Dividends can be more reliable than share prices as they’re driven by the companies performance itself and not by the whim of investors.

As part of a total return / reinvestment strategy, this income could be reinvested into income assets or back into the equity market depending on the relative valuations.

The emotional benefits of dividend re-investment. In fact, with this investment strategy you can actually welcome falling share prices.

There seems to be some perverse human characteristic that likes to make easy things difficult. WB

Disclosure – Non-Independent Marketing Communication

This is a non-independent marketing communication commissioned by Greencoat UK Wind. The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

UKW’s NAV total return, which had been previously announced, was -8.5% for the year to 151.2p per share, with the most significant movements from downward power price forecasts, largely seen in the first half, and a revised expectation on long term wind speeds, announced with the Q4 NAV on 29/01/2025. The final results provided more colour on this, which has seen a number of recent years wind speeds incorporated into the data, serving to lower expected long term electricity generation by 2.4%.

UKW maintained its portfolio valuation discount rate at higher levels, with the forecast return to investors being a 10% return on NAV (net of all costs).

Over 2024, electricity generation was 5,484GWh, 13% below budget owing to low wind and lower availability, with a notable export cable failure at Hornsea 1 in the first half of the year. This represents c. 2% of the UK’s electricity demand, and is enough to power 2m homes, avoiding 2.2m tonnes of CO2.

Underlying dividend cover for 2024 was 1.3x on a normalised basis. The board is targeting a dividend of 10.35p per share with respect to 2025, a rise in line with December’s RPI of 3.5%. This is a twelfth consecutive increase by RPI or better, making the UKW one of very few FTSE 250 constituents to increase its dividend each year for the past decade.

UKW completed a £725m refinancing of its RCF and near maturing term loans in September 2024 with its existing set of lenders. The Company reduced the size of its RCF to £400m (down from £600m), of which £270m was drawn at 31/12/2024. The next maturing term facility expires in November 2026. The refinancing was well supported by UKW’s existing lender base, demonstrating a strong demand for UKW credit.

During the year, UKW divested partial stakes in two wind farms for £41m, and made a £14.25m highly accretive follow on investment in Kype Muir Extension, taking its stake to 65.5%. During 2024, UKW bought back 59.2m shares, and subsequently announced it had completed its initial £100m buyback programme.

Over the next five years, UKW expects that excess cash generation will exceed £1bn, and that additional capital will be available through further disposals. The Company has initiated a further share buyback programme of £100m. Remaining excess capital will be applied dynamically and allocated between further, or accelerated, share buy backs and repaying debt to reduce gearing.

At the 2024 AGM, the Company held a Continuation Vote, at which 11% of shareholders voted in favour of discontinuation, and therefore the resolution confirmed continuation. Given the shares have traded at a discount greater than 10% on average during 2024, a continuation vote will also be held at the 2025 AGM, which will take place at 4pm on 24/04/2025.

As part of a phased succession process Stephen Lilley will be stepping down after the 2025 AGM. Matt Ridley will be joined by Steve Packwood as investment managers of the business. The other key figures in the Investment Manager’s team dedicated to managing the Company remain unchanged.

Kepler View

2024 has been a tough year for the renewable energy infrastructure sector, and Greencoat UK Wind (UKW)has not been immune from sectoral headwinds. Lower power prices and lower inflation have both been negatives, yet bond yields remaining stubbornly high has meant that there has been no offsetting reduction in discount rates. Operationally, lower wind resource has been compounded by an issue with the Hornsea 1 wind farm (the largest asset, now fixed), and as a result electricity generation has been below budget. Despite this, it is heartening that UKW’s normalised dividend cover is 1.3x, which illustrates the resilience built into UKW’s model. Shareholders have continued to receive their dividends, which at the current share price of 113.75p, yield 9.1%.

Over the year, surplus revenues and proceeds from disposals (achieved at NAV), have enabled the bulk of the £100m share buyback programme to be executed (it was formally completed on 14/02/2025 a fortnight before the annual results were published). The board’s continued confidence in the model is illustrated by their commitment to continue the trajectory of the dividend, which sees the target dividend increase in line with the December RPI figure. This has been achieved every year since listing, except for 2024 which saw the increase significantly more than RPI. A further positive for sentiment is the announcement of the new £100m buyback programme which, according to the results announcement, may be upsized depending on the results of disposals. With gearing near the soft limit of 40% of gross asset value, proceeds from disposals will likely be weighed against reducing borrowings. As highlighted in the results call, the board and manager are focused on doing what is right by shareholders, and see realizing assets and buying shares back at the current discount as a highly accretive. The announcement on 10/12/ 2024 is another example of UKW implementing shareholder friendly initiatives. Management fees from 01/01/2025 run on the lower of market capitalization and NAV. This level of fee reduction is, as yet, unmatched by UKW’s peers. The manager is therefore even more strongly aligned with shareholders in the desire to see the share price improve.

