Strong stock selection and a pickup in M&A activity has driven AEI’s outperformance over 12 months…

Kepler

Overview

Thomas Moore, manager of abrdn Equity Income (AEI), employs an index-agnostic approach to investing in UK equities, aiming to deliver above-average and growing income to investors, alongside capital growth. His strategy centres on stock selection, targeting companies based on their individual merits and alignment with the trust’s objectives, rather than their weighting in an index. This flexible approach enables him to uncover value across the market, including opportunities in areas often overlooked by traditional equity income strategies.

Over the past year, Thomas has capitalised on market volatility by making a number of adjustments to the Portfolio on valuation grounds. This included investing in well-established, high-yielding large-cap names such as M&G and Imperial Brands, whilst also identifying compelling prospects in the small- and mid-cap space, adding Petershill and Galliford Try, which offer attractive yields and greater growth potential, to the portfolio.

Focussing on higher-yielding companies has allowed Thomas to maintain AEI’s competitive yield of 7.0%. This is a significant premium to the market and the second highest in the AIC UK equity income sector. In addition to yield, Thomas screens for companies with dividend growth potential, helping the trust maintain its consistent dividend growth record, despite difficult economic conditions, with 2024 marking the 24th consecutive year of dividend increases.

The market backdrop has not been supportive to the investment process – given the outperformance of larger-cap growth stocks – resulting in the trust underperforming its benchmark over a five-year period. However, the trust has seen a marked improvement in Performance over the past 12 months, delivering NAV total returns of 24.3%, outpacing the FTSE All-Share Index’s return of 17.6%. Outperformance stemmed from strong stock selection and heightened M&A activity. Defensive mega-cap names like Imperial Brands, which continues to thrive under new management, and financial holdings such as NatWest, Barclays, and HSBC, which benefitted from the ‘higher for longer’ interest rate environment, were key contributors to returns.

Analyst’s View

We think the UK market, despite recent challenges, presents an intriguing opportunity for investors, given the current divergence in equity valuations. The UK plays host to a range of well-established, operationally strong and attractively valued companies. The key is identifying undervalued opportunities with genuine upside potential.

Thomas brings years of UK market experience, with expertise in spotting valuation mispricings. His index-agnostic approach allows him to explore the entire market, beyond traditional equity income constraints, for attractively valued companies with latent recovery potential. AEI has faced headwinds over the past five years, as Thomas’s focus on smaller companies and more value-oriented stocks, which have been largely out of favour, led to underperformance versus the benchmark., AEI’s Performance has rebounded more recently, outperforming its benchmark as market conditions have turned more favourable for Thomas’s strategy. Easing UK-specific headwinds have triggered portfolio re-ratings, whilst historically low valuations for smaller companies – in cases due to prolonged economic pressures rather than weak fundamentals – have driven heightened M&A activity. Several smaller portfolio holdings have been sold at large premiums following private bids.

With a 7.0% yield, a premium to the market, and a 24-year track record of consistent dividend growth, we think AEI offers a compelling proposition for income-focussed investors seeking differentiated exposure to the UK. As interest rates fall and the appeal of high-yielding bonds and bank accounts diminishes, AEI could be a well-positioned destination for investors seeking higher-yielding opportunities with potential for capital growth.

Bull

Offers one of the highest yields in the sector, supported by strong reserves

Differentiated portfolio including a bias to UK small- and mid-caps

Trust has recently reduced its charges

Bear

Exposure to small and medium-sized companies may bring more sensitivity to the UK economy

Use of gearing could magnify the gains but also the losses

Value-tilted portfolio has seen the trust struggle when growth style outperforms

Bluefield Solar (LON: BSIF), the London listed UK income fund focused primarily on acquiring and managing solar energy assets, is pleased to announce the Company’s first interim dividend for the financial year ending 30 June 2025 (the ‘First Interim Dividend’).

The First Interim Dividend of 2.20 pence per Ordinary Share (January 2024: 2.20 pence per Ordinary Share) will be payable to Shareholders on the register as at 7 February 2025, with an associated ex-dividend date of 6 February 2025 and a payment date on or around 7 March 2025.

The Board is pleased to reaffirm its guidance of a full year dividend of not less than 8.90 pence per Ordinary Share for the financial year ending 30 June 2025 (2024: 8.80 pence). This is expected to be covered by earnings post debt amortisation.

