If you bought at issue price and simply re-invested the dividends, you would be in profit but you would have built a substantial holding, which hopefully you will be benefit from, one day..

Yield on issue 5.5%. Current yield 8.5%

Discount to NAV 20%

GOLDMAN RAISES SUPERMARKET INCOME REIT PRICE TARGET TO 94 (92) PENCE – ‘BUY’

Supermarket Income announced a dividend of 6.1p per share, up 1.7% from 6.0p a year ago.

Looking ahead, Chair Nick Hewson said: “In the context of the recently challenging macro headwinds, we can now begin to consider the possibility of a more favourable interest rate environment. Market expectations of modest interest rate cuts over the coming months, albeit not returning to the levels of the 2010s, provide confidence that we have now seen the floor in this current cycle.”

He added: “Looking ahead, we remain optimistic that the improving interest rate environment should provide positive tailwinds for the company.”

3 Tax-Free Funds Throwing Off “Stealth” Dividends Up to 12%

Michael Foster, Investment Strategist Updated: February 24, 2025

Today we’re going to use a simple strategy to (legally!) beat the tax man. The key is a (too) often-ignored group of funds whose dividends are beyond the reach of the IRS.

The low-risk assets behind this income stream really should be part of any income investor’s portfolio. And the three funds we’ll discuss below, which yield up to 7.3%, are a great place to start. Thanks to their tax-free status, their “real” yields will likely be considerably more for us.

Enter “Boring But Beautiful” Municipal-Bond Funds

Here’s the truth on taxes: If you’re an American and you receive any kind of income, you’re going to get taxed. This is a constant of life. But there is one exception: municipal bonds, the income from which is tax-free for most Americans.

That tax-exempt status drives plenty of investors to muni bonds, making them a secret weapon for state and local governments and American industry, as these bonds fund many infrastructure and other public works projects around the country.

It adds up to a big difference-maker for many folks. A municipal, or “muni,” bond yielding 4% might not seem impressive at first glance, but for someone in the top federal tax bracket, this 4% tax-free yield is equivalent to a taxable yield of 6.6%.

And of course, the higher our “headline” muni-bond yields get, the bigger the taxable-equivalent yield: for that same taxpayer in the top federal bracket, for example, 5% yields turn into 8.3% on a taxable-equivalent basis.

Creating Your Own “Tax-Free Income Machine”

The best way to buy municipal bonds is through closed-end funds (CEFs), which give us three key advantages:

Active management: The world of municipal bonds is challenging for individuals to access, so we want pros from well-established firms like BlackRock, Nuveen and others “running” our muni-bond portfolio for us.

High yields: Plenty of muni-bond CEFs pay 4%, 5% and more, which, as we just saw, translates into a bigger yield on a taxable-equivalent basis.Discounts to net asset value (NAV): Because CEFs have more or less fixed share counts for their entire lives, they can, and often do, trade at different levels than the per-share value of their portfolios, and regularly at discounts. That lets us buy our “munis” for 90, 85 and sometimes even fewer cents per dollar of assets, as we’ll see in a moment.

With all that in mind, let’s go ahead and create a tax-free income portfolio with just three CEFs, all of which are diversified across municipalities, projects and credit ratings.