With the levered portfolio prospective NAV total return standing at 10% post fees, we think UKW continues to look attractive on a risk adjusted basis against many other investment opportunities. The discount has moved narrower from the widest point seen last week, and UKW’s share price should benefit from any further disposals achieved. Most importantly, the board and the manager continue to demonstrate their commitment and alignment to take the appropriate actions in the long term interest of shareholders. In the meantime, shareholders stand to receive an attractive covered dividend delivered by UKW’s resilient business model.

Completion of Share Consolidation and Total Voting Rights

Following the announcement on 18 July 2024 that shareholder approval was granted at the Regional REIT Extraordinary General Meeting, the Company is pleased to announce that the Company’s Share Consolidation, representing a Consolidation Ratio of 1 Consolidated Share for every 10 Ordinary Shares, has today become effective.

All stats from before this period fairly meaningless

A Brief History.

The decision to go ‘all in’ on office blocks only after Covid, when lots of workers were working from home, seemed perverse and so it proved.

Further to the Company’s announcement on 27 June 2024, Regional REIT is pleased to announce that shareholder approval of the Capital Raising and Share Consolidation was obtained at today’s Extraordinary General Meeting.

The Company has therefore raised approximately £110.5 million of gross proceeds, in aggregate, by way of a fully underwritten Placing, Overseas Placing and Open Offer of 1,105,149,821 New Ordinary Shares.

The Capital Raising was fully underwritten by Bridgemere Investments Limited (“Bridgemere”), which is part of the Bridgemere group of companies established by Steve Morgan CBE.

Regional REIT Ltd shares fell on Thursday, after the commercial property investor announced a GBP110.5 million fundraising plan.

It will raise the funds through a placing, overseas placing and open offer of 1.11 billion shares at 10p each.

Shares in Regional REIT were down 30% to 15.27 pence each in London on Thursday morning.

The overseas placing concerns existing shareholders in “certain restricted jurisdictions” where an open offer cannot be made.

In addition, it announced a 1 for 10 share consolidation.

The fundraise will enable it to repay a GBP50 million retail bond.

It added that GBP26.3 million will go towards trimming debt and remaining GBP28.4 million will provide it with “provide additional flexibility to fund selective capital expenditure on assets”.

Chair Kevin McGrath said: “The capital raising, supported by Bridgemere, will enable the company to strengthen significantly Regional REIT’s financial position, reducing indebtedness and provide the company with greater financial flexibility and liquidity headroom.”

Following shareholder approval at the extraordinary general meeting held on the 18 July 2024, the Company successfully raised £110.5m of gross proceeds in aggregate, by way of a fully underwritten Placing, Overseas Placing and Open Offer of 1,105,149,821 New Ordinary Shares. The Capital Raise was fully underwritten by Bridgemere Investments Limited whom we now welcome as a significant new Shareholder with a holding of 18.7%.

Forward Looking

Steve Morgan CBE is a prominent English businessman, investor, and philanthropist. He is best known as the founder of Redrow plc, one of the UK’s leading housebuilders. Born in Liverpool in 1952, Morgan had a humble upbringing and entered the business world at the age of 21. Over the years, he transformed Redrow into a highly successful company, which became a FTSE 250 firm.

Morgan has also been recognized for his contributions to the construction industry and philanthropy, receiving an OBE in 1992 and a CBE in 2016. He continues to lead Bridgemere, a group of companies involved in housebuilding, property development and leisure.

Regional REIT Ltd – commercial property investor – In six months to June 30 reports pretax loss of GBP27.1 million, widened from GBP12.1 million a year prior. Rental and property income falls slightly to GBP44.2 million from GBP44.4 million. Property costs rise to GBP20.4 million from GBP18.4 million. Administration and another costs narrow however to GBP4.7 million from GBP5.3 million. Notes loss from change in fair value of investment properties is GBP37.9 million compared to loss of GBP29.5 million. Declares interim dividend of 2.20 pence, cut from 2.85 pence a year ago. Blames “persistently high interest rates and poor investor sentiment” for the disappointing half. Is optimistic, however, as the “regional office market has begun to show early signs of reaching an inflection point”. Concurrently, Shore Capital Markets lifts Regional REIT to a ‘hold’ rating from ‘sell’.

