How to Invest in CEFs (for 8.6%+ Dividends, 20%+ Upside)

Michael Foster, Investment Strategist

What if I told you I could get you a steady 8.6% dividend right now with ease? And with a big slice of that income rolling your way every month, too?

The key is to invest in an often-overlooked investment called a closed-end fund (CEF). As I write this, there are about 500 CEFs in existence, and they yield around 8%, on average. Some pay more than that, such as the 5 CEFs I reveal in my free investor report, “Indestructible Income: 5 Bargain Funds With Steady 8.6% Dividends.”

With a 8.6% average payout, you’d be banking a nice $25,800 yearly income stream (or about $2,150 a month!) on just a $300K nest egg. Imagine what that could do for your retirement. And those dividends are set to stay high in the years to come, no matter what happens with the Fed or the wider economy.

Probably the best thing about CEFs, including the five CEFs I’ll share with you in my free “Indestructible Income” report, is that they hold many of the blue-chip stocks you know well (and are probably sitting in your portfolio right now). So you don’t even have to change investments to get these 8%+ payouts!

The only difference? Instead of settling for lame S&P 500 dividends, you’ll be banking a cool 8.6%. And you’ll set yourself up for potential price upside, too!

At this point you may be wondering why we don’t hear a lot more about CEFs, given the huge dividends these funds pay out. Truth is, they’re overlooked for the silliest of reasons: investors hear “closed-end fund” and immediately think CEFs are too complicated. Journalists don’t help. They’d rather blather on about the newest gadget from the likes of Apple (AAPL) or the latest tweet (X?) from Elon Musk.

CEFs’ Huge Dividends Demystified

That’s too bad because CEFs really are quite simple: they’re like mutual funds or ETFs in that they pool money from investors, which the fund’s managers then use to buy a basket of stocks, bonds, real estate investment trusts (REITs) or other investments, depending on the CEF’s mandate.

The fund managers then buy and sell over time, handing profits over to us as dividends. CEFs trade on public exchanges and can be bought and sold, just like a stock.

(I give you a high-level breakdown of how CEFs work, including how they can generate big price upside while paying you outsized dividends, in your free “Indestructible Income” report.)

CEFs’ “plain vanilla” setup is great for us, for a couple of reasons.

First, and most important, it means CEFs are heavily regulated. Just like big companies, such as Microsoft (MSFT), Home Depot (HD) or Walmart (WMT), CEFs must account for their operations and file statements with the SEC every quarter. Even more reassuringly, most CEFs are managed by the biggest financial institutions, with the most investment resources and deepest connections at their disposal.

BlackRock is the best example. Not many people know that this monolith, whose $11.5 trillion in assets under management dwarfs the GDP of many countries, is a big CEF issuer.

Second, being publicly traded means CEFs are liquid. If you need cash, just sell your shares during market hours, Monday through Friday from 9:30 a.m. to 4 p.m. Eastern time. And buying CEFs has never been cheaper, with the advent of zero-cost trading.

That’s just the start of the great deal you get with CEFs.

