VWRP

Current value would be £125,441

Using the 4% rule that would give an income of £5,017.00 versus the Snowball fcast income of £9,120.00.

Investment Trust Dividends

VWRP

Current value would be £125,441

Using the 4% rule that would give an income of £5,017.00 versus the Snowball fcast income of £9,120.00.

| Why It’s (Almost) Time to Buy This 15.6% Yielder by Michael Foster, Investment Strategist There are two things I need to bring to your attention right now, especially if you’re an income investor. One is my outlook for the market, as volatility really hits home. The other is a 15.6%-yielding(!) fund that just changed its name and ticker – and really grabbed contrarians” attention in the process. Let’s start with what’s really going on with this wild market. The NASDAQ is now down more than 10% from its peak price, and stocks on the whole are down for the year. I don’t expect this to last very long. My take: 2025 is likely to be a year of volatility rather than a year of decline. Even so, the volatility we’ve seen so far is relatively new. It was only the middle of last month that stocks started making a clear reversal from their long climb, and the NASDAQ 100 is still up 12.6% annualized over the last three years as I write this, while the S&P 500 is up an annualized 9.6%. Short-Term Dips Against a Long-Term Bull Backdrop Just a quick look at the chart tells you that buying the dip during this period has been a winning strategy. It also tells us that both indices are setting up for another dip-buying opportunity, where stocks will fall to a point where they become irresistible. COVID Has Reduced the Odds We’ll See Another 2008 During volatile markets, however, the psychological pressures are tough, with sharp declines and trillions of dollars of wealth seemingly vanishing in a matter of days. This has always been a problem for markets, but I think it’s less of a problem now, for one reason: COVID-19. This might sound a bit strange, so let me explain. At the start of the pandemic, trillions of dollars disappeared in hours. People were literally prohibited from economic activity, as they were forced to stay in their homes. Oil prices actually went negative. And yet stocks recovered, both because of monetary policy (the Fed swooped in with emergency rate cuts and massive buys of government bonds – so-called “quantitative easing”) and, after that, technological progress (including changes in infrastructure responding to the pandemic, such as new supply chains; new medical technologies; and, of course, AI). In other words, investors have already seen the worst and it’s fresh in their minds, so even if we face a recession over the next year or two, stocks are unlikely to collapse like they did in 2020 or 2008. So, in a sense, this time is different, but not in the way one might think: People are less likely to give in to total fear (or 2020-like despair!) as the business cycle weakens. Which means that while stocks are likely to fall, they’re not likely to collapse. Buying the Dip In such a situation, a smart play is to buy the dip slowly, steadily and strategically. Since fear is unpredictable, we can’t wait for the market to bottom and swoop in to buy everything, but we can start buying when there’s a correction, buy a little more as it worsens, and buy even more when it becomes a full-on bear market. And we can essentially double our “dip-buying discount” by purchasing stocks within a closed-end fund (CEF) trading at an attractive discount to net asset value (NAV, or the value of its underlying portfolio). That’s where the BlackRock Technology and Private Equity Term Trust (BTX), payer of that outsized (to say the least) 15.6% dividend. BTX is the fund’s newest ticker, which BlackRock changed from BIGZ last month. It also changed the name from the old monicker: the BlackRock Innovation and Growth Term Trust. As the name