How I’d try to ironclad my second income before interest rates fall

Jon Smith explains a couple of tactics he’s looking to implement in his dividend portfolio to try and protect his second income stream.

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

It’s very likely that interest rates will start to fall later this summer. From the current base rate of 5.25%, the market’s expecting a cut in August (or September at the latest).

The dividend yields in the stock market are related to interest rate movements. Thus, I’m expecting yields to also fall in the coming year. So here’s what I can do to try and protect my second income from dividends.

A couple of ideas

A stock’s dividend yield is calculated by using its current share price and the dividend per share from the past year. I can’t predict exactly what the future dividend per share will be. But I can buy the stock and lock in the share price cost.

Let’s say a company pays out the same dividend over the next year. If I purchase the stock now, the yield will be the same in the coming year.

But if I decide to hold off and the share price increases over the next year, the dividend yield will fall. This has happened to me in the past and I still rue some of my missed opportunities.

What about if I already own a stock that I think could suffer if interest rates fall? In that case, I’d try and iron clad my income now by hedging my bets.

What this means in practice is to look for a stock that should do well with falling interest rates. Then if my existing holding cuts the dividend, I’ll be protected as the new stock should keep paying it. In fact, it could increase the payment if it does well.

An example right now

For example, I currently own shares in Barclays. However, lower interest rates could make the bank less profitable, which could cause the dividend per share to drop.

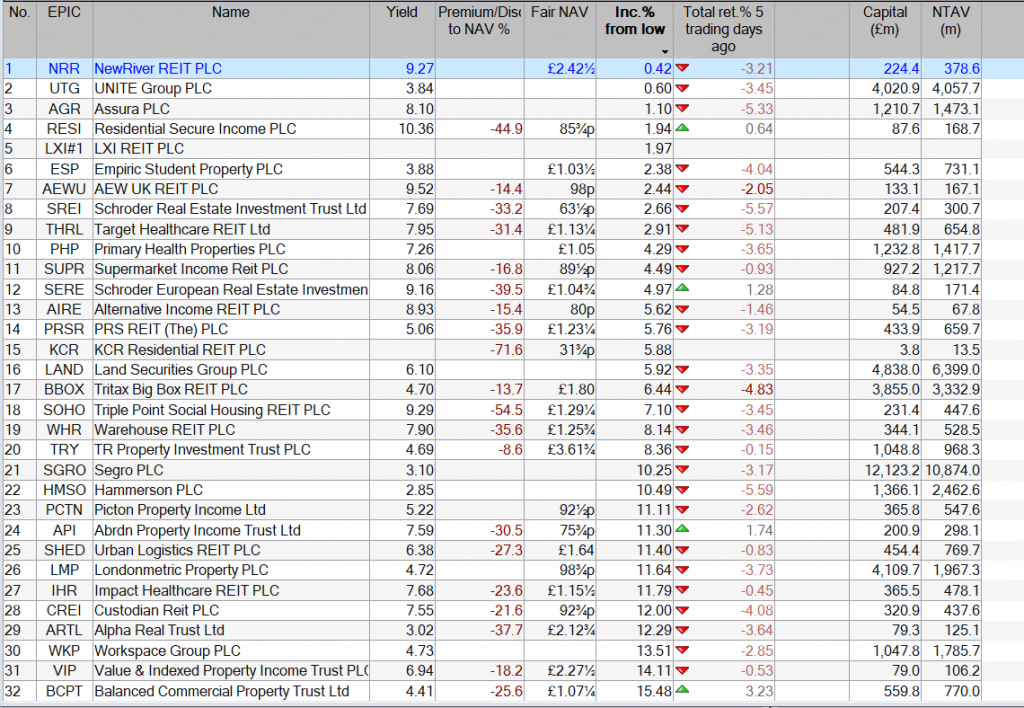

SHED

As a result, I’m thinking about buying the Urban Logistics REIT (LSE:SHED). This FTSE 250 stock has a dividend yield of 6.38%.

I think lower interest rates should help to make the company more profitable. This is because the real-estate investment trust (REIT) has to finance new acquisitions and the existing portfolio via some loans. The lower the interest rate, the cheaper a new loan would be.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

Further, lower interest rates will help to ease pressure on tenants that lease out the properties. The industrial and logistics properties are home to some consumer-facing businesses. If customers spend more as they feel more confident with lower interest rates, it ultimately does help the REIT. Through higher profitability, I’d expect the dividend per share to increase.

The risk is that the benefit to the company takes a long time to filter through. After all, the tenants aren’t going to get an instant boost from any interest rate cut.

Ultimately, I’m seriously thinking about buying shares in the REIT to help hedge against the potential of my dividend income falling.

