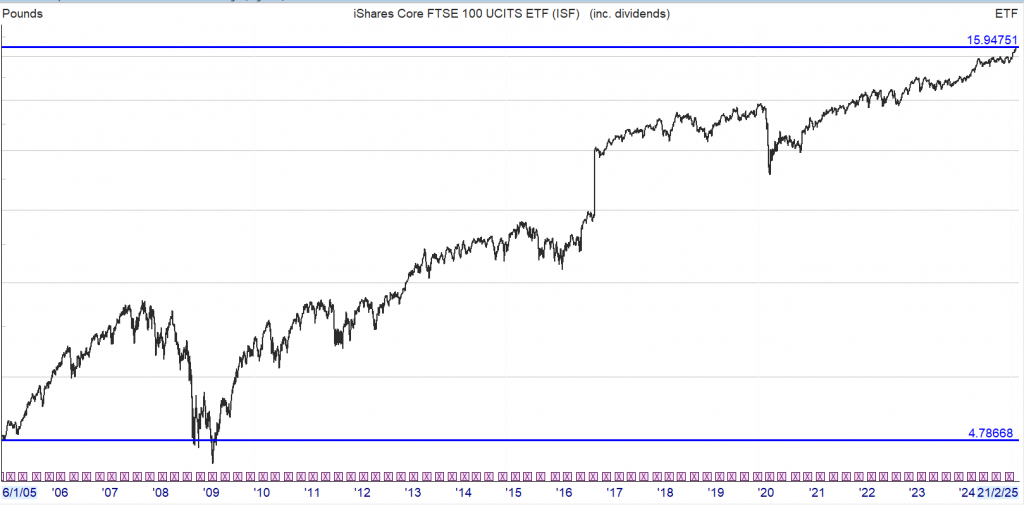

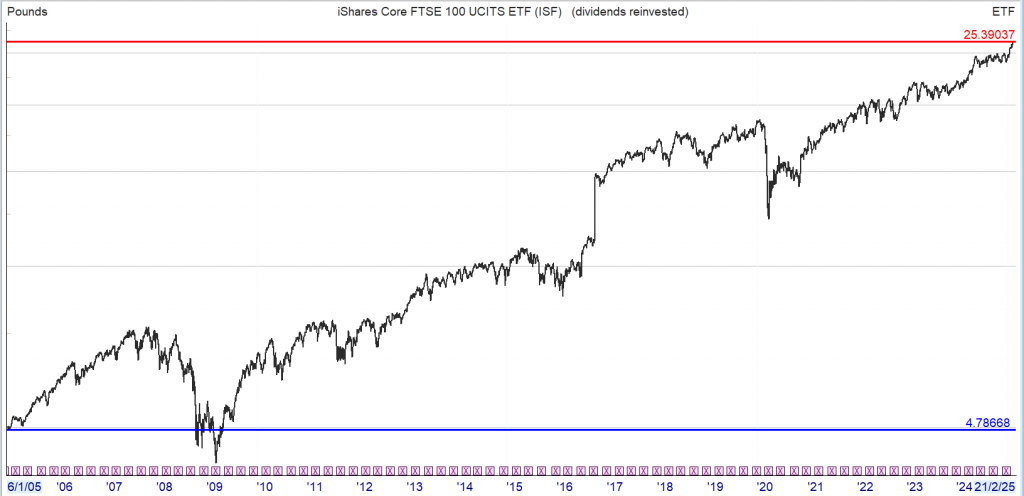

Note: The four years, even including dividends, you made zero, zilch, nothing.

If you knew that falling markets were a plus as you get more shares for your money and you simply stick to your task and re-invest the dividends back into the share, the outcome will always be favourable, that is with a tracker or quasi tracker, if you can choose the time when to sell.

The year has started on a somewhat more positive footing than 2024 ended, with the median average share price across the real estate sector marginally up. The outlier was Ground Rents Income Fund, which has received several proposals for the company that have so far been rejected by the board (see page 3 for details). A potentially groundbreaking deal by Tritax Big Box REIT, which would see it become the largest data centre player in the UK, saw its share price rise by just over 10% in the month. It was also a positive month for fellow logistics specialist Urban Logistics REIT, which had seen its discount to NAV widen to 35% at the end of 2024. It still trades on an unjustifiably wide 30% discount. A positive quarterly trading update from Unite Group saw an in-kind positive reaction in its share price, with the student sector continuing to display compelling supply and demand characteristics and rental growth prospects. Assured inflation-linked rental growth within its care home portfolio saw Care REIT up its dividend target. Meanwhile, British Land went into partnership with an Abu Dhabi investor to unlock the development of a major City of London office scheme.

