Investment Trust Dividends

Cordiant Digital Infrastructure’s Chairman buys shares AGAIN; Gulf Investment Fund launches a tender offer; Diverse Income maintains its unbroken record of dividend growth; while Partners Group Private Equity shares sit on a 6.7% yield full-year payout was raised.

By Frank Buhagiar•28 Aug

Cordiant Digital Infrastructure (CORD) Chairman and co-founder, Steven Marshall, snapped up a combined 440,919 CORD ordinary shares at an average price of 74.56 pence each. As per the company’s press release, following the purchases, which were made in July and August 2024, Marshall now holds 9,516,119 ordinary shares in the company. Regular readers will know, the purchases are not the only ones made by Marshall over the past year or so. With the share price still trading at a steep discount to net assets (-37%) chances are they won’t be the last.

Gulf Investment Fund Launches Tender Offer

Gulf Investment Fund (GIF) announced a tender offer for up to 100% of each shareholder’s holding in the fund. The tender offer is being proposed in line with the authority granted by shareholders at the December 2023 Annual General Meeting. The Tender Price will be announced at a later date.

Winterflood notes that “As it would not be in the interests of shareholders to be invested in a sub-scale illiquid fund, the fund shall not be obliged to proceed with any tender offer where the Board believes it would reduce the fund to such a size that it would no longer be fit for purpose. This minimum size condition shall be a post tender offer share capital of not less than 38m shares.” Thing is, according to the February Half-year Report, the US$2.5352 NAV per share reported for 31 December 2023 was based on 40,103,204 ordinary shares in issue. The tender then unlikely to be a particularly large one.

Dividend Watch

Diverse Income (DIVI) increased its full-year dividend by +4.9%. As announced in the latest Annual Report, a recommended final dividend of 1.2p per share will raise the payout for the year to 4.25p from 4.05p. The dividend increase maintains the trust’s “unbroken good and growing dividend record.”

Partners Group Private Equity (PEY) shares are currently sitting on a prospective dividend yield of 6.7%. That’s according to the latest Half-year Report and follows the payment of the first interim dividend of EUR 0.355 per share to shareholders in June. All in line with the fund’s objective to distribute 5% of previous year-end NAV for each financial year via semi-annual payments in June and December.

| Pearle Skoienhearthis.at/htnweb/d-drillCrumb@gmail.com207.228.38.159 How do I know if a WordPress theme supports a subscribe option. | Reply | Hey there, Ever wanted to start an online coaching business? People from all kinds of professional backgrounds are seeking advice online for personal growth and lifestyle improvement. So, now is the right time to start an online coaching business. If you’re looking for an all-in-one coaching platform, then you might want to take a look at CoachKit by MemberPress. It is an all-in-one platform that combines memberships, branding, payments, recurring subscriptions, content access rules, scheduling, community support, client management, reminders…and more. It is indeed the only complete coaching toolkit for WordPress. Here’s what makes it different from the rest: Effortless integration. CoachKit is guaranteed to work seamlessly with your existing WordPress website. Unlimited EVERYTHING. Build as many coaching programs as you want, onboard new coaches, and grow your business without restrictions. Seamless client management. CoachKit’s milestones and habits will keep your clients accountable and motivated, while the built-in messaging system keeps you and your clients connected. Automate everything. Free yourself from tedious tasks and focus on what you do best. CoachKit handles renewals, reminders, upgrades, payments, reminders, and more. Imagine a world where you can focus 100% on coaching, not tech. That’s CoachKit by MemberPress for you. |

A 9.5% yield! Could 10,000 shares of this FTSE 250 fund grow to £12k a year of passive income?

There are many great high-yield dividend shares on the FTSE 250 index. I’ve found one that could deliver a lucrative second income.

by Mark David Hartley

Published 28 August

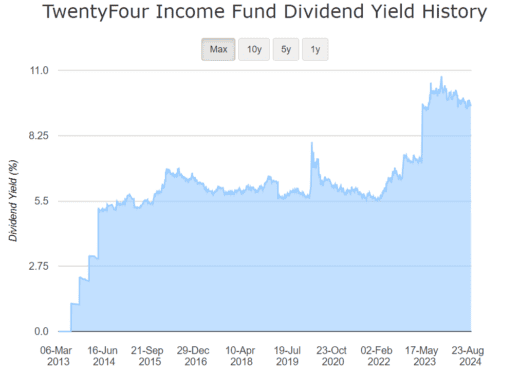

TFIF

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services. Become a Motley Fool member today to get instant access to our top analyst recommendations, in-depth research, investing resources, and more.