The blog rules for any new readers, don’t panic there are only two.

Accumulation.

Buy Investment Trusts that pay a dividend to buy more Investment Trusts that pay a dividend.

Any Trust that drastically changes its dividend policy will be sold even at a loss.

De-accumulation.

Instead of reinvesting the dividends, the dividends are used to pay a ‘pension’ and u can leave the capital to any deserving relatives but please remember those wee cats and dogs. The earlier u start on this journey the more u will benefit from compound interest and may have surplus dividends to re-invest for that special occasion.

nordvpn special coupon code 2024 350fairfax.org andrapryor@hotmail.com 102.129.235.26 Hello, i believe that i saw you visited my web site thus i got here to return the want? I am attempting to to find issues to improve my web site! I assume its ok to use some of your ideas!! My blog – nordvpn special coupon code 2024

£££££££££££

All articles can be copied but please include any wealth warning. GL

Money expert Becky O’Connor of PensionBee reveals the most useful – and profitable – real world sums.

Compound growth, which generates massive gains the longer you save and invest, is lesson number one… so what are the others?

3. Understand your risk profile

Risk is an inherent part of investing, but it’s a tough balance. Take too much risk, and you might find yourself racking up some painful investing lessons.

But taking too little (or no risk in the case of cash) is a risky strategy in itself. It could have a hugely detrimental effect on your finances in the future because you might not reach your goals.

And our risk appetite isn’t static. It can change as our circumstances change so needs reviewing regularly.

4. Diversify your investments

This reduces the risk of any one stock in the portfolio hurting the overall performance.

But diversification doesn’t just mean investing in different stocks. It also means having exposure to different sectors, assets, and regions.

5. Rebalance your investments

Trimming the excesses and redirecting funds into underperforming assets ensures that your risk-return equilibrium remains intact.

This calculated approach of buying low and selling high has the potential to bolster long-term returns.

Whether nearing retirement or sprinting towards a shorter investment horizon, rebalancing grants the opportunity to recalibrate allocations to achieve the desired financial destination.

6. Review costs and fees

Investors cannot control the market, but they can control how much they pay to invest. Understand the costs associated with your investments – not least the platform charge.

7. Drip feed your investments

A good and proven way of lowering your investment risk is by investing small amounts regularly. Most often, investors do this by drip-feeding investments monthly to help smooth out the inevitable bumps in the market.

The advantage is that you also buy fewer shares when prices are high and more when prices are low – a process known as pound-cost averaging.

8. Set clear goals

Define your financial goals and time horizon before making investment decisions. Avoid making impulsive decisions based on short-term market fluctuations. Stick to your investment strategy.

Investing over many years eventually reaches a ‘tipping point’ where your returns double what you’ve put in to date, highlights new research from Interactive Investor.

Putting £250 per month into investments returning 5 per cent a year would see a gain of £83 on your £3,000 total contributions, or 3 per cent, in year one.

This means that your returns after that year would represent just a small percentage of the total pot.

But by year 10, the power of compounding would mean the portion delivered by investment growth would make up 30 per cent of the overall portfolio, and by year 20 it would be 72 per cent.

At year 26 it would hit 105 per cent – with a pot containing £78,000 worth of your monthly contributions over the period now worth £160,229.

Then you’ve reached the tipping point where your returns double what you’ve put in.

If you paid in the same amount but achieved an annual investment return of 7 per cent, it would take 18 years to reach the investment ‘tipping point’, calculates II.

You can use This is Money’s long-term saving and investing calculator to see how compounding works. When considering compounding, you also need to take into account inflation and charges.

Compounding returns offer a layer of protection against investment volatility, says Myron Jobson, senior personal finance analyst at ii.

‘Generally, as your investment grows, compounding becomes more significant, and there’s a point where growth outpaces new contributions.

‘This varies for each individual’s investment strategy and market conditions.

‘In our scenario, the investment tipping point is 26 years, but the reality is many investors will hit their financial goal, be it investing to buy a home or for retirement, a lot sooner.’

Jobson explains: ‘The nature of investing means the annual rate of return isn’t fixed, meaning you can earn more or less in a given year, depending on the market environment.

Jobson adds that for pension savers, retirement investments are turbocharged by the tax relief and employer cash that are added to your own contributions.

‘This dual advantage not only amplifies the initial investment but also leverages compounding over time, accelerating the growth of the pension fund.’

Pensions are possibly the longest-term investment you will ever have, which makes them particularly fertile ground for compounding to work its magic.

Think of your own and your employer’s pension contributions as the seeds, tax relief as the water, your investment plan as the soil and compound growth as the sunshine, helping to grow what eventually becomes a mature pension pot for when you retire.

