Market reaction when companies cut their dividend.

Full year dividend rebased to 2.0 pence per share:

· With macroeconomic uncertainty continuing and interest rates now expected to remain elevated for some time, the Board has taken the decision to rebase the dividend to a level that is sustainable and substantially covered by adjusted earnings over time. The additional financial flexibility will enable the Group to effectively progress its strategy to deliver on the value accretive opportunities it has created.

· The Board has therefore declared a second interim dividend of 1.0 pence per share, bringing the total dividend for the year to 2.0 pence per share. This will be paid as an ordinary dividend on 13 May 2024, with an ex-dividend date of 4 April 2024. The Board will look to maintain a sustainable dividend going forward, with the intention that future dividends reflect the progression in underlying earnings.

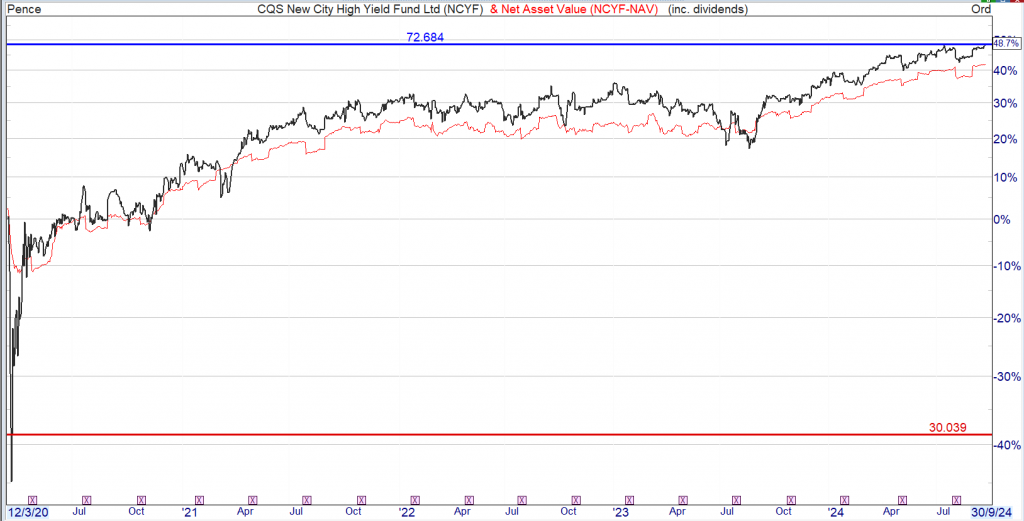

Watch to see if they maintain the dividend, which should be a yield of around 6% and then decide if the risk versus/reward is worth taking the trade for the huge discount to NAV.

If the dividend isn’t maintained the discount to NAV could widen ever further. But as always best to DYOR as it’s your hard earned.

Income and ESG-focused investors shouldn’t dismiss the real estate revival…

David Brenchley

Updated 21 Sep 2024

Disclaimer

Disclosure – Non-Independent Marketing Communication

This is a non-independent marketing communication commissioned by Schroder Real Estate. The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

It’s been a tumultuous few years for the commercial property market, but signs are there that a corner has been turned and things are looking up.

If you’re reading this during your working day from the comfort of your home office for some light relief in between Zoom calls and taking in Amazon packages, it may not feel like that’s the case, but hear us out.

It’s true that office and retail buildings have been hit because working from home remains a popular option for many employees and e-commerce is still in the ascendency. Yet, as we will explore here, the reality is more nuanced.

In addition, rising interest rates have undoubtedly had an impact on real estate investment trust valuations, but they finally look to have peaked, meaning the direction of travel is reversing.

Certainly, valuations, on average, of most property sectors are now starting to climb in earnest and there’s a feeling that we’re at the foothills of exciting times for real estate investors.

Green shoots

We’ve touched on a few of the headwinds that have contributed to falling property capital values. The MSCI UK Monthly Property Index has fallen some 25% in the past two years, with offices taking the brunt of that and falling 32%. Industrial properties are down 27% and retail premises have fallen 20%.