(“SEEIT” or the “Company”) Interim Dividend Declaration

SDCL Energy Efficiency Income Trust plc is pleased to announce the third quarterly interim dividend in respect of the year ending 31 March 2025 of 1.58 pence per Ordinary Share, covered by net operational cash received from investments.

The shares will go ex-dividend on 13 March 2025 and the dividend will be paid on 31 March 2025 to shareholders on the register as at the close of business on 14 March 2025.

You’ve no doubt heard pundit after pundit say that you need at least a million dollars to retire well.

Heck, we’ve all heard it so often, I bet it’s the first number most people think of when someone says “retirement savings”!

Let me explain why this endlessly repeated fallacy is dead wrong. You’ll actually need a lot less than that.

I’m talking about just $600,000. And in some parts of the country you could easily do it on less: a fully paid-for retirement for just $500,000.

Got more? Great. I’ll show you how you can retire filthy rich on your current stake.

I know that sounds ridiculous in these inflationary times, but stick with me for a few moments and I’ll walk you straight through it.

The key is my “8% Monthly Payer Portfolio” lets you live on dividends alone—without selling a single stock to generate extra cash.

And you’ll get paid the same big dividends every month of the year – so that your income and expenses will once again be lined up!

This approach is a must if you want to quickly and safely grow your wealth, and safeguard your nest egg through the next market correction, too!

This isn’t just a dividend play, either: this proven strategy also positions you to benefit from 10%+ yearly price upside potential, in addition to your monthly dividends.

That’s the Power of Monthly Dividends

We’ll talk more about that price upside shortly. First, let’s set up a smooth income stream that rolls in every month, not every quarter like the dividends you get from most blue-chip stocks.

You probably know that it’s a pain to deal with payouts that roll in quarterly when our bills roll in monthly.

But convenience is far from the only benefit you get with monthly dividends. They also give you your cash faster—so you can reinvest it faster if you don’t need income from your portfolio right away.

More on that a little further on. First I want to show you…

How Not to Build a Solid Monthly Income Stream

When it comes to dividend investing, many “first-level” investors take themselves out of the game right off the hop. That’s because they head straight to the list of Dividend Aristocrats—the S&P 500 companies that have hiked their payouts for 25 years or more.

That kind of dividend growth is impressive. But here’s the problem: these folks are forgetting that companies don’t need a high dividend yield to join this club—and without a high, safe payout, you can forget about generating a livable income stream on any reasonably sized nest egg.

Worse, you could be forced to sell stocks in retirement—maybe even into the kind of plunges we saw in March 2020 or throughout 2022—just to make ends meet.

That’s a nightmare for any retiree, and leaning too hard on the so-called Aristocrats can easily make it a reality: the ProShares S&P 500 Dividend Aristocrats ETF (NOBL), which holds all 66 Aristocrats, still yields just 2% as I write this.

Solid Monthly Payers Are Rare Birds …

You can certainly build your own monthly income portfolio, and the advantage of doing so is obvious: you can target companies that pay more than your average Aristocrat’s paltry payout.

Trouble is, only a handful of regular stocks pay in any frequency other than quarterly, so we’ll have to patch together different payout schedules to make it happen.

To do that, let’s cherry-pick a combo of well-known payers and payout schedules that line up. Here’s an “instant” 6-stock monthly dividend portfolio that fits the bill:

Procter & Gamble (PG) and AbbVie (ABBV) with dividend payments in February, May, August and November.

Target (TGT) and Chevron (CVX), with payments in March, June, September and December.

Sysco (SYY) and Wal-Mart Stores (WMT), with payments in January, April, July and October.

Here’s what $600,000 evenly split across these six stocks would net you in dividend payouts over the first six months of the calendar year, based on current yields and rates:

You can see the consistency starting to show up here, with payouts coming your way every single month, but they still vary widely—sometimes by $875 a month!

It’s pretty tough to manage your payments, savings and other needs on a lumpy cash flow like that.