now says, the fund invests part of its portfolio in private equity, which can have bigger returns than public stocks in the long run, while the “term” refers to the fact that the fund will come to maturity in 12 years. (Although there is fine print stating that the fund can convert to a perpetual fund, and I fully expect this to happen, so I don’t pay much attention to the “term” in the name here). The most important thing here (besides the huge dividend, of course) is the discount, which has been narrowing lately: BTX’s Fading Discount Since the melodramatic fear-induced selloff of 2022, BTX’s discount has narrowed as investors realized that a 20%-off sale on the fund’s tech-stock holdings, including Marvell Technology (MRVL) and NVIDIA (NVDA), was a sweet deal. BlackRock, the fund’s management firm, even realized this and started a stock-buyback program in early 2024. There’s just one problem (or at least there was): BTX (under its former incarnation, BIGZ) lagged other BlackRock tech CEFs. But these days the fund is worth your attention (even though it’s a bit too speculative for us to add to our CEF Insider portfolio). From BIGZ to “Bigger X” The changes to this fund run much deeper than a rebrand. BlackRock also made major revisions to its mandate, letting it invest even more in tech stocks. Now, at least 80% of its assets will be in public and private tech companies, instead of the previous focus on small- and mid-cap growth stocks. That mandate didn’t work because small-cap stocks have underperformed other types of stocks for years, as you can see in the benchmark index fund for small caps, in blue below, compared to the NASDAQ (in orange) and the S&P 500 (in purple). Small Caps = Small Profits This wasn’t always the case, and the reason why small caps underperform more now than they used to is another article unto itself. In short, this was one of the reasons why I was wary of BTX when it was BIGZ. Ironically, BIGZ wasn’t as “big-focused” as it should have been. That has changed, along with BTX’s fund managers, with the fund now being run by Tony Kim and Reid Menge. This is great news because Tony and Reid also manage the BlackRock Technology Opportunities Fund (BGSAX), which has run the table on the indices, including the NASDAQ (seen by the performance of its benchmark index fund in orange below), a particularly tough one to beat. Tony and Reid Are Master Fund Managers – and They’re Coming to BTX This kind of outperformance deserves a premium, which BTX will likely get eventually. Until then, the fund remains attractive when it trades at a discount, as it is now. 5 Urgent Monthly Dividend Buys to Grab on This Dip (With Steady 10% Yields) Make no mistake: Times like these, when fear is high and volatility is rampant, are when fortunes are made – especially for income investors like us. Because when stock (and CEF!) prices go down, dividend yields go up. And we’re here to “lock in” those rich payouts! BTX is interesting here, but it’s still pretty speculative – and so best for the short-term, not the long. But not to worry, because I’ve been busy lining up other opportunities for us to lock in big payouts set to last us a lifetime. Like the 10%-yielding monthly dividend CEFs I want to show you today. Each of these 5 stout monthly payers is cheap now. Taken together, they instantly diversify our cash across the best US and international stocks, real estate investment trusts (REITs), corporate bonds and more. I know I don’t have to tell you that dividends that big are a lifesaver in choppy markets like these, since they keep our bills paid, letting us rest easy till things settle down again. Don’t miss your chance to buy these 5 reliable income plays now, while they’re cheap. Click here and I’ll tell you more about these 10%-yielding monthly payers and give you a free Special Report revealing their names and tickers. |

