On track to double your stake but as you can see from the chart above it’s about timing and then time in.

Buying yield would have been 5.75%.

Top ten holdings

Current yield 4.77% Discount to NAV 4.3%

Investment Trust Dividends

On track to double your stake but as you can see from the chart above it’s about timing and then time in.

Buying yield would have been 5.75%.

Top ten holdings

Current yield 4.77% Discount to NAV 4.3%

‘I’m 65 years old with a £100,000 pension pot – how much can I get in retirement?’

Story by Temie Laleye

A £100,000 pension pot could now secure a significantly higher income in retirement, with recent market shifts driving up annuity rates.

Experts have explained how much a 65-year-old could expect to receive annually and why shopping around for the best deal has never been more important.

A 65-year-old with a £100,000 pension can now get up to £7,882 per year.

Retirees can get this guaranteed income for life through a single life level annuity with a five-year guarantee, according to latest data from Hargreaves Lansdown’s annuity search engine. This is up 63 per cent on what was available five years ago.

Couple at laptop© GB News

Helen Morrissey, head of retirement analysis Hargreaves Lansdown said: “Annuity incomes have been a ray of sunshine for retirees in these turbulent times.

“These increases are welcome news for anyone in the market for a guaranteed income in retirement and have contributed to a real revival in a market that was once considered on the edge of extinction.

“2024 was a bumper year for the annuity market and current rates will continue to fuel interest.”

Pension folder© GB News

Using an annuity search engine is crucial for retirees to understand what the market can offer before making their final decision.

This revival in annuity values has driven increased market interest, with Financial Conduct Authority retirement income market data showing sales up 38.7 per cent in 2023/24.

Morrissey has warned that while annuity incomes are currently strong, they may begin to dip if the Bank of England starts cutting interest rates — as widely expected in May.

Pensioners look at statements© GB News

However, she urged savers not to panic. Rates aren’t expected to drop as sharply as they rose, and a return to the ultra-low levels seen in previous years is unlikely.

Morrissey noted that retirees don’t need to annuitise their full pension all at once.

Buying annuities in stages can provide greater flexibility and allow income to rise over time — particularly for those who may qualify for enhanced annuities due to age or health conditions.

She said: “You can secure guaranteed income as your needs change. And if you develop a qualifying condition, you’ll get a further bump in income.”

Fancy a gamble with your retirement ?

This is up 63 per cent on what was available five years ago.

Plus you have to surrender all your hard earned. GL with that.

Story by Ben McPoland

UK supporters with flag© Provided by The Motley Fool

Incredibly, the FTSE 100 just completed 11 days of positive gains. This was the blue-chip index‘s best run since 2019 !

The Footsie tanked in early April when President Trump’s sweeping tariffs announcement threatened to send the global economy into a tailspin. Since then though, there have been rowbacks and pauses from the US administration. This has calmed markets, at least for now.

Specifically for the FTSE 100, it means the index has nearly clawed back all the losses following Trump’s announcement. I certainly didn’t expect 11 days of gains, proving once again how utterly unpredictable markets can be in the short term.

But we’re not out of the woods just yet. The 90-day pause on most ‘reciprocal’ tariffs ends in July. Depending on what happens then (or before), the index could pull back sharply or keep climbing to notch new record highs. It’s a bit of a coin toss.

Moreover, there will already damage done to global growth from all the uncertainty. How much damage we don’t know yet, but the 10% blanket tariff is still in place, as is the extraordinary 145% duty on goods from China.

At the price of 400p, the dividend was 26p a yield of 6.5%.

Latest full year dividend 33.5p a yield on the buying price of 8.25%

A current yield of 3.76% trading at a small premium

You have doubled your capital invested, which could now be withdrawn, leaving a share in your Snowball producing income at a cost of zero, zilch, nothing.

You also have received the dividends which could have been re-invested back into the share until the yield fell and then switched to investing in another high yielding Trust.

Sadly Mr. Market didn’t give you another chance to buy but one to keep in your watch list, if the opportunity arises.

IPS Highlights

| · | The Company’s wholly-owned provider of professional services is a key differentiator to other investment trusts and offers additional portfolio flexibility. |

| · | Accounts for c.19% of 2024 NAV but has funded approximately one-third of dividends paid by the Company in the last 10 years. |

| · | IPS has now delivered seven consecutive years of mid to high single digit underlying growth, with a 5 year underlying PBIT CAGR of 7.3%. |

| · | 2024 valuation of £194.5 million (excluding net assets), up 83.6% since 2019. |

| · | Non cash goodwill impairment of £17.0 million on the 2021 acquisition of CSS. |

Awards

Winner in the Active-Income category for the third year in a row at the 2024 AJ Bell Investment Awards.

Winner of the Best for Long-Term Income award at the QuotedData awards.

Recognised by the AIC as an “ISA Millionaire” performer

Depending on when you bought, you have nearly achieved the holy grail of investing that you have doubled your money.