I’ve found a lesser-known FTSE 250 stock that looks like it could be a promising dividend payer. Over the past 10 years, its annual dividend’s increased from 6.38p per share to 9.96p — an annual increase of 4.15%.

If it keeps that up, it could pay 15p per share in 10 years. That’s a pretty decent return on shares that currently cost just over £1. The yield‘s now 9.5%, having almost doubled in the past few years.

So what kind of income could I expect to earn from the stock? Well, assuming the yield and growth continue, 10,000 shares could be worth £114,330 in 21 years (with dividends reinvested). And that’s not taking into account any potential share price growth. At that point, the annual dividend could be around £12,000 a year.

See the 6 stocks

That would be a nice bit of extra income for a relatively small initial investment. But what stock am I talking about — and will it keep performing well?

TwentyFour Income Fund‘s (LSE: TFIF) a closed-ended, fixed-income mutual fund managed by Numis Securities. The fund invests primarily in high-yield European asset-backed securities. Based in Guernsey, it’s only been operating for just over 10 years but already seems to be doing well.

A high yield means this fund is in the top 10 dividend payers of 250 UK companies. It also offers good value with a price-to-earnings (P/E) ratio of only 5.7. That’s well below the UK market average of 14.4.

Sometimes this figure’s low because the price has been crashing, but over the past year it’s up 6.48%. That suggests the fund’s not only cheap but also performing well.

In the same vein, the high yield isn’t inflated by a falling price. Rather, it’s the result of generous payouts by the company. This increases the likelihood that it could remain high for the indefinite future.

One problem I find with close-ended funds is that they provide little or no information about their holdings. This requires a lot of trust on the investor’s part, with only the performance of the fund to go on.

TFIF is mostly investing in UK-based asset-backed securities and securitised loans. This puts it at risk of falling in price if the UK economy takes a dip. We all know from 2008 that certain investments like mortgage-backed securities can be risky.

The level of risk depends on how well the fund’s managed. And with a market-cap of only £786m, liquidity could be an issue — meaning it may be hard to find buyers at the right price when trying to sell.

There’s always a level of risk and reward involved!

To maximise gains, I think it’s best to invest via a Stocks and Shares ISA. This type of ISA allows UK residents to invest up to £20,000 a year tax-free.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

I already hold several similar funds in my portfolio so I’m not planning to buy the stock today. But it’s on my watchlist and I think it’s worth considering for investors looking to increase their dividend income.

Note the dividend is 2p which equates to 8p a yield of 7.3%, any surplus funds are paid with the final dividend in April where the last dividend was 3.96p, so the headline yield is not guaranteed. Trading at 4.4% discount to NAV

There is a sister company SMIF which pays a monthly dividend but trades at a small premium. As always it’s best to DYOR.

The Motley Fool

How to create a ton of passive income within an ISA in 3 easy steps

By Edward Sheldon, CFA

Passive income’s often said to be the ‘holy grail’ of personal finance. With this form of income, investors get paid without having to actively work for the money.

Here, I’m going to explain how UK investors can potentially build up a ton of passive income within an ISA in just a few simple steps. Let’s get into it.

Pick the right ISA

Thanks to higher interest rates, it’s possible to generate passive income within a Cash ISA. At present, some of these accounts are offering interest rates of around 5%.

However, if an investor wants to generate a really high-level income, Stocks and Shares ISAs are a better bet, in my view. That’s because these products offer access to high-yielding investments such as dividend stocks and income funds.

So if I was looking to create a powerful passive income stream, I’d start by opening this type of ISA.

Look for attractive dividend stocks

Once I have an account open, my next move would be to identify some attractive high-yielding dividend stocks.

Now, this part of the process can be a little tricky. This is due to the fact that high-yielding stocks don’t always turn out to be good investments.

Sometimes, a high yield’s actually a signal that the underlying company has fundamental problems. So it’s important to look beyond a company’s yield and think about its long-term prospects.