And the bigger problem is that we’re pulling in $16,700 in yearly income on a $600,000 nest egg. That’s not nearly enough for us to reach our ultimate goal of retiring on dividends alone, without having to sell a single stock in retirement.

We need to do better.

Which brings me to…

Your Best Move Now: 8%+ Dividends AND Monthly Payouts

This is where my “8% Monthly Payer Portfolio” comes in. With just $600,000 invested, it’ll hand you a rock-solid $48,000-a-year income stream. That could be enough to see many folks into retirement.

The best part is you won’t have to go back to “lumpy” quarterly payouts to do it!

Of all the income machines in this unique portfolio, nearly half pay dividends monthly, so you can look forward to the steady drip of income, month in and month out from these plays.

$$$$$$$$$$$$$$$$

Read more over at

My name is Brett Owens and I’m an unabashed dividend investor. Ever since my days at Cornell University and all through my years as a startup founder in Silicon Valley, I’ve hunted down safe, stable, meaningful yields.

For the last 10 years, I’ve been investing my startup profits and finding 7%, 8%, even 10%+ dividends with plenty of double-digit gains along the way. In recent years, I started writing about the methods I use to generate these high levels of income.

Today I serve as chief investment strategist for Contrarian Income Report – a publication that uncovers secure, high-yielding investments for thousands of investors. Since inception, my subscribers have enjoyed dividends more than 4 times the S&P 500 average, plus healthy annualized gains!

A 4% income target gives investors a wide range of asset classes and funds to choose from, according to Hawksmoor’s CIO.

By Emma Wallis,

For an investor planning to live off their savings, the first question is how much they can safely withdraw each year.

Financial advisers sometimes use a ballpark figure of 4%, which is known as the financial independence (FI) number. It stems from a study by academics at Trinity University, who calculated an individual could withdraw 4% of their savings annually over 30 years without running out of money – based on returns from equities and bonds between 1925 and 1975.

There are two ways to do this. Either by investing in assets that pay an income or by drawing down the pot. The latter makes portfolios vulnerable to sequencing risk, however. If a large part of the portfolio is invested in equities and a severe market downturn occurs at the beginning of the journey when the portfolio is largest, an investor’s money will run out much sooner.

Today, achieving a 4% income from dividends, bond payouts and cash is achievable. As such, Richard Philbin, chief investment officer (investment solutions) at Hawksmoor Investment Management, created a portfolio that should provide an income while also producing some capital returns so that investors can dip into reserves if required.

He suggested combining investments that pay a high yield today with those offering a smaller initial income but greater potential for dividend growth. The caveat, however, is that investors would need to hold onto those assets for a long time to reap the rewards of dividend growth.

He suggested putting 50-60% in equities, 30-45% in fixed income, 5-15% in infrastructure and zero to 10% in other assets, such as alternative investments and multi-asset funds.

“That would easily get you a 3.5% to 4% yield and it would give you a very diverse yield as well. It allows you to look at different markets so you can diversify your portfolio and, over time, it could give you both capital growth and income growth,” he explained.

Investors could tweak the above asset allocation, for instance by increasing their fixed income or infrastructure exposure to boost the yield.

Equity income funds that Philbin rates include Redwheel UK Equity Income, Man Income, M&G Global Dividend, Zennor Japan Equity Income and Pacific North of South EM Equity Income Opportunities.

There was one firm, however, where he selected two funds: Guinness Global Equity Income and Guinness Asian Equity Income.

Both have a similar approach to portfolio construction, with a flat, concentrated portfolio of 30-35 holdings and a low starting dividend with a focus on dividend growth over time. “Therefore, patience (from an investor’s perspective) is needed,” he said.

“They have proven themselves over the medium-to-longer term and the risk/reward trade-off is impressive. Portfolio volatility relative to portfolio return – compared to the peers – makes the numbers massively impressive. As we are longer-term investors, we like to invest in managers with similar philosophies and Guinness has proven that.”

For investors who want to juice up their income stream, he suggested Schroder Income Maximiser, which aims to deliver a 7% yield by using derivatives to boost the income. This could help offset other funds where the starting yield is lower.