However, property has a key role to play within certain portfolios and as we start to see interest rates drop, there are plenty of positives for the asset class moving forward.

Rental growth remains strong

The first thing to note is that while property values have been falling over the past couple of years, rents have been rising. Indeed, overall rental values have risen about 7.5% in the past two years, with rents in the industrial sector (which include logistics assets) up 15%, office rents rising 4% and retail up 1%.

Rents have been rising

Source: MSCI UK Monthly Property Index

This has happened largely because there is a lack of good-quality buildings. In addition, the fact that rising build costs means there aren’t enough new buildings in the pipeline to bridge the supply-demand imbalance we see in commercial property should see rents continue to grow.

This is important because, as we will discuss later on, rents provide real estate investment trusts (REITs) with their income-generating quality, which is a key component of their total returns, and their attractiveness to investors.

As you can see from the previous chart, most of the fall in capital values happened in 2022, with 2023 being a year of consolidation. This year has been more positive, with values rising through the second quarter of 2024. As things continue to improve, the worst may finally be behind us.

If rising property valuations pick up, this should feed through positively to REIT net asset values. Add this to the rental picture, and total returns from the sector could start to look much better moving forward.

Interest rates are reversing

We mentioned before that the rapid rise in interest rates that we saw from the end of 2021 has been negative for the property sector. Interest rates in the UK went from 0.1% to 5.25% in the space of 18 months.

This caused a repricing in REITs because higher interest rates increase the cost of their debt while simultaneously increasing the income available from lower-risk assets such as government bonds. Higher interest rates have also crimped spending in the economy and made it harder to finance debt.

Some relief came in August, when the Bank of England cut interest rates to 5%. There may not be another cut in September, but we’ve almost certainly hit peak rates and are likely to see them return to a downward trend.

This should take some pressure off consumers’ wallets and give them more money to spend in the economy while also having a positive effect on property financing through lower mortgage rates and cheaper costs of finance for investors.

Income advantage

A second-order effect of falling interest rates is that the interest paid on savings accounts has started and will continue to drop. The 5% that you could get from a bank, money market fund or government bond has largely disappeared and been replace by somewhere around the 4% mark.

As this carries on falling, more people could start to consider investing in real assets again. There are plenty of places in the investment company space to find a yield north of the 3.9% that a 10-year gilt pays.

REITs are perfectly placed to take advantage of this. Most of the companies in the AIC: Property – UK Commercial sector have yields between 6% and 8.5%, meaning they can provide both a decent premium over the 10-year gilt yield and diversification away from an equity-heavy income portfolio.

A good rule of thumb when valuing commercial property assets is to compare their yields with the 10-year gilt yield. Often, a 150 to 200-basis-point premium over the 10-year gilt is seen as the ‘right’ number. The fall in the gilt yield may mean that there are opportunities within UK commercial property investment companies, but investors must make that judgement themselves, on a case-by-case basis.

Taking Schroder Real Estate (SREI) as an example, earlier on in the interest rate cycle, our analysts thought that the share price was around the right level, with SREI’s underlying property yield at around the same level as the 10-year gilt.

Today, things look more interesting. SREI’s underlying property yield is 6.1%, putting the valuation at the ‘right’ level and suggesting that the current share price undervalues the portfolio.

The need for active management

Real estate should certainly not be dismissed. For all its challenges, a thriving property sector will always be necessary.

Employees might value having the option to work from home on Mondays and Fridays, for instance, but they still need an office to go to for some of the week, at least. Some 88% of full-time central London office workers go into the office at least one day per week, according to the Centre for Cities think tank.

Hybrid working

Source: Centre for Cities

In addition, e-commerce hasn’t had a negative impact on all sectors or retail. Internet shopping will struggle to replace convenience stores in airports and train stations, for example, while out-of-town stores selling bulkier items such as garden furniture and DIY items remain defensive areas of the market.

Working from home has also been a benefit for high streets in wealthier catchment areas, while there have been positives to the rise of ecommerce, particularly where logistics spaces are concerned. These are buildings such as warehouses and distribution and fulfillment centres where goods sold online are stored, picked and distributed. Logistics assets make up a large part of the industrials sector.

