The Results Round-Up – The Week’s Investment Trust Results

Among this week’s results, CT Global Managed Portfolio’s Chairman gets his wish; Scottish American tells a fable; while Pantheon International looks to bust a myth or two.

ByFrank Buhagiar•02 Aug, 2024•

CT Global Managed Portfolio (CMPI/CMPG) waiting for sentiment to improve

CMPI/CMPG’s Annual Report presumably includes twice as many numbers as most other funds. That’s because the trust, which invests in other investment companies, is comprised of two share categories: Income (CMPI) and Growth (CMPG). NAV total return for CMPI came in at +7.0%; CMPG +12.7%. Neither could match the FTSE All-Share’s +15.4%. But over the longer term, CMPG has returned +271.5% over the 15 years to 31 May 2024 (+9.1% compound per year). That beats the FTSE All-Share’s +242.5% (+8.6% compound per year).

Alternative investment companies partly to blame for the underperformance over the latest full year. As Chairman, David Warnock, writes “Discounts remained wide and interest rates which stayed ‘higher for longer’ led to reduced NAVs and share prices.” Good job then, interest rates have peaked, although Warnock believes “It may require actual cuts to be delivered for sentiment to improve; however, it does appear a more favourable environment for equity markets is a distinct possibility.” Right on cue, CMPG’s share price rose on 01 August 2024, the day of the BoE’s first UK rate cut.

Winterflood: “Negative performance in both portfolios largely attributed to widened discounts over FY and the valuation impact from higher discount rates. Annual dividend +2.9% to 7.40p per share, representing 13th consecutive year of dividend growth.”

Smithson (SSON) painting a positive picture

SSON’s -1.8% NAV per share total return for the latest half year couldn’t match the MSCI World SMID Index’s +3.4%. Chair, Diana Dyer Bartlett, describes the performance as “frustrating”. The investment managers describe it as “like watching paint dry”. As the Chair explains “The performance of the MSCI World Index, which is driven by the performance of a small number of very large technology stocks, has been very strong. The MSCI SMID Index has returned 12.8% over that period, whilst the MSCI World Index has returned 31.6%.”

Bartlett still believes good returns can be delivered by investing in small and mid-cap stocks. And the numbers back this up: SSON’s +8.2% annualised NAV per share performance since inception nearly six years ago is 0.5 percentage points higher than the MSCI World SMID Index. As for the paint-watching, the investment managers add “While we may have to remain patient a little longer while the paint dries, we remain very optimistic that the picture will be worth it.” Seems the market agreed. Shares were in demand on the day of the results.

Numis: “We believe that the portfolio has sound fundamentals that place it in a strong position to outperform over the long run and that the shares offer value on a c.11% discount to NAV.”

Scottish American (SAIN), steady as she goes

SAIN posted a +5.5% NAV total return for the latest half year, a little off the benchmark’s +12.2%. Three reasons cited for the underperformance: “market sentiment”; “not owning certain non-yielding or deeply cyclical companies which have benefitted from the current environment”; and “SAINTS’ diversifying investments in property and other areas have underperformed equities”

The Interim Management Report puts the performance into context by drawing on the fable of the race between the hare and the tortoise – hare bounds ahead at the start but becomes so over-confident stops to take a nap. This allows the tortoise, who has maintained a steady pace, to overtake the hare and finish first. “We firmly believe that all is well: perseverance remains the name of the game. The underlying growth of the portfolio remains strong, if a little more ‘tortoise’ than the market’s ‘hare’. We remain staunch believers that focusing on companies which steadily compound their earnings and dividends ever-higher will stand SAINTS’ shareholders in good stead in the long-term.” Shares definitely a tortoise on results day, barely moved.

Winterflood: “A third of underperformance comes from cyclicals, and another third from not owning Nvidia. Infrastructure (-4.4%) and fixed income (-4.4%) portfolios showed negative returns while property (+3.1%) portfolio made a positive yet modest contribution through income generation.”

Pantheon International (PIN), busting myths

PIN reported a +6.1% increase in NAV per share for the full year. Growth was down to valuation gains but also from the private equity group’s £200 million buyback programme which added +4.7% to NAV. Over ten years, annualised NAV per share growth stands at +13.5%. The portfolio continues to perform well with underlying investments clocking up +17% EBITDA growth and +14% revenue growth. Growth just half the story. Avoiding losses the other and, here too, PIN has a strong track record. The fund’s realised and unrealised loss ratio for all its investments over the last 10 years is just 2.3%.