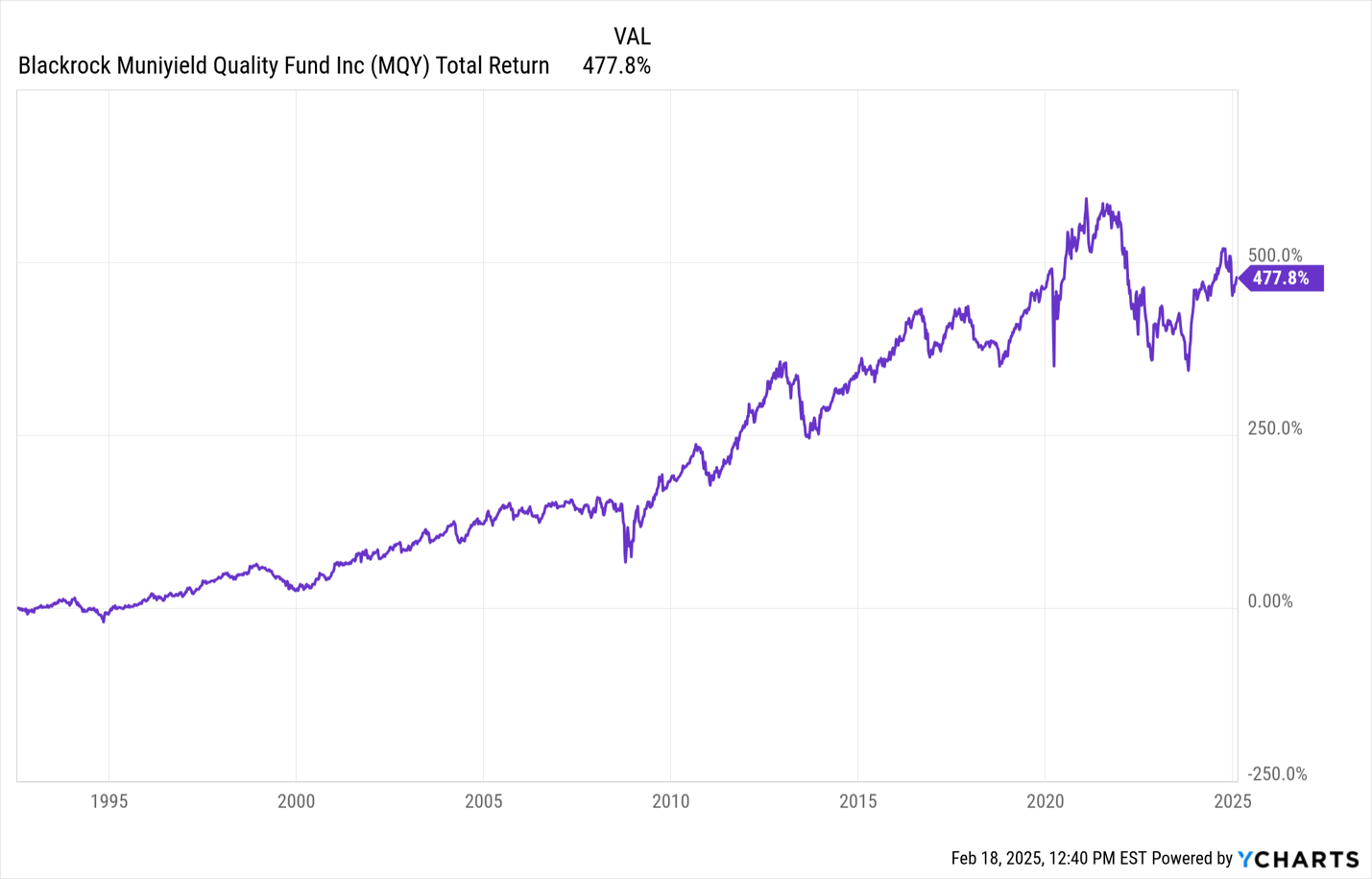

Muni Pick #1:BlackRock MuniYield Quality Fund (MQY)

MQY is notable for its consistent performance and ability to offer tax-free income for a long time, making it a great long-term hold.

MQY’s Long History of Profits

MQY currently trades at a 7% discount to NAV, so we’re paying 93 cents for every dollar of assets with this one. Cheap! Moreover, like all muni-bond funds, MQY dropped in 2022, as interest rates rose. But now, with rates having come down a bit, and likely to move lower over time, the fund is nicely positioned to grind higher, in addition to handing us a nice long-term (and of course tax-free) income stream.

The kicker here is that MQY’s 5.9% yield—already attractive on its own—“converts” to a 9.8% taxable-equivalent yield for top income earners.