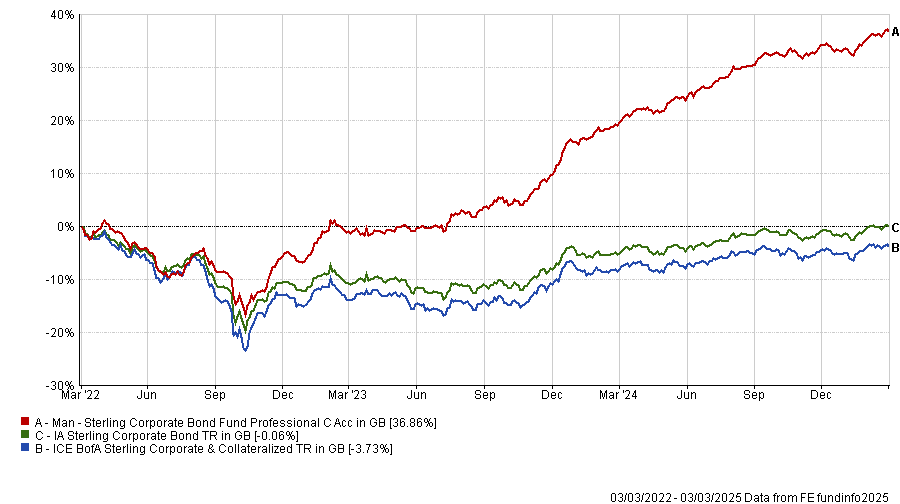

Within the fixed income space, Philbin highlighted Man Sterling Corporate Bond and Premier Miton Strategic Monthly Income Bond. They are complementary because Man Group has more exposure to high-yield bonds whereas Premier Miton focuses on investment-grade credit. “They provide a good spread of risk and have both consistently outperformed their peer groups,” he noted.

Both funds pay out income every month, which savers could spend, reinvest or use to rebalance their portfolio. “If you are retired, it’s nice to know you’ve got some money coming into the bank each month,” he added.

Performance of fund vs benchmark and sector over 3yrs

Source: FE Analytics

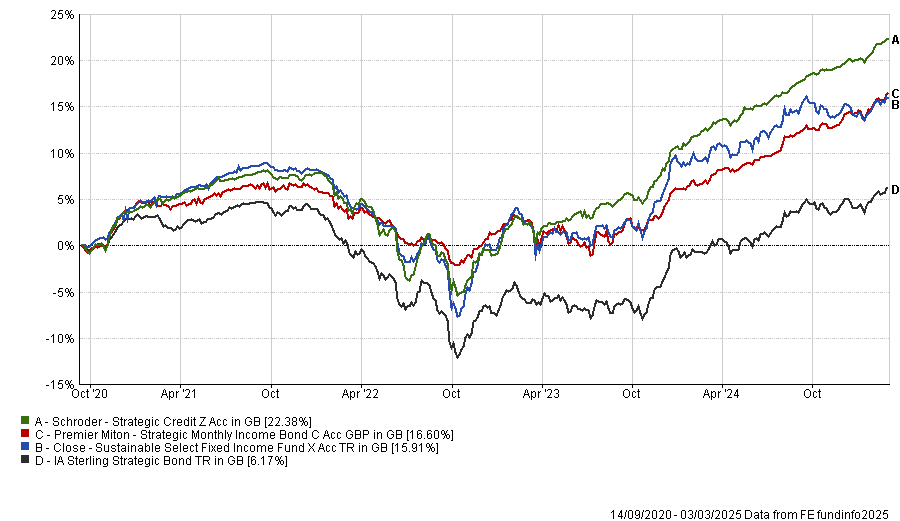

In the strategic bond space, Philbin also likes Schroder Strategic Credit and Close Sustainable Select Fixed Income.

To turbocharge the income, Royal London Short Duration Global High Yield Bond is another option. High-yield bonds can be used to boost a portfolio’s overall yield but they can be volatile so opting for shorter-dated bonds helps to mitigate default risk and interest rate risk, he explained.