CC Japan Income & Growth Trust PLC ex-dividend date CQS Natural Resources Growth & Income PLC ex-dividend date Edinburgh Investment Trust PLC ex-dividend date Henderson Far East Income Ltd ex-dividend date JPMorgan Claverhouse Investment Trust PLC ex-dividend date M&G Credit Income Investment Trust PLC ex-dividend date Residential Secure Income PLC ex-dividend date Schroder Oriental Income Fund Ltd ex-dividend date Schroder UK Mid Cap Fund PLC ex-dividend date Sequoia Economic Infrastructure Income Fund Ltd ex-dividend date Supermarket Income REIT PLC ex-dividend date

The companies known as the Magnificent Seven make up over 20% of the global stock market. And a lot of this is based on their perceived advantage when it comes to artificial intelligence (AI).

The big US tech firms hold all the aces when it comes to cash and computing power. But Deepseek – a Chinese AI lab – seems to be showing this isn’t the advantage investors once thought it was.

What is DeepSeek? DeepSeek doesn’t have access to the most advanced chips from Nvidia (NASDAQ:NVDA). Despite this, it has built a reasoning model that is outperforming its US counterparts – at a fraction of the cost.

Investors might be wondering about how seriously to take this. But Microsoft (NASDAQ:MSFT) CEO Satya Nadella is treating DeepSeek as the real deal at the World Economic Forum in Davos:

“It’s super impressive how effectively they’ve built a compute-efficient, open-source model. Developments like DeepSeek’s should be taken very seriously.”

Whatever happens with share prices, I think investors should take one thing away from the emergence of DeepSeek. When it comes to AI, competitive advantages just aren’t as robust as they might initially look.

US AI Microsoft is set to spend $80bn on AI in 2025. Very few other companies are able to do anything like this and that gives the company a huge advantage — at least, at first sight.

Investors should be careful though, in thinking about what that means. While it puts the firm in a strong position against its competitors, DeepSeek’s latest model indicates it’s not insurmountable.

Equally, Nvidia is the leader when it comes to AI chips. But while the threat from a rival catching up might be limited, the risk of demand falling as customers do more with its earlier products also needs considering.

The emergence of DeepSeek has highlighted both of these challenges. And for the biggest US tech stocks trading at high prices, I expect this to have a meaningful impact on share prices sooner or later.

Is this an opportunity? The biggest question for investors is whether a drop in share prices is a buying opportunity. From my own perspective, I think it’s reason to be careful, but I’m also wary about overreacting.

If there’s one thing I think investors should take from the emergence of DeepSeek, it’s that a competitive advantage in this area is harder to maintain than it might initially seem. And that cuts both ways.

The US hyperscalers might have just seen their lead cut — or even eliminated entirely — by DeepSeek. But I think counting them out when it’s just been shown how hard it is to stay ahead in this industry is very reckless.

I don’t expect them to stay behind for long, but the question is whether they can ever establish a long-term lead. Apparently, big advantages in cash and computing power don’t guarantee this.

Warren Buffett has been staying away from AI – and tech in general – following his misjudged investment in IBM. And I think a lot of investors would be wise to consider following his example.

It turns out, assessing who has a durable edge when it comes to AI is harder than it looks. So even if the Magnificent Seven pulls the stock market lower, investors should be careful.

The post Is DeepSeek about to cause a stock market crash ? appeared first on The Motley Fool UK.

£££££££££££££££

Whilst all days including weekends and holidays are good days to have a dividend re-investment plan, some days are better than others.

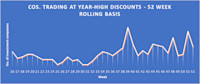

Discount Watch We estimate the number of funds trading at year-high discounts to net assets dropped by 12 to 16 last week. Alternatives still dominate with 12 names but among the four non-alternatives – wealth preserver Ruffer (RICA). Share price hit a year-high discount on Monday 13 January but after releasing an update a few days later the discount almost halved. Was it something the investment managers said ?

By Frank Buhagiar

We estimate there to be 16 investment companies which saw their share prices trade at 52-week high discounts to net assets over the course of the week ended Friday 17 January 2025 – 12 less than the previous week’s 28. Usual graph below but, as it’s still early days for 2025, the number of year-high discounters is shown on a rolling rather than year-to-date basis.