This is why it’s important to seek out real estate portfolio managers that are skilled at proactively managing their property portfolios. An additional challenge is how they repurpose outdated and obsolete property spaces into buildings that are fit for the 21st century.

Capturing the green premium

One factor that real estate lends itself to is on environmental, social and governance (ESG) grounds. You can be much more impactful for ESG in real estate than in many other asset classes.

The first point to make here is that real estate has one of the highest carbon footprints of any sector of the economy. The built environment generates 40% of global carbon emissions every single year, according to the International Energy Agency (IEA). Building operations are responsible for 27%, while building, infrastructure materials and construction – typically referred to as ‘embodied carbon’ – are responsible for 13%.

Most of today’s building stock in the UK will still be in use in 2050, meaning that decarbonising the real estate sector is a crucial objective if we want to reach net zero carbon emissions by 2050 and to achieve the Paris Agreement’s target of limiting global warming to 1.5°C above pre-industrial levels.

Fortunately, it’s possible to profit from the transition from brown to green, with the right strategy and management team.

The green premium refers to the fact that environmentally efficient buildings can command both higher capital values and better rental yields than property in the same location of a similar age with a larger carbon footprint.

The green premium for London offices is about 20%, for regional offices it’s 8% and for multi-let industrials it’s between 5% and 10%. It works with rents, too. Each additional step improvement in energy performance certificate (EPC) ratings results in an average 3.7% increase in capital values and a 4.2% increase in rent for London offices, according to JLL.

Essentially, investors are prepared to pay higher prices for buildings with strong sustainability credentials because they tend to be rented out more quickly and have higher occupancy rates. They are, of course, less at risk of obsolescence from ever-tightening environmental regulation.

In real estate, ESG isn’t just a box-ticking exercise; it’s a clear and sustainable investment strategy that delivers modern buildings that are fit for purpose while increasing returns for investors.

The green premium in action

SREI has repositioned its investment strategy to capture and harness the green premium. Shareholders approved the addition of sustainability KPIs to the investment objective in December 2023.

The company aims to deliver a mixture of income and capital growth while achieving meaningful and measurable improvements in the sustainability profile of the majority of the portfolio’s assets. Over recent years they have increased their exposure to multi-let industrial estates that now represent over half the portfolio value.

Managers Nick Montgomery and Bradley Biggins believe that there is a significant green premium on the right property assets in the UK, with tenants willing to pay more for energy efficient buildings and for a good environment for employees. This is where active asset management of a property portfolio really comes into play.

The Stanley Green industrial asset in Cheadle, Greater Manchester, is a key example of SREI’s brown-to-green strategy in action. The asset was bought in late 2020 for £17.3 million. At the time it had a 150,000 sq ft warehouse space, trade counter units and a 3.4-acre development site.

A further 11 units were added in May 2023, bringing the asset’s total space to around 229,000 sq ft. SREI made sure that it minimised the carbon used during the construction phase and designed the units to be as efficient as possible for its future occupiers. This included using partly recycled cladding that is highly thermally efficient, and adding in a higher proportion of roof lights and more natural light, which means it requires less energy.

The units have air source heat pumps, which absorb heat that is then used to generate heating and hot water for the warehouse. There are also rooftop solar panels across the site, where any unused power is sold back to the national grid. Those solar panels also power the 24 electric vehicle charging points.

The new units achieved an A+ EPC rating and an Excellent accreditation from the independently run Building Research Establishment Environment Association Method (BREEAM).

Stanley Green was last valued at £40 million on 31/03/2024, which gives a reversionary yield of 6.4%. Capital expenditure on the project totalled £9 million. In addition, a 4,000 sq ft unit on the existing estate with EPC ‘C’ rating was recently let at £14 per sq ft, whereas the comparable operationally net zero carbon units with EPC ‘A+’ have been let at around £19.50 per sq ft, reflecting a 39% premium.