Caution remains the catchword in real estate stocks, and several continue to lose substantial value, especially for those operating in perceived troubled sub-sectors. Stale house prices and concerns around the strength of the economy weighed on housing developer Henry Boot. Meanwhile, Life Science REIT continues to struggle with a further double-digit fall in its share price. Over 12 months it has lost 40.8% in value and now trades on an astonishingly wide 55% discount to NAV. Coming off a strong 2024, in which its share price rose 14.2%, diversified specialist Schroder REIT had a bumpy start to 2025. It was a similar story for long income specialist Alternative Income REIT and its discount to NAV has now widened to almost 16%. Shareholders seem to have become wary of Phoenix Spree Deutschland’s realisation programme, with the already depressed shares falling another 4.9%. Residential Secure Income is another company undertaking a sell-off of its portfolio. The almost 5% drop in its share price in January may be down to pessimism over how much it would receive for its portfolio of retirement and shared ownership homes after it reported a 5.6% write-down in their value.

Valuation moves

Company

Sector

NAV move (%)

Period

Comments

Picton Property

Diversified

2.3

Quarter to 31 Dec 24

Like-for-like portfolio valuation increase of 2.2% over the quarter to £737.4m

AEW UK REIT

Diversified

0.9

Quarter to 31 Dec 24

1.2% like-for-like valuation increase for the quarter to £192.0m

Safestore

Self-storage

14.6

Full year to 31 Oct 24

13.6% increase in property value to £3,284.1m

Residential Secure Income

Residential

(8.8)

Full year to 30 Sept 24

Portfolio value fell 5.6% to £325.7m

Ground Rents Income Fund

Residential

(34.5)

Full year to 30 Sept 24

Like-for-like reduction in value of portfolio of 30.5%, to £71.5m, over the financial year

With the cost-of-living crisis increasing pressure on households, the importance of earning a second income’s rising rapidly. Luckily, dividend shares offer a potential solution to this problem, allowing focused investors to earn impressive long-term passive income.

So how does investing in dividend shares work? What are the risks? And which dividend stocks should investors consider buying in 2025?

Dividends explained Not all businesses are high-flying enterprises. The London Stock Exchange is home to many mature businesses whose explosive growth days are now in the rear-view mirror. However, with the strong demand for their products and services, their cash flows remain robust. As such, with no other use of capital internally, management teams are returning a large chunk of this cash back to shareholders – the owners.

Typically, dividend payments come every quarter, although this frequency can be different depending on the business and its cash flow timings. However, most companies like to keep payment timing relatively consistent. And investors can leverage that to establish a reliable and predictable income stream.

Due to their maturity, investing in dividend shares is often considered to be a relatively low-risk strategy. And historically, that’s certainly proven to be true in terms of lower share price volatility. However, even the biggest and most stable enterprises have their fair share of threats to contend with.

If cash flows become disrupted, dividends can often find themselves under pressure. And if market conditions become too adverse, shareholders may see their payouts get cut or even outright cancelled. As such, the second income generated by an investment portfolio can take a hit on relatively short notice.

Luckily, such risks can be managed with prudent market monitoring and portfolio diversification.

Best income stocks to buy now? There are a lot of UK dividend shares to pick from. However, not all of them offer the best value or long-term income potential. And depending on the risk tolerance and time horizon of an investor, the best dividend shares to buy can vary, depending on the individual.

That said, there continues to be some interesting opportunities within the real estate sector right now. LondonMetric Property‘s (LSE:LMP) one such business. It’s currently digesting its recent large acquisition of LXi. However, despite generating impressive free cash flow and offering a 6% yield, shares continue to trade at a discounted valuation. Higher interest rates have wreaked havoc on property prices, even in the commercial sector where LondonMetric operates. And with the book value of its assets marked down, shares are still trading at a forward price-to-earnings ratio of 13.9.

To be fair, weakened asset prices can be problematic. Suppose management suddenly needs to sell properties to raise capital. In that case, it will likely have to do it at a discount, given the weakness in the commercial real estate market. And the group’s £2.2bn of debt does add pressure to the bottom line, due to higher interest rates.