Big drop in the number of investment companies trading at 52-week high discounts to net assets maybe, but same old story of alternative funds dominating the list on concerns higher bond yields will lead to higher discount rates and lower asset valuations. Alternatives account for 12 of the 16 on the list, 10 of which are renewables while infrastructure and property both chip in with one fund each.

In the interests of writing about something different this week, mention in despatches goes to Ruffer (RICA). Not because the capital preservation trust traded at a year-high discount to net assets of -7.59% on Monday 13 January, but because the discount had practically halved to -4.5% just a few days later on 16 January 2024. That was the day RICA released its investment managers’ performance review.

Not that the numbers were spectacular: over the six-month period to end of December, NAV total return came in at -0.4%, share price total return +0.2%; while NAV total return for the 12 months to end of December 2024 was unchanged at 0.0% and share price total return down -0.7%. Something the investment managers said then ? Perhaps, the comment, “We currently see the elastic band which tethers prices and fundamentals as stretched taut, with the potential for an aggressive snap back” resonated with investors, especially as this could result in “a redemptive performance moment” for the fund. Or was it talk of the fund’s protective armoury ? “We do not attempt to time every market turn, but we do seek to ensure the portfolio’s protective armoury is in place when we sense moments of danger” ? Investors maybe sensing danger too.

Top five

Fund

Discount

Sector

Ceiba Investments CBA

-74.95%

Property

Ecofin US Renewables RNEW

-53.19%

Renewables

Gore Street Energy Storage GSF

-52.31%

Renewables

Aquila Energy Efficiency AEET

-46.99%

Renewables

US Solar Fund USF

-46.35%

Renewables

The full list

Fund

Discount

Sector

Ruffer RICA

-7.59%

Flexible

Biotech Growth BIOG

-15.10%

Healthcare

BBGI Global Infrastructure BBGI

-19.52%

Infrastructure

Ceiba Investments CBA

-74.95%

Property

Octopus Renewables Infrastructure ORIT

-38.96%

Renewables

Gore Street Energy Storage GSF

-52.31%

Renewables

Aquila Energy Efficiency AEET

-46.99%

Renewables

Bluefield Solar Income BSIF

-33.20%

Renewables

Ecofin US Renewables RNEW

-53.19%

Renewables

Foresight Environmental Infrastructure FGEN

-38.07%

Renewables

Foresight Solar FSFL

-38.00%

Renewables

Greencoat Renewables GRP

-30.16%

Renewables

Greencoat UK wind UKW

-23.10%

Renewables

US Solar Fund USF

-46.35%

Renewables

Oryx International OIG

-35.60%

UK Smaller Companies

Vietnam Enterprise VEIL

-24.46%

Vietnam

Funds mentioned in this article: Ruffer Investment Company Biotech Growth Ord Oryx International Growth Ord Vietnam Enterprise Ord BBGI Global Infrastructure Ord Aquila Energy Efficiency Trust Ord Gore Street Energy Storage Fund Ord Foresight Environmental Infra Ord Foresight Solar Ord US Solar Fund Ord Ecofin US Renewables Infrastructure Ord Greencoat Renewables Greencoat UK Wind Bluefield Solar Income Fund Octopus Renewables Infrastructure Ord

The Telegraph spots an outlier in London’s investment trust space: M&G Credit Income (MGCI). Outlier, because such has been demand for the debt fund that it has actually been able to issue new shares; while The Times thinks investors could soon wake up to the opportunity that is value investing and cites Temple Bar’s (TMPL) outperformance of the wider market over the last 3 years as evidence.

By Frank Buhagiar

Questor – This trust offers a yield more than three times greater than inflation

M&G Credit Income Investment Trust (MGCI) is a fund in demand. Exhibit#1: MGCI issued 6.6m shares to satisfy demand over the past year. Exhibit#2: The shares trade at a 1% premium to net assets, making the debt fund something of an outlier in London’s investment company space. All the more impressive given The Telegraph’s Questor Column describes the current environment for a fund manager investing in debt as “tricky.” A nod to rising government borrowing costs around the world.