Richard Williams

| Best performing funds in price terms | (%) |

|---|---|

| IWG | 15.8 |

| Schroder REIT | 11.2 |

| Assura Group | 10.3 |

| Urban Logistics REIT | 5.5 |

| Supermarket Income REIT | 4.7 |

| Value & Indexed Property | 4.3 |

| First Property Group | 4.0 |

| PRS REIT | 4.0 |

| Helical | 3.3 |

| Warehouse REIT | 2.5 |

Source: Bloomberg, Marten & Co

| Worst performing funds in price terms | (%) |

|---|---|

| NewRiver REIT | (9.8) |

| Care REIT | (8.4) |

| Harworth Group | (8.0) |

| Workspace Group | (8.0) |

| Grit Real Estate Income Group | (7.1) |

| Custodian Property Income REIT | (6.4) |

| Derwent London | (6.2) |

| Great Portland Estates | (5.2) |

| Regional REIT | (4.9) |

| Ground Rents Income Fund | (4.6) |

Source: Bloomberg, Marten & Co

Macroeconomic uncertainty continues to weigh on the performance of the listed real estate sector, as the potential for a slower than anticipated interest rate cutting cycle grows with inflationary pressures expected from both domestic and international policy. The sector was down 1.7% on average in February, despite a raft of positive results indicating a turn in the valuation outlook (see page 2). Flexible workspace behemoth IWG saw impressive gains during the month and is now up just over 25% in 2025. Schroder REIT returned to positive territory having fallen in January, after posting a quarterly NAV uplift (see page 2). Over 12 months, its share price has risen almost 25%. Assura’s share price increased off the back of news of a bid for the company (see page 3 for details), while PRS REIT’s shares continue to make gains as a sale of the company moves a step closer (see page 3). Urban Logistics REIT’s positive start to 2025 continued after it reported a flurry of letting deals (see page 4). Its share price is up 12.9% in the year to date. Shareholders responded positively to Value & Indexed Property announcing a move to the UK REIT regime that it expects will boost its dividend and liquidity in its shares.

There was an eclectic mix of property companies whose share price returns over February made the list of worst performing, reflecting investors’ broad-brush attitude towards the sector. Retail specialist NewRiver REIT lost almost 10% in value during the month, even after reporting the successful integration of the Capital & Regional portfolio and a strong Christmas trading period. Care home provider Care REIT also saw a sizable fall in its share price despite strong occupational drivers giving it confidence to up its dividend target for 2025. Another company to report a positive trading update but frustratingly end the month in negative territory was Custodian Property Income REIT. Weak economic growth may be weighing on the London office developers. However, they are bullish about the core market given the complete lack of supply and robust demand for best-in-class offices. Regional REIT’s struggles continue after reporting a further write down in the value of its portfolio, with its share price now down 17.7% over 12 months. Having seen its share price bounce following a number of bids for the company, Ground Rents Income Fund fell back 4.6% in February after its suitor stepped away from talks.

| Company | Sector | NAV move (%) | Period | Comments |

|---|---|---|---|---|

| Schroder REIT | Diversified | 2.5 | Quarter to 31 Dec 24 | Value of portfolio rose 1.5% to £473.9m |

| Target Healthcare REIT | Healthcare | 0.9 | Quarter to 31 Dec 24 | Like-for-like valuation increase of 0.6% to £924.7m |

| Custodian Property Income REIT | Diversified | 0.9 | Quarter to 31 Dec 24 | Portfolio value up 0.5% on like-for-like basis to £586.4m |

| Alternative Income REIT | Diversified | 0.8 | Quarter to 31 Dec 24 | Portfolio valuation increase of 0.6% to £106.2m |

| Grit Real Estate Income Group | Rest of world | (12.4) | Half year to 31 Dec 24 | Portfolio value dropped 2.3%. NAV fall mainly due to increased finance costs |

| Unite Group | Student accom. | 5.7 | Full year to 31 Dec 24 | 4.8% like-for-like portfolio valuation increase to £6.0bn |

| Shaftesbury Capital | Retail | 5.2 | Full year to 31 Dec 24 | Portfolio valuation increased by 4.5% on a like-for-like basis to £5.0bn |

| Tritax Big Box REIT | Logistics | 4.7 | Full year to 31 Dec 24 | Portfolio value of £6.55bn, up 3.7% on like-for-like basis |

| Derwent London | Offices | 0.6 | Full year to 31 Dec 24 | Portfolio valuation growth of 0.2% in 2024 to £5.0bn |

| SEGRO | Logistics | 0.0 | Full year to 31 Dec 24 | Portfolio value increased 1.1% to £17.8bn |

| Primary Health Properties | Healthcare | (2.8) | Full year to 31 Dec 24 | Investment portfolio valuation down 1.4% to £2.75bn |

| Hammerson | Retail | (27.2) | Full year to 31 Dec 24 | Valuations stable, NAV fall due to sale of outlet village business at a substantial loss |

Source: Marten & Co

Assura Group rejected a bid for the company from a consortium comprising Universities Superannuation Scheme (USS) and US private equity giant KKR valuing it at £1.562bn. The most recent proposal at 48.0p per share was a 28.2% premium to the share price, but a 2.8% discount to its last reported NAV. USS has backed away from any further potential offers, while KKR said it was considering a further bid. It has until 14 March to announce its intentions.