One of the beauties of pensions is that if you start paying into them early, as so many workers now do thanks to auto-enrolment kicking in at age 22 (set to come down to 18), you will benefit from around 45 years of compound growth from the investments within that pension.

In fact, assuming roughly similar average annual investment returns, the impact of compound growth for younger pension savers who maximise their workplace pension contributions in their early career rather than starting with lower contributions or even foregoing a pension altogether for more immediate priorities, can be really astonishing.

Someone who makes the same annual contribution of £2,000 a year for their whole working life, but misses five years of pension contributions in their twenties would have a pot £22,000 lower at retirement, at £121,450 rather than £143,215.

“Compounding can work against you too, in that percentage fees on investment products can add up the wrong way, magnifying the reduction in your investment pot over time”

However, if they choose to keep paying in when they are young and instead miss those five years of contributions when they are older, from 60 to 65, the impact on their pension pot is much smaller – with a pot size around £11,000 lower, at £131,895, highlighting the greater importance of contributions made early on to eventual pot size.

Unfortunately, compounding can work against you too, in that percentage fees on investment products can add up the wrong way, magnifying the reduction in your investment pot over time.

Of course if your investment grows by significantly more than the fee, the impact of this is reduced, but it’s worth keeping an eye on and making sure you aren’t being charged over the odds for an investment that isn’t delivering.

How to get the most out of long-term investing

Myron Jobson of Interactive Investor offers the following tips.

1. Take advantage of Isa allowances

The shrinking capital gains and dividend tax allowances provide the impetus for investors to invest through a tax-efficient wrapper if they haven’t already done so.

The transfer, however, will involve selling and buying back shares, which could trigger a capital gains tax bill.

Over the long term Bed & Isa is likely to outweigh the charges that might apply.

2. Consider using your partner’s Isa allowance

You can also help reduce your taxable income by transferring assets between spouses or civil partners.

Each year you can shelter £20,000 from tax in an Isa – so £40,000 between two.

Only married couples and civil partners can transfer assets tax-free, meaning those who aren’t could potentially trigger a tax liability.

Alliance Trust PLC ex-dividend payment date BlackRock World Mining Trust PLC ex-dividend payment date Canadian General Investments Ltd ex-dividend payment date Downing Renewables & Infrastructure Trust PLC ex-dividend payment date Fair Oaks Income Ltd ex-dividend payment date Great Portland Estates PLC ex-dividend payment date Henderson EuroTrust PLC ex-dividend payment date JPMorgan European Growth & Income PLC ex-dividend payment date JPMorgan Global Growth & Income PLC ex-dividend payment date Law Debenture Corp PLC ex-dividend payment date Premier Miton Global Renewables Trust PLC ex-dividend payment date Regional REIT Ltd ex-dividend payment date Temple Bar Investment Trust PLC ex-dividend payment date Triple Point Social Housing REIT PLC ex-dividend payment date

We argue a position in bonds should be diversified with alternatives…

Thomas McMahon

Disclaimer

KEPLER

This is not substantive investment research or a research recommendation, as it does not constitute substantive research or analysis. This material should be considered as general market commentary.

Let’s get one thing clear: in bond land, ten bps is a lot. That is one-tenth of a percent to you. A bond fund manager who can outperform his peers by ten bps is a king. In this world, the 19,000 extra bps (190% to me and you) that have been earned by being in high yield bonds rather than equities since the great financial crisis (GFC) are the riches of Croesus. Following three successive months in which IA funds saw net outflows across equity, fixed income and mixed asset, March 2024 saw a huge surge of cash jump back into bonds. Net retail sales of fixed income funds hit £809m in the month, while equity funds saw just £149m flow in and mixed asset funds saw outflows. Given how strongly fixed income performed after the last crisis, are investors right to be buying back into bonds, and could they repeat their stunning performance?

Do bonds offer attractive returns ?

They say a picture paints a thousand words, so let’s start with a chart. The graph below shows returns to UK high yield bonds and UK equities from the bottom of the 2007/2008 great financial crisis. If you had gone 100% into UK high yield bonds in March 2009, you would be up 500% since then, and have about 60% more money than if you had invested 100% in UK equities. You would have actually outperformed the S&P 500 Index until August 2017 too.

UK EQUITIES VS UK HY BONDS

Source: Morningstar Past performance is not a reliable indicator of future results

The cumulative relative return chart shows that much of this outperformance was earned at the start of the period. After a brief retrenchment, high yield outperformed equities by around another 20 percentage points up to mid-2020, before adding even more to relative returns by the start of 2021. Some of these gains have been given back since.