The fund’s attractive dividend yield of around 8.4%, “making it one of the higher yielding trusts in its peer group”, one reason cited for why the shares are in demand – the annual dividend is calculated at 4% plus Sonia (the sterling interest rate benchmark), meaning the dividend moves up and down with official interest rates. The high payout level is down to the fund’s relatively high exposure to private credit (53% of the portfolio as at the end of November 2024) – private credit securities tend to come with higher yields, compensation for having lower liquidity compared to public credit.

Risk management appears front and centre of the investment approach. 80% of the portfolio is invested in floating rate debt thereby making the fund less sensitive to interest rate risk compared to peers. Meanwhile, 70% of the portfolio is invested in investment grade debt. The portfolio is well diversified too – in all there are 130 holdings. According to Questor “Across its six-year life, the portfolio has experienced some defaults, but diversification and good credit analysis means the impact has been limited.” That does mean that “M&G Credit Income’s returns are respectable but not best in class” which leads Questor to “suspect that investors’ degree of enthusiasm for the trust will reflect their individual risk appetite. Questor says: hold”. Well they do say each to their own.

Tempus – Is it time to look at value investing? There may be good returns

As The Times’ Tempus points out “Value investing is not as popular as it once was among first-time retail investors, with most market newcomers seeking out racier returns in the world of artificial intelligence, fintech or even cryptocurrency rather than in unloved stocks.” But this could be changing as investors “wake up to the value opportunity in the UK market”. It’s an opportunity that value investor Temple Bar Investment Trust (TMPL) has been capitalising on – over the last three years the fund has generated a total return of +24%, easily beating the FTSE All-Share’s +17%.

The outperformance, testament to the fund managers Nick Purves and Ian Lance at Redwheel, who have been running the fund since October 2020, and the trust’s concentrated portfolio of 34 stocks, a third of which belong to the financial sector. Since Purves and Lance have been at the helm, TMPL has generated a net asset value total return of over +100%. That compares favourably to its UK equity income peers, which have delivered a weighted average return of around +86%.

The shares also offer a dividend yield of 3.6%, although that is slightly lower than the 4.3% sector average. And then there’s the discount which, according to Tempus, “suggests that the fund represents decent value for a prospective investor. It currently stands at just over 8%, slightly wider than recent history and compared with an average discount of 4.9% among rival funds. Advice Buy.” The value investor a value play itself, it seems.

The Results Round-Up: The week’s investment trust results

The Saba Saga reaches the Weekly Round-up. 2 of the 7 targeted by the activist reporting impressive numbers: Baillie Gifford US Growth (USA), +29.4% NAV return; Edinburgh Worldwide (EWI), NAV up +12.8% for the year and up +13.3% between 31 Oct and 31 Dec 2024 alone. Elsewhere, CC Japan Income & Growth (CCJI) and Invesco Asia (IAT) post NAV total returns of +16.1% and +6.3% respectively.

By Frank Buhagiar

Edinburgh Worldwide (EWI) needs shareholders to vote

EWI put out what could be its last set of annual results as an investor in global smaller companies – unless shareholders turn out in force to reject activist investor Saba Capital’s proposals at the upcoming general meeting on 14 February – Saba proposing to replace the Board with its own appointees, appoint itself manager and then switch to a strategy centred on investing in other investment trusts. All a far cry from what Chairman Jonathan Simpson-Dent describes as EWI’s “unique portfolio of publicly traded and private businesses operating at frontiers of technological innovation and transformation. The Company is a global smaller companies specialist aiming to generate long-term capital appreciation by early access to emerging businesses with significant disruptive growth potential.”

As for performance, during the year to 31 October 2024, net asset value (‘NAV’) per share increased +12.8% and the share price +26.1%. That compares to the S&P Global Small Cap Index’s +21.6% total return in sterling terms. Simpson-Dent believes this could be “the long-awaited start of Edinburgh Worldwide’s recovery.” And he could well be right as since period end share price and NAV are up +23.6% and +13.3% respectively between 31 October and 31 December 2024 – the S&P Global Small Cap Index by contrast is up just +2.5%.” The existing strategy coming good then. Thing is, the nascent recovery could well be stopped in its tracks if shareholders don’t show up and vote against Saba’s proposals at the upcoming general meeting. Share price hardly moved on the day – shareholders perhaps too busy instructing their brokers to vote against Saba’s proposals.