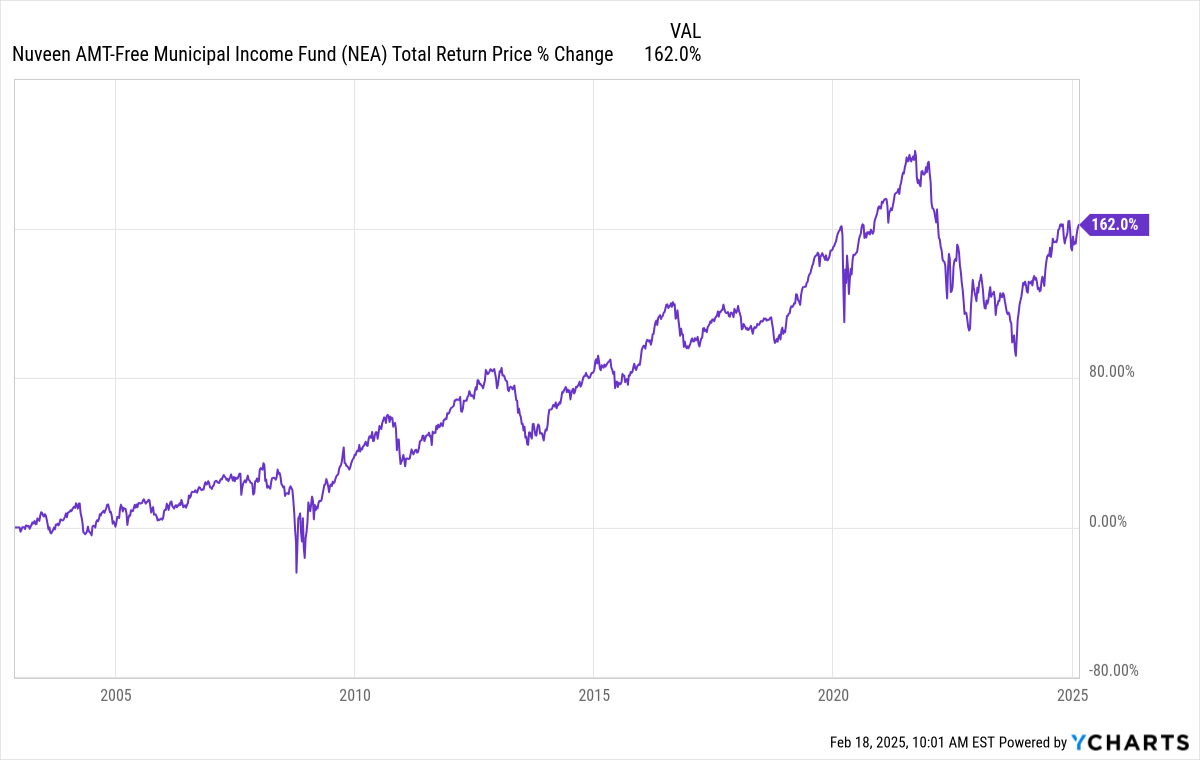

Muni Pick #2:Nuveen AMT-Free Quality Municipal Income Fund (NEA)

Let’s carry on with NEA, known for its strong management team (Nuveen gets access to high-quality municipal-bond issuances early, which is possible thanks to the company’s deep contacts in the muni-bond world and the fact that the muni market is small).

Like MQY, NEA trades at a discount (4.9% in this case) but its yield clocks in at a massive 7.6%, thanks in no small part to higher yields the fund has been able to lock in as interest rates rose and stayed elevated.

And like MQY, this fund has a long track record of healthy total returns, especially for a stable asset class like munis.

NEA Keeps Delivering Income and Gains

Bear in mind, too, that thanks to NEA’s high yield, much of that return has come in the form of dividend cash.