At the time of writing, the site is partially let with negotiations for the rest of the site underway. The goal is to have it fully let by the end of SREI’s current financial year.

Nick and Bradley’s knowledge of the industry is reflected in the sectoral make-up of the portfolio: while many peers are reducing their office exposure, SREI is maintaining its exposure in line with the benchmark index, albeit with almost half the office space used for university and other non-traditional office uses. Lots of parts of the office market are struggling at the moment, but others, particularly those that pay attention to ESG-related factors, are still seeing demand. With SREI’s more explicit ESG strategy now in place, the office sector could be a significant opportunity for the trust in the coming years.

Diversification

Up until now, we’ve been focusing on the UK market, because almost all the UK-listed REITs focus on the UK, a specific country or a specific sector. As with any investment portfolio, though, it’s important not to put all your eggs in one basket. Diversifying away from the UK brings plenty of benefits.

Broadening your search out just a little bit can bring positive results. Consider hopping across the English Channel and adding some exposure to Europe, for instance.

The Continental European real estate market is much larger and more diverse than the UK market. France and Germany have large and mature office and industrial markets , while the Netherlands is home to Rotterdam, Europe’s largest seaport, which has an abundance of industrial and logistics assets.

A unique offering

As the only generalist REIT focused on Europe, Schroder European Real Estate (SERE) is a compelling proposition for investors who want to diversify their property exposure beyond UK shores.

SERE has a balanced portfolio across the main sectors of office, industrial, and retail, with exposure focused on growth cities in Germany, France, and the Netherlands.

This diversification allows the managers to search in a much bigger pool of opportunities. A recent acquisition that few other REITs would be able to make was that of a car showroom in Cannes, France, for example.

Manager Jeff O’Dwyer argues that demand for property is increasingly concentrated in ‘winning cities’, which is where he and Schroder Capital’s team of c. 200 real estate professionals focus.

Winning cities tend to give the trust access to competitive advantages. They often have a good diversity of business, a deep talent pool, show good governance and infrastructure and hence generate above average economic, employment and population growth. Some of the trust’s assets are in smaller economies that boast higher-value industries.

Active management is important here because winning cities change over time. Jeff has over 25 years’ experience in real estate including over 20 years in Europe, with periods of working in Germany and Italy, as well as Australia and New Zealand. The wider team is based in cities such as Paris, Frankfurt, Munich, Amsterdam, Stockholm, and Zurich.

SERE is also able to create value by repositioning assets. It recently upgraded one office building in Paris to a higher technical standard, spending less than €40 million buying the building, investing about €30 million in upgrading it and selling it for more than €100 million. The 39% uplift in rent and 35% profit when it was disposed of allowed SERE to pay shareholders a special dividend.

Looking ahead

It’s been a tricky few years for property investors, with a changing environment and the risk of obsolescence for many sectors. However, REIT managers have shown a remarkable ability to move with the times, repurposing buildings to become fit for purpose in an ever-changing world.

As some of the headwinds that have contributed to historically wide discounts for REITs dissipate and conditions become more favourable, investors are likely to start focusing again more on the sector’s more enduring characteristics, such as its income-generating ability, inflation-linked cashflows and

I’m really impressed together with your writing abilities as smartly as with the structure for your blog. Is that this a paid subject or did you modify it yourself? Anyway keep up the nice high quality writing, it is rare to peer a great weblog like this one today..

£££££££££££

WordPress currently charge £7.20 per month, although this was discounted for the first 6 months.

The above portfolio is what a de-accumulation portfolio might look like, yours may be different. This information is being repeated as new readers join the blog to follow the Snowball, welcome all. When the next market crash arrives u should be ready.

Working Example

If u bought at 30p for the yield, as the price may have continued to fall

2020 dividend 4.46p a yield of 14.9%

This years expected dividend 4.5p a yield of around 15% on the buying price but as the price rises the yield falls so a running yield of 8.57%

If u include the dividends earned but not re-invested in the Trust u have more than doubled the amount u invested. Of course the one consideration u would have needed funds to re-invest and as most Trusts fell in unison, I’ll leave that with u to come up with a solution.

