If the price is

Above the cloud it’s sunny

Below the cloud it’s raining on your parade

In the cloud u need an umbrella in case it starts to rain.

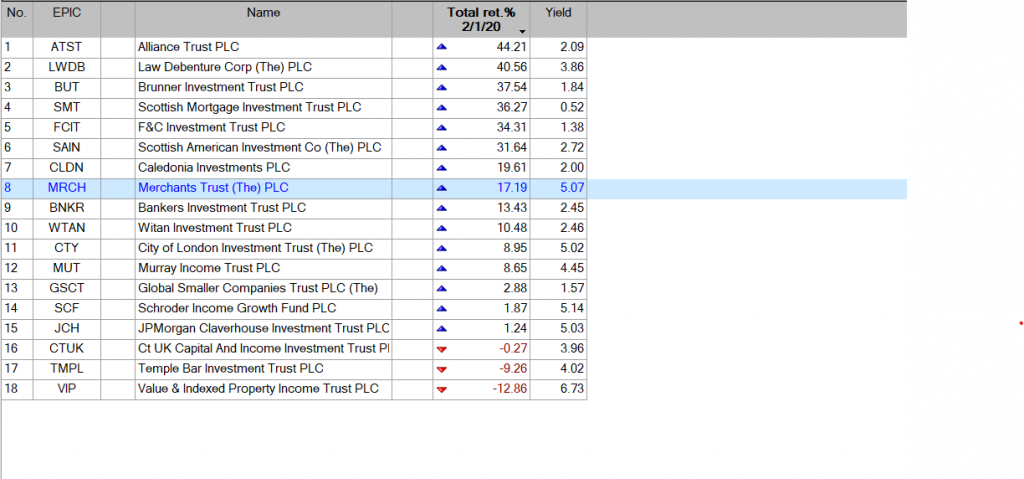

Investment Trust Dividends

If the price is

Above the cloud it’s sunny

Below the cloud it’s raining on your parade

In the cloud u need an umbrella in case it starts to rain.

I’ve sold 2k of ADIG for a loss £10.14.

The delay in returning cash near to NAV makes them

less of an investment in a weak market.

cash to re-invest £2020.00

Post covid, as always timing and then time in.

The period reviewed is pre covid.

I’ll update post covid anon but

LWDB looks the safest bet for income/growth.

Possible entrants for the blog portfolio but not at

the current yields, although they could provide

some stable foundations for a new portfolio.

Difficult market.

Stick to your plan and be thankful

u can still re-invest at some great yields.

Residential Secure Income plc

Net Asset Value and corporate update

Residential Secure Income plc (“ReSI plc”) (LSE: RESI), which invests in independent retirement living and shared ownership to deliver secure, inflation-linked returns, is pleased to announce its unaudited first quarter net asset value (“Net Asset Value” or “NAV”) as at 31 December 2023 and to update on recent corporate activity for the period.

Strong operational performance reflecting defensive nature of assets

· Portfolio focused on direct leases with pensioners and part homeowners

· Rent collection consistent at over 99% for the quarter

· Rental growth of 6.6% on 449 properties (15% of portfolio) giving 1.3% like-for-like growth

· Shared ownership portfolio fully occupied with record 96% retirement occupancy continuing

Advancing sale of Local Authority Portfolio

· Exchanged on sale for £5.8mn of assets in line with September 2023 book value, with completion scheduled to occur by early April 2024

· As announced at year end, proceeds will be used to pay down floating rate debt

· Remainder of the Local Authority portfolio under offer with due diligence advancing

Fully covered dividend

· Quarterly dividend of 1.03 pence per share (“p”) announced today in line with FY24 target3

· 121% dividend coverage from Adjusted EPRA earnings of 1.25p

· Local Authority Portfolio Sale is expected to reduce annualised dividend coverage by c.6% but improve its quality through repayment of floating rate debt

Valuation decline as a result of a 10 basis point outward yield shift across the portfolio

· Total EPRA return for the quarter of -0.8% (0.7p) to give EPRA NTA of 80.1p (£148.3mn) as at 31 December 2023

· Driven by a 1.3p, or 0.6% decrease in like-for-like investment property values, as follows:

o 1.8p increase from inflation-linked rent reviews in the quarter

o 3.1p decrease resulting from a further 10 basis points outward yield shift

· Annualised net rental yields now 5.6% in retirement and 3.5% in shared ownership

Resilient balance sheet with long-term and low-cost debt

· Diverse portfolio of 3,293 homes worth £343mn

· 21-year average debt maturity, 90% fixed or index linked

· Loan-to-value ratio of 52% and reduced to 43% when including 22% reversionary surplus

