4th Interim dividend for the year ending 31 August 2024

The directors have declared the fourth interim dividend of 6.20p per ordinary share in respect of the year ending 31 August 2024. The dividend will be paid on 29 November 2024 to shareholders on the register at 25 October 2024 (the record date). The shares will be quoted ex-dividend on 24 October 2024.

BBGI Global Infrastructure SA dividend payment date Custodian Property Income REIT PLC ex-dividend date Invesco Bond Income Plus Ltd ex-dividend date JPMorgan China Growth & Income PLC ex-dividend date Livermore Investments Group Ltd ex-dividend date TwentyFour Income Fund Ltd ex-dividend date

win88 Hey there this is somewhat of off topic but I was wondering if blogs use WYSIWYG editors or if you have to manually code with HTML. I’m starting a blog soon but have no coding knowledge so I wanted to get guidance from someone with experience. Any help would be enormously appreciated !

Trading update for the first half ended 30 September 2024

Assura plc (“Assura”), the diversified healthcare REIT, today announces its Trading Update for the six months to 30 September 2024.

Jonathan Murphy, CEO, said:

“We have made strong strategic progress in the first half of the year. The £500 million acquisition in August of a private hospital portfolio accelerates the delivery of our broader healthcare strategy while our £250 million joint venture with USS diversifies our funding. We are also very pleased to have been certified as the first FTSE 250 B Corp recognising our high standards of social and environmental performance.

“The purchase of 14 UK private hospitals materially increases our exposure to the structurally supported private healthcare market as we continue to diversify our offering to meet changing UK healthcare demands. The joint venture with USS, the UK’s leading private pension scheme, provides a new source of funding and opportunities to recycle capital into our growth pipeline.

“The need for investment in healthcare infrastructure was starkly outlined by the recent Lord Darzi report – which found the primary care estate to be plainly not fit for purpose and more than 1 million people to be waiting for community services. We are at an inflexion point in the UK, with structural changes to the delivery of healthcare services, the Government targeting preventative services in a community setting, and rising demand for private providers. Assura has firmly positioned itself to facilitate this change, being well-placed to work with all healthcare providers to deliver high-quality, sustainable facilities for the long-term..”

Delivery against our strategic objectives

• Portfolio of 14 private hospitals acquired for £500 million: day 1 rental income of £29.4 million, WAULT of 26 years, 100% subject to annual index-linked rent reviews, let to tier 1 private healthcare providers with strong rent cover of 2.3 times

• Portfolio now stands at 625 properties with an annualised rent roll of £179.1 million (March 2024: £150.6 million)

• Three developments completed with a total combined spend of £46 million; GP surgery in Shirley, ambulance hub at Bury St Edmunds and our largest in-house development project to date of the Northumbria Health & Care Academy at Cramlington

• Positive progress on rent reviews, 129 settled in the first half, covering £20.4 million of existing rent and generating an uplift of £1.7 million (8.2% uplift on previous passing rent, 3.0% on an annualised basis)

• Initial tranche of seven assets agreed for transfer to joint venture with USS

• Completed seven asset enhancement capital projects (total spend £3.0 million) and seven lease regears (existing rent £0.6 million); on site with a further four capital projects (total spend £5.6 million)

• Quarterly dividend increased by 2.4% to 0.84 pence per share, as announced at the full year results, with effect from the July 2024 payment

Pipeline of opportunities for strategic expansion and further growth

• Advanced discussions taking place for the disposal of 12 assets

• Currently on site with five developments; total cost of £44 million with £27 million remaining to be spent. On site schemes include two net zero carbon buildings in the UK (one GP medical centre, one NHS children’s therapy centre) and three developments for the HSE in Ireland.

• Pipeline of 14 capital asset enhancement projects (projected spend £8.8 million) over the next two years

• 32 lease re-gears covering £3.9 million of existing rent roll in the current pipeline

Strong and sustainable financial position

• Weighted average interest rate 3.0% (March 2024: 2.3%); all drawn debt on fixed rate basis

• Weighted average debt maturity of 5.1 years, limited refinancing on drawn debt over the next 3 years. Over 40% of drawn debt matures beyond 2030, with our longest maturity debt at our lowest rates

• A- rating reaffirmed by Fitch in August following private hospital portfolio acquisition

• Net debt of £1,575 million (March 2024: £1,217 million) on a fully unsecured basis with cash and undrawn facilities of £143 million

Full results for the six months ended 30 September 2024 will be announced on 14 November 2024.