However, despite these handicaps, demand from tenants and occupancy remains strong, as do cash flows. That’s why LondonMetric Property’s already in my income portfolio, and I feel other investors may want to consider it for theirs.

The post Here’s how to start earning a second income with dividend shares appeared first on The Motley Fool UK.

Zaven Boyrazian has positions in LondonMetric Property Plc. The Motley Fool UK has recommended LondonMetric Property Plc. Views expressed on the companies mentioned in this article are those of the writer and therefore may differ from the official recommendations we make in our subscription services such as Share Advisor, Hidden Winners and Pro. Here at The Motley Fool we believe that considering a diverse range of insights makes us better investors.

Alternative Income REIT PLC ex-dividend date Fair Oaks Income Ltd ex-dividend date Fair Oaks Income Realisation Ltd ex-dividend date Greencoat UK Wind PLC ex-dividend date ICG Enterprise Trust PLC ex-dividend date Invesco Perpetual UK Smaller Cos Investment Trust PLC ex-dividend date JPMorgan Emerging EMEA Securities PLC ex-dividend date Majedie Investments PLC ex-dividend date Murray Income Trust PLC ex-dividend date NextEnergy Solar Fund Ltd ex-dividend date Octopus Renewables Infrastructure Trust PLC ex-dividend date Pershing Square Holdings Ltd ex-dividend date Target Healthcare REIT PLC ex-dividend date

Investment trusts can hold back up to 15% of the income generated from the underlying holdings each year. In leaner periods, such as during the global financial crisis and the Covid-19 pandemic, many investment trusts maintained or increased their dividends by dipping into income retained during better times.

In contrast, most funds cut dividends as they cannot hold back income and are required to pay investors all the income received each year. So, when there’s a shortage of dividend cheques during challenging times, funds have no get-out-of-jail card and dividend cuts are pretty much inevitable.

How the revenue reserve actually works

It’s easy to get the impression that the revenue reserve is somehow “ring-fenced”, but that’s not the case. In reality, it amounts to little more than an accounting tactic, an entry in the books to show retained revenue. That money is part of the trust’s NAV and is invested in the same way as the rest of the portfolio. If some of it is needed to top up dividend distributions, then the manager has to sell holdings or dip into the cash element and the NAV is affected.

Of course, even for those investment trusts with healthy income reserves, there’s no guarantee that dividends will be maintained or increased.

Purpose of the portfolio

The hypothetical portfolio has been created to show DIY investors how they can build their own diversified income portfolios. The funds are chosen on the basis that over the medium to long term they would be expected to grow both capital and income. However, there are no guarantees that this will be achieved.

Moreover, you must be mindful of the fact that overall total returns (capital and income combined) can decline, especially in the short term.

The line-up for the 2025 portfolio

As I’ve picked each investment trust for the medium to long term, I’m inclined to avoid making many changes each year. However, there are certain things I consider, including a fund manager change, short- and long-term performance, and whether I can simplify the portfolio.

There was a manager change in 2024 at JPMorgan Claverhouse. Its longstanding fund manager of 12 years, William Meadon, departed last summer. The baton has passed to Callum Abbott, who managed Claverhouse alongside Meadon for the past six years. Anthony Lynch and Katen Patel, who oversee the JPM UK Equity Income fund, have also joined Claverhouse as co-managers. The investment approach remains the same.

When a fund manager leaves to join a rival firm or retires, it’s important to see evidence of good succession planning so that the handover is smooth.

While Abbott has been working alongside Meadon for the past six years, the news of Meadon’s departure felt abrupt as it was a short notice period, with Meadon’s departure announced on 24 June 2024 and his exit taking place in August. Another way of doing it would have been to install the two new co-managers alongside Abbott before Meadon’s departure.

Due to Meadon’s long tenure and the succession planning not being as smooth as it could have been, I’ve decided to remove JPMorgan Claverhouse from the £10,000 income challenge for 2025.

In its place, I’ve chosen Dunedin Income Growth Ord DIG

Managed by Rebecca Maclean and Ben Ritchie. It’s a concentrated portfolio of best ideas, holding around 36 stocks, with a focus on both dividend growth and capital growth. It has a sustainable investment approach and can hold up to 25% in overseas stocks.

