Following July’s general election, the UK now offers a new diversification benefit, according to James Klempster, deputy head of the Liontrust multi-asset team. It has become “a relative haven of stability after nearly a decade of political uncertainty”.

“This reinforces our confidence in the UK stock market, which has been driven by valuations and the potential for capital flows,” he noted.

The UK’s role as a ballast within portfolios is partly due to its sector composition. The domestic market has more of a defensive, value tilt with higher weights to financial services, energy and healthcare, in stark contrast to the technology-heavy US market.

Furthermore, the power of dividend compounding in the UK equity market helps underpin returns, Cobbe pointed out. “Dividends are a major driver of total returns in the UK equity market given the slower earnings growth and lower multiples in the UK compared to the US, so for a defensive posture, a dividend-focused strategy such as VT Munro Smart-Beta UK fund should prove an even more effective diversifier in challenging markets,” he said.

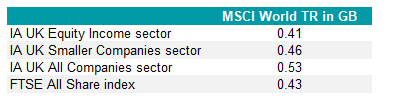

Equity income funds offer even greater diversification benefits to the broader stock market. The IA UK Equity Income sector has the lowest one-year correlation to the MSCI World amongst all of the Investment Association’s UK equity fund sectors, as the table below illustrates.

Correlations between UK equity sectors and the MSCI World Index over 1yr

Source: FE Analytics, data to 29 Aug 2024 in sterling terms

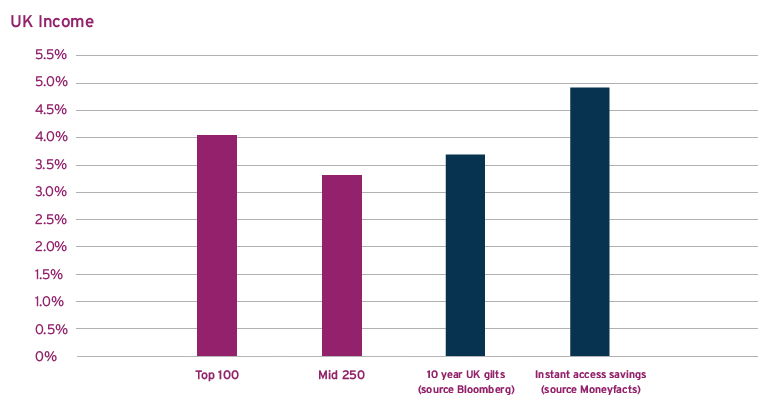

Dividend income from equities is set to become a more attractive source of income as the Bank of England cuts rates and yields on savings accounts and gilts falls commensurately. Computershare expects UK large-caps to yield 4% based on its forecasts for regular dividends in the year ending 30 June 2025, as the chart below illustrates.

Source: Computershare UK Dividend Monitor, Q2 2024 edition

While Cobbe argues that diversification is the main reason for an investment in UK stocks, Klempster is confident of the market’s potential to outperform. “We believe the UK could turn versus the other majors. It is hard to predict when, but to our mind it will not require a major catalyst. UK stocks have already had a relatively strong start to 2024 and its economy has surprised on the upside as the UK emerges from the shallow recession that started at the back end of 2023,” he explained.

Meanwhile, Ben Conway, chief investment officer of Hawksmoor Investment Management, thinks the most exciting aspect of the UK stock market is the level of valuation dispersion. “We find that the lower down the market-cap spectrum one goes, the cheaper stocks become,” he said.

abrdn European Logistics Income PLC ex-dividend payment date BlackRock World Mining Trust PLC ex-dividend payment date Capital & Regional PLC ex-dividend payment date CT UK Capital & Income Investment Trust PLC ex-dividend payment date Dunedin Enterprise Investment Trust PLC ex-dividend payment date Empiric Student Property PLC ex-dividend payment date JLEN Environmental Assets Group Ltd ex-dividend payment date MIGO Opportunities Trust PLC ex-dividend payment date Triple Point Energy Transition PLC ex-dividend payment date

Average expected return around 7.5%. Things to know if u want to trade.