3 super-safe dividend shares I’d buy to target a £1,380 passive income!

By Royston Wild

Provided by The Motley Fool

Dividends from UK shares are never, ever guaranteed. As we saw during the Covid-19 crisis, even the most generous and financially secure company can postpone, suspend, or axe shareholder payouts when catastrophes happen.

But as investors, we can take steps to minimise the chances of dividend disappointment. Choosing defensive companies that enjoy stable earnings (like utilities, healthcare providers, and food manufacturers) is one tactic.

So is selecting companies with strong balance sheets, market-leading positions, and diversified revenue streams. This can protect earnings when economic conditions suddenly worsen.

It’s also important to spread one’s capital across a variety of different shares. Such diversification reduces the impact of company and industry-specific factors on investors’ returns.

Three top stocks

With all this in mind, here are three super-safe dividend shares on my watchlist today.

As I say, dividends are never a sure thing, and broker projections can sometimes fall short. But if current forecast are correct, a £20,000 investment spread equally across these dividend shares would provide a passive income of £1,380 this year alone.

A top REIT

Source: TradingView

Out of this bunch, let’s take a deep dive into Assura first. As the chart above shows, this FTSE 250 company has a long history of dividend growth even during times of crisis.

City analysts expect this proud record to continue, too, even as the threat from high interest rates remains.

Retirees: Unlock the Secrets to Earning Passive Income and Secure Your Golden Years

As a result, the firm’s dividend yields lift to 8.5% for next year, and to 8.6% the year after.

Elevated interest rates depress net asset values (NAVs) for property stocks and can significantly raise their borrowing costs. But the defensive nature of Assura’s operations — it owns and lets out primary healthcare properties, like doctor surgeries — allows it to pay a large and growing dividend each year.

The real estate investment trust (REIT) is expanding rapidly, to help it grow earnings beyond the medium term. But sector rules mean that this expensive programme doesn’t have catastrophic implications for dividends.

Under REIT regulations, Assura must pay a minimum 90% of annual rental profits out in the form of dividends. Combined, these factors make the business a rock-solid income pick in my book.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

FTSE 100 dividend stars

Source: TradingView

Combined with Legal & General and Diageo in a portfolio, I think I could enjoy a truly spectacular dividend for years to come. As you can see, these two stocks also have long histories of sustained payout growth.

But the FTSE 100 firm’s balance sheet has still allowed it to regularly grow dividends over the past decade. And with a Solvency II capital ratio of 223%, it remains cash rich today.

Diageo, meanwhile, is another reliable dividend stock thanks to its strong position in the largely resilient alcoholic drinks market. While it faces extreme competitive pressures, fashionable labels like Guinness and Captain Morgan help to lessen this threat.

I also like the Footsie firm’s wide diversification across different geographies and drinks segments. This provides earnings (and thus dividends) with added stability.

The post 3 super-safe dividend shares I’d buy to target a £1,380 passive income, appeared first on The Motley Fool UK.

£££££££££££

The Snowball only invests in Investment Trusts as most Trusts have reserves they can use to continue to pay their dividends, as during the Covid crisis.

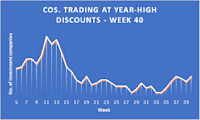

The number of investment companies trading at 52-week high discounts has risen to 12 but which region contributed the most names week ended Friday 4 October.

By Frank Buhagiar

We estimate there to be 12 investment companies that saw their share prices trade at 52-week high discounts over the course of the week ended Friday 04 October 2024 – three more than the previous week’s nine.

Last week, it was Japan-focused funds that contributed the most names to our list of year-high discounters. One week on, not a Japan-focused trust in sight. Instead, three funds that invest in the Asia Pacific Region – Fidelity Asian Values (FAS), JPMorgan Asia Growth & Income (JAGI) and Schroder Oriental Income (SOI). Four if you include JPMorgan Emerging Markets (JMG) – as at 31 July 2024, the fund had near enough three-quarters invested in Asia.