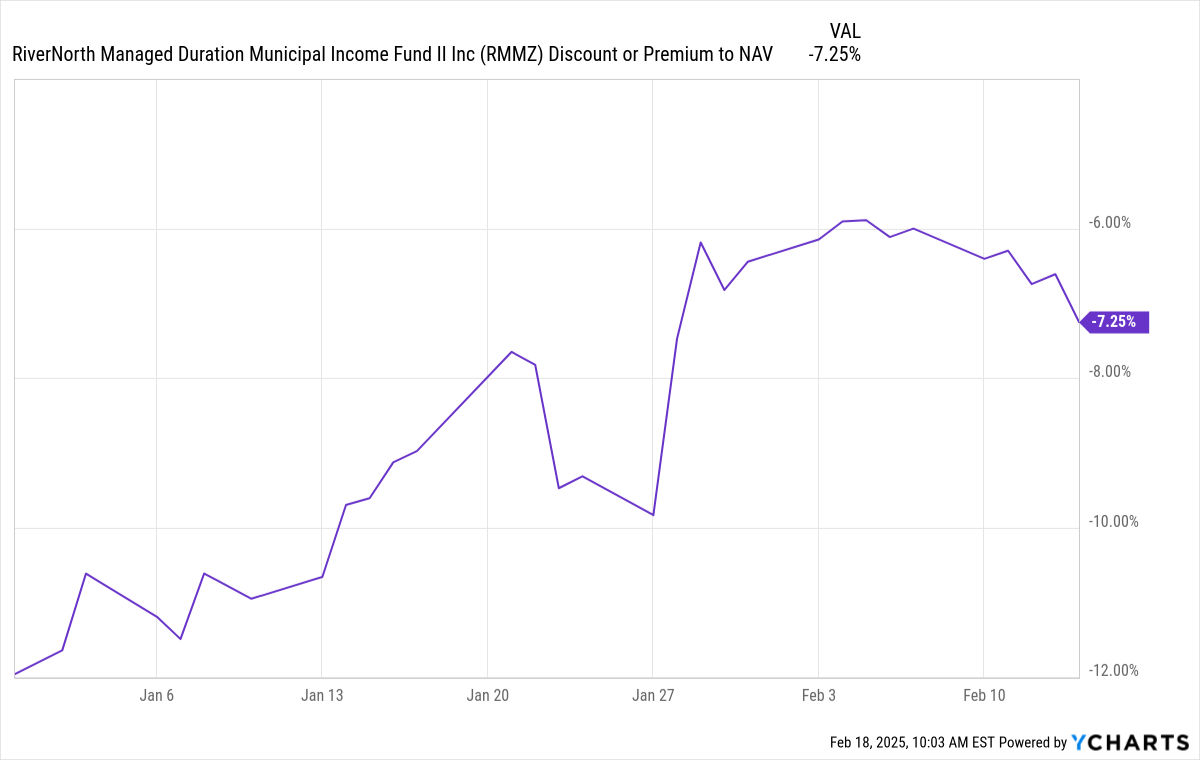

Muni Pick #3:RiverNorth Managed Duration Municipal Income Fund II (RMMZ)

Finally, for further diversification in the muni-bond fund space, consider RMMZ, which has an interesting method of managing duration and credit risk: It buys more individual municipal bonds when the muni market is hot, then leans more into buying other muni-bond CEFs when the market is cold and CEF discounts are unusually wide.

RMMZ’s Clever Approach to Maintaining Income

Source: RiverNorth Capital Management

This fund also trades at a wide discount to NAV—7.4% today—which is yet again a nice bonus for a high-yielding fund. But the real standout stat is RMMZ’s yield: 7.2%. On a taxable-equivalent yield basis, that’s 12%. Plus, RMMZ’s discount to NAV has been eroding, giving investors who buy at a discount the potential to sell at a profit as the discount shrinks.

RMMZ’s Discount Is Evaporating

RMMZ is far from perfect: its payouts were cut at the start of 2025 by two-tenths of a penny, and if that were to happen again, its current yield would “fall” to around 7%, with little effect on that 12% taxable-equivalent yield for our top income earner!