VWRP accumulation ETF where any earned dividends are automatically re-invested.

From the covid low, if u bought in 2019 u were printing a low but that would be the same for most Trusts/ETF’s.

A definition of an uptrend a series of higher highs. With hindsight u can see when the ETF printed £90 it was reluctant to go higher, u do not need to know the reason why, just to realise it isn’t go higher yet (resistance).

Upon reaching resistance the chart has 3 options, to continue higher, go lower, or go sideways.

Once u realise it isn’t go higher, u can draw a line on your chart and wait for the price to go higher, sometimes there is a false breakout (bear trap) where the price goes above the line and then falls back, no one said making money is easy.

U can see there was no clear breakout for 2 years.

U could use the trading period to accumulate shares using your dividends or wait for the breakout, knowing that if u can choose the time to sell, that u will not lose any of your hard earned.

Chart resistance is clear to see, remember the 3 options. If u had accumulated under resistance, u may wish to take some of your profit or u may wish to hold for the hope of more profit.

U should make more in the last years of your Snowball, whatever time frame u use, so that’s why lifestyling is detrimental to your final retirement ‘pension’.

Remember falling markets are a plus as the price of Investment Trusts fall the yield rises.

Note: although it’s possible to have a Snowball yielding 8% at present it may not be possible to re-invest your dividends at the same rate.

In a rising market your Trusts should increase in value and u may be able to re-invest any profits back into your Snowball, thus achieving 8% compound growth. Of course any Trusts already in you Snowball will return the same amount of dividends gently increasing, hopefully, overtime.

Are dividend stocks the best way to earn passive income? Mark Cuban is a fan. by Mark David Hartley

The Motley Fool

Nasdaq recently published an article detailing Mark Cuban’s ideas on passive income. The world-famous investor is known for his role on Shark Tank and as the owner of the NBA basketball team, the Dallas Mavericks.

He made his fortune selling a tech startup during the dot-com bubble and has gone on to become a well-known and respected investor. The article outlines his preferred investment options, such as private equity, AI companies, and the S&P 500. As a contrarian investor, many of his ideas go against traditional advice.

But his feelings on dividends struck a chord with me.

He notes how their regular cash payments equate to real-world value. The best part is, that these payments can be reinvested to maximise gains through the miracle of compound returns.

With two dividends to be announced next week the Snowball fcast of 8k and target of 9k should be confirmed.

The fcast/target for next year can also be made an increase of 1k.

The current indication for dividends earned this year is around 10k but will depend on when the December dividends are paid, as some may be held back to be paid in January for tax purposes. This of course would give a boost to the 2025 fcast total.

If income of 9.8k is received this year that equals the year 2028 fcast so the Snowball will be well ahead of the plan and halfway to doubling the income.

Literacy Capital, BBGI Global Infrastructure, CT Private Equity and Chelverton UK Dividend Trust all reported this week, but which of the four is ranked No.1 out of ALL UK-listed investment companies in terms of NAV performance over the three years to June 2024?

By Frank Buhagiar•30 Aug, 2024

Literacy Capital (BOOK) Tops the Charts

BOOK’s Interim results for the six months ended 30 June 2024 opens with a one-line summary “Strong first half; celebrates third year anniversary with NAV performance ranked #1 out of all UK-listed investment companies.” As for what a strong first half looks like, how about a +4.4% NAV increase and +9.9% share price rise. That compares to the FTSE Investment Company Index’s +5.8% increase and the FTSE All-Share’s +7.4%.

And according to CEO, Richard Pindar, for the three years to June 2024 the fund was ranked #1, with its NAV performance being comfortably ahead of all other UK-listed investment companies. A thumbs up for BOOK’s strategy of “focusing on smaller businesses that are poorly served or ignored by traditional private equity funds, as well as the benefits that our fund structure can deliver to portfolio companies and BOOK’s shareholders. We believe it is worth continuing to emphasise these points, as they are still not widely understood by the market.” And right on cue, share price was unmoved on the day of the results. But more numbers like the above and likely won’t be too long before the market sits up and takes notice.