No results out from any of the four, but a look at the share price graphs for each trust shows that they all set new year-high discounts in the first few days of the week – hence their appearance on this week’s list. By Friday 4 October, however, all four shares had staged a recovery. Something of a mystery then. But could it be down to Chinese markets being closed for Golden Week? Fair to say, prior to the holiday, Chinese markets had been on a tear in response to a series of measures announced by the authorities to support the economy – China’s CSI 300 blue-chip index rallied more than 25% over the nine days running up to the holiday week.

With China being closed for the week, other markets such as India became the main performance drivers. Shame then that India didn’t have a good week – the BSE Sensex Index was off 5%. Elsewhere, Singapore’s STI index was basically flat (+0.44%) while South Korea’s KOSPI was down 4% or so. Without China to turbocharge performance, no surprise then that all four funds succumbed to a little profit-taking early on in the week. After all, the shares of the four were up strongly the week before – JAGI, the stand out with a +7.5% gain week ended 27 September.

But what about the recovery they all enjoyed towards the end of the week? Well, this could be down to investors positioning themselves for the big China reopening in anticipation of Chinese markets picking up where they left off. Question is, will they?

Four funds from the renewable energy infrastructure space reporting on the same day may have just been a coincidence, but it does provide an excuse to check-in on the sector.

By Frank Buhagiar

7:00 am Monday 30 September 2024, four funds from London’s renewable energy infrastructure sector publish results/updates. Coincidence or did a memo do the rounds ? Regardless, with the four funds heralding from three different sub sectors, the flurry of announcements provides an opportunity for a quick health check for London’s renewables space. After a challenging year that saw interest rates stay higher for longer, revenues come under pressure and share prices trade at record-high discounts, any positives to take away?

The four funds: Bluefield Solar Income Fund (BSIF) and US Solar Fund (USF) from renewable energy infrastructure; Gresham House Energy Storage Fund (GRID) from battery storage; and SDCL Energy Efficiency Income (SEIT) from energy efficiency.

BSIF on the Back Foot

As broker Numis points out, BSIF was on the back foot from the off. “Following a record year for earnings in 2023, it was always going to be tough to beat.” As per the Annual Report: Net Asset Value (NAV) came in at £781.6m (2023: £854.2m), reflecting reduced long-term power price and inflation forecasts; underlying earnings (pre-amortisation of debt) stood at £94.6m (2023: £108.4m); while total return was down at -0.83% (2023: 5.45%). Operating performance was also lower year-on-year as generation fell 3%. Two reasons cited: outages and the weather – irradiation levels were around 4.3% below expectations.

Positives include underlying earnings (post debt) of 10.57p more than enough to cover the 8.8p annual dividend. Also, a large portion of group revenues have a high degree of visibility: power purchase agreements and subsidies cover 80%+ of 2025’s revenues and 63% for the next two years. There was a small increase in the dividend target to 8.9p from 8.8p too.

And post-period end, Mauxhall Farm (44.4MW) and Yelvertoft (48.4MW) were energised, bringing total operational capacity up to 883MW; while the sale of a 50% stake in a 112.2MW portfolio of UK solar assets to strategic partner GLIL Infrastructure was completed. Further disposals are being considered with the proceeds earmarked to reduce debt and fund the development of the 1.5GW pipeline. Despite the tough environment, BSIF still getting things done.

Numis: “Looking forward, we believe BSIF remains well-placed to deliver attractive returns from its asset base, which includes a significant pipeline and a long-term strategic funding partner.”

Jefferies: “On the distribution side, underlying dividend cover and dividend growth are disappointing due to multiple factors, but with upside in cover expected when looking forward.”

JPMorgan: “BSIF benefits from having what look, in the context of current forward market prices, attractive prices on its fixed PPAs over the next couple of years. This will help it in terms of dividend cover and earnings although new fixes will likely be agreed at incrementally lower levels reflecting the prevailing forward market as the old fixes roll off. We are Neutral.”

USF Looking to Maxmise Shareholder Value

USF, like BSIF, reported a reduction in NAV to US$230.4m (31 December 2023: US$258.2m) for the half year, although this was largely due to the return of US$18.6 million plus costs to shareholders via a tender offer. NAV per share was 4% lower at US$0.75 (31 December 2023: US$0.78 per share). A combination of a 40 basis point increase in the risk-free rate used for valuing the US portfolio, US$6.8 million dividends and changes to both operating and macroeconomic assumptions all to blame here.