The current planned dividends for the GetRichSlow Snowball portfolio. As always best to DYOR as mistakes can creep into published information. If u are nearing your de-accumulation stage, ‘secure’ dividends are more important than owning Trusts trading at a discount to NAV.

Keystone Positive Change considers merger with open-ended equivalent; Gulf Investment Fund proposes a wind up; and PRS Reit makes up with its shareholders.

Frank Buhagiar

Keystone Positive Change Looking to Scale up

Keystone Positive Change (KPC) announced it’s considering implementing a transaction in the near term to address the size of the Company, the low liquidity in the Company’s shares and the discount at which they have been trading, while enabling Shareholders to retain exposure to a global impact strategy. Might sound like that’s a lot to achieve in one transaction, but among the options being considered by the Board is rolling the fund’s assets into the £1.8 billion Baillie Gifford Positive Change Fund, an FCA authorised open-ended investment company. One advantage here is that the two Baillie Gifford funds are “substantially” invested in the same portfolio of listed equities.

The Board is seeking shareholder feedback on the potential rollover. Activist investor and 17% shareholder Saba Capital presumably will be among those providing feedback, that is if they haven’t already.

JPMorgan: “a rollover into the open-ended version of the strategy makes sense in that it would eliminate the discount, and enable those who believe in the strategy to remain invested. But we would expect a 100% cash exit to be offered alongside a rollover option.”

Gulf Investment Fund Wind up on the Cards

Gulf Investment Fund’s (GIF) Board intends to put forward proposals to shareholders to wind up the company. As per the fund’s press release, this follows the launch of a tender offer for up to 100% of each shareholder’s holding in the company. Problem is, the tender appears to have been so popular that the fund received irrevocable commitments covering so many shares that if accepted would have resulted in “the minimum size condition in respect of the Tender Offer (being a post Tender Offer share capital of not less than 38,000,000 Shares) not being met.” Because of this, the tender will no longer proceed. Hence the wind-up proposal.

PRS Reit Makes up with Shareholders

PRS Reit (PRSR) has settled its differences with the shareholders who recently called for a general meeting to be held. The requisitioners wanted shareholders to be given the opportunity to vote on resolutions calling for two directors, including the current chairman, to be replaced with Robert Naylor and Christopher Mills, both of Hipgnosis Songs sale fame. A week, clearly a long time in the investment trust world for the build-to-rent REIT announced an agreement has since been reached that will see the requisitioners withdraw their Requisition Notice.

In return, Robert Naylor and Christopher Mills will be appointed to the Board as non-executive directors while current Chairman, Steve Smith, who was nearing the end of his term anyway, will step down and be replaced, on an interim basis, by Senior Independent Director, Geeta Nanda.

Winterflood: “This appears to be a positive outcome for PRSR shareholders, with most of the changes proposed by the requisitioning shareholders, which clearly had the support of a significant number of institutional investors, being implemented by the Board without the need for convening a GM, thereby saving some costs. Robert Naylor and Christopher Mills have notable experience in extracting shareholder value after being appointed to investment trust Boards, for example conducting the sale of Hipgnosis Songs Fund (SONG) to Blackstone earlier this year. We therefore expect them to have a significant impact on the upcoming strategy review.” Just goes to show, it’s good to talk.

The Results Round-Up – The Week’s Investment Trust Results

No shortage of results this week. Among those reporting, a private equity fund that would have made investors £2.2m had all ISA allowances and dividends been invested in the trust between 1999-2023; and another with a portfolio that reminds its own investment managers of Hans Christian Andersen’s Ugly Duckling story.

ORIT has had a busy half-year. The company acquired a large solar complex in Ireland, secured a PPA (power purchase agreement) for its Crossdykes onshore wind farm, and made a follow-on £5.9 million investment to develop its pipeline of offshore wind and sustainable fuels projects. As for the financials, NAV total return came in at +2% while the dividend target for the year was raised by 4% to 6.02p.