Chair, John Singer CBE, explains that, as well as the corporate objective to deliver an attractive risk-return over the long term, the fund is on a mission “to dispel the myths that have surrounded the private equity sector for so long”. So, PIN is increasing its marketing efforts to widen its appeal “And we will continue to do this in the spirit of transparency and communication”. That’s the spirit. Market liked what it heard too, share price ticked higher.

Numis: “PIN’s shares currently trade on a c.33% discount, which we believe offers significant value”.

JPMorgan: “Overall we like PIN’s approach to capital allocation and it remains one of our top picks among the diversified listed private equity companies. We remain Overweight.”

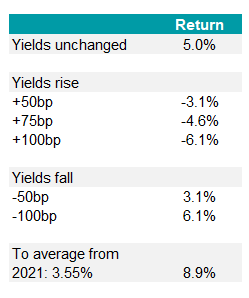

RIT Capital Partners (RCP), a fund built for the times

RCP Chairman, Sir James Leigh-Pemberton, described the flexible investor’s half-year investment performance as solid with the NAV per share increasing by 4.2% (including dividends). All three strategic investment pillars – Quoted Equities, Private Investments and Uncorrelated Strategies – performed positively. RCP’s objective is to grow shareholder wealth meaningfully over time, through a diversified and resilient global portfolio. And the numbers show the fund has delivered. “Since inception in 1988, our NAV has averaged an increase of 10.5% per annum (including dividends), with lower volatility than stock markets.”

Looking ahead, the investment managers are not worried about current geopolitical and economic uncertainty, as “Our portfolio is built for times like this – focused on capturing long-term growth opportunities while being resilient through diversification.” Shares showed resilience on results day, closing marginally higher.

Numis: “The discount remains wide at 26% and we believe this offers significant value given improved disclosure and communication, and evidence for progress with realisations in the private portfolio.”

JPMorgan: “We are Overweight RCP which is a constituent of our investment companies model portfolio.”

Henderson Smaller Companies’ (HSL) year of two halves

HSL reported above average NAV growth for the full year: +14.5% NAV total return compares favourably to the AIC UK Smaller Companies sector’s average of +14.1%. The full-year number does not tell the whole story, however. At the half-way stage, NAV total return was a negative 7.7%, meaning NAV put on +24.0% in the second half. Not enough to keep pace with the Deutsche Numis Smaller Companies Index (ex-investment companies). The 3.7% shortfall was put down to stock-specific issues, but fund manager Neil Hermon is not losing much sleep over it thanks to the robust operating performance of the portfolio companies, their sound finances and attractive valuations. Nor is the market it seems, shares only fractionally lower following the results.

Numis: “Henderson Smaller Companies remains one of our top picks within the UK smaller companies sector. We continue to rate the management team highly and believe that following a period of poor performance over the last 2-3 years, the manager is starting to reap the rewards of sticking to the Growth at a Reasonable Price investment approach.”

F&C Investment Trust (FCIT) maintaining balance

FCIT’s +13.2% NAV total return for the half year beat the FTSE All-World Index’s +12.0%. The Fund Manager’s Report highlights the performance of the Magnificent Seven tech giants – Alphabet +31.8%, Microsoft +20.4%, Amazon +28.4%, Apple +10.7%, Nvidia +151.9%, Meta +44.1% and Tesla -20.4% – not just because they have been driving markets, but because FCIT holds every single one of them with all but Tesla featuring in the global fund’s top-ten holdings.

Not that FCIT is putting all its eggs in the technology basket. For “the Company is well positioned to benefit from a broadening of the rally driven by improving economic momentum outside of the US. Our balanced approach within our portfolio across recognised styles, including value, growth/quality and momentum, provides our shareholders with a well-diversified, global equity investment portfolio”. Shares finished the day marginally lower.

Numis: “The fund has a reasonable track record, with NAV total returns broadly in line with the index over one, three and five years.”

JPMorgan: “FCIT also benefits from low fees and is one of the highest quality large cap global investment trusts. We are Overweight FCIT.”