The Q2 dividend of 0.56c is in line with the albeit reduced annual target of $0.0225 per share, which is expected to be fully covered by cash generated from operations. As with BSIF, total generation of 365GWh was 6.8% below budget due to outages and below forecast solar irradiance during Q1 2024, particularly at USF’s largest asset, the 128MW Milford site – not just the UK in need of more sunshine.

It’s no secret that USF is holding out for an exit opportunity. As Chair, Gill Nott, explains “Our focus remains on taking steps to ensure the Company’s portfolio is robust, optimised and capable of being presented to the market for a future liquidity event in order to maximise shareholder value.” Perhaps because of this (and/or the fund’s small size) not much in the way of broker commentary following the results.

GRID Looking Forward to Renewed Growth

As previously reported, GRID saw NAV fall over the half year. NAV per share came in at 109.16p, 19.91p below the 31 December 2023 figure. 19.47p of the fall was down to updated third-party revenue forecasts following the introduction of a more conservative provider.

Progress was made operationally. Capacity was up 34% year-over-year to 790MW, although portfolio revenues fell 12.8% year-over-year to £17.9m (HY 2023: £20.5m) which, in turn, drove a 23.9% decline in EBITDA to £10.4m (HY 2023: £13.8m). This was down to “especially difficult market conditions in Q1 2024” that led to the dividend being suspended. Action has been taken to remove at least some of the volatility from revenues after “a landmark tolling arrangement” was signed with Octopus Energy. GRID expects to receive annualised contracted revenues of c.£43m from the tolling arrangement which will see Octopus contract 568MW for two years from H2 2024 onwards.

Encouragingly, since period-end, average net revenues for July and August came in at the highest levels of the year so far and c.25% higher than those seen in H1 2024. Furthermore, with the current construction programme expected to conclude in H2, the operational portfolio is set to breach the 1GW barrier.

Fund manager, Ben Guest, notes “The tolling agreement and conclusion of the construction programme have stabilised the business and provided the visibility required for the Board and Manager, with our shareholders, to be able to look forward to renewed growth. It is good to be looking forward to new growth in 2025 and beyond with a large portfolio and a more stable earnings outlook, as our starting point.” Sense of “the worst is behind us” there.

Numis: “The tolling arrangement will provide a degree of revenue stability and management reaffirms its previous comments that if merchant revenues stay at recent August levels (c.£45,000/ MW/yr) this would result in annualised EBITDA of c.£45.7m.”

JPMorgan: “deeper renewable penetration and higher consumer winter demand may improve trading revenues over the next six months.”

SEIT Well Positioned for Growth

SEIT’s interim update for the six months to 30 September, a little light on numbers but did flag operational cash flows are in line with expectations. The 6.32p 2025 dividend target was also reaffirmed and is covered by net operational cash flows. The announcement did highlight that portfolio companies Onyx and EVN are growing fast and ahead of budget and so require further capital. (Onyx, a provider of distributed clean energy solutions to commercial and industrial customers in the US; EVN, an electric vehicle charging platform in the UK). Financing, co-investment and disposal opportunities are therefore being explored to support their future growth as well as reduce the debt facility.

Investment manager, Jonathan Maxwell, thinks “The portfolio is well positioned for growth” and that “Interest rate cuts in the US and UK are likely to have a positive impact on the value of SEEIT’s portfolio on a discounted cash flow basis. While this may in due course reduce SEEIT’s weighted average discount rate, we view it as prudent to materially absorb decreases in risk free rates through increases in risk premiums for the September 2024 valuation due to ongoing economic and geopolitical uncertainty.” Cautious optimism from the investment manager.

Numis: “It will be interesting to see what SEIT management can secure to enable it to fund the growth capital requirements of the business. The board and manager comment that it remains focussed on the discount to NAV, as well as keeping gearing within limits.”

Jefferies: “Looking beyond Onyx and EVN, the other portfolio companies are less capital hungry, so this disposal or co-investment activity should also increase the overall financial flexibility of the fund, with additional project-level debt clearly an option for the more cash generative investments.”

