With just one Trust to declare a dividend for July, the total for dividends received will be £6,579.00

Snowball fcast 8k

Target 9k a yield of 9% on capital invested.

Investment Trust Dividends

With just one Trust to declare a dividend for July, the total for dividends received will be £6,579.00

Snowball fcast 8k

Target 9k a yield of 9% on capital invested.

Dividend Declaration

The Board has approved a fourth dividend of 1.5 pence per share, bringing the total dividend for the period ending 31 March 2024 to 7.5 pence per share as per the dividend target of 7% of average NAV over the reported period. Based on the 31 March 2024 share price, this dividend was equal to a 11.6% yield.

The ex-dividend date will be 27 June 2024, and the record date is 28 June 2024. The dividend will be paid on or around 15 July 2024.

Dividend Policy

Subject to the applicable requirements and restrictions contained in the Companies Law, the Company may consider making interim dividend payments to Shareholders, having regard to the net income remaining after the potential reinvestment of cash or other uses of income, at a level the Directors deem appropriate, in their sole discretion, from time to time. There is no fixed date on which it is expected that dividends will be paid to Shareholders.

It is the intention of the Company to continue to pay a stable quarterly dividend with the potential for additional payments if investment returns permit

| R9owyn ibbspor.com kandicebliss@rediffmail.com | Hey! Do you use Twitter? I’d like to follow you if that would be okay. I’m absolutely enjoying your blog and look forward to new updates. |

Experts discuss the differences between the two global equity income trusts and share their preference.

By Jean-Baptiste Andrieux

Reporter, Trustnet

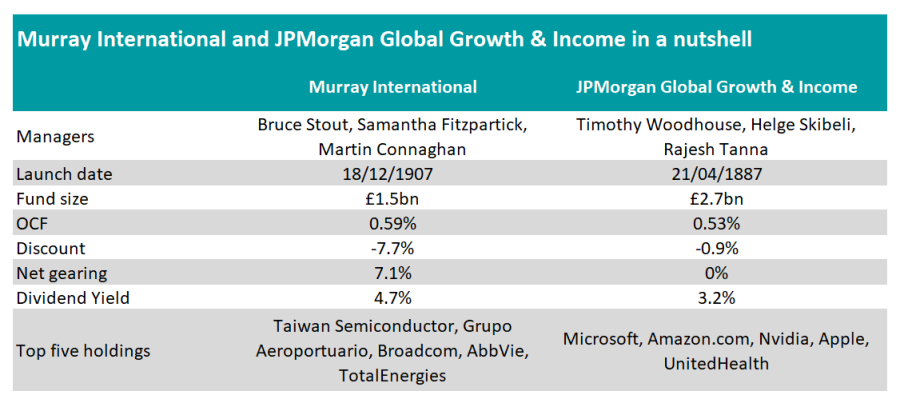

Murray International and JPMorgan Global Growth & Income have built a strong following over the years and are, as such, the two largest investment trusts in the IT Global Equity Income sector.

However, the two trusts built their reputations under very different circumstances.

Murray International is managed by abrdn’s Bruce Stout, who will retire at the end of this month and is being replaced by Martin Connaghan and Samantha Fitzpatrick. Stout made a name for himself during the global financial crisis, its peers and the broader market by focusing on high-quality companies and valuations.

Since 2014, however, Murray International’s performance has been subdued, placing it in the bottom quartile of its sector over the past 10 years.

JPMorgan Global Growth & Income has established its reputation through consistency; it has outperformed its benchmark in nine of the past 10 calendar years and is by far the best-performing global equity income investment trust of the past decade. This strength has enabled the trust to absorb several competitors in recent years, such as Scottish Investment Trust, JPMorgan Elect and JPMorgan Multi-Asset Growth & Income, and to issue new shares at a premium.

Performance of trusts over 20yrs and 10yrs vs sector and benchmark

Source: FE Analytics

These contrasting experiences imply a different approach to investing: Murray International operates as a conventional income portfolio, while JPMorgan Global Growth & Income takes a more flexible approach. In the event of an income shortfall, the trust’s capital reserves are used to top up the dividend – a practice that enables JPMorgan to invest in companies with a lower yield but greater prospects for long-term capital growth.

David Johnson, analyst at QuotedData, said: “Because of their different approaches to dividends, JPMorgan Global Growth & Income is able to invest in a much broader range of lower-yielding companies such as tech firms. Therefore, it has been able to offer investors exposure to non-dividend payers while still offering a 4%-ish yield.

“Murray International, on the other hand, has a more conventional income portfolio, investing in high-dividend payers. This means that it has historically had a strong bias to value stocks, while JPMorgan Global Growth & Income has been much more malleable, currently having a growth-stock bias, including a large allocation to US technology.”