RELATIVE RETURNS OF UK EQUITIES VS HY

Source: Morningstar Past performance is not a reliable indicator of future results

So, is this an investment strategy? Equity markets are now off their post pandemic lows, but bonds have double dipped. Investors have been increasingly positive on fixed income, with the IA recording massive inflows in March from both retail and professional investors. Anecdotally, we hear that wealth managers have also been adding to fixed income in recent months.

We think there are three reasons that this time is likely to be different, investors should be wary of chasing yield in bonds, and a fixed income bucket should probably remain diversified.

1) The first point is that credit spreads were the source of a greater proportion of the return on offer from bonds in 2009 than they are today. UK rates had been cut from 5.75% at the end of 2007 to 2% at the end of 2008, and were at just 1% when our period starts, so almost all the yield on offer in sterling bonds was from credit spreads. Today, UK rates sit at 5.25% and high yield bonds yield around 7% at the index level, so are only offering an additional 175bps return a year for credit risk. In the US market, the picture is even worse, with the USD market offering less than 100 bps of additional spread over short-term rates. In other words, there isn’t a lot of scope for an improving picture for the economy or for corporate earnings to be reflected in bond fund returns. This time round, a vastly greater proportion of returns are likely to be due to duration – i.e. movements in interest rates. The picture is even worse in the sterling investment grade sector which retail investors are currently favouring (going by IA data). Here yields are only around 5.4%, meaning only a few bps are on offer for taking the credit risk of lending to a company rather than HMG. Even a bond fund manager would struggle to get excited about that. Our first point is that bonds don’t offer much extra return over short-term money market funds, i.e. cash.

2) The second point is that the rate outlook looks bumpy. A cut seems more likely than a raise at the next BoE meeting, but even that is now less certain in the US, after some strong data. Better economic data would be good for credit spreads, but as discussed above, there is more limited scope for these to tighten and deliver returns. Better economic data would suggest higher inflation, which would see rates stay high or be hiked, which would see a greater, negative impact on bonds through duration. Your author suggested that central banks were underestimating the persistence of inflation in early 2022 by anchoring on the past cycle. Now there is a danger that investors are anchoring on the secure glide path down in rates developed market rates saw after the debt binge of the 2000s. Keeping monetary policy as loose as possible worked well in the deflationary world in the 2010s, but inflation is proving more persistent in this cycle. Rearmament, massive spending on net zero initiatives, those initiatives’ vast demand for metals and minerals and the huge costs of reorganizing supply chains in the light of geopolitical tensions are all inflationary. The political climate is also different. In the 2010s, austerity was a message that plenty of people were listening to, but these days it is about as popular as a country that has apparently won two world wars and one world cup at a camp song contest.

3) There is another reason why returns are likely to be lower in this cycle, for high yield in particular. At the height of the GFC, many banks were forced to issue debt at eye wateringly high yields. This subordinated debt was essentially emergency funding, with lenders taking a massive mark-up for taking the risk of being last in the queue to get paid back, while the solvency of developed world banks was in doubt. To take an extreme example, Barclays Bank issued £3bn in debt which paid a 14% coupon, in perpetuity. As the banking system settled down and these bonds de-risked, they helped deliver outstanding returns to those managers who were brave enough to buy in (and enough bps of alpha to buy a lambo in some cases). This dynamic is absent from the current market, as our recent crisis was caused by the impact of the pandemic and the subsequent inflation rather than any issues in credit markets. In fact, the banking industry looks pretty healthy, and is benefitting from a higher net interest margin thanks to high short-term rates.

How can we protect ourselves against the risks in the bond market?

For these reasons, we would be wary of committing exclusively to the conventional bond market, and would want to diversify this exposure with shorter-duration assets or those with less credit risk. In our view, the current rate outlook makes taking a punchy position in duration questionable. The UK corporate bond market has a duration of c. 6 at the time of writing, meaning that a loss of 6% would be expected for a 100 bps parallel shift in the yield curve. This is down from pre-crisis, thanks to the effect of the sell-off in prices, but means there are significant downside risks in the event of a resurgence in inflation. If inflation is accompanied by high nominal GDP growth, then this could be good for credit spreads, but they are already extremely narrow, so there is little to be gained there, and any rate hike effect should be far greater. On the other hand, if we end up with runaway inflation and a recessionary environment, there is the potential for bonds and equities to sell off together as they did in 2022. While this danger seems to have receded, it has not gone away entirely, and in particular the ever-worsening geopolitical situation, and the current conflicts in Ukraine and Israel, offer one route to this outcome.