Storms Subsiding

The sector has faced a near-perfect storm of challenges: high-interest rates, falling power prices, unfavourable weather. Such has been the severity of the storm, drastic action has been taken: business models adapted, capital allocation policies adopted, strategic partners found, dividends suspended and, in the case of USF, sales sought. The sector is navigating the tough conditions. Not just a case of battening down the hatches. By securing a partner or selling assets, funds are being raised to reduce debt yes, but also to develop pipelines.

And arguably with interest rates coming down and power prices already lower, the worst of the storm could well have passed. Discounts are already narrowing, though more is required before equity markets reopen as a source of growth capital. In the meantime, based on the above updates at least, individual funds are getting their respective houses in order in anticipation of better times ahead.

The Results Round-Up – The Week’s Investment Trust Results

ICG Enterprise delivered +2.8% NAV growth for the latest half year, with share price total returns outperforming at +10.3%. Other trusts also had notable performances: FEML saw an 18.7% return, PAC achieved a +10.8% gain, and ESCT delivered a +19.5% share price return.

By Frank Buhagiar

ICG Enterprise’s (ICGT) Engine of Growth

ICGT posted a +2.8% NAV per share total return for the latest half year. Share price fared even better with a +10.3% total return. Chair, Jane Tufnell, says the “solid NAV per Share growth” during a period of “continued economic and political headwinds” is down to “robust underlying earnings growth (LTM EBITDA growth: 14%), an active capital allocation policy and prudent balance sheet management.” The long-term track record stacks up well too. Over the five years to 31 July 2024, the fund’s investment strategy has delivered annualised NAV per share and share price total returns of +12.5% and +11.7% respectively. The Chair believes there’s more to come. That’s because “the Board maintains its positive outlook that private equity remains a strong engine of growth to outperform public markets.” The market seemed to agree, marking the shares up 10p to 1194p on the day.

Jefferies: “ICGT’s NAV continues to make some modest headway despite challenging market conditions and a FX headwind.”

Numis: “It is positive to see exits at continued uplifts to carrying values, with an average uplift of 26% on full exits during the period. We believe that the 39% discount is too wide for a high-quality manager and that the opportunistic buyback programme, alongside regular buybacks, should help to narrow the discount over time.”

JPMorgan: “we remain Overweight on account of the favourable portfolio metrics (14% LTM EBITDA growth,14.9x valuation, 4.4x debt) and disciplined capital allocation, with the buybacks and dividends.”

Fidelity Emerging Markets (FEML) Firing on All Cylinders

FEML’s +18.7% full-year NAV return comfortably ahead of the MSCI Emerging Markets Total Return Index’s +13.2%. That’s some second-half turnaround – in the first half, FEML’s +3.2% total return fell short of the index’s +4.4%. Chair, Heather Manners, believes this shows “the investment process is now firing again on all cylinders and driving strong NAV performance.” Stock selection, the main driver of outperformance during the year. But the Portfolio Managers also point out that “The Company’s extensive ‘toolkit’ added significant value over the year.” For toolkit, read gearing, mid-cap exposure, financial derivatives. The Managers believe this toolkit and the flexibility it delivers will prove its worth in today’s uncertain environment, “we will continue to use this flexibility to closely manage risk, all the while exploiting the most exciting opportunities throughout the emerging market universe.” Not much excitement around the share price which closed largely flat.

Numis: “FEML has a performance triggered tender offer, for 25% of share capital at a 2% discount to NAV, should the NAV underperform the MSCI EM in the five years to 30 September 2026. Performance has been disappointing within this period to date, with FEML producing NAV total returns of -13.4%, lagging the +3.9% from the MSCI EM index despite recent improved performance. Underperformance has predominantly been driven by overweight exposure to Russia prior to the invasion of Ukraine”.

JPMorgan: “the past financial year has seen an improvement in relative performance and shows some of the benefits of the strategy the managers follow. The use of short positions and what the managers describe as a toolkit, meaning use of financial derivatives, has added significant value despite the risk limits imposed. This is a differentiating feature of FEML vs its AIC Global EM peers. We are Neutral.”