I don’t know about you, but that’s a pretty reasonable “downside” to me. The upside is that these funds all have diversified portfolios in municipal bonds, which sport just a 0.1% default rate across the asset class.

The bottom line: If you need a tax break (and who doesn’t?), these are three funds worth serious attention.

Play Defense With Munis. Then BUY These 10% Dividends for Trump 2.0 GAINS

I know there’s a lot of uncertainty out there, and these 3 muni-bond CEFs, with their stability and huge tax-free dividends, are the perfect way to protect your portfolio.

But we do NOT want to fully pull back into our shell. Because Trump 2.0, despite its disruption out of the gate, is going to set us up with some terrific income (and growth) opportunities in the coming years—and we do NOT want to miss out on those.

Contrariain Outlook

$$$$$$$$$$$$$$$$$

I know absolutely nothing about Munis, so it’s strongly advised that you do further research before deciding to invest any of your hard earned.

The current profit for the Snowball on closed positions is £13,443.00

The current loss for the Snowball on closed positions is £8,855.00

Both include dividends received.

Whilst the Snowball’s plan isn’t a trading strategy but a buy and hold forever, if the market gods allow it, if a profit can be taken and invested back into a higher yielder, the Snowball will grow quicker.

Remember a profit is not a profit until the underlying share is sold and the profit banked.

Obviously, we should all think more like Warren Buffett

By James Baxter-Derrington Investment Editor

Each and every year since Berkshire Hathaway stopped operating primarily as a textile manufacturer and began its path to synonymity with “investing genius”, its chair has produced an annual letter.

Since 1973, the Oracle of Omaha has also invited shareholders to quiz him in person at an event which has come to be known as “Woodstock for Capitalists”.

With Woodstock still a few months away, investors will have to make do with Warren Buffett’s annual letter for now.

Part of Buffett’s appeal is precisely what allows him to succeed so famously – contrition and honesty.

The very first subhead of his letter reads “Mistakes – Yes, We Make Them at Berkshire”. In fact, Berkshire’s birth as Buffett’s investment vehicle was a mistake, if you ask him. Thanks to a desire to get even with somebody he felt had slighted him, Buffett says he missed out on $200bn of compound returns by purchasing the firm.

There is nobody so famous for offering investment lessons as Buffett, and his letter continues in this vein. A tip for life as well as investing, he describes “delaying the correction of mistakes” as the “cardinal sin” – or, in the words of his late business partner Charlie Munger, “thumb-sucking”.

“Problems, he would tell me, cannot be wished away. They require action, however uncomfortable that may be.”

Delaying the inevitable will only ever cause further pain – a 50pc loss is considerably better than a 100pc loss.

To be honest with yourself is also to prevent yourself from believing lies – was your 2018 purchase of Tesla really genius? Did you actually predict 1,800pc growth?

“If you start fooling your shareholders, you will soon believe your own baloney and be fooling yourself as well,” he says.

The letter also takes a moment to touch on a point I addressed last week – the opportunity of Japan.

Given the firm’s near-entire US focus, it bears considering just what it means for Berkshire to have spent the past six years building stakes in Japanese companies.

The rationale was straightforward: “We simply looked at their financial records and were amazed at the low prices of their stocks. As the years have passed, our admiration for these companies has consistently grown. Greg has met many times with them, and I regularly follow their progress. Both of us like their capital deployment, their managements and their attitude in respect to their investors.”

(Greg is Greg Abel, heir apparent to Berkshire Hathaway.)

Has it worked? Berkshire has spent an aggregate $13.8bn (£10.9bn) purchasing its stakes, which are currently worth $23.5bn.

Buffett also references the success of their “yen-balanced strategy” – “the annual dividend income expected from the Japanese investments in 2025 will total about $812m and the interest cost of our yen-denominated debt will be about $135m”.

Decent.

To invest like Warren Buffett is simple – buy Berkshire Hathaway; to think like Warren Buffett is a little tougher, but will offer returns beyond capital growth.