Liberum: “We maintain our BUY rating with a 115p TP and continue to be encouraged by the high level of earnings visibility, strong dividend cover, three-year track record of a CPI-linked uplift to the dividend, diversified portfolio, execution of the capital recycling programme and attractive discount to NAV.”

HydrogenOne Capital Growth (HGEN) on the Rise

HGEN’s share price stole the show over the half-year period, up +7.8% compared to NAV per share’s +0.6%. Progress was made at the portfolio company level too with an aggregate £76 million in revenues generated, that’s +44% year-on-year growth. What’s more, so far this year, investors have backed HGEN’s portfolio companies to the tune of €670m.

Winterflood: “NAV per share +0.6% to 103.6p (pre-announced), driven by valuation uplifts at multiple private investments and lower discount rates, with offsets from fees and FX.”

Greencoat Renewables’ (GRP) Proactive Management

GRP’s NAV per share for the half year came in at 112.1 cents, a little off H1 2023’s 113.2c. Despite this, operating cashflows funded €33 million in debt repayments as well as a €25 million share buyback. Meanwhile “proactive revenue management” has increased contracted revenues to 77% of the total for the 2024 – 2028 period, providing a high level of visibility.

Jefferies: “The results once again highlight GRP’s conservative valuation assumptions, coupled with significant capital allocation flexibility driven by the portfolio’s high level of contracted cash flow generation.”

HgCapital Trust (HGT) Tops the Charts

HGT’s +6.4% NAV total return for the half year was trumped by the +12.7% share price return. Over 10 years, share price total return now stands at +20.0% p.a. and for the third year in a row, the private equity fund tops the Association of Investment Companies’ (AIC) list of funds that would have made investors more than £1m had the full annual ISA allowance been invested in the same trust each year between 1999 and 2023. Together with reinvesting dividends into HGT shares, this would have generated a tax-free amount of over £2.2m as at 31 January 2024!

JPMorgan: “We see no reason to change our Overweight recommendation, with HGT the only pure play listed way to invest in leading private European profitable software and services companies”.

Pacific Horizon (PHI) Focused on the Horizon

PHI’s +4.8% NAV per share total return for the full year was a little behind the MSCI All Country Asia ex-Japan Index’s +6.8%. Tables turned over five years: NAV total return stands at +96.1% compared to the index’s +17.0%. Chairman Roger Yate’s thinks there’s more to come: “There remains a wealth of opportunities for the patient investor. Based on the encouraging macroeconomic trends and stock-specific opportunities, there is every reason to be optimistic about the long‑term prospects for the portfolio.”

JPMorgan: “Shareholders have suffered from a de-rating of the shares that had been trading on a premium between mid-2020 and early 2022 reflecting its strongest period of performance. The current 10.7% discount feels fairer, and is broadly in line with most peers.”

Nippon Active Value Fund’s (NAVF) Beats the Non-Benchmark

NAVF posted a +6.9% NAV increase for the half year. The MSCI Japan Small Cap Index (sterling terms) was largely flat, which means since the fund’s 2020 launch, NAV is up +89.2% compared to the index’s +16.7% return (sterling terms with dividends reinvested). Not that NAVF has a benchmark. As Chair Rosemary Morgan explains “Our strategy does not target any index. Our focus remains on medium and small capitalised companies, where we can build up significant stakes to enable productive engagement with their management.” So, “Even if investors’ focus shifts to opportunities away from Japan, we are confident that our activist approach will continue to perform well.”

Winterflood: “Managers believe that due to the majority of the portfolio being ‘domestic-facing, with little exposure to export or currency-led industries’, they are less impacted by a stronger Yen than portfolios composed of large international businesses.”

AVI Japan Opportunity’s (AJOT) Hidden Gems

AJOT’s “unique brand of constructive engagement and high-quality research” delivered a +7.7% NAV per share total return (sterling terms) for the half year, easily trumping the MSCI Japan Small Cap Index’s -0.2% sterling return. According to Chairman Norman Crighton, there should be more to come “The lack of research coverage of small-cap companies relative to large-caps continues to present us with abundant opportunities. Foreign investors have predominantly allocated their capital into larger companies with greater liquidity rather than taking time to uncover small-cap opportunities.”