Pacific Assets’ (PAC) Step-Up

PAC’s+10.8% NAV total return for the half year, a major step-up from last year’s +0.3%, although not quite enough to match the peer group average of +12.9% and the MSCI All Country Asia Pacific ex Japan Index’s (sterling) +14.9%. The main culprits behind the shortfall, Chinese and Hong Kong exposure.

Over longer timeframes, performance is assessed against UK CPI plus 6%. As Chairman Andrew Impey explains, that’s because “we believe that our largely UK-based investors are seeking to protect and grow their capital in real terms by extracting a premium over their home markets from the faster growing Asian economies.” Over the last five years, the trust has generated a +7.7% annualised return, a little behind the annualised CPI plus 6% figure of 10.8%. Impey puts this down to “unusually high inflation experienced in the UK and globally in recent years.” That means with inflation back around the 2% target level “the challenge presented by our performance objective of exceeding UK CPI plus 6% will become more achievable.” Market adopted a wait-and-see approach, shares ended the day unchanged.

Winterflood: “High exposure to India helped performance, with 5 of top 10 stock contributors being Indian companies. Top detractors were mainly Chinese/Hong Kong stocks.”

European Smaller Companies’ (ESCT) Picks and Shovels

ESCT outperformed the benchmark by +1.9% over the full year thanks to a +12% NAV total return. The share price topped the lot with a +19.5% total return. The latest numbers add to ESCT’s longer-term track record of outperformance: over five years, NAV total return stands at +73.3% almost double the benchmark’s +37.2%.

Chairman, Christopher Casey, gives three reasons why he thinks the outlook for European small-caps is positive: “very low valuations”, the falling cost of capital and “improving economic optimism”. But what seems to excite the Chairman most is that “Europe is fortunate to be the provider of the ‘picks and shovels’ of the big structural growth trends such as Artificial Intelligence, the ‘Green Transition’ and industrial automation. It is an exciting time for the European smaller company space.” Based on the muted share price reaction, seems investors are keeping a lid on their excitement for now.

Numis: “We regard ESCT as an attractive vehicle for investors looking for exposure to small/mid cap growth companies in Europe. It is currently trading at a 10.7% discount to NAV, and we note that Saba has been increasing its position, currently 13% as at 8 October, which may be a catalyst for corporate action.”

Winterflood: “the current valuation does not offer extraordinary value, although we would highlight that the Board has notably increased the level of buybacks this year, which should limit downside discount risk to an extent. In addition, we think there is scope for a re-rating should the fund’s strong absolute and relative performance record be sustained, potentially supported by economic improvement in Europe benefitting small caps.”

Fidelity Asian Values (FAS), the Contrarian

FAS’ +3.2% NAV total return for the year couldn’t match the MSCI All Countries Asia ex Japan Small Cap Index’s +13.7% in sterling terms. Chair, Clare Brady, puts the underperformance down to the portfolio managers’ investment style which is “bottom-up, contrarian and value-focused. While this style has historically delivered differentiated investment returns, it can also lead to periods of underperformance when extreme momentum is driven by investors focusing on a narrow range of areas, as has been the case recently in countries, sectors and themes such as India, technology and artificial intelligence (AI).”

One positive “With much of the investing world continuing to be in thrall to all things AI, your Portfolio Managers’ positioning in unloved and overlooked areas arguably carries limited downside potential, compared to other areas of the market, with the possibility of significant upside.” Nothing in the results to stop the shares’ recent strong run in its tracks. That’s likely down to the fund’s significant overweighting to China which has benefited from the series of measures unleashed by the authorities to stimulate the economy and market – shares are up almost 10% over the past month alone.

Winterflood: “Underperformance attributed to country allocation, especially notable overweight to China/Hong Kong (portfolio average weighting of 41% vs index 13%). Allocation to China/Hong Kong close to historical high due to process of taking contrarian positions in undervalued businesses. Underweight to India (19% vs 31%) also detracted.

Ian Cowie: UK trusts aren’t cheap, so here’s what I’m backing

Our columnist explains why he’s focusing on the hot topic of renewable energy rather than eyeing potential discount opportunities among UK equity investment trusts.

by Ian Cowie from interactive investor

Next Monday’s UK International Investment Summit will see Prime Minister Keir Starmer pitch for more foreign funds to back British businesses. Fortunately, many London-listed investment trusts already make it cheap and convenient to obtain exposure – but one of the most interesting does not contain the words “British” or “UK” in its title.