Depending when you bought you may be sitting on a substantial loss.

You would have built up a large position with the Trust, so stick to your task until it stick’s to you, as long as it continues to pay a dividend.

Current yield 7.6%

Discount to NAV 35%

Dividends

The Company has declared the following interim dividends in respect of the year:

Quarter to

Declared

Paid/to be paid

Amount (p)

30 June 2024

31 August 2024

6 October 2024

1.6

30 September 2024

22 November 2024

27 December 2024

1.6

Total

3.2

The total dividend was therefore in line with the Group’s target for the year of 3.2p. 1.6 dividends were property income distributions and 1.6 was a non-property income distribution. The cash cost of the total dividend for the year will be £13.6 million (30 September 2023: £13.6 million).

Nov 2024

19 February 2025

Warehouse REIT plc

(the “Company” or “Warehouse REIT”, together with its subsidiaries, the “Group”)

Dividend Declaration

The Company has declared its third interim dividend in respect of the third quarter of the financial year ending 31 March 2025 of 1.60 pence per ordinary share, payable on 11 April 2025 to shareholders on the register on 14 March 2025. The ex-dividend date will be 13 March 2025.

The dividend of 1.60 pence per ordinary share will be paid in full as a Property Income Distribution.

“First of all, never play macho man with the market. Second, never overtrade”. – Paul Tudor Jones

Most investors prefer to do something rather than do nothing, even when that something often proves to be an unnecessary mistake, notably overtrading. Overtrading, or excessive buying and selling or churning of investments, is a mistake that can erode total returns.

It is essentially the mistake of being a ‘busy fool’ or being reactive rather than proactive. We can often believe we are being productive by continually reacting to changes in our investments when we are doing so unnecessarily.

Frequent trading often incurs additional transaction costs and increases the chances of making impulsive, ill-informed and costly decisions. Investors should adopt a disciplined approach and resist the urge to trade excessively.

It is essential to identify a well-defined strategy and stick to it, avoiding unnecessary transaction costs and potential losses. One of the main mistakes people make when trading or investing is focusing only on making very high returns in a short period.

abrdn Equity Income Trust PLC ex-dividend date abrdn European Logistics Income PLC ex-dividend date Alliance Witan PLC ex-dividend date Downing Renewables & Infrastructure Trust PLC ex-dividend date Scottish American Investment Co PLC ex-dividend date Triple Point Venture VCT PLC ex-dividend date

If you had bought after the Covid crash and simply re-invested the dividends, you are near to achieving the holy grail of investing in that you will be able to take out your stake and re-invest in another high yielder.

Current yield on RECI 9.7%, if you re-invested the capital in another Trust (for comparison purposes only) of 10.3% your yield on invested capital would be 20%.

Long term investing and if you look at the start of the chart, a good reason for booking profits and re-investing to spread the risk.

Again a simple do nothing strategy, apart from re-investing the dividends.

Is the dividend secure ?

The fcast is to flatline at the current yield of 9.7% based on todays price.

What do they do ?

Real Estate Credit Investments Limited (RECI) is a closed-ended investment company which originates and invests in real estate debt secured by commercial or residential properties in the United Kingdom and Western Europe.

RECI is externally managed by Cheyne Capital’s real estate business was formed in 2008 and currently manages $6.5bn via private funds and managed accounts. Its investments span the entire spectrum of real estate risk from senior loans, mezzanine loans, special situations to direct asset development and management.

RECI’s aim is to deliver a stable quarterly dividend with minimal portfolio volatility, across economic and credit cycles, through a levered exposure to real estate credit investments.

Investments may take different forms but are principally in:

Self-Originated Deals: predominantly bilateral senior real estate loans and bonds

Market Bonds: listed real estate debt securities such as Commercial Mortgage Backed Securities (CMBS) bonds.

Loan arranger, higher risk but loans secured on property provides some security.

Not that one though.