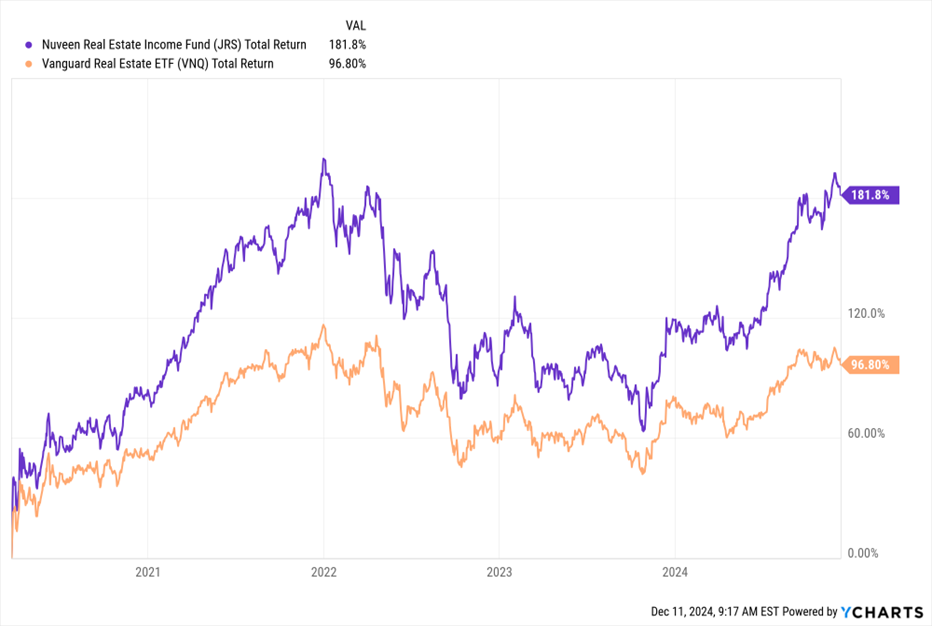

Take a CEF called Nuveen Real Estate Income Fund (JRS). It holds high-yielding real estate investment trusts (REITs), which own a range of properties, from shopping malls to warehouses, and are exempt from corporate taxes so long as they pay out 90% of their profits to us as dividends.

The fund hands out a 7.3% dividend as I write this and holds a lot of familiar names in the REIT space, like warehouse owner Prologis (PLD), data center REIT Equinix (EQIX) and apartment REIT Camden Property Trust (CPT).

Normally, if you bought these stocks on an exchange, you’d have to pay the market price. But with JRS, you’re getting these companies for 4% less than if you bought the shares directly, as of this writing. That may not sound like a lot, but it really is a deal in disguise, as we’ll see in a moment.

This buying opportunity exists even though JRS crushed the benchmark REIT ETF, the Vanguard Real Estate ETF (VNQ), since the depth of the pandemic selloff, something many pundits will tell you an actively managed fund simply isn’t supposed to do.

JRS Clobbers Its Benchmark—and It’s Still Cheap!

How is this possible? Because of a funny quirk with CEFs: they tend to trade for less than what their portfolios are actually worth. And their current portfolio value is laid right out in front of us through a figure called net asset value, or NAV, which is easy to spot on any CEF screener worth its salt. Many CEFs, like the five I spotlight in your free “Indestructible Income” report, will go from trading at a discount to a premium and back again on the regular.

JRS is a good example: in the last decade, it’s traded at premiums as high as 4% and discounts as wide as 20%.

This, in effect, gives us a “buy low, sell high” setup that actually works: we simply buy our CEFs when they trade at unusual discounts and then sell when those discounts flip to premiums! And you get paid well to ride that particular train, with payouts like JRS’s 7.3% yield. This is why investors—particularly billionaire investors—love CEFs!

How to Buy in 3 Simple Steps

The first step to participating in the CEF market is easy: open a brokerage account. Any brokerage that lets you buy and sell shares will allow you to buy and sell CEFs. And now that many trading platforms require a low (or no) minimum to open an account, along with zero brokerage fees, there’s really no barrier to anyone getting into CEFs.

After you’ve opened your account, you’ll need to select the best CEF for you. There are a lot of things to consider in this step, so be sure to take your time and do your research. (I’ll give you some proven, actionable tips for picking the best of these funds—and avoiding the laggards, in “Indestructible Income.”)

You’ll need to consider what asset class you want to buy into (stocks? municipal bonds? real estate?). Then you’ll need to decide what yield you want (is 6% enough? Want 7%? 9%?). You’ll ideally want to choose a fund that is well managed and trades at a big discount. Here too, research is the key.

Finally, all you need to do is log into your brokerage account, enter the ticker for the fund you’ve chosen—like JRS above—and click “Buy.” Then sit back and let the dividends come to you.