Performance of strategic bond funds vs sector over 5yrs

Source: FE Analytics

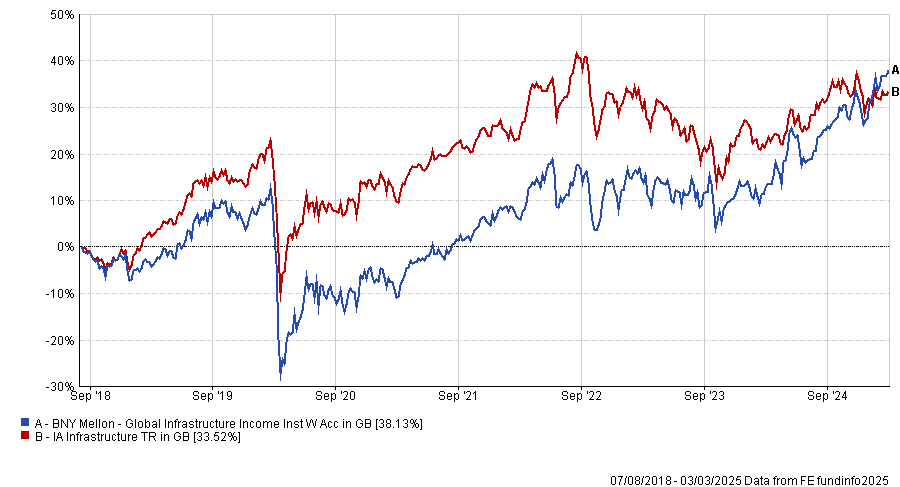

Moving onto infrastructure, Philbin has carved out a sizeable allocation here as assets such as roads and railways have long-term contracts that are government-backed and inflation-linked, possess natural monopolies and can raise prices every year, for example.

He has invested in James Lydotes’ BNY Mellon Global Infrastructure Income fund since launch.“The first couple of years were a little bit scary for us but the past couple of years have more than made up for it and the fund manager’s doing a brilliant job,” he said.

Performance of fund vs sector since inception

Source: FE Analytics

Some investment trusts in the infrastructure space such as Gore Street Energy Storage have double-digit yields and wide discounts, with the potential for capital appreciation.

“Some of these infrastructure products are screaming buys. Yes, there’s a bit of volatility with them, but you’re getting a good starting yield and you are going to get the closing of that discount,” he said.

Real estate investment trusts (REITs) also have the potential to deliver capital growth and income, Philbin added.

Finally, other assets for the remaining 10% allocation might include esoteric investment trusts such as Tufton Assets, which invests in ships. It has a yield close to 10%, pays dividends quarterly and its dividend is covered 1.8x, he said.

Partners Group Private Equity, which used to be known as Princess, has a 6.6% dividend yield and was trading on a 28.8% discount as of 31 December 2024. Its private equity exposure provides an element of diversification and the potential for capital growth, he noted.

Investors could also use multi-asset funds here. Philbin likes the Aegon Diversified Monthly Income fund, which pays a monthly income amounting to 5% per annum.

£££££££££££££££

But as always best to DYOR before you invest your hard earned.

Are these 2 of the best dividend stocks to consider buying in these uncertain times?

Searching for safe-haven dividend stocks to buy ? Here are two from the FTSE 100 and FTSE 250 I think merit a close look right now.

Posted by Royston Wild

Image source: Getty Images

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services. Become a Motley Fool member today to get instant access to our top analyst recommendations, in-depth research, investing resources, and more.

Confidence among stock traders and investors is plummeting. With fears over the macroeconomic and geopolitical landscape growing, so are concerns over the capital gains and dividend income that global stocks might deliver in 2025 and potentially beyond.

I’m not saying that fresh trade tariffs, signs of resurgent inflation, and a weakening US economy are nothing to worry about. However, with some shrewd stock picks, UK share investors can limit the impact these hazards may have on their portfolios.

Here are two I think are worth considering today. I’m expecting them to deliver solid dividends regardless of these external factors.

The PRS REIT

We need to keep the rain off our heads regardless of the economic backdrop. This can make residential property stocks like The PRS REIT (LSE:PRSR) lifeboats for investors in tough times.

Rent collection at this FTSE 250 share has ranged between 98% and 100% in the last three years, even despite the twin problems of higher-than-normal inflation and a struggling domestic economy.

It’s worth noting that private rental growth in the UK is cooling sharply at the moment. Latest Zoopla data showed annual growth of 3% for new lets, down from 7.4% a year ago.

Further cooling is possible, although Britain’s rapidly growing population could put a floor under future declines. PRS REIT’s focus on the family homes sector, where accommodation shortages are especially sharp, might also support rental growth.

I’m certainly confident that the business will remain profitable enough to continue paying a large and growing dividend. Under real estate investment trust (REIT) rules, the company has to pay at least 90% of yearly rental earnings out to shareholders.

For this financial year (to June 2025), PRS REIT’s dividend yield is a market-beating 3.8%.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

BAE Systems

The stable nature of arms spending makes defence stocks classic safe havens during tough times. With Europe proposing hikes to regional defence budgets, now could be an especially good time to consider buying shares like BAE Systems (LSE:BA.)