An activist investment company – Achilles – was launched, raising £54m from investors. Its focus will be on companies in the property, infrastructure, and renewables sector, where it aims to work with boards to realise value for shareholders. It is managed by Harwood Capital Management and led by its chief executive Chris Mills, with Robert Naylor on the board of directors. The pair worked together to achieve an exit for investors at Hipgnosis Songs Fund and more recently is working with PRS REIT on a strategic review.

The sale of PRS REIT moved a step closer, with the board announcing that it has received several non-binding proposals to acquire the company. The majority of these proposals were pitched within a price range representing a premium to the current share price and a discount to the latest published NAV. The board said that it intends to invite a subsection of parties to enter into a due diligence process, which is expected to be completed no later than March 2025.

Home REIT received a number of non-binding offers for the full portfolio from “credible parties” that have been selected to proceed to the next stage of the process. It had put its portfolio of 862 properties up for sale seeking £175m.

A firm offer for Ground Rents Income Fund did not materialise after the board rejected several approaches from Victoria Property and time lapsed on the offer period. GRIO said it was fully committed to implementing the realisation strategy approved by shareholder in November 2024.

Helical and its joint venture partner Transport for London entered into a development financing arrangement with HSBC to provide £125m to fund the construction of 10 King William Street, the over-station development at Bank underground station, in the City of London.

Warehouse REIT agreed to change its investment management agreement, with the basis of its fee calculation switching from NAV to the lower of NAV and market capitalisation, effective from 1 April 2025. This would result in an annual saving of around £2.1m and a boost in earnings of 0.5p per share. There will be a transition period to this new fee arrangement, with the fee in the first financial year only (ending 31 March 2026) being subject to a floor of no lower than 70% of EPRA NAV.

Supermarket Income REIT has acquired nine Carrefour supermarkets in France for €36.7m and sold a Tesco store in the UK for £63.5m. The company now has 26 Carrefour stores in France, representing around 5% of its gross assets.

Primary Health Properties acquired a health & wellbeing clinic with urgent care and diagnostic facilities in Cork, Ireland, for €22m, at a yield of 7.1%. The company’s portfolio in Ireland now represents 9% of the total portfolio.

In a lettings update, Urban Logistics REIT announced that it completed new lettings on five units, totalling 301,000 sq ft of space and £3.0m of annual rent, since 30 September 2024. Portfolio vacancy reduced from 8.1% to 6.2%.

Great Portland Estates made four new lettings for ‘fully managed’ office space at its Piccadilly Estate, in London’s West End. The space was let 13.7% ahead of ERV, securing £1.6m of annual rent at an average of £240 per sq ft, representing a net premium of 98% to traditional leases.

Sirius Real Estate acquired a business park in Reinsberg in Saxony, Germany, for €20.4m and a 6% net initial yield, and the Earl Mill business park in Oldham, for £5.7m and net initial yield of 13.9%.

Schroder European REIT sold its 50% interest in a distressed shopping centre in Seville, Spain. The asset had been marked down in SERE’s book at nil value and the sale reflects this, with the outstanding debt transferring to the purchaser. This strengthens the company’s balance sheet by reducing its net loan-to-value (LTV) ratio from 25% to 21%.

Life Science REIT let 17,200 sq ft at Building 1020 at its Cambourne Park Science & Technology Campus in Cambridge, to 42 Technology Limited, a product design and innovation consultancy. The company signed a 10-year lease, and is paying a rent of £25.50 per sq ft, ahead of the June 2024 ERV.

Henry Boot secured outline planning permission on appeal for 112 homes on a freehold site in Yalding, Maidstone, Kent, after a lengthy planning battle with the local council.

If you are searching for the next takeover target, the risk is lower if you have a higher yield to keep you warm as you wait to be proved right or wrong.

Note: the yields in the table are the yields available last week before this week’s bids.

After Covid struck five years ago, several UK real-estate investment trusts (Reits) suspended or slashed their dividends.