· Sale of local authority portfolio will allow for repayment of all floating rate and short-term debt

Outlook

· Strong rental inflation-linked growth expected to continue, underpinned by wage/pension growth

· Strong and accelerating institutional appetite for residential exposure

· Focus on driving retirement performance including rationalising portfolio footprint, driving rents, and reducing leakage

· Continuing to review options for further disposals which support maximising shareholder value

· Acute need for more affordable homes, estimated at £34bn annually

· Particular shortage of independent retirement accommodation for growing elderly population and accessible homeownership options providing significant opportunity to scale these platforms and drive returns

Unsurprisingly TENT has moved from the trending up portfolio

to the trending down portfolio.

As always best to DYOR before making any trading decisions.

Posted on | By Bruce Packard

Bruce remembers a metaphor from the founder of the Georgian Stock Exchange and wonders how it might apply to Chinese financial markets.

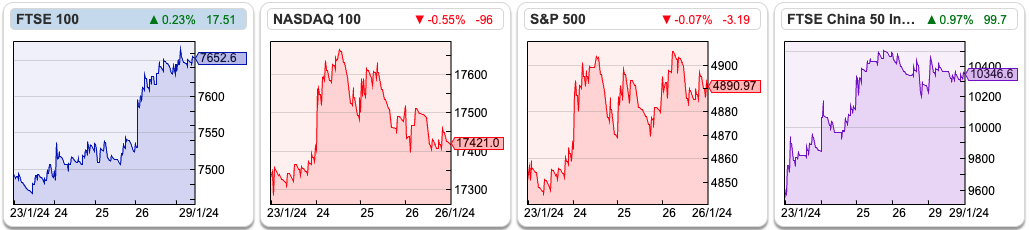

The FTSE 100 was up +2.2% to 7653 last week. The Nasdaq100 and S&P500 rose +2.4% and 1.1%. Brent Crude was up +4% in the last 5 days, most of which was on Monday morning. Chinese stockmarkets have bounced with the FTSE China 50 up +8.3% and the Hang Seng +7.5%.

The FT has reported that the Chinese authorities have tried to halt the sell-off in domestic equities. For instance, institutional investors have been told not to sell equities and short selling has been curbed. That might explain the short-term bounce but the FTSE China 50 is still down -31% in the last 12 months. ETFs tracking US and Japanese markets are becoming increasingly popular among Chinese retail investors, such that mutual funds were hitting limits that were designed to protect capital controls. The Chinese Yuan (CNY on Sharepad) is linked to the US dollar – but allowed to fluctuate around a narrow band. If the CNY continues to weaken, that could also be bad news for commodities and mining shares.

Many years ago I met the founder of the Georgian Stock Exchange, a chap called Gogi Loladze. He cut a dashing figure and was something of a capitalist philosopher, in the style of George Soros. Autocratic leaders, he said, craft their own narratives, and prevent any data that contradict their stories from circulating. However, these autocrats feared financial markets, because liquidity requires buyers and sellers to trade on good (that is, not unfair) information. The financial markets are like a barometer, it tells you what the air pressure is, and if a storm is blowing in, the meteorological instrument will warn you. That’s in contrast to government statistics like GDP which can be manipulated by less scrupulous leaders.

Gogi was keen to develop the Georgian Stock Exchange because

i) it would provide an alternative source of capital in competition to the banking system

ii) it would strengthen Georgia institutionally, which at the time wanted to be the “Singapore of the Caucasus”

iii) it would make him rich.

Building any two-sided platform is hard and he couldn’t get to critical mass and benefit from network effects. The Georgian Stock Exchange still exists but is owned by the large banks, which are not keen to develop it for some of the same reasons above. As a generalisation bankers prefer “discretion” (also known as secrecy) to the circulation of financial information.

Since then it has struck me that Gogi’s insight from a former Soviet Union country could apply equally well to China, which is communist, and increasingly autocratic but has a huge stock market. The Chinese GDP figures were announced a couple of weeks ago and were in line with expectations at c. +5%. No one seems to have a convincing narrative on why Chinese equities are selling off, but I would be wary. Below is a chart showing the FTSE China 50 (XINO) has fallen for 3 consecutive years in a row.

Impact Healthcare REIT plc

(“Impact” or the “Company” or, together with its subsidiaries, the “Group”)

2023 UPDATE, DIVIDEND DECLARATION AND 2024 DIVIDEND TARGET

HIGHLIGHTS

Our tenants continue to improve their performance with higher care home occupancy and increased fees to residents as inflation peaked in the year. Our rent increases are largely capped at 4%, so this helps tenants’ rent cover, and makes our income more secure. Boosted by an acquisition, our total rent roll grew strongly and this has flowed through to both earnings and dividend growth.