Numis: “The Board of Edinburgh Worldwide (EWI) has published a circular for a general meeting to be held 14 February requisitioned by activist investor Saba Capital, which currently holds 23.7% of EWI’s share capital, in which it urges shareholders to vote against all resolutions. Since 31 October, EWI’s NAV total return is 17.1% vs. 7.2% for the benchmark.”

JPMorgan: “EWI’s main argument in its defence is that its strategy is a unique one that has a good long-term record. But while it can point to a 125.3% NAV TR since 31/12/14 (8.5% pa) to 16/1/25, with 147.7% TSR (9.5% pa) over the same period, both have lagged behind the benchmark’s 163.4% (10.1% pa). That said, the unquoted portfolio makes a true comparison with a fully quoted benchmark more challenging. Even though EWI has underperformed, the mandate remains more interesting, in our view, than Saba’s potential offering, but given the performance difficulties over recent years some shareholders may not give EWI the benefit of the doubt. We estimate that with no votes from platforms, EWI would need to muster support of around 62% of its remaining shareholder base of ~38% to defeat Saba, assuming no further increase in Saba’s stake.”

Baillie Gifford US Growth (USA) posts +29.4% NAV return but will it be enough to keep Saba at bay?

USA reported an eye-catching +29.4% NAV return over the latest half-year period, almost double the S&P 500’s +15.3% total return in sterling terms. But as the Half-year Report notes “despite this extremely strong performance, Saba (Capital) has sought to introduce self-serving and destructive proposals to remove the independent Board and try to assume control of the Company.” Because of this “The Company and the strong growth potential shown in today’s results is directly under threat in a vote where every vote will count. We therefore reiterate urging all shareholders to VOTE AGAINST Saba’s proposals – it’s critical they do not miss the opportunity to save their investment from an uncertain and potentially destructive trajectory.”

For those thinking one impressive half-year performance does not a summer make, the longer-term performance record stacks up too: since launch on 23 March 2018 to 30 November 2024, the NAV return stands at +186.1%, pretty much in line with S&P 500’s +190.5% in sterling terms. No wonder Chair Tom Burnet doesn’t hold back in his statement “Saba is cynically counting on other shareholders not voting their shares to give them the best chance of taking effective control of the Company. Therefore, it is vital that shareholders vote on the Requisitioned Resolutions no later than 12 noon on 30 January 2025 (platform voting deadlines will be earlier) as the future of their investment depends on it.” A rallying cry from the Chairman and a rally in the share price on the day of the results too – up 4.5p to 262p.

Numis: “In the interim results, the current Board repeats its call to shareholders to vote against the resolutions, a view we echo. It has undoubtedly been a difficult time since the peak of the 2021 euphoria around tech companies, but USA’s record from launch remains good, with NAV total returns of 197%, marginally behind the 202% for the S&P 500, which has been a difficult index to beat given the dominance of a few tech companies. Performance has picked up with NAV total returns of 40.0% vs 30.1% for the S&P 500 over the last year.”

Liberum: “Significant outperformance by the largest cadre of companies in the US has presented a headwind, yet the focus on idiosyncratic opportunities in exceptional companies has helped the managers generate outsized returns from select holdings, in-line with the stated investment process, and we think there remain significant further opportunities for significant upside from names within the portfolio. Recent returns have benefitted from a narrowing of the discount; whilst Saba have claimed that this is as a result solely of their buying, we note that discount narrowing also coincided with a pick-up in NAV relative returns.”

CC Japan Income & Growth’s (CCJI) beats the index and the drum

CCJI’s full year NAV total return came in at +16.1%, comfortably ahead of the Topix’s +13.4% (sterling). The outperformance no one-off either. The cumulative NAV total return since inception in 2015 to 31 October 2024 stood at +152.5%, easily beating the TOPIX’s +100.6%. Chair June Aitken thinks “This long-term track record of high absolute returns and outperformance of the Index attests to the Investment Manager’s skill in identifying companies paying income to shareholders whilst still offering strong growth potential.” Hard to argue with those numbers.

Good to see Aitken taking the opportunity to beat the drum for investment trusts in her statement “for a plethora of reasons, not least including high costs and lack of access across platforms, investing directly into Japanese equities is challenging for individual UK investors and we believe that investment trusts provide a low cost and effective means by which to do so. In a complex investment region like Japan, active management is needed to unlock the most attractive return profile.” Can’t argue with that either. Shares ended the day 1.5p higher at 191p.