He warned, however, that JPMorgan Global Growth & Income’s flexibility to invest broadly may make the constituents of its portfolio – and therefore its performance – less predictable.

Its shares have been less volatile than Murray International’s, but that may be because JPMorgan Global Growth & Income tends to trade fairly close to NAV, Johnson added.

According to FE Analytics, JPMorgan Global Growth & Income is currently trading at a 0.9% discount and has had a volatility of 15.4% over the past five years. By comparison, Murray International’s discount stands at 7.7% and it has experienced a volatility of 19% over the same period.

Although the aforementioned factors may seem to favour JPMorgan Global Growth & Income, investors should note that it currently has a lower yield of 3.2%, compared to Murray International’s yield of 4.7%.

Moreover, the fact that JPMorgan Global Growth & Income tends to trade close to NAV or even at a premium means it is particularly exposed to derating risk, according to Mick Gilligan, head of managed portfolio services at Killik & Co.

“Because of the derating risk (the discount was as wide as 15% back in 2016) investors should take an extra-long term view with this one,” he cautioned.

Which trust should you pick?

Albeit belonging to the same sector, the two investment trusts are distinct propositions that cater to different types of investors.

For instance, JPMorgan Global Growth & Income has a stronger track record of providing a balanced combination of capital growth and income. Therefore, it would be a more suitable option for investors seeking a blend of these two elements.

Gilligan added: “JPMorgan Global Growth & Income has more of a growth bias and should be attractive to investors that believe interest rates have peaked and are likely to decline in the months ahead.”

Conversely, Murray International is likely to be a better fit for investors who prefer a value-focused approach and a more conventional income strategy, where dividends directly reflect portfolio income generation, according to Emma Bird, head of investment trusts research at Winterflood.

“In addition, Murray International trades on a considerably wider discount, so is more likely to appeal to investors looking for a value opportunity,” she added.

Source: FE Analytics

Nonetheless, Bird’s preference is for the JPMorgan investment trust, due to its “impressive long-term performance record”, which she expects to continue.

“With a market cap of £2.7bn, the fund offers a large, liquid, low-cost vehicle, with an ongoing charges ratio of just 0.50%, the lowest in the Global Equity Income peer group,” Bird said.

“In our opinion, the fund’s enhanced dividend policy, which targets an annual payment of at least 4% of the previous year-end NAV, makes good use of the investment trust structure, and the fund currently provides an historical yield of 3.4%.”

Johnson favours JPMorgan Global Growth & Income as well. He also mentioned sector peer Invesco Global Equity Income, which he said now follows a very similar approach, following a recent restructuring.

However, Gilligan picked Murray International, which is his preferred trust in the sector. His choice is primarily due to the larger discount, but also partly because value stocks look particularly cheap relative to growth stocks.

“Murray International has a value style and so is better suited to investors that are less optimistic about the path of interest rates. It is also attractive for investors that need a growing income, given its record of dividend increases and scope to continue them,” he concluded.

However, Gilligan picked Murray International, which is his preferred trust in the sector. His choice is primarily due to the larger discount, but also partly because value stocks look particularly cheap relative to growth stocks.

Fans of Warren Buffett taking his photo Provided by The Motley Fool

Investing in the stock market can seem daunting. But by turning to Warren Buffett for some inspiration, I think many issues that seem complex can be simplified.

Buffett is one of the most successful investors of all time. Starting with a tiny sum aged just 11, the ‘Oracle of Omaha’ has gone on to build a fortune above $120bn.

Now, unfortunately, the chances of me amassing a fortune similar to Buffett’s are slim. However, that’s not to say I should ignore what he says and the actions that he’s taken. His advice can help retail investors starting out with small sums to try and beat the market.

If I were to start from scratch today, here are the three Buffett tips I’d follow.

Be consistent

Beginning without any existing capital may be demotivating. But investors can still build up large sums starting with minimal outlay. The key to this is consistency. I’m aware that putting money aside at the end of every month and investing it is vital to growing my pot.

I’d also take steps such as always reinvesting my dividends. From this, I’d benefit from compounding, which means I’d be earning interest on my original investment as well as my returns. With this, I can build my nest egg up more quickly. On multiple occasions, Buffett has pinpointed the power of compounding as a key reason for his wealth accumulation.

Long-term vision

Coupled with consistency is investing for the long run. It’s easy to be tempted by online advertising promoting quick gains in the stock market via methods such as day trading. But the market has proved time and time again the best way to see rewards is to buy stocks and hold them for years and decades.