The two big diversified Reits sum up the highs and lows. Land Securities paid out 45.55p per share in 2018/19, falling to 23.2p in 2019-2020. It should pay 40.5p this year. British Land fell from 31.47p to 15.04p; it’s now back to 23p.

Yet share prices are mostly back to where they were in 2020 or even lower. This isn’t just true for the office sector, where one can understand why many investors remain cautious. It applies almost across the board, and the reasons why are clear.

For a double whammy, higher yields elsewhere make the Reits’ own payouts look less compelling. Pre-Covid, Land Securities yielded about 4.5%, now it yields 7.5%. Over the same period, the 10-year gilt has gone from about 0.75% to 4.75%.

Still, look at recent updates and you wonder if investors are too bearish. Shaftesbury, which owns large swathes of London’s West End, reported a 7% net asset value total return for 2024. The shares are down 8% over 12 months. London office specialist Derwent reported stable values and solid leasing trends. It’s off 13% over the year. Logistics firms such as Segro, Tritax Big Box and LondonMetric – which were market darlings until early 2022 – reported okay results, yet the shares remain in the red. And so on. Tailwinds may be picking up, but they’ve yet to be noticed.

Of course, they may be wrong – real estate is cyclical and in every cycle, experienced investors get big calls wrong. Indeed, the news that Land Securities now plans to sell £2 billion of offices to invest in residential property is hard to understand – selling cash-generating assets near a likely market-bottom to fund ambitious new developments for a completely different type of tenant under a government that is very keen to intervene in the housing sector feels like a bold move, and not necessarily what shareholders want. Still, at these levels and with news improving, the iShares UK PropertyETF (LSE: IUKP) sector tracker looks like a promising contrarian play.

((Image credit: London Stock Exchange))

This article was first published in MoneyWeek’s magazine.

How US stock market falls could affect your pension – and what to do about it

Story by Callum-mason

Stock markets in the US fall with worries about the economic impact of President Donald Trump’s tariffs thought to be behind the dip.

The S&P 500, a stock market index tracking the stock performance of 500 of the largest companies listed on stock exchanges in the United States, was down over 8 per cent at close on Monday compared to its all-time high in February.

The Nasdaq, which focuses more on technology stocks, also dipped, as did Asian markets at Tuesday opening.

Many people in the UK will have investments exposed to the US, and pensions are no exception to this.

So why are stock markets falling, how could it affect UK retirement savers, and what should they do in reaction to it? The i Paper explains below.

Why are stock markets tumbling?

Investment experts are generally saying that the dip in US stock markets is due in large parts to President Donald Trump’s tariff policies.

The President has imposed and threatened tariffs – tax on imports – on various countries, with many sticking retaliatory tariffs back on the US.

These tariffs can damaging for businesses, as they cause extra costs.

Lindsay James, investment strategist at Quilter, said: “It had been widely expected that Donald Trump’s policies, whilst widely trailed in his election campaign, would in reality be watered down in order to maintain a business-friendly environment conducive to ongoing gains in the stock market.

“However, the reality so far has been quite different, with on again/off again tariffs and no clear lines of negotiation, all perhaps designed to support his broader goal of seeing a manufacturing resurgence in the US.”

Do US stock markets impact UK pensions?

Many people with pensions will find that their cash has some exposure to companies listed on US stock markets, which could be negatively affecting the size of their pension savings at the moment.

“Most people will be in automatic enrolment default funds which should have global exposure – although clearly the US is a big part of the globe,” said Tom Selby, director of public policy at AJ Bell.

He also said that people who had self-invested personal pensions (SIPPs) may have a large allocations of technology stocks in the US.

David Gibb, chartered financial planner at Quilter Cheviot, added: “Many UK pension funds have significant exposure to US equities.

“In recent times, the US market has been the engine of growth for pension funds, largely driven by the performance of the Magnificent Seven tech stocks.”

What should pension savers do?

Exactly how you should react to the stock market fall as a pension saver depends on multiple factors, including your age and your exposure to US stocks.

But experts generally agree the key thing is not to panic.