Winterflood: “Manager sees signs of UK domestic trading conditions improving. NAV TR +49% p.a. since IPO in June 2021; top performer across all UK investment trusts.”

BBGI Global Infrastructure (BBGI) Keeps Delivering

BBGI reported a +2.4% NAV total return for the six months to 30 June 2024. Other financial highlights at the half-year stage include zero drawings on the revolving credit facility; net cash of GBP20.6 million; and a 6% dividend increase. And it was the dividend that Chair, Sarah Whitney, chose to focus on “Our high-quality inflation-linked cash flows generated by our portfolio of availability-style core infrastructure assets has enabled us to meet consistently or exceed dividend targets since the IPO in 2011, providing our shareholders with predictable, progressive and fully cash-covered dividends for over a decade.” Whitney goes on to note how, at the current share price, the shares offer FY 2024 and FY 2025 dividend yields of 6.3% and 6.4% respectively.

CEO, Duncan Ball, meanwhile has his eyes fixed on the future “Stabilising, and potentially reducing interest rates, combined with an ever-increasing demand for infrastructure investments, presents a long-term growth opportunity for BBGI.” Shares barely budged on the day of the results – market clearly focusing on the long term.

Jefferies: “The portfolio valuation was little changed over the half, while cash flow generation was typically robust.”

Liberum: “The results were largely as expected with limited changes from the FY 23 results. We continue to prefer: (1) infrastructure funds with a higher terminal value and better scope for earnings growth at the investment level which can drive NAV growth.”

Winterflood: “With the shares trading at a current discount of 8% (relative to 11% 5-year average premium), we believe that BBGI is undervalued and hence we continue to recommend the fund for core Infrastructure exposure.”

Investec: “The portfolio continues to perform well operationally and financially, and the company remains well positioned with a conservative balance sheet. We remain comfortable with our Hold recommendation.”

Numis: “We view BBGI as a high-quality business but maintain a preference for the revenue diversification and higher inflation linkage on offer elsewhere in the Core infrastructure sub-sector.”

CTPE noted a pick-up in realisation activity during the first half – realisations and associated income came in at £52.3m, a +31.4% increase on the same period last year. What’s more, realisations were struck at a 35% premium to prior valuations. Other half-year vitals include a +0.8% NAV total return; and a 6.5% dividend yield based on the period-end share price. Letting the side down, however, a -4.5% share price total return on the back of a widening discount. Chairman, Richard Gray doesn’t sound overly concerned though, as “there now appears to be a mild but definite pick-up in activity.” This includes a “substantial increase in realisations over the course of this reporting period with some more significant ones to come in the near future.” As for why this is important “Realisations are usually at a significant premium to recent carrying value and so have the benefit of enhancing NAV as well as strengthening the balance sheet and creating more shareholder value.”

And doesn’t sound like reinvesting the proceeds from realisations will be all that hard either “There are many investable funds and co-investments being appraised by our managers. Experience shows that investments made during, or immediately after, economic slowdowns usually perform very well.” Market liked what it heard – shares tacked on 11.5p on results day to close at 454p.

Winterflood: “In our view, realisations of c.10% of NAV YTD at a +35% uplift offer transactional evidence to support the prevailing NAV, which is particularly relevant given a 36% share price discount, and represents a continuation of the trend across the sector.”

JPMorgan: “The shares are trading at a headline discount of 34.7%, but taking into account proforma net debt the implied discount on the unquoteds is narrower at 30.2%. This looks about fair relative to peers in our view and therefore we see no need to change our Neutral recommendation.”