We think that investors could profit by being diversified in the bond sleeve of their portfolio. This can be done through more unconventional fixed income products. For example, M&G Credit Income (MGCI) invests in private as well as public debt markets, generating a very high yield without taking on the credit risk of a high yield fund. The portfolio is majority floating rate, meaning that investors effectively earn the UK short-term interest rate plus a spread. This spread is wider than it would be for a portfolio of public investments of similar credit risk, typically due to the extra yield that can be earned for the illiquidity and complexity of the private deals. We explain the model in full in our recent note. Key points to note are that any rate hikes would actually boost the yield on offer from the fund without seeing much impact at all on the price. We think the trust offers an attractive way to hedge the risks to the current recovery narrative. Annualising the last quarterly dividend, the historical yield is c. 9.3%, achieved without the use of any gearing, while trading on a discount of 1.4%.

Sequoia Economic Infrastructure Income (SEQI) also operates in the private debt space. SEQI owns a highly diversified portfolio of loans made to infrastructure projects. These are spread across digital infrastructure, power and renewables projects, transport and other sectors. These loans are mostly bilateral or made with a small group of lenders, allowing the management team to negotiate attractive terms to both parties. It has c. 40% in floating rate loans which helps reduce the duration, although the managers have been increasing fixed rate debt at the margin as they can lock in higher rates than in the past. Duration is nonetheless very low, at 2.2 years versus 1.2 years for MGCI. The high yield is one factor that reduces the duration: the current ‘yield to worst’ on the portfolio (which includes an early capital return baked in, assuming borrowers take advantage of any early repayment options) is 10%, and this is without the use of gearing. SEQI’s shares currently yield 8.6% on a historical basis and trade on a 14% discount. We will be publishing a full note on the trust in the coming weeks; click here to be notified.

Another way to diversify the bond sleeve of a portfolio is via alternatives. Greencoat UK Wind (UKW) is the largest trust in the AIC Renewable Energy Infrastructure sector, and is large enough to have generated 1.5% of UK electricity demand in 2023. UKW owns wind farms, and takes on debt at the fund level to help generate an attractive yield, which is currently c. 7%. The board seeks to raise its dividend by at least the growth in RPI over any year, and has achieved this even through the recent inflationary surge. We think this could be an attractive feature if inflation proves more persistent. The managers model a 10% levered portfolio IRR, made up of a c. 6% dividend yield on NAV and real NAV preservation by reinvesting excess cash flows. This offers a considerably higher spread over the base rate than bonds, albeit for taking more specific industry risk. UKW’s shares trade on a 10.6% discount to NAV at the time of writing, which also adds to the total return potential. There is effective duration to consider, as rising rates would reduce the discount rate used to value the assets. But in our view the positive sensitivity of the NAV to inflation and rising power prices offsets this and means the trust offers an interesting diversification element to a bond or bond-plus sleeve. Key risks to consider in the coming years are the need to re-gear, and with rates higher this will likely be a slight headwind to the economics of the fund.

A more diversified option, albeit with a slightly lower expected returns, is The Renewables Infrastructure Group (TRIG). In our latest note we explain how TRIG has an expected NAV return of c. 8%. This is with some significant inflation-linkage however, meaning that a good proportion of returns should be considered real, unlike conventional bonds. The portfolio is highly diversified and getting more so. It is spread across six European countries (including the UK), bringing exposure to different subsidy regimes, with assets across offshore wind, onshore wind and solar. Rising interest rates have hit the NAV over the past two years, but this has been offset to some extent by the impact of high inflation on asset values – over the next ten years, 51% of expected portfolio returns have an inflation link. It is worth noting that the inflation expectations TIG is using are currently lower than those of in the market, so this suggests prudence and the potential for write-ups should the market be right. Like UKW there are risks to the NAV should we see further rate hikes, but like UKW we think the offsetting features to bonds (which have this risk in spades) are highly attractive.

Conclusion

Bonds add a lot of value to a portfolio, and if they are bought when the conditions are right, can deliver exceptional returns. Their generally lower volatility than equities means that improvements to a portfolio’s risk-adjusted returns can be particularly striking. However, we think investors would be mistaken to commit entirely to conventional fixed income at this juncture – especially high yield, or long duration bond portfolios. The outlook for rates and the pricing in the market means that significant risks abound and we think bonds are unlikely to perform as well as they did post GFC. On an income basis, we think there is a strong case to be made for diversification to avoid the heavy duration risk in conventional bond markets, while credit markets seem to have already baked in an economic recovery. Bond-like alternatives look like attractive components of a diversified bond-like sleeve in a portfolio. In particular, the discounts they are currently trading on make them look cheap in our view, and add to the long-term return potential.

")

")