Helen Morrissey, head of retirement analysis at Hargreaves Lansdown said: We will all experience periods of stock market turbulence during our pension saving journey.

“In recent memory we have seen this with the Russia/Ukraine conflict and the Covid pandemic. Making knee-jerk reactions such as changing investment strategy or cutting back on contributions can crystallise losses and make it harder for your fund to recover.”

Experts say that general guidance going forwards is to make sure that your pension is spread across lots of different markets.

“It is crucial that portfolios are not overly concentrated in a small handful of names. Such concentration can lead to outcomes that cause discomfort, especially during market downturns,” said Gibb.

For those closer to retirement, there may be a different strategy.

Many with their money in default funds will find that their provider automatically moves their cash to reduce the risk, which Gibb said may make the downturn “less severe”.

Morrissey said: “If you are coming up to retirement then you may choose to put off taking an income from your pension until the situation is more settled. It could also prove a further incentive for people to lock into a guaranteed income for life through an annuity.”

££££££££££££££££

Yep, TR plan a gamble with your future.

Current cash for reinvestment £747.00

Current shares xd £1,342.00

Plus SDIP to declare their dividend for March.

Solactive GlobalSuperDividendTMIndex

DESCRIPTION

TheSolactive Global SuperDividendTM Index tracks the price movements in shares of the100international companies with the highest

dividend yield subject to several qualitative dividend outlook checks. The components are weighted equally. Index adjustments are

conducted annually with additional quarterly dividend sustainability checks. The index is a total return index and published in USD.

FACTSHEET-ASOF11-Mar-2025

SolactiveGlobalSuperDividendTMIndex

TOP COMPONENTS AS OF11-Mar-202

Company Ticker Country Currency IndexWeight(%)

KERRYPROPERTIESLTDORD 683HKEquity BM HKD 1.31%

CHONGQINGRURALCOMMERCIAL-H 3618HKEquity CN HKD 1.28%

HYSANDEVELOPMENTCOLTDORD 14HKEquity HK HKD 1.28%

C&DINTERNATIONALINVESTMENTGROUPLTD 1908HKEquity KY HKD 1.27%

ABRDNPLC ABDNLNEquity GB GBp 1.26%

HANGLUNGGROUPLTDORD 10HKEquity HK HKD 1.25%

KENONHOLDINGSLTD KENITEquity SG ILs 1.22%

CITICTELECOMINTERNATIONALHO 1883HKEquity HK HKD 1.22%

DNOASA DNONOEquity NO NOK 1.18%

GROWTHPOINTPROPERTIESLTD GRTSJEquity ZA ZAr 1.15%

PCCWLTDORD 8HKEquity HK HKD 1.15%

SANSIRIPCL SIRITBEquity TH THB 1.14%

GLOBALNETLEASEINC GNLUNEquity US USD 1.13%

HKBNLTD 1310HKEquity KY HKD 1.13%

VTECH(VTECH)HOLDINGSLTDORD 303HKEquity BM HKD 1.12%

FACTSHEET-ASOF11-Mar-2025

Solactive Global SuperDividendTM Index

The Oak Bloke

May 31, 2024

A monthly dividend, almost 1% a month. Does that leave you slightly salivating, reader? You’d have to have dysfunctional salivary glands wouldn’t you?

It is tempting.

But is it safe. Let’s try to assess that.

SDIP is run by a large German index operator called Solactive.

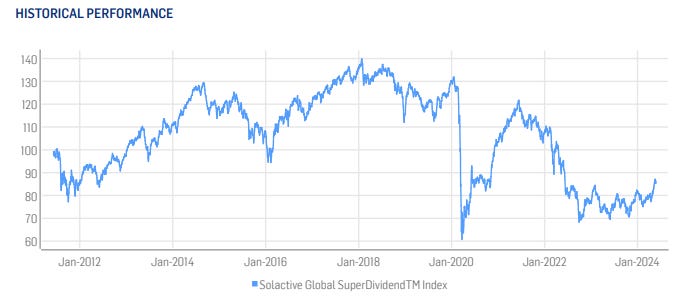

The reason many avoid this ETF is historically capital losses appear to offset the rich dividend income. Over three years, shows SDIP as having a “continuous” 30% fall during which time is would’ve provided around a 33% income. Like a dragon consuming its own tail things are not going to end well….. apparently.