Numis: “AJOT is our preferred pick and features on our recommended list”.

Petershill Partners’ (PHIL) Clean Sweep

PHIL reported a clean sweep of growth for the half year: $146m total income (H1 2023 $138m); $128m Adjusted EBIT (H1 2023 $120m); and $94m Adjusted Profit After Tax (H1 2023 $68m). PHIL’s Ali Raissi-Dehkordy and Robert Hamilton Kelly put the strong showing down to the alternative asset management firms in which the fund invests raising $14 billion of fee-eligible assets between them. Along with the growth in fee-paying AuM (assets under management), this has translated into higher gross management fees. Rounding off the solid numbers, the fund announced a special dividend.

JPMorgan: “We think the solid H1 print is reassuring, and the special dividend will be taken positively by investors today. We are Overweight.”

Foresight Solar Fund (FSFL) on Track to Hit Dividend Target

FSFL reported a 114.9p NAV per Ordinary Share at the half-year stage, a little down on the 118.4p reported six months earlier. The difference is largely down to lower-than-budgeted generation due to poor weather and a fall in power price forecasts. Despite this, the fund remains on course to hit its 8p per share dividend target for 2024 and 1.4x dividend cover.

Investec: “The shares currently offer a dividend yield of 8.5% and we estimate a prospective steady state return of c.10%. We maintain our Buy recommendation.”

Murray Income’s (MUT) Patience Delivers

MUT’s full-year NAV per share total return came in at +9.9%, a tad behind the FTSE All Share’s +13.0%. But, as the investment managers point out, “Our investment process encompasses a patient buy and hold approach” and it’s a process that has delivered over longer timeframes – over five years, annualised NAV per share has beaten the FTSE All-Share Index by +0.2%. As for what type of companies the fund buys and holds, these are “high-quality companies with robust competitive positions and strong balance sheets, which are led by experienced management teams capable of delivering premium earnings and dividend growth.”

Winterflood: “Performance benefited from stock selection in Consumer Discretionary and Telecommunications sectors and overweight exposure to Industrials and Technology sectors. This was offset by negative stock selection in Industrials, Financials, and Consumer Staples sectors.”

Ruffer’s (RICA) Ugly Duckling

RICA posted a +1% NAV total return for the full year in line with the aim to deliver positive NAV total returns. No one-off either. 2024 sees RICA chalk up 20 years, during which the wealth preserver has generated an annualised total NAV return of +6.9%. That’s a little behind the FTSE All-Share’s +7.4%. However, as Chairman Christopher Russell points out, RICA has achieved this “equity-like return with bond-like volatility and a positive return when equity markets have suffered a significant down-draft.”

Speaking of down-drafts, the investment managers “believe investors are complacent and we have arguably never seen an equity market as crowded, narrow, and myopic as the one we see today.” No surprise then that the portfolio has been positioned defensively. So much so, it brings to mind “Hans Christian Andersen’s Ugly Duckling story. It is a portfolio filled with unloved assets – shunned, even derided by other investors. But assets whose worth will become starkly apparent in time – as they turn to swans.”

Winterflood: “Equity upside drove returns (+3.0%), supported by gold and precious metals exposure (+2.0%), commodities (+1.8%) and cash and short-dated bonds (+1.6%), while protection strategies (-3.2%), Yen exposure (-2.2%) and long-dated inflation-linked bonds (-0.8%) detracted.”

City of London (CTY) Delivers Across the Board

CTY’s latest year was neatly summed up by the opening paragraph of Chairman Sir Laurie Magnus’ full-year statement “City of London produced a net asset value (NAV) total return of 15.6% outperforming the FTSE All-Share Index total return of 13.0%. The City of London’s NAV total return has exceeded the FTSE All-Share Index over 1, 3, 5, and 10 years. The dividend was increased for the 58th consecutive year and fully covered by earnings per share.” Not much more to say.

Numis: “We continue to view City of London IT as a solid option for investors seeking income from UK equities