Real Estate Credit Investments Limited (the “Company”)

Ordinary Dividend for RECI LN (Ordinary shares)

Real Estate Credit Investments Limited announces today that it has declared a third interim dividend of 3.0 pence per Ordinary Share for the year ending 31 March 2025. The dividend is to be paid on 4 April 2025 to Ordinary Shareholders on the register at the close of business on 14 March 2025. The ex-dividend date is 13 March 2025.

How you could bank tens of thousands of dollars in yearly dividend cash for every $500,000 invested, and …

A half-million dollars is a lot of money. Unfortunately, it won’t generate much income today if you limit yourself to popular mainstream investments.

The 10-year Treasury pays around 4% as I write this. That’s not bad, historically speaking, but put your $500K in them and you’re only looking at $20,000, barely over the poverty level for a two-person household. Yikes.

And dividend-paying stocks don’t yield nearly enough. For example, Vanguard’s popular Dividend Appreciation ETF (VIG) pays around 1.7%. Sad.

When investment income falls short, retirees are often forced to sell their investments to supplement their income.

Of course, the problem here is that when capital is sold, the payout stream takes an immediate hit – so that more capital must be sold next time, and so on.

Avoid the Share Selling “Death Spiral”

Some financial advisors (who are not retired themselves, by the way) say that you can safely withdraw and spend, say, 4% of your retirement portfolio every year. Or whatever percentage they manipulate their spreadsheet to say.

Problem is, in reality, every few years you’re faced with a chart that looks like this.

Apple’s Dividend Was Fine – Its Stock Wasn’t

As you can see, the dividend (orange line above) is fine — growing, even — but you’re selling at a 25% loss!

In other words, you’re forced to sell more shares to supplement your income when they’re depressed.

Remember the benefits of dollar-cost averaging that built your portfolio? You bought regularly, and were able to buy more shares when prices were low?

In this case, you’re forced to sell more shares when prices are low.

When shares rebound, you need an even bigger gain just to get back to your original value.

The Only Reliable Retirement Solution

Instead of ever selling your stocks, you should instead make sure you live on dividends alone so that you never have to touch your capital.

This is easier said than done, and obviously the more money you have, the better off you are. But with yields still pretty low, even rich folks are having a tough time living off of interest today.

And you can actually live better than they can off of a (much) more modest nest egg if you know where to look for lesser-known, meaningful and secure yield.

I’m talking about annual income of 8%, 9% or even 10%+ so that you’re banking $50,000 (and potentially more) each year for every $500,000 you invest.

You and I both know an income stream like that is a very nice head start to a well-funded retirement.

And it’s totally scalable: Got more? Great!

We’ll keep building up your income stream, right along with your additional capital.

And you’ll never have to touch your nest egg capital – which means you won’t have to worry about or running out of money in retirement, or even the day-to-day ups and downs of the stock market.

The only thing you need to concern yourself with is the security of your dividends.

As long as your payouts are safe, who cares if your stock prices swing up or down on a given day?

Most investors know this is the right approach to retirement.

Problem is, they don’t know how to find 8%, and 10% yields to fund their lives.

And when they do find high yields, they’re not sure if these payouts are safe. Will the company or fund have enough cash flow to pay the dividends into the future?

And how sensitive are these payouts to the latest headline, Fed policy changes or unrest on the other side of the globe?

The ONE Thing You Must Remember

If I could leave you with just one nugget of investing wisdom today, it would be to NEVER overlook the incredible wealth-building power of dividends.

Few investors realize how important these unglamorous workhorses actually are.

Here’s a perfect example…

If you put $1,000 in the dividend-paying stocks of the S&P 500 back in 1973, you would have had $87,560 by 2023, or 87x your money.

But the same $1,000 in the non-dividend payers would have grown to just $8,430 — 90% less.

That’s why I’m a dividend fan.

The stock market is a fantastic wealth-building machine, but it doesn’t always go straight up!

There have been plenty of 10-year periods where the only money investors made was in dividends.

And that’s what gives us dividend investors such an edge.