But look at just the past 1 year – the picture improves – capital losses are near zero.

Zooming out gives the best (and fairest?) picture of all. If you go back 13 years (I could only find this view on Solactive’s own web site to when you query your usual tools or your broker’s tools you can’t see this full picture for some reason)

Since inception, your capital AND dividend (total return) losses would actually be 10%

so while there are periods of growth 2020 and 2022 were periods of sharp loss (net of dividends)

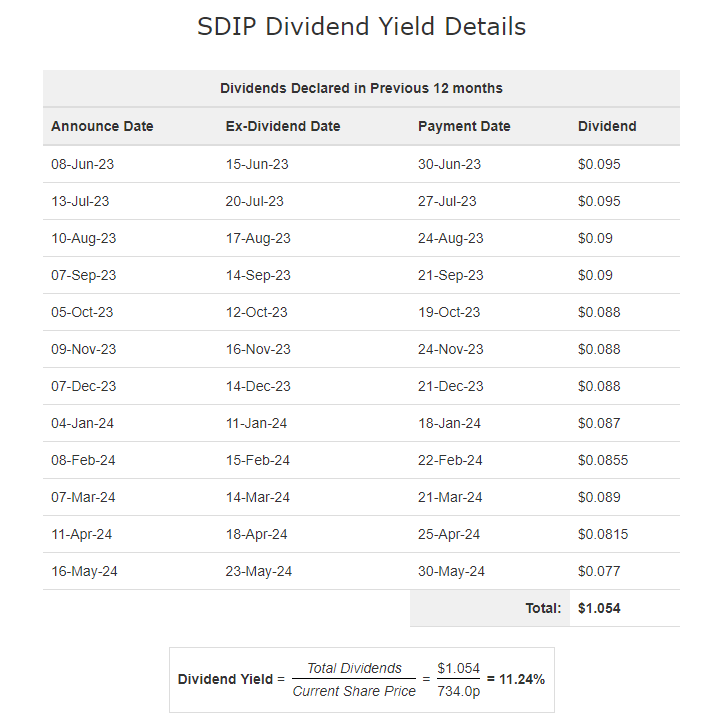

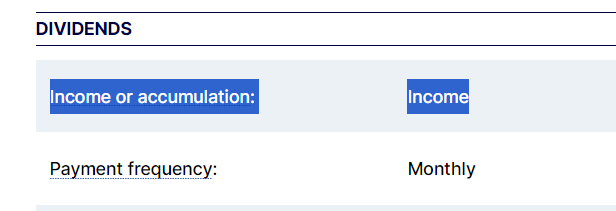

SDIP is listed as an income stock in the UK – not accumulation.

So the question is what causes the capital to drop?

The index started with the Top 100 dividend payers across major markets. They then screen each quarter for any that have dropped below the Top 200 (i.e. 100 worse than the top 100) and replace them. They also screen for dividend cuts or an overall negative outlook concerning the companies’ dividend policy (“Dividend Cut Review Date”). Theoretically if you’ve got a high yield company that is in financial trouble it doesn’t get picked. Certainly all of the samples I took were well established – I share some examples below.

If any changes need to be implemented, the index will be adjusted at the close of the last trading day of the month. Companies may be excluded on quarterly reviews and replaced with the top ranked company from the selection pool that is currently not an index member (i.e. position 101). The company that is added to the index composition at the quarterly review dates will be given the same weight as the member that will be deleted, calculated as of the trading day before the adjustment takes place.

Also SDIP is rebalanced quarterly over a five-day period (“Rebalancing Period”). Beginning on the Adjustment Day, and continuing until the fourth Trading Day following the Adjustment Day. Essentially the winners are sold and the losers are bought each quarter.