We’ve experienced major volatility in the last few years. And I’m certain 2024 will be similar. From interest rates to conflicts and elections, there are plenty of events that will impact the market this year. However, by remembering my goal, I can ignore short-term peaks and troughs in favour of long-term gains.

Buffett once said: “If you don’t feel comfortable owning a stock for 10 years, you shouldn’t own it for 10 minutes”. I factor this into every investment decision I make.

Ready to pounce

Buffett also said it’s good to “be greedy when others are fearful”. And this is another piece of advice I think is important.

What he essentially means when he says this is to capitalise on opportunities that other investors may be turning their backs on. While 2024 may be volatile, with that comes the opportunity to buy cheap shares.

£££££££££

Also there are more important things in life than investing.

Schroder European Real Estate Investment Trust plc, the company investing in European growth cities and regions, announces its half year results for the six months ended 31 March 2024.

Portfolio indexation underpins earnings growth and 109% covered dividend, supported by low-cost, fixed-rate debt profile

| · | Underlying EPRA earnings increased 3% to €4.3 million on the prior six month’s EPRA earnings of €4.2 million (31 March 2023: €3.8 million), primarily due to rental growth offsetting the impact of higher interest costs |

| · | Two quarterly dividends of 1.48 euro cents per share (‘cps’) declared, bringing the total dividends relating to the period to 2.96 euro cps, 109% covered by EPRA earnings |

| · | Net Asset Value (“NAV”) of €165.3 million, or 123.6 cps, (30 September 2023: €171.4 million or 128.2 cps), largely driven by continued outward yield movement of the underlying portfolio |

| · | NAV total return of -1.3% based, in part, on an IFRS loss of €2.2 million (31 March 2023: -4.7% total return/€8.7 million IFRS loss) |

| · | Strengthened balance sheet with completion of all near-term refinancings on attractive terms, with no further debt expiries until June 2026 and a low average interest cost of 3.2% |

| · | Low Loan to Value of 24% (net of cash), and €26 million of available cash, provides significant flexibility |

Dividend:

· 11% increase in total dividends paid of 8.35p per ordinary share for the twelve months ended 31 March 2024 (31 March 2023: 7.52p).

· Dividend cover for the twelve months ended 31 March 2024 was 1.3x (31 March 2023: 1.4x).

· Increased target dividend to 8.43p per ordinary share for the year ending 31 March 2025.

· Attractive high dividend yield of c.11%, as at closing share price on 17 June 2024.

· Forecasted target dividend cover of 1.1x – 1.3x for the year ending 31 March 2025.

· Total ordinary dividends paid since IPO of £345m or 67.8p per share.

NextEnergy Solar Fund Limited

(“NESF” or the “Company”)

£20 Million Share Buyback Programme

The Board of NextEnergy Solar Fund, a leading specialist investor in solar energy and energy storage, is pleased to announce that it has approved an initial share buyback programme (the “Programme”) of up to £20 million.

The Board believes that the Company’s current level of discount to its Net Asset Value (“NAV”) is unjustified. Based on the historical and projected financial and operational performance of the Company’s diversified high-quality solar plant portfolio and the recent data points from the Company’s asset sales, the valuation of the Company’s underlying NAV remains robust. The Board continues to maintain a disciplined approach to capital allocation and considers the Programme to be in the best interest and value to its shareholders at this point in time.

The Board will continue to review the Company’s discount to NAV alongside the Company’s level of gearing and maintain full discretion and flexibility over future increases to the size of the Programme.

The Programme will be carried out under the existing shareholder authorisation granted at the last Annual General Meeting for purchases of Ordinary Shares by the Company in the market for up to 14.99% of the Company’s issued capital. The Programme will be conducted within certain pre-set parameters including those prescribed by the Market Abuse Regulation 596/2014 (as it forms part of domestic law by virtue of section 3 of the European Union (Withdrawal) Act 2018 (as amended)) and Chapter 12 of the Listing Rules.

Helen Mahy, Chairwoman of NextEnergy Solar Fund Limited, commented:

“NextEnergy Solar Fund continues to maintain a strong financial platform in a challenging environment. After careful consideration and review, the Board of Directors have taken action aimed at narrowing the Company’s current share price discount to its Net Asset Value and implemented a Share Buyback Programme. We are confident that the Programme will strengthen the Company’s share price performance and are pleased with the ongoing progress against the Company’s strategic objectives, by completing the second phase of its Capital Recycling Programme. The Board and Investment Adviser view the current size of the Company’s discount to NAV as unjustified and this Programme is in the best interests of our shareholders. The Board remains committed to maintaining a disciplined approach to capital allocation and continues to prioritise narrowing the discount.”

© 2026 Passive Income Live

Theme by Anders Noren — Up ↑