One dividend stock I like the look of today is FTSE 250 company the Renewables Infrastructure Group (LSE: TRIG). It’s an investment company that owns a portfolio of clean energy assets (wind and solar farms etc).

Looking ahead, the transition away from fossil fuels towards renewable energy is likely to be a huge theme. So the backdrop for this company should be quite favourable.

Currently, the yield here is around 7.0%. This means that a £3k investment could potentially generate annual income of about £210 (dividends are never guaranteed though).

Over the last two years, this company’s share price has taken a hit due to higher interest rates. After this fall, I reckon now’s a good time to consider building a position in it.

That said, there’s always the chance that the share price could dip further. Falling energy prices are one risk to consider with this company.

Diversify to reduce risk

Given that every company has its own risks, the last step in my passive income plan is spreading capital out over a number of different stocks.

This move – which is known as ‘diversifying’ a portfolio – can help to reduce stock-specific risk. This, in turn, can improve the chances of generating strong overall returns.

For example, if you only own three stocks and one of them tanks, your overall returns could be ugly. However, if you own 20 stocks and one falls heavily, it’s probably not going to be so bad.

With small-caps on the up, The Telegraph is backing North Atlantic Smaller Cos. manager, Christopher Mills, to keep outperforming, while MoneyWeek believes healthcare REITS, Assura and Primary Health Properties, could be beneficiaries of the new UK government.

By

Frank Buhagiar

28 Aug, 2024

Questor: This Fund Manager Has Returned 13pc a Year for 42 Years – Now is a Good Time to Buy

In 1982, Christopher Mills, founder of investment group Harwood Capital, became manager of the North Atlantic Smaller Companies Trust (NAS). 42 years on and the £555 million investment trust, which remains under Mills’ stewardship, has consistently outperformed the UK stock market, generating an annualised +13% return compared to the FTSE All-Share’s +8.9%. Over ten years, NAS’ total return of +147.5%, comfortably ahead of the Deutsche Numis Smaller Companies index’s +61.2%.

That successful track record, testament to the fund’s Anglo-American approach to investing in small-cap stocks, although currently only around 10% of the fund is invested in U.S. businesses while over 75% is in UK stocks. It’s also a nod to NAS’ activist strategy whereby the fund manager doesn’t just buy and hold sizeable stakes in companies, but also helps management teams transform/turnaround their businesses. And yet despite that track record, the shares currently trade at a 29% discount to net assets – a battle scar of the tough time small-cap funds in general have had these past three years or so, as the high inflation/interest rate environment put investors off the sector.

But things could well be looking up for both small caps and NAS itself. Small-cap indices are showing signs of life as interest rates come down; while NAS’ share price is up 10% over the past 12 months. All in all, Questor sees enough to slap a buy rating on NAS stock. And, it seems, The Telegraph tipster is not alone “we take comfort that Peter Spiller, the manager of Capital Gearing Trust, a longstanding Questor tip, is a big fan. Mr Spiller, who pips Mills to the post as the UK’s longest-serving fund manager, holds him in high regard and owns 6.8pc of North Atlantic. With small companies rallying on a strengthening UK economy, that’s a powerful endorsement.” Safety in numbers and all that.

MoneyWeek: Top Healthcare REITs for Your Portfolio

MoneyWeek has come up with two names in the Real Estate Investment Trust (REIT) space that stand to benefit from the change in government in the UK – Assura (AGR) and Primary Health Properties (PHP).

Fair to say the two trusts have quite a bit in common. Both are focused on building, managing and leasing healthcare facilities, such as GP practices and hospitals. Both primarily rent out their facilities to the NHS, meaning their tenant base is largely government-backed – currently 89% of PHP’s income is paid for by the UK and Irish governments. Both operate in a sector where underlying demand for the facilities they provide is being driven by an ageing population. And both stand to benefit from new Chancellor Rachel Reeves’ decision to scrap the previous plan to build 40 new hospitals across the UK – with NHS waiting lists at record levels “private providers are likely to have to step in to fill the gap.”