· 13.2% increase in contracted rent to £48.8 million for the 2023 year (+£5.7 million). Rental growth was driven by inflation-linked rent reviews (capped at 4%) plus a significant acquisition.

· 2.2x tenant rent cover(1) in Q3, up from 1.9x in the same quarter the previous year. This is the strongest quarterly tenant performance since the Company’s inception in 2017.

· 20.8 years weighted average unexpired lease, up from 19.7 years the previous year.

· Delivered a 3.5% increase in dividends per share in 2023 with a Q4 dividend of 1.6925 pence in line with our target of 6.77 pence per share for the year to 31 December 2023.

· 2.7% increase in dividend target to 6.95p for the 2024 year.

PORTFOLIO TRADING UPDATE

· Stronger tenant rent cover is driven by several factors: improving room occupancy; growth in average weekly fees charged by tenants; and rent increases largely being capped at 4%.

· The Group has received 100% of rent payments due (excluding the ex-Silverline homes) for the quarter to 31 December 2023 .

· Tenants maintained their profit recovery in Q4 and, based on the 88% of the Company’s portfolio that has reported so far, we estimate that the full year 2023 rent cover rose to 2.0x, up 0.2x compared to the full year 2022 of 1.8x.

· Occupancy at 31 December 2023 was 88.2%, up from 87.4% at 31 December 2022.

· The average weekly fees the Group’s tenants charge for the care they provide grew by c.12% in the 12 months to 31 December 2023.

· The £5.7 million growth in contracted rent was due to;

o £3.9 million from the acquisition of a portfolio of six homes near Shrewsbury leased to Welford, in January 2023.

o £1.6 million from 119 rent reviews in the year at an average increase of 4.1%.

o £0.3 million from rentalised capital expenditure with the largest projects being at Mavern and Yew Tree.

o Less £0.2 million from the disposal of one home.

· The former Silverline portfolio of seven homes continues to show improved performance under the management of Melrose, an affiliate of the Minster Group

o Melrose has undertaken a significant amount of work in a relatively short space of time including: measures to stabilise staff teams and to reduce use of agency staff; settling outstanding invoices with suppliers; renegotiating utility contracts; and focusing on improving processes and the care environment for both staff and residents.

o The portfolio of four homes in Scotland has an average occupancy of 88% and is now cashflow positive. Negotiations are well advanced to transfer these homes back to rent generating operational leases.

o The portfolio of three homes in Bradford is expected to be cashflow positive by the end of first quarter of 2024 with discussions underway on a new management proposal.

· At 31 December 2023, our portfolio comprised 140 healthcare properties, of which:

o 138 are care homes managed by 13 tenants on fixed-term leases with an average WAULT of 20.8 years (no break clauses), subject to annual upward-only Retail Price Index-linked rent reviews (with a floor and cap at 2% p.a. and 4% p.a., respectively on 117 leases, and 1% p.a. and 5% p.a. on 21 leases).

o In addition, the Group owns two healthcare facilities leased to the NHS with an annual CPI uplift (uncapped).

o In total, the Group had 14 tenants across its Portfolio.

FINANCING

· As at 31 December 2023 the Group’s drawn debt was £184.8 million:

o 95% hedged through a combination of fixed debt (£75 million at 3.0%) and SONIA interest rate caps (£50 million at 3% and £50 million at 4%).

o EPRA LTV of 27.7% based on 30 September 2023 balance sheet information.

o The current average cost of drawn debt, including hedging and fixed rate borrowings, is 4.56%.

DIVIDEND DECLARATION AND 2024 DIVIDEND TARGET

· The Board has today declared the Company’s fourth interim dividend for the year ended 31 December 2023 of 1.6925 pence per ordinary share, payable on 23rd February 2024 to shareholders on the register on 9th February 2024. The ex-dividend date will be 8th February 2024. This dividend will be paid as a Property Income Distribution (“PID”).

o This is consistent with the prior three quarters dividends and delivers on the Company’s annual dividend target of 6.77 pence per share for the year ended 31 December 2023. This is in line with the Company’s dividend policy, which seeks to maintain a progressive dividend that is covered by its adjusted earnings.

· The target dividend for the year to 31 December 2024 is 6.95 pence per share, a 0.18 pence increase from the prior period.

· The Company expects to report its full accounts for the year to 31 December 2023, which will include an updated valuation of the portfolio, in late March 2024.

© 2026 Passive Income Live

Theme by Anders Noren — Up ↑