I like this particular firm because of its considerable financial resources and strong balance sheet, which add extra strength to dividend forecasts. This has underpinned steady payout growth dating back to the early 2010s.

Free cash flow remains considerable, and in 2024 remained stable at around £2.5bn. In my opinion, this gives BAE enough wiggle room to continue paying a growing dividend while also servicing its rising debt pile (net debt increased to £4.9bn last year following the acquisition of Ball Aerospace).

I think its terrific record of dividend growth makes it a great passive income stock to consider, even though recent share price strength has reduced its forward dividend yield to a modest 2.3%. This is some way below its 10-year average of around 4%.

On the downside, BAE Systems may face the prospect of cooling US sales as President Trump seeks to boost government efficiency. But on balance, I think the FTSE 100 stock still merits a close look from savvy dividend investors.

££££££££££££££££££

Note:

The PRS REIT plc

(“the PRS REIT” or “the Company”)

Q2 Dividend Increased

and

Update on the Strategic Review & Formal Sale Process

The PRS REIT, the closed-ended real estate investment trust that invests in high-quality, new build, family homes in the private rented sector, is pleased to declare an increased interim quarterly dividend of 1.1 pence per ordinary share (Q2 24: 1.0 pence) in respect of the second quarter (October-December 2024) of its current financial year ending 30 June 2025.

The dividend increase reflects the Company’s continued strong rental and earnings growth. Accordingly, the dividends declared in respect of the first six months of its current financial year (being 2.1 pence in aggregate) will be covered by EPRA earnings.

One hundred per cent. of the Q2 dividend (1.1 pence per share) will be paid as a Property Income Distribution.

The Q2 dividend will be payable on or around 7 March 2025, to shareholders on the register on 21 February 2025. The ex-dividend date will be 20 February 2025.

Update on the Strategic Review & Formal Sale Process

The Board of The PRS REIT plc is pleased to provide an update on its Formal Sale Process, a constituent of its Strategic Review announced on 23 October 2024.

The Board confirms that, having made available a data room to multiple interested parties, it has now received several non-binding proposals in connection with the acquisition of the Company. The majority of these proposals were pitched within a price range representing a premium to the current share price of 109.2 pence per share and a discount to the latest published net asset value as at 30 June 2024 of 133.2 pence per share. The Board intends to invite a subsection of such parties to enter into a confirmatory due diligence process which is expected to be completed no later than the end of calendar Q1 25.

There can be no certainty that an offer will be made, nor as to the terms on which any offer will be made. Further announcements regarding the Formal Sale Process will be made when appropriate.

Reflecting on the remit of the Strategic Review, the Board continues to explore all the options available to the Company, with a view to maximising value for the Company’s shareholders.

If you had bought around the covid low, you could have taken out your stake and re-invested in another high yielder. Where safety first was the best policy.

Since the NAV peak a constant decline, although they paid out a special dividend of 5.1% of NAV.

The company is winding down so as they sell assets the dividend will fall, current dividend 15% of the reduced share price.

Depending on how long and for how much the assets are sold for the Snowball will print a loss.

BB comment

chucko1

By the paltry volume having gone through so far (most being mine), it seems that no one gives a damn anymore.

They ought to – those repayments are equal to about 1/3 of the shrivelled market cap. When you get that amount back at flat to NAV and the SP is at a 50% discount, there would have been quite a few buyers had it not been for the revulsion many must feel about this sorry episode.

But we are only a part of the way through. It’s like a movie where most of the murders occur in the opening scenes, while the consequences of these murders are explored as the main focal point thereafter.

Still a risky proposition given the concentrated nature of the portfolio, with DEINDE being roughly 80% of the value of the market cap.

As said, at this level, 1p dividends (if adequately earned from income – they just about are) equates to 15% yield. That’s not irrelevant although hardly lavish compensation for the trials one has to bear in owning/[analysing ? – ha ha this thing.

Recent investor discussions regarding Assura Plc (AGR) reflect a cautious sentiment amid concerns about takeover interest and market fundamentals. Key commentators express skepticism about the potential bid from KKR, noting their shift of focus away from the UK healthcare sector. George Stobart articulates this anxiety, stating, “KKR’s withdrawal will lead to a straight line down to 33p.” Conversely, some investors, like bmcollins and husbod, see the potential for upside at lower price points, indicating their willingness to buy if the stock dips below 40p. Comments such as “33p would be perfect for a top-up” highlight a bullish perspective among certain segments of investors who believe in Assura’s long-term value.