Dunedin Income Growth has either held or grown its dividend for the past 44 years. It would have been classed by the Association of Investment Companies (AIC) as a “dividend hero” (defined as 20 years or more of consecutive dividend increases) if it had not held its dividends at the same level in 2010 and 2011. It is currently a “next-generation” dividend hero, with 13 years of consecutive increases.

There were a couple of other investment trusts I considered, including Murray Income Trust Ord MUT

and Law Debenture Corporation Ord LWDB, but what swung it for Dunedin Income Growth was the overseas exposure and sustainability focus. Both these elements bring something different to the £10,000 portfolio.

I also considered adding TR Property Ord TRY

To replace the property void created by the delisting of Balanced Commercial Property. However, I’m cautious on the outlook for the asset class due to the prospect of economic growth remaining sluggish and inflation potentially surprising on the upside. This could result in fewer interest rate cuts than expected this year, with the Bank of England indicating last month that four cuts were on the cards for 2025. I would sooner wait to see if those interest rate cuts materialise, and revisit property exposure next year.

Please note: following the publication of this article (on 4 February 2025) there was an announcement about a proposed merger betweenJPMorgan Global Growth & Income and Henderson International on 7 February. If given the green light by shareholders, Henderson International Income’s assets will be rolled into JPMorgan Global Growth & Income. The current fund managers and investment objective of JPMorgan Global Growth & Income will remain the same. If approved, the merger is expected to take effect by July 2025.

Portfolio weightings

The 2025 portfolio requires £190,000 for the £10,000 income challenge (a portfolio yield of 5.26%). All yield figures were sourced in late January, but bear in mind that yield figures are not static.

UK equity exposure comprises 45% of the portfolio. City of London has the highest weighting at 15%. Its longstanding fund manager, Job Curtis, has been at the helm since 1991. Curtis manages the portfolio in a conservative fashion, focusing on companies producing plenty of excess cash to pay dividends. Curtis mainly sticks to Britain’s biggest firms that are listed in the FTSE 100 index.

Over the long term, returns have been solid, but arguably a bigger attraction is that the trust is a consistent dividend payer, having raised payouts each year since 1966.

The other three trusts are allocated 10% each: Merchants Trust, Dunedin Income & Growth, and Diverse Income.

Merchants Trust aims to deliver an above-average level of income and income growth, as well long-term growth of capital, through investing mainly in higher-yielding large UK companies. It has lagged the averaged UK equity income trust over one and three years but is ahead over five years. Merchants has raised its dividend for 42 consecutive years.

Diverse Income invests across the UK equity market but has a bias towards UK smaller companies. Its fund manager, Gervais Williams, has said that he’s the most bullish he’s been about the prospects for the UK market in 30 years.

Williams explains that he seeks to “identify companies which generate more income growth than most of the market. If the income growth comes through, then that drags the share price up over time. Not every year, but over the longer term. It is the capital appreciation along with the good and growing income which ultimately delivers the return.”

For global/overseas income, 35% is allocated. JPMorgan Global Growth & Income has 20%. It aims to outperform the MSCI All Country World index over the long term. It’s “style neutral”, meaning that it doesn’t favour value or growth, for example. It holds 50 “best idea” stocks, and looks to trim its winners and recycle the money into underperformers it still has conviction in.

Henderson International Income has a 10% weighting. This trust gives the portfolio a different source of income. Its investment approach involves favouring defensive and value stocks, with the US weighting of 34% notably less than global indices holding around 70%.

Of the “Magnificent Seven” technology stocks, it holds only Microsoft Corp MSFT

In its top 10 holdings. Another difference compared to other global income strategies is that it doesn’t invest in the UK. Ben Lofthouse has managed HINT since launch in 2011.

Utilico Emerging Markets has been handed 5%. Its approach is very different from peers as it focuses on investing predominantly in infrastructure and utility companies across the emerging markets. Despite recent challenges, the same structural growth drivers remain across emerging economies, including growing middle-class populations driving consumption.

TwentyFour Income is a 10% weighting. When this bond trust was chosen two years ago, a key attraction was that most of the bonds it held were floating rate, meaning they benefited from interest-rate rises. The team expects interest rates to remain higher for longer. If this plays out, its strategy looks well placed to benefit.