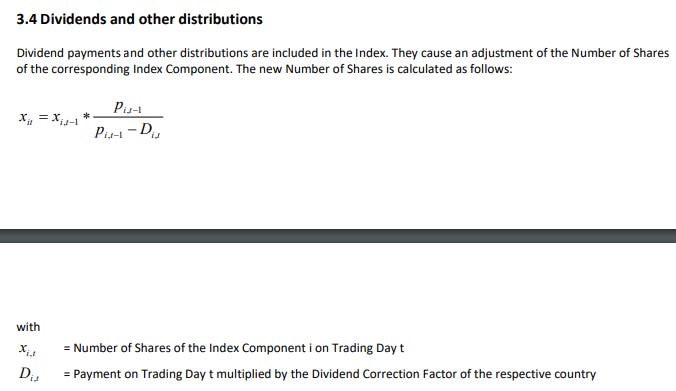

Any Corporate Action event such as acquisition, tender offer, dividends paid etc etc is also considered and a formula is used to rebalance the holding. The formula below means that if I hold 100 units of share X with an index price of £100 (P) then receive a £10 dividend (D) this means I now need to hold 111 units instead. This assumes the £10 is tax free (no dividend correcting factor).

So the largest percentage dividends lead to me holding proportionately more of that share.

If I also have 100 units of Share Y also £100 and that pays 8%. Then 100 X (100/100-8) = 108.7 units. So the 10% share “crowds out” the 8% share over time.

In other words reader SDIP is a cold, calculating index relentlessly pursuing high dividends and capital gains or losses are immaterial to its judgment.

I’m not going to go through all 100 holdings but digging in to some examples here’s what I found.

Land Bank in Eastern China. Share price has halved in the past year and the dividend has been cut. Housing is in all sorts of trouble in China with 25m-30m unsold properties. It paid a 10% dividend but that is now 5.7%. This is an example of a holding that will get removed from the index, at the end of the quarter.

Meanwhile its share price has fallen, so rebalancing would’ve meant buying more each quarter to rebalance it.

Dividends in 2022 were $3bn, and $0.6bn in 2023. An 80% cut. Ouch.

The Red Sea Houthi crisis, the Chinese economic downturn and falling shipping rates have all affected Orient Overseas.

Produced 16.7Mt of coal in 2023 and 581koz of PGMs. The dividend is around 9.5% and while it reduced in 2023, due to PGM basket falling it remains high.

In the SDIP Top 100 I see British names of BATS, VOD, Serica, M&G, DEC among the Top 100. That gives you an idea as to how they arrive at their top 100 list. Big established companies with big dividends, but cyclicals which do well in boom not bust.

£££££££££££££

Note the date: so some of the information may have changed but as always best to DYOR before committing any of your hard earned. GL

2024 Highlights

| · | Share price total return outperformed the FTSE Actuaries All-Share Index with a total return of 15.9% for 2024, compared with 9.5%. |

| · | NAV total return with debt and Independent Professional Services (“IPS”) business at fair value for FY 2024 of 13.6% (13.2% with debt at par). |

| · | A solid performance from IPS, with net revenue increasing by 6.2% and valuation up 5.1% to £194.5 million (excluding net assets). |

£££££££££££££

Belt and Braces.

A dividend hero but sadly the yield of 3.8% too low for the Snowball.

Dividend Highlights

| · | Proposed 2024 dividend increase of 4.7% to 33.5 pence per Ordinary Share (2023: 32.0 pence per Ordinary Share) compared to Group revenue return per share of 33.48 pence. |

| · | Dividend yield of 3.8% (based on our closing share price of 884 pence on 11 March 2025). |

| · | Over the last 10 years, we have increased the dividend by 113.4% in aggregate (7.9% CAGR), reflecting strong IPS cashflow and good Portfolio performance. |

| · | We have a strong reserve position, and the Board is confident in achieving continued growth of dividends over time, building on our record of 46 years of increasing or maintaining dividends to shareholders. |

© 2026 Passive Income Live

Theme by Anders Noren — Up ↑