Weekly 360 – the week’s Investment Trust results

Vietnam Holding gets another five years, Witan predicts a recovery in 2024 and Tufton Oceanic Assets sets course for 2030. Catch up on the week in Investment Trusts with Frank Buhagiar.

By

Frank Buhagiar

Vietnam Holding (VNH) gets another five year

VNH’s interims help explain why shareholders recently voted for the continuation of the fund–performance. According to Chairman Hiroshi Funaki, “several shareholders told us that they were delighted by the Fund’s performance.” Easy to see why – over the last six months NAV per share came in “4.8% higher than the Vietnam All Share Total Return Index (VNASTR). Above all, the Fund has outperformed VNASTR over 1, 3, 5 and 10 years.”

Looking ahead, no sitting on laurels for the investment managers “The Vietnamese stock market is volatile, and so requires active on-the-ground research and interaction capabilities. We do not take our outperformance to the market and our peers for granted”.

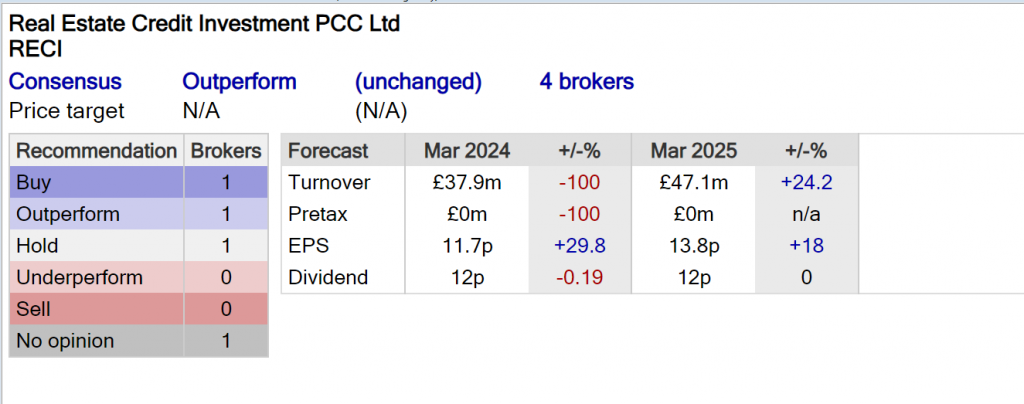

Winterflood “Overweight in Telecommunications contributed to returns. Elsewhere, Bank holdings (largest sector, although underweight to index) fell -3.6%.”

Witan (WTAN) is staying watchful

WTAN’s 12.7% NAV Total Return for the year, a little short of the benchmark’s 14.7% but, as Chairman Andrew Ross explains, “our core managers in aggregate outperformed. Our lagging of the benchmark was entirely attributed to weakness from the GMO Climate Change Investment Fund and Witan’s holdings in investment companies. We see prospects for both to recover in 2024.” As for the sprinkling of magic during the year, CEO Andrew Bell reveals “The magic ingredient for equity markets was excitement over the prospects for companies directly exposed to the accelerating development of generative AI.”

Bell also provides a weather forecast “The fact that the days lengthen from December to June does not guarantee trouble-free weather on the way. Consequently, alongside a generally positive view of the world’s medium-term prospects, a heavy dose of watchfulness is warranted.”

Numis: “The big news from Witan’s announcements this morning is the pending retirement of Andrew Bell, which has resulted in the Board considering management arrangements for the fund.”

JPMorgan sees “no reason to change our Neutral recommendation at this stage”.

Tufton Oceanic Assets (SHIP) sets course for 2030

SHIP’s NAV Total Return for the half year may have come in at 9.6% but the share price moved in the opposite direction from US$0.99 to US$0.98. Okay, only the smallest of losses, but, as Chairman Rob King writes, SHIP was not alone “In common with most of the UK-listed investment funds sector, the Company’s shares traded at a significant discount, on average at 31% discount to NAV over the financial period.”

That discount has been exercising the mind of the Board. King adds “Considering the ongoing share price discount to NAV and the Company’s forthcoming continuation vote at the AGM in October 2024, the Board conducted a mid-term strategy and capital allocation policy review.” The result? “ (the board) believe the correct strategy for SHIP over the medium term, through to 2030, is to continue investing in fuel-efficient second-hand vessels to maximise shareholder returns, intending to realise the Company’s portfolio of assets starting from 2028, well before the decarbonisation of shipping accelerates.”

Liberum: “SHIP’s annualised NAV TR of 13.2% since inception in 2018. On a five-year view, returns rank seventh across all alternative funds with market caps above £100m”.

Numis: “The fund has proved itself to have a nimble management team who are able to navigate changing markets.”

JPMorgan US Smaller Companies (JUSC) believes history is on its side

JUSC’s small cap focus meant performance struggled to match that of the large caps. According to the investment managers “The S&P 500 rose 26% (in USD terms) during the year, led by a handful of mega-cap tech stocks, the so-called ‘Magnificent 7’.” The small cap index, the Russell 2000 Index (Net), could ‘only’ manage a 10.1% gain (in GBP terms). JUSC’s NAV increased by 4.6% (sterling).