Financial highlights discussed include the implications of asset sales and dividends, with references to improving yields and capital growth prospects. Notably, views from Green Street indicate some shareholder support for the board’s rejection of KKR’s offer, which they argue would not adequately reflect Assura’s intrinsic value. Investors seem to be weighing the risks of further asset impairments against the potential for future growth, suggesting a nuanced and divided outlook on the stock’s trajectory: “his anaemic growth of 3% implies a return of c10-12%,” reflects a belief in slow but steady growth. Overall, investor sentiment appears to be a mix of caution regarding market conditions and optimism about the potential for capital appreciation at favourable entry points.

Disclaimer Disclosure – Non-Independent Marketing Communication

This is a non-independent marketing communication commissioned by Sequoia Economic Infrastructure Income. The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research. Kepler.

SEQI offers a yield of almost 9% without the use of gearing…

Overview Sequoia Economic Infrastructure Income (SEQI) offers exposure to infrastructure assets. The trust invests in debt, meaning that its investments are higher up the capital structure than equity and therefore more secure in the case of financial difficulty. These are private, off-market deals, which helps the specialist team managing the portfolio to generate a very high yield for investors, without the use of gearing. SEQI’s historic yield is 8.9% at the time of writing

SEQI is managed by a team of private infrastructure debt specialists, who have brought the asset class out of the banks and into the mainstream via the investment trust structure. Lending to infrastructure gives exposure to economically dynamic and vital trends such as digitalisation—via data centres, broadband networks, and telecom towers—and the greening of the grid—via renewable energy and investments in the network itself. SEQI’s portfolio is highly diversified across industries, with a focus on defensive sectors, as we discuss Portfolio.

In recent months, investment activity has included investments in digitalisation and the broadband network, and the managers report they are continuing to look for ways to invest in ESG-friendly sectors such as renewables. Activity has included a loan to finance the construction of a power plant located next to a Microsoft data centre in Ireland.

NAV performance has been stable, and dividends achieved high, with very few non-performing loans. Good progress has been made recently, and the exposure to NPLs is just 3.7%. Nonetheless, in keeping with the broader investment trust sector, the Discount has remained wide and sits at 19% at the time of writing. The board has embarked on one of the most extensive buyback programmes in the sector to boost shareholder value.

Analyst’s View It is easy to get lost in the details of a private debt portfolio, but at its core, it is a relatively simple model. Companies that can’t or don’t want to access the public debt markets borrow money from specialist teams of lenders who have the knowledge and resources to do all the underwriting work and the research necessary to satisfy themselves about the creditworthiness of the borrower. The lenders earn a higher yield for doing that work (and saving borrowers the costs of raising public debt) and for the illiquidity of the private debt.

This illiquidity means that trading is not a major part of the model like a traditional bond fund. The management team, led by Steve Cook, make loans for three to five years with the aim of holding to maturity. Companies will prefer to raise money this way if they are raising small amounts of debt or if they operate in specialist areas or want bespoke conditions in the deals – Steve and his team, with many years of experience originating this debt in investment banks, are able to assess the risks and do the analysis required to make these deals work .

We think the main benefit from an investor’s point of view, is the high yield, which can be achieved without the use of Gearing and without the volatility in the value of the investments. Most of the trusts which offer yields that compare to SEQI’s, do so by gearing up extensively, bringing costs and volatility. Similarly, short-dated loans, roughly 40-50% floating rate at any one time, are less volatile with regard to valuation than publicly traded debt, which will typically have a higher duration. SEQI pays to have its portfolio revalued each month by an external party, PWC, which should reduce any concerns the value is stale.

As an investment trust, there is, however, potential volatility in the shares, and a wide Discount has opened up. The board is committed to returning substantial amounts of capital via buybacks, which should provide some comfort, but in our view interest rate cuts are likely to be the cause of a sustained shift in the rating.

Bull A high dividend yield from a portfolio with relatively low credit risk Highly diversified exposure to a specialist asset class via an experienced team Significant buyback programme offers additional source of NAV return and demonstrates conviction in portfolio

Bear Unfamiliar asset class for many investors Yield on floating rate portion of portfolio may fall with interest rates As a credit fund, only modest NAV upside expected