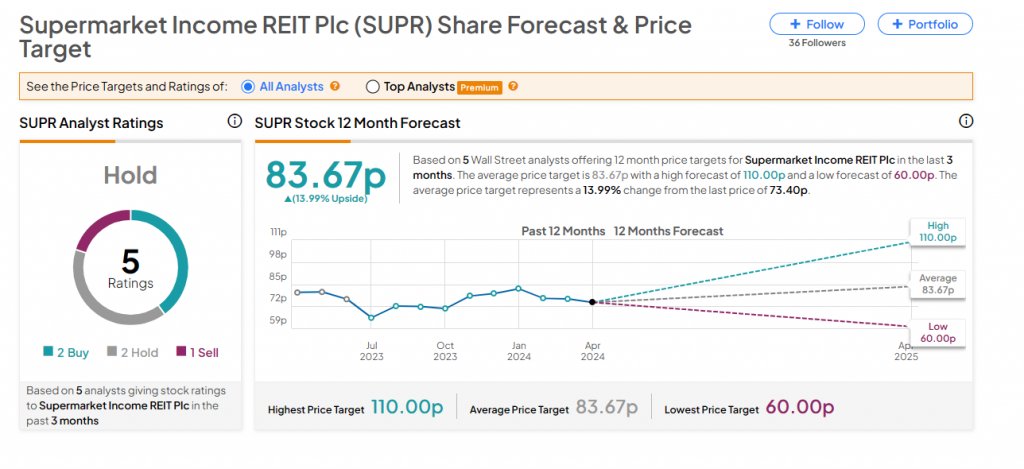

INVESTING EXPLAINED: What you need to know about KIDs – Key Information Documents

Story by City & Finance Reporter

In this series, we bust the jargon and explain a popular investing term or theme. Here it’s KIDs.

What are these?

Nothing to do with children, or goats as you suspected. KID stands for Key Information Document – a summary of the facts and figures you need to know before choosing a fund.

This information, compiled by the fund manager, includes the fund’s objectives, its risk and reward profile, the charges and performance data.

Looking up: KIDs are a summary of the facts and figures you need to know before choosing a fund

The document is a requirement of the PRIIPs – packaged retail and insurance-based investment products regulations – an EU-wide safety standard for investors.

The KID is a shorter, simplified version of the document that it has largely replaced, known as the KIID – Key Investor Information Document.

This is a requirement of another EU-wide set of rules UCITS – Undertakings for Collective Investment in Transferable Securities Directive.

Both sets of EU regulations were ‘on-shored’ by the UK post-Brexit.

Collective investment is a fancy name for any type of fund, including investment trusts and ETFs – exchange traded funds.

Why am I reading about this now?

The methods used to calculate some of the other numbers in the KID, such as the charges, have become the source of controversy.

There is a particular row over the forward-looking performance figures in the document which are widely considered to be misleading.

Investment trust managers argue that KIDs – which are supposed to ensure that consumers make an informed decision – are doing the exact opposite.

The trade body Association of Investment Trusts (AIC) says that ‘too many KIDs overstate potential performance – and understate risks which can mislead consumers about the returns that they could receive’.

The AIC also takes issue with the cost disclosure rules, although the watchdog Financial Conduct Authority (FCA), which says that the current system is ‘not supporting good customer outcomes’ has made some concessions on this front.

Is this going to get sorted out?

As part of the wide-ranging Edinburgh reforms to financial services, the Government has pledged to establish a new disclosure regime to replace PRIIPs and UCITs.

To date, however, the House of Commons committee overseeing the reforms says the big promises are yet to be fulfilled. This adds to the pressure for action this year.

In the meantime, where can I go for information that’s more reliable?

While waiting for the replacement to the KID, it is always worth checking whether any funds you have appear on the recommended lists prepared by AJ Bell, Bestinvest, Fidelity, FundCalibre, Hargreaves Lansdown and Interactive Investor.

Bestinvest’s Dog Fund ratings are a guide to the funds that are not delivering, whatever their KID may say.

Despite the fuss, I’m still interested in looking at the KIDs for my Isa funds…

You should be able to find a fund’s KID on the website of the manager, and also on the funds sections of platforms like Interactive Investor and AJ Bell.

KIDs are not the most exciting read. But, setting aside their shortcomings, you may find out some stuff you did not know – and probably should have.