Of the two, MoneyWeek thinks that “Assura looks to be the better buy. The stock is trading at around 80% of book value and has an 8.2% forward dividend yield. PHP is around 10% more expensive on a book-value basis and only offers a forward dividend yield of 7.4%.” Nevertheless “both Assura and PHP look well placed to benefit from Labour’s drive to increase investment in the UK economy and improve access to healthcare. A portfolio of both would provide exposure to these themes while reducing company-specific risk.” And if that’s not enough “With interest rates heading lower, these companies may start to look much more attractive from an income perspective.”

Story by Mark David Hartley

The Motley Fool

Dividends are a great way to build compounding returns in a Stocks and Shares ISA. With tons of reliable investment trusts in Britain, it’s easy to find those that pay regular and reliable dividends.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

Investment trusts offer instant a to a highly diversified portfolio of stocks, often across various industries and regions. Since professionals manage them, the returns are usually reliable — although they typically incur a small fee of around 1%.

City of London Investment Trust (LSE: CTY) is considered the number one dividend hero by The Association of Investment Companies. It’s been paying an increasing dividend for 58 consecutive years.

It holds assets across eight European countries with a heavy weighting towards UK stocks. This means it risks losses if the UK economy declines. While the yield of 4.7% is far from the highest in the UK, its track record is reliable. When aiming for long-term passive income, I like this type of stock. I can set it up with a dividend reinvestment plan (DRIP) and leave it to grow.

The price increased 188% since 1994, equating to an annualised return of 3.6% a year. That’s below the FTSE 100 average but is normal for stocks that deliver value via dividends.

The property play

UK real estate has become a core focus of my investing strategy since the Labour Party took power. Just how effective its new housing policies will be remains to be seen – but I’m optimistic.

Value and Indexed Property Income Trust (LSE: VIP) invests in high-yielding but less popular sectors of UK commercial property. It boasts an attractive 6.8% yield and has been increasing its dividend for 37 consecutive years.

UK real estate has become a core focus of my investing strategy since the Labour Party took power. Just how effective its new housing policies will be remains to be seen – but I’m optimistic.

The five-year dividend growth rate’s small, at only 2.27%, but payments are reliable and consistent. And with the price up 28% in 10 years, its annualised return’s 2.5%. However, this growth’s largely cancelled out by the higher-than-average ongoing charge of 1.88%.

Investing in property-related trusts can be risky though. If a global crisis sends the economy into freefall, real estate could be hit hard. This is reflected in the trust’s volatile price, falling sharply in 2008 and 2020.

With a 4.83% yield, JPMorgan Claverhouse (LSE: JCH) is another investment trust with a great track record. Its dividend has increased for 51 consecutive years, with a five-year growth rate of 4.64%.

This trust also holds some of the top stocks on the FTSE 100, including Shell, AstraZeneca and HSBC. It’s similar to, and could be considered as an alternative to, the City of London. The yield’s slightly higher but with a bit less growth over the past 30 years. It’s up 120% in three decades, delivering an annualised return of 2.7%.

It has a low-risk gearing range of between 0 and 20%, currently at 8%. Still, with a focus mainly on UK stocks, it’s at risk of losses if the local economy falters. It also has an ongoing charge of 0.7%, which eats into profits.

£££££££££££

If u want to buy any of the above for your Snowball but still want to earn a blended yield of 7% per year, u would have to pair trade them with a higher yielder.

VPC Specialty Lending Investments PLC

(the “Company”)

DIVIDEND DECLARATION

The Board of Directors of the Company has declared an interim dividend of 1.89 pence per share for the three-month period to 30 June 2024. The dividend will be paid on 3 October 2024 to shareholders on the register as at 6 September 2024. The ex-dividend date is 5 September 2024.

The dividend declared of 1.89 pence per share represents a 2.00p equivalent dividend adjusted to reflect the reduction to NAV as a consequence to the B-Shares issued to shareholders on 19 April 2024 and redeemed on 25 April 2024.

The Board notes that, as previously described, changes to the portfolio composition as debt positions are repaid or restructured are resulting in materially lower levels of income at a portfolio level which will be reflected in what is likely to be a substantial reduction in the dividend in future periods, although as an investment company dividends will represent a distribution of no less than 85% of gross income.

££££££££££££££

Still a yield of 17% so no change until more cash has been returned.

© 2026 Passive Income Live

Theme by Anders Noren — Up ↑