Numis: “Outperformance has continued post period end with the NAV up 4.4% on a total return basis, vs a 3.0% return from the Topix, in sterling terms. We note the fund has a three-yearly continuation vote, with the next coming up at the AGM in March 2025.”

Invesco Asia’s (IAT) big ambitions

IAT’s +6.3% NAV total return for the half year couldn’t quite match the MSCI AC Asia ex Japan Index’s +8.6%. Share price total return fared better though, up +9.6%. Perhaps that’s down to shareholders getting excited about the company’s proposed combination with Asia Dragon (DGN) which is due to complete on 14 February 2025, Valentine’s Day of course – is there a romantic or two among those involved in the tie-up? Certainly Chairman Neil Rogan has big ambitions for the enlarged trust “Our aim is to make this the go-to Asian trust, trading on a premium rating, growing organically and also through further combinations.”

Who’s to say Rogan won’t get what he wants. After all, he has got his way in the past as “In previous Chairman’s Statements I lamented that not much had changed. Now everything seems to be changing” and goes on to cite Trump’s victory in the US election and his plans to impose tariffs and cut taxes. “Many have already defaulted to a pessimistic scenario or are waiting on the sidelines but there is a significant probability of a positive outcome. Even a muddling-through outcome could produce positive returns, especially given the relatively low starting valuations for many of Asia’s stockmarkets.” Here’s to just muddling through. Shares closed off 3p to 340p – market sitting on the sidelines until the DGN tie-up completes?

Winterflood: “Underperformance primarily driven by underweight position in Chinese Financials. As previously announced, the combination with Asia Dragon, whereby IAT will be the ongoing vehicle, has been approved by IAT shareholders and remains conditional upon, amongst other things, the passing of resolutions at GMs of DGN to be held on 4 and 13 February.”

Why Dividend Investing is the Ultimate Long-Term Strategy

When it comes to investing for the long term, dividend investing stands out as one of the most reliable and rewarding strategies out there. It’s not just about watching your portfolio grow over decades—it’s about getting paid to wait while it does. That’s why I love it. And here’s why I believe dividend investing is the king of long-term investing.

1. Dividends Are Real Cash in Your Pocket When a company pays a dividend, it’s literally handing you a portion of its profits. This isn’t some hypothetical future value or a “maybe someday” scenario—it’s cold, hard cash hitting your account. And you can do whatever you want with it: reinvest, pay bills, or treat yourself. Contrast that with growth stocks, where you’re banking on the hope that the price goes up. Dividends give you tangible returns right now, regardless of what the stock price is doing.

2. The Magic of Compounding Reinvesting dividends is where the real magic happens. Each dividend payment buys you more shares, which then earn more dividends, which buy even more shares. It’s like a financial snowball rolling downhill, getting bigger and bigger over time. This compounding effect is one of the most powerful forces in investing, and dividend stocks make it easy to harness. The longer you stick with it, the more impressive the results become.

3. Stability and Predictability Dividend-paying companies are often established, financially stable businesses with a history of profitability. They’re not swinging for the fences—they’re focused on consistent performance. That stability can provide peace of mind during market turbulence. Plus, many companies aim to increase their dividends every year, even during downturns. That means your income keeps growing, regardless of what’s happening in the broader market.

4. Built-In Discipline Dividend investing encourages a long-term mindset. When you’re focused on building a stream of passive income, you’re less likely to panic during market dips or chase the latest hype stock. It’s all about consistency and patience.

5. It’s a Hedge Against Inflation Over time, inflation eats away at the value of your money. But dividend stocks often provide a natural hedge. Companies that regularly grow their dividends typically do so at a rate that outpaces inflation, helping you maintain your purchasing power.

Bottom Line Dividend investing isn’t flashy, but that’s what makes it so effective. It rewards patience, discipline, and a long-term focus. Whether the market is up, down, or sideways, dividend-paying stocks keep working for you, providing steady income and compounding growth. If you’re looking for a strategy that stands the test of time, this is it. Start small, stay consistent, and watch as your dividendspatience, discipline, and a long-term focus snowball into something incredible over the years.