomic assumptions and longer expected operating lives for certain assets.

Onshore Wind Review Reshapes Portfolio Valuation

According to management, the reassessment of its onshore wind portfolio reduced NAV by £30.4 million after replacing pre-construction production estimates with operational performance data. While the revision negatively affected valuations, the trust believes it provides a more realistic and resilient assessment of the portfolio’s long-term value.

The company also revised the expected operating lifespan of selected onshore wind farms and updated decommissioning cost assumptions to better reflect current market standards. Gearing increased to 46.6% of gross asset value during the period. Despite these adjustments, the trust highlighted that approximately 86% of expected revenue through June 2028 has already been fixed, supporting its commitment to a progressive dividend policy that remains fully covered.

Dividend Support Offsets Recent Financial Weakness

Octopus Renewables Infrastructure Trust continues to benefit from a strong balance sheet, although recent financial performance has been affected by losses, lower shareholder equity and weaker free cash flow. These factors continue to weigh on the trust’s overall outlook despite its solid solvency position.

Technical indicators remain moderately constructive in the near term, while the trust’s high dividend yield continues to underpin valuation. However, the negative price-to-earnings ratio reflects the impact of recent losses.

About Octopus Renewables Infrastructure Trust plc

Octopus Renewables Infrastructure Trust plc is an investment company focused on renewable energy infrastructure across the UK and Europe. Its portfolio includes onshore wind, offshore wind and solar assets at both operational and development stages, with the objective of delivering reliable long-term cash generation through disciplined investment management and a progressive dividend strategy.

This article was written by the editorial team at InvestorsHub/ADVFN and is provided for informational purposes only.

Dividend increases could offer useful clues about a company’s financial confidence.

National Bank of Canada (TSX:NA) raised its payout after reporting strong second-quarter growth.

Thomson Reuters (TSX:TRI) extended its dividend-growth streak to 33 consecutive years.

Foolish investors always love to hear dividend hike news from stocks they already own. Usually, increasing dividends also shows that management feels good about the company’s earnings, cash flow, and ability to keep growing. Of course, no dividend is guaranteed, but businesses that raise their payouts year after year tend to have a solid financial base and strong fundamentals behind them.

Two well-known Canadian companies recently gave investors another reason to pay attention. National Bank of Canada (TSX:NA) followed strong banking results with a higher quarterly dividend, while Thomson Reuters (TSX:TRI) extended a dividend-growth streak that now stretches beyond three decades.

Let’s take a closer look at both stocks, their financials supporting these latest dividend increases, and why each could still appeal to long-term income investors.

Source: Getty Images

National Bank stock

National Bank of Canada offers investors a great mix of rising income, strong earnings growth, and expanding operations. The bank mainly provides personal and commercial banking, wealth management, capital markets, and international financial services.

Its shares have gained 60% over the last year and 34% year to date to currently trade at $230.99 apiece, giving the bank a market capitalization of about $88.7 billion. At this market price, it has a 2.3% annualized dividend yield.

That strong share-price performance has been backed by National Bank’s improving results. In the second quarter of its fiscal 2026 (ended in April), the bank’s net income rose 38% year-over-year (YoY) to about $1.2 billion, while its adjusted earnings advanced 13% to $3.23 per share. Growth across its business segments helped drive those gains. Lower provisions for credit losses also played a major role, since its quarterly results a year ago included initial provisions tied to acquired Canadian Western Bank loans.

Similarly, National Bank’s wealth management net income climbed 18% YoY to $274 million, while U.S. specialty finance and international net income rose 10% to $186 million.

Following those strong results, National Bank raised its quarterly dividend by 6% to $1.32 per share. Meanwhile, the bank continues to pursue synergies from its Canadian Western Bank acquisition and plans to expand further through transactions involving selected Laurentian Bank portfolios.

With solid capital levels, growing earnings, and another payout increase, National Bank remains an attractive choice for investors seeking dependable dividend growth.

Thomson Reuters stock

For investors looking beyond the banking sector, Thomson Reuters also offers a healthy combination of recurring revenue, artificial intelligence (AI)-linked growth, and rising dividends.

In short, Thomson Reuters provides software, information, and technology to legal, accounting, compliance, and media professionals. Its shares currently trade at $145.55 per share with a market cap of $63.5 billion. The stock has fallen 20% year to date, while its annualized dividend yield stands at 2.6%.

This weakness in TRI stock contrasts with the underlying strength in the company’s operating results. Its first-quarter revenue rose 10% YoY to US$2.1 billion, helped by a 10% rise in recurring revenue and 15% growth in transaction revenue. Meanwhile, its organic revenue grew 8%, while the legal professionals, corporates, and tax, audit, and accounting professionals segments delivered combined organic growth of 9%.

The company’s adjusted earnings also climbed 10% YoY in the latest quarter to US$1.23, and free cash flow jumped 19% to US$332 million. Demand for many of its products, such as Westlaw, CoCounsel, Practical Law, Pagero, and Confirmation, supported growth across its core businesses.

Encouraged by these results, Thomson Reuters raised its annualized dividend by 10% to US$2.62. That marked its 33rd consecutive year of dividend increases and its fifth straight 10% hike. Moreover, the company is continuing to invest in AI, including its acquisition of Noetica.

Its long dividend-growth record, healthy recurring revenue, and continued investment in AI-powered professional tools make Thomson Reuters an appealing stock for long-term investors.