The investment managers do not sound overly concerned “the third quarter earnings of our portfolio companies exceeded expectations.” What’s more, the managers believe history is on their side “As 2024 unfolds, we are constructive on the outlook for small-cap companies, given a compelling valuation case and potential for small caps to benefit as they have historically after similar periods of large cap concentration.”

Numis: “We believe that the fund has gained recognition in the market as a consistently strong performer. The shares currently trade on c.9% discount to NAV, which offers an attractive entry point, in our view”.

European Assets’ (EAT) full-year performance – a mixed bag

EAT reported an 8.2% NAV total return (sterling) for the year, a little short of the benchmark’s 9.8% return, prompting Chairman Jack Perry to write “the portfolio performance for the year was on one hand satisfactory, in that it compared well with the peer group and allowed us to announce an increase in dividend, but also disappointing in that it lagged the Benchmark.” As for what lay behind the shortfall “European market leadership came from value stocks, providing a headwind for our growth biased portfolio. Smaller companies also struggled”.

The investment managers however “think this is an excellent opportunity for the creation of long-term returns. We expect to use any further volatility to take advantage of this opportunity and gear the portfolio further.”

Numis: “The key news from European Assets’ results is tweaks to the investment process. The fundamental approach remains the same, with the fund investing in ‘quality growth’ companies, although greater focus will be spent on ensuring that if companies are more expensive than the market, that this is justified.”

Fidelity European’s (FEV) long-term track record remains intact

FEV’s 17.5% NAV total return was comfortably ahead of the benchmark’s +15.7%. Chairman Vivian Bazalgette points out the strong performance was no one-off “The longer-term performance record is also strong, with NAV and share price total returns ahead of the Benchmark Index over three, five and ten years to the end of December 2023.”

As for the outlook, a word of advice from Bazalgette “it would be unwise to buy too fully into the idea that ‘normalising’ interest and inflation rates will ensure a rosy picture in 2024.” With that in mind, “The Portfolio Managers’ focus is unchanged and continues to be on finding attractively valued companies with good prospects for cash generation and dividend growth over the longer term, with positioning driven by opportunities at the individual stock level rather than macro developments.”

JPMorgan: “This was another period of strong performance from FEV, which has been fairly consistently outperforming its benchmark and peers, including on a risk-adjusted basis.”

Literacy Capital (BOOK) helping disadvantaged children

BOOK’s net assets stood at £300.3m as at 31 December 2023, a 19% increase on the previous year after costs, expenses and charitable donations. Charitable donations? As well as generating returns for investors through its private equity portfolio, BOOK also helps “disadvantaged children across the UK get a fair chance” – in 2023, the fund gave £2.8m of charitable donations (£2.3m in 2022), bringing total donations to above £8.5m since the fund’s inception.

On performance, CEO Richard Pindar has this to say “Following extremely strong performance years in 2021 and 2022 (NAV growth of +94.1% and +51.7% respectively), it has been challenging to repeat this level of performance in 2023 (+19.0%), as weaker UK macroeconomic conditions have impacted the growth of certain portfolio companies.”

Liberum: “The 19% NAV return in 2023 is the highest in the sector (ex-3i) and the 3-year NAV return of 217.7% even blows 3i out of the water (140%).”

Winterflood thinks the results highlight the “benefits of its differentiated approach within the peer group, whereby a concentrated portfolio of reasonably small, founder-led companies has been curated through opportunistic partnerships (e.g. retiring founders).”

JPMorgan Claverhouse (JCH) keeping up with the benchmark

JCH posted a 7.3% NAV return for the full-year. Okay a little off the benchmark’s 7.9% but, as Chairman David Fletcher, explains “a favourable environment, together with the changes that the Portfolio Managers made to the portfolio in the first half of the Company’s financial year, in particular its cyclical investments, contributed to an out-performance against the Benchmark in the second half of the year”.

In their outlook, the investment managers talk barbells “your Company remains a modestly-geared portfolio that uses a barbell approach of owning both attractively valued, high-yielding stocks, as well as growth stocks. Our barbell approach is naturally diversifying, and our portfolio is currently focused on robust, liquid, globally-diversified blue-chip, UK listed stocks.”

Numis “JPMorgan Claverhouse remains one of our favoured picks in the UK Equity Income Sector. It has outperformed the FTSE All Share by 1.0% pa following the shift to a more fundamentally driven, higher conviction approach in 2012, producing NAV total returns of 136% (7.4% pa) compared with 113% (6.4% pa) for the index.”

Baillie Gifford Japan (BGFD) sticking to its guns

BGFD clocked a +7.8% NAV total return for the latest half-year period. That compares to the TOPIX’s +13.1% (sterling). According to the Interim Management Report, the shortfall is down to large caps outperforming the medium/small caps, an area which BGFD is naturally drawn to “We are looking for companies with the ability to grow sales and profits significantly over the long term which means that we are naturally orientated towards a higher weighting in medium and smaller companies.”

And the fund managers are sticking to their guns “We continue to be positive about the outlook for the portfolio of stocks held by your Company. Whilst these types of businesses have not been the short-term focus of the market, many continue to make solid operational progress and benefit from longer-term secular trends such as the moves towards digitalisation, automation and AI.”

Winterflood notes that “Share price TR +2.5% as discount widened from 6.7% to 11.5%” while “23.1m shares (3.5% of share capital) bought back over HY.”