For example, consider the hot topic of renewable energy. Not many people now remember Boris Johnson’s brief enthusiasm for turning Britain into “the Saudi Arabia of wind”.

Back then – and now – the problem with renewable power is how to keep a modern economy warm and in work when the wind won’t blow and the sun don’t shine. Industrial-scale batteries, such as those operated by specialist investment trusts including Gore Street Energy Storage Fund Ord

GSF

1.08%

and Gresham House Energy Storage Ord

GRID

0.00%, provide short-term solutions but in my view not long-term answers to the difficulty of balancing energy demand and supply.

Pumped storage hydropower (PSH) can utilise gravity in hilly or mountainous regions with plenty of water – such as Scotland or Wales – to store energy over any length of time. When renewable electricity from wind or solar sources is plentiful, it is used to pump water from a low-level loch or lake to a higher-level reservoir. Then, when renewable power is scarce, gravity is allowed to draw the water down through dynamos to generate sufficient electricity to supply demand.

The technology has been in use for decades, with Britain’s four PSH facilities in Scotland and Wales delivering up to 2.8 gigawatts (GW) of electricity whenever needed. But capital costs are high – digging tunnels inside mountains don’t come cheap – and there are environmental concerns about disrupting or even destroying wildlife, such as salmon.

Even so, ways can be found for PSH to deliver cleaner, greener power than alternative sources such as coal, liquefied natural gas (LNG) or oil. Jean-Hugues de Lamaze, fund manager of the self-descriptive investment trust Ecofin Global Utilities & Infra Ord

EGL

1.30%

“As the world is turning to renewables to decarbonise, storage is becoming critical – and therefore increasingly valuable – to bridge intermittency and seasonality.

“Pumped hydro is currently the main storage source with about 90% of global capacity, according to the International Hydropower Association. There aren’t any concentrated large, stock market-listed pumped hydro companies in Europe, but several energy utilities own PSH assets.”

De Lamaze added: “Iberdrola is a leader in pumped storage with 4.5GW of installed capacity in Spain and Portugal and the ambition to invest another €1.5 billion in storage over the next two years.

“SSE is developing the fully consented Coire Glas project in the Scottish Highlands – Britain’s biggest pumped hydro scheme in 40 years – which would more than double Britain’s current storage capacity.”

That extra PSH could go a long way to avoid excess electricity being earthed – or, essentially, thrown away – when there is too much wind and demand falls far short of supply.

Not that such problems have prevented Greencoat UK Wind

UKW

0.29%

from topping the Association of Investment Companies (AIC) “Renewable Energy Infrastructure” sector over the past decade and five-year periods with total returns of 128% and 30% respectively, followed by 15% over the past year. UKW generates 7.1% dividend income, which has risen by an annual average of 8.1% over the past five years but remains priced -12.3% below the net asset value (NAV) of its £4.7 billion assets.

Meanwhile, EGL has generated total returns of 35% over the past year and 48% over five years but lacks a 10-year record, as it was launched in September 2016. Income-seekers may also note its 4.2% dividend yield, which independent statisticians Morningstar calculate has increased by an annual average slightly above 4% over the past five years. Even so, shares in this fund with total assets of £276 million continue to be priced nearly -13% below their net asset value (NAV).

To put those numbers in perspective, it is notable that the AIC’s “UK Equity Income” sector currently offers similar average income – 4.1% – albeit rising more slowly by 3% per annum – and with a much smaller average discount of -5.4%. Nor do the AIC’s ‘UK All Companies’ or “UK Smaller Companies” sectors look terribly cheap on average discounts both currently around -11%; yielding 3% and 2.9% dividend income respectively.

No doubt Starmer will put a more positive spin on British bargains at next week’s UK International Investment Summit. Let’s hope this prime minister’s enthusiasm for renewable energy in general – and PSH in particular – proves longer lasting than that of his predecessor, Boris Johnson.

Ian Cowie is a freelance contributor and not a direct employee of interactive investor.

Ian Cowie is a shareholder in Ecofin Global Utilities and Infrastructure (EGL) and Greencoat UK Wind (UKW) as part of a globally diversified portfolio of investment trusts and other shares.