It said: “In the UK, the extra borrowing unveiled in the new Labour government’s first Budget in October is expected to bring a short-term boost in growth that will limit the Bank of England’s capacity to cut rates. In the US, the tax cuts and tariffs proposed by Donald Trump on his way to winning the presidential election in November are widely considered to be inflationary, which has weighed on market expectations for US rate cuts.

“This shift in expectations for the next 12 months or so is naturally a positive for floating-rate assets such as Asset Backed Securities (ABS). Given ABS coupons generally move up and down in line with base rates, higher-for-longer rates would mean higher-for-longer income.”

And finally, Greencoat UK Wind gets a 10% weighting. It aims to provide investors with a yearly dividend that increases in line with RPI inflation. This has been successfully achieved each year since the trust launched in 2013.

The 2024 line-up fell slightly short of the target, with £9,921 of income generated. This was down to less income than expected from Balanced Commercial Property, which was delisted in mid-November after being taken over by US private assets firm Starwood.However, given BCPT’s strong share price performance, up 38.2% in 2024 until its delisting, some of those gains could have been used to make up for the shortfall.

In terms of overall total returns (including reinvested dividends), the portfolio returned 9.4% in 2024.

Before revealing the line-up for the £10,000 income challenge in 2025, let’s look at how last year’s constituents fared.

How the 2024 portfolio fared

It’s been a tough couple of years for the investment trust sector, with the average discount standing at around -15%. The discount reflects the gap between an investment trust’s share price and the value of its underlying investments (the net asset value or NAV). When a trust’s share price is above the NAV, it trades on a premium, resulting in new investors paying more than the underlying assets are worth.

However, with the hypothetical income portfolio it’s pleasing to see only two funds in the red in 2024, Greencoat UK Wind UKW 0.42% and Utilico Emerging Markets Ord UEM2.39%, with respective share price total return losses of -8.6% and -3.1%.

Greencoat UK Wind suffered after investor sentiment towards renewable energy infrastructure soured. This led the discount to increase, from around -13% at the start of 2024 to over -20% at the start of 2025.

Since interest rates started rising in late 2021, the renewable energy infrastructure sector was impacted and experienced less demand from investors. As interest rates rise, so do bond yields. As a result, income seekers have more options and can take less risk, as the safest types of bonds, UK and US government bonds, offer yields of around 4.5% compared to virtually nothing when interest rates were at rock-bottom levels.

The hope is that falling interest rates will act as a catalyst for a change in fortunes for the sector, as well as other investment trust strategies that have been out of favour.

Utilico Emerging Markets’ performance was not helped by its discount moving from around -15% to around -20% (from the start of 2024 to the start of 2025). Investor sentiment towards emerging markets has been knocked by continued geopolitical tensions and the eruption of war in the Middle East.

After Balanced Commercial Property, the second-best performer was

JPMorgan Global Growth & Income Ord JGGI, up 19.8%. Among the trust’s winners in 2024 were its top four holdings among the US technology giants capitalising on advancements in artificial intelligence (AI); Microsoft Corp MSFTAmazon.com Inc AMZN, NVIDIA Corp NVDA0. and Facebook-owner Meta Platforms Inc Class A META.

Diverse Income Trust Ord DIVI

Came second in terms of performance, up 15.9%. Gervais Williams, its fund manager, said the return was driven by smaller company shares starting to stage a recovery after a couple of tough years as interest rates rose. He picked out Galliford Try Holdings GFRD and Yu Group YU. as two stocks that stood out in performance terms.

In third place was TwentyFour Income Ord TFIF

up 12.9%. This specialist bond fund aims to generate attractive risk-adjusted returns principally through income distributions. This objective was certainly achieved in 2024. It invests in UK and European Asset-Backed Securities that have high yields and are floating rate (meaning they benefit from interest rises). Therefore, the higher interest rate environment has benefited this fund.

Elsewhere, City of London Ord CTY

Delivered 10.6%, followed by UK equity income peers

JPMorgan Claverhouse Ord JCH0 and Merchants Trust Ord MRCH, with gains of 8.3% and 3.9%.

Finally, global equity income trust Henderson International Income Ord HINT

Investing £3.33 into an ISA every day from 22 could result in a £60,000 passive income Story by Dr. James Fox

I already had a Stocks and Shares ISA when I started work at 22, and it was topped up by inheritance and sporadic gifts. However, it wasn’t until much later that I started making regular contributions to my ISA.