Chelverton UK Dividend Trust’s (SDV) Year of Two Halves

SDV’s NAV total return of -7.5% for the full year doesn’t tell the whole story. For performance at the UK equity income trust picked up markedly in the second half of the year with NAV rising +20.3% in the six months to 30 April 2024, a nod to the improvement in sentiment seen towards the mid and small-cap stocks that SDV invests in. And according to the Investment Manager’s Report, the majority of the fund’s portfolio companies “continue to trade profitably, generate significant levels of cash and pay dividends.”

The relatively strong operational showing at the portfolio company level is not going unnoticed if an uptick in corporate activity is anything to go by – six of the fund’s holdings were the subject of corporate activity in the year to April 2024. The investment managers don’t sound 100% happy about this though “We must also hope that we do not lose too many of our holdings to takeovers at prices which do not reflect the full medium-term potential of the business. As long-term, fundamental investors, we would far rather continue to back the management teams of growing, cash generative businesses, than settle for a quick return based on current low levels of valuation.” Results were good for an initial 3p spike in the share price to 172p.

Winterflood: “Ordinary shares moved from 3.8% premium to 6.5% discount; 395k shares issued at a premium over FY. 2025 ZDPs moved from 4.6% to 6.3% discount.”

How much do I need to invest in UK shares to stop working and live off passive income?

Story by Royston Wild

The Motley Fool

To my mind, the best way to try and create a passive income is to invest in a broad range of UK shares.

What about savings accounts? Well, with interest rates falling again, I’m expecting these products to start delivering mediocre returns again.

Past performance is no guarantee of future returns. But with the Stocks and Shares ISA delivering an average annual return of 9.64% (according to Moneyfarm research) in the past decade, I think building a portfolio of British stocks will be the best way to go.

But how much would I need to invest so I can stop work and live off the passive income?

Hitting a £50k income

The first thing I need to consider is how much my everyday expenses will be. I also must think about what luxuries I want to enjoy. After all, none of us want to work for decades without having some lavish living to look forward to.

It says the average single person needs £43,100 a year to live a comfortable retirement. People in this bracket will get to enjoy regular holidays in the UK and overseas, a new car every few years, and a four-figure kitty to spend on clothes.

For this exercise, I’ll round my annual income target up to £50,000 to give me a margin of safety. So how much will I need to invest each year to reach this?

If I can manage to hit that 9.64% average return that ISA investors enjoy, I’ll need to spend £8,376 a year on UK shares for 25 years, reinvesting any dividends I receive along the way.

At this point, I’ll have built a nestegg north of £833,420.

Source: thecalculatorsite.com

I could then invest this in 6%-yielding dividend shares to target just over £50,000 in passive income each year. Remember, however, that dividends are never guaranteed.

Demand for FTSE 250 shares has risen sharply in 2024 thanks to the improving UK economic outlook. This pickup probably isn’t a surprise. Around 60% of the index’s earnings come from Britain.

The UK’s second-most-prestigious index has consequently risen around 7% in value in the year to date, pushing valuations higher. But don’t be mistaken, there are still many great bargains for investors to go hunting for.

Buying cheap shares has two significant advantages. Undervalued stocks can deliver stunning capital appreciation over time as the market wises up to their cheapness and share prices soar.

Value shares also provide investors with a margin of safety. If a company suddenly experiences adverse conditions, the scale of share price losses can be far more limited.

Value shares also provide investors with a margin of safety. If a company suddenly experiences adverse conditions, the scale of share price losses can be far more limited.

Solar star

Solar star The threat of higher-than-normal interest rates means property and infrastructure companies like NextEnergy Solar Fund (LSE:NESF) remain ultra cheap.

This particular investment fund — which owns more than 100 renewable energy assets mainly in the UK — trades at a 20.2% discount to the estimated value of its assets.

While they’re not without risk, renewable energy stocks like this have terrific long-term potential. As the climate emergency worsens, demand for their power should rapidly increase. This makes NextEnergy worth serious consideration, and especially at current prices.