When you lock in an 8%+ yield, you’re booking an income stream that’s bigger than the stock market’s long-term average return right off the bat.

Of course you can’t just buy every ticker symbol out there with a flashy yield, or you’ll get burned pretty fast.

So let’s wipe the false promises of mainstream finance from our minds and start thinking the “No Withdrawal” way…

Supermarket Income REIT plc (LSE: SUPR), the real estate investment trust with secure, inflation-linked, long-dated income from grocery property, is pleased to announce its progress against a number of key portfolio initiatives which were outlined in the announcement on 18 November 2024. These significant actions demonstrate the attractions of our high quality portfolio, our conservative valuations and our ability to recycle capital to drive earnings accretion.

Sale of Tesco, Newmarket for £63.5 million

The Company has completed the sale of Tesco, Newmarket to its operator, Tesco plc, for £63.5 million. The sale was completed at a 7.4% premium to the 30 June 2024 valuation. This sale of a large format omnichannel store at an attractive valuation, underlines the strategic importance of the Company’s assets to the supermarket operators. The passing rent of the store upon disposal was £3.5 million.

In recycling the proceeds, the Board will consider options to create accretive value for shareholders.

The Company continues to actively explore opportunities to recycle capital through individual asset sales and potential joint ventures at attractive valuations.

Lease renewals – average 4% rent to turnover[1] and 35% above MSCI rents

The Company has successfully completed three lease renewals on Tesco stores located in Bracknell, Bristol and Thetford, which were the three shortest leased Tesco stores in the Company’s portfolio. These store leases have been renewed at an average 4% rent to turnover1, 35% above MSCI’s supermarket benchmark index and 13% above the Company’s valuer’s estimated rental values (as at 30 June 2024). The leases have been extended to 15 years with annual RPI-linked rent reviews (subject to a 4% cap and a 0% floor). The regeared stores are expected to benefit from a capital value growth which will be fully reflected in the 30 June 2025 valuation.

The lease renewals demonstrate the affordable rental levels for the Company’s strong trading, large format omnichannel stores. The Company’s WAULT has increased from 11 years to 12 years[2]. The Company’s next material lease expiry is not until 2032[3].

Earnings enhancing acquisitions – nine omnichannel Carrefour supermarkets in France

The Company has continued to demonstrate its ability to deploy capital into earnings enhancing assets with an attractive spread to the cost of debt. The Company has completed the acquisition of a portfolio of a further nine omnichannel Carrefour supermarkets in France. The stores were acquired through a direct sale and leaseback transaction (“SLB”) with Carrefour, for a total purchase price of €36.7 million (excluding acquisition costs), at a portfolio net initial yield of 6.8%[4]. The Company now has 26 Carrefour stores in France, representing c. 5%[5] of its gross assets.

The nine stores, which have an average gross internal area of c. 40,000 sq ft per store, operate under the Carrefour Market brand and are all well established with long trading histories and low competition in their catchment areas. These omnichannel supermarkets form part of Carrefour’s “Drive” online grocery fulfilment network.

The SLB portfolio has been acquired on a weighted average lease term of 12 years (with a tenant-only break option in year 10), subject to annual uncapped inflation-linked rent reviews.

This acquisition was financed through a private placement with an institutional investor for €39 million of new senior unsecured notes (the “Notes”). The Notes have a maturity of seven years and a fixed rate coupon of 4.1%.

Following the placement of the Notes and receipt of proceeds from the sale of Tesco, Newmarket, the Company has a pro-forma LTV of 38%.

Nick Hewson, Chair of Supermarket Income REIT plc, commented:

“We have made significant progress on the portfolio initiatives that we set out in November 2024, which together are intended to support our earnings growth. These transactions highlight the inherent value of the portfolio, the importance of these stores for the grocery operators and our ability to crystalise value as part of our capital recycling strategy. We remain focused on continuing to make good progress with our remaining strategic initiatives, including delivering further cost savings for the Company, and we look forward to updating the market in due course.”