The rationale

Investing £3.33 per day is the equivalent of investing £100 per month. That would have been about 5% of my first paycheque. It might not sound like a lot, especially as it would now take me more than three months to afford one Tesla share, but it adds up over time. Plus, investors can use fraction shares to gain access to more expensive stocks.

The secret ingredient is compounding. This is what happens when investors keep their money invested over the long run. It’s like a snowball that, as it gets bigger, can pick up even more snow.

As we can see from the below graph, £100 really starts to compound after 15 years — this example assumes a growth rate of 10% annually. Towards the end of the 46-year period, £100 of monthly contributions should seem very affordable, while the portfolio will be growing at an impressive rate.

Why 46 years? Well, that’s the number of years between me starting work at 22 and my predicted retirement age at 68.

Source: thecalculatorsite.com

Getting there

So, we’ve got the formula. But how can we actually turn £3.33 a day into a small fortune? Well, many novice investors will invest in index-tracking funds. This is a wise move that provides diversification and relatively low risk.

Buffett’s value investing approach, focusing on undervalued companies with strong fundamentals, has proven successful over decades. However, investors should consider risks such as Berkshire Hathaway’s large size potentially limiting future growth opportunities, the challenge of finding attractively priced acquisitions in the current market, and the eventual succession of leadership as Buffett ages.

Despite these concerns, Berkshire Hathaway’s strong balance sheet, cash-generating businesses, and proven investment philosophy make it an attractive option for long-term investors seeking stability and growth potential. Over 10 years, the average return is 12.3%. This is one I’m adding to my daughter’s pension.

The passive income part

In the above example, £100 a month would grow into almost £1.2m over 46 years. Now, with all that money invested in stocks, funds, and bonds with an average yield of 5%, an investor would receive around £60,000 a year or £5,000 monthly.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

The post Investing £3.33 into an ISA every day from 22 could result in a £60,000 passive income appeared first on The Motley Fool UK.

9% dividend yield! Could buying this FTSE 250 stock earn me massive passive income?

Story by Stephen Wright

9% dividend yield! Could buying this FTSE 250 stock earn me massive passive income?

With the Bank of England cutting rates, savers are likely to get weaker returns on their cash than they did before. But there’s a FTSE 250 stock that I think looks interesting right now.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

Reliable income

Assura owns 625 properties, including GP surgeries, primary care hubs, and outpatient clinics. Over 99% of the portfolio is currently occupied and the average lease has over 10 years remaining.

With the vast majority of its rent coming from either the NHS or HSE, the threat of a rent default is minimal. And the company stands to benefit from a general trend towards people living longer.

Debt can often be an issue for REITs, but Assura is in a reasonable position. Its average cost of debt is around 3% – which isn’t bad at all with interest rates currently at 4.25%.

In other words, Assura looks like it’s in decent shape. It operates in an industry that should be fairly resilient, it has tenants that are unlikely to default, and its balance sheet doesn’t look like a concern.

A 9% dividend yield can often be a sign to investors there’s something to be concerned about. It isn’t immediately obvious what that might be in this case – but a closer look is more revealing.

Share count

With any company, investors need to keep an eye on the number of shares outstanding over time. In particular, they need to pay attention to whether this is going up or down.

Assura’s share count has been rising quite considerably over the last few years. Since 2019, the number of shares outstanding has grown by around 4.5% per year.

That means investors have had to increase their investment by 4.5% each year in order to maintain their ownership in the overall firm. And that really cuts into the return from the dividend.

If this continues, investors aren’t going to be in a position to simply collect a 9% passive income return. They’re going to reinvest around half of it to stop their stake in the business reducing.

This is actually a symptom of a wider risk with Assura. Its dividend policy means it often has to raise capital through debt or equity, so there’s a real risk of the share count continuing to rise.

A huge passive income opportunity?

A stock with a 9% dividend yield often comes with a catch. And I think this is the case with Assura – while the firm distributes a lot of cash, a good amount has to be reinvested to prevent dilution.

That’s not necessarily a devastating problem. But it is something for investors to be realistic about when thinking about passive income opportunities.

The post 9% dividend yield ! Could buying this FTSE 250 stock earn me massive passive income ? appeared first on The Motley Fool UK.

£££££££££££££££

The yield you earn will be the yield based on your buying price, hopefully gently rising over time, unless they cut the dividend.