As most of the profit is in earned dividends, most probably best to use the share as a milk cow and invest the dividends into another higher yielding share. Once you have received all your capital back in the form of dividends you will have a share in your Snowball producing income at zero risk.

Real Estate Credit Investments Limited (RECI) is a closed-ended investment company which originates and invests in real estate debt secured by commercial or residential properties in the United Kingdom and Western Europe.

RECI is externally managed by Cheyne Capital’s real estate business which was formed in 2008 and currently manages $6.5bn via private funds and managed accounts. Its investments span the entire spectrum of real estate risk from senior loans, mezzanine loans, special situations to direct asset development and management.

RECI’s aim is to deliver a stable quarterly dividend with minimal portfolio volatility, across economic and credit cycles, through a levered exposure to real estate credit investments.

Current yield 9.8% Discount to NAV 15%

Thursday 1 May

Bellevue Healthcare Trust PLC ex-dividend date

CQS Natural Resources Growth & Income PLC ex-dividend date

CQS New City High Yield Fund Ltd ex-dividend date

Dunedin Income Growth Investment Trust PLC ex-dividend date

Edinburgh Investment Trust PLC ex-dividend date

Global Opportunities Trust PLC ex-dividend date

Henderson Far East Income Ltd ex-dividend date

Henderson International Income Trust PLC ex-dividend date

M&G Credit Income Investment Trust PLC ex-dividend date

Mobius Investment Trust PLC ex-dividend date

Schroder Oriental Income Fund Ltd ex-dividend date

Sequoia Economic Infrastructure Income Fund Ltd ex-dividend date

Starwood European Real Estate Finance Ltd ex-dividend date

I’ve bought back RECI for the Snowball 7351 shares for 9k, yielding an income of £882.00 p.a.

Passively tracking the index is the best way to invest in the domestic market.

By Patrick Sanders

Reporter, Trustnet

Markets hate uncertainty, but volatility has been a common feature of the investment landscape for the past half a decade, in which markets have been shaken by everything from a global pandemic to the outbreak of war.

This year, uncertainty has continued as markets have had to grapple with US president Donald Trump’s fluctuating and unclear approach to trade threatening a full-blown trade war with China.

As such, in the first part of a new series, Trustnet examines market capitalisation, investment style and the performance of active and passive funds to determine the ‘ultimate way’ to invest in each major market since the start of 2020. Here we begin with the UK.

While past performance is not a guarantee of future returns, if volatility is here to stay, it may be helpful for investors to know what has done well in the past five years of market uncertainty.

Market capitalisation and investment styles

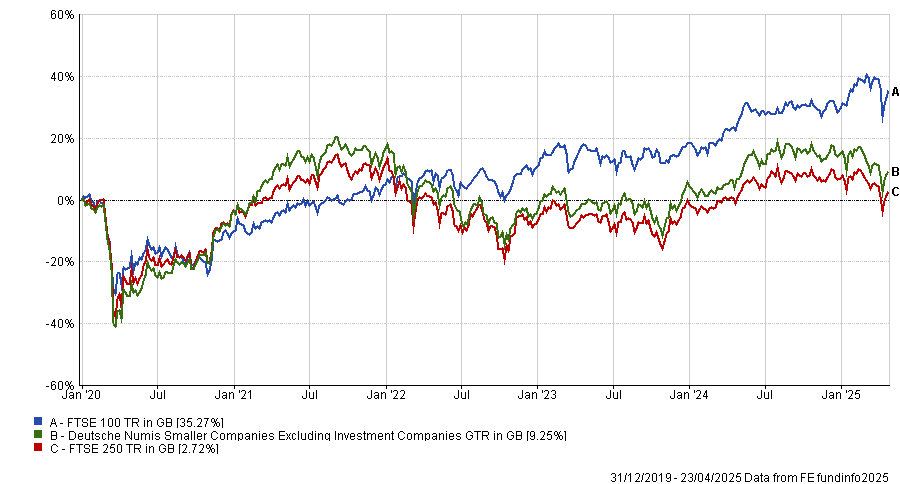

Of the three main UK market indices, the large-cap FTSE 100 is the best performer, up 35.3% since the start of 2020. Investors have sought the relative safety of larger companies in the past few years, as blue-chips tend to be more international and better prepared to deal with market shocks.

The make-up of the UK market, in particular, has been beneficial here. It is made up predominantly of large banks, which were boosted by rising interest rates, and oil majors, which have rocketed as the oil price jumped on the back of Russian sanctions following the country’s invasion of Ukraine.

As investors have taken risk off the table, other areas have struggled. The small-cap Deutsche Numis Smaller Companies index is up by 9%, a difference of 26 percentage points, while the mid-cap FTSE 250 is up by just 2.7% as investors have shunned domestic names.

Performance of indices since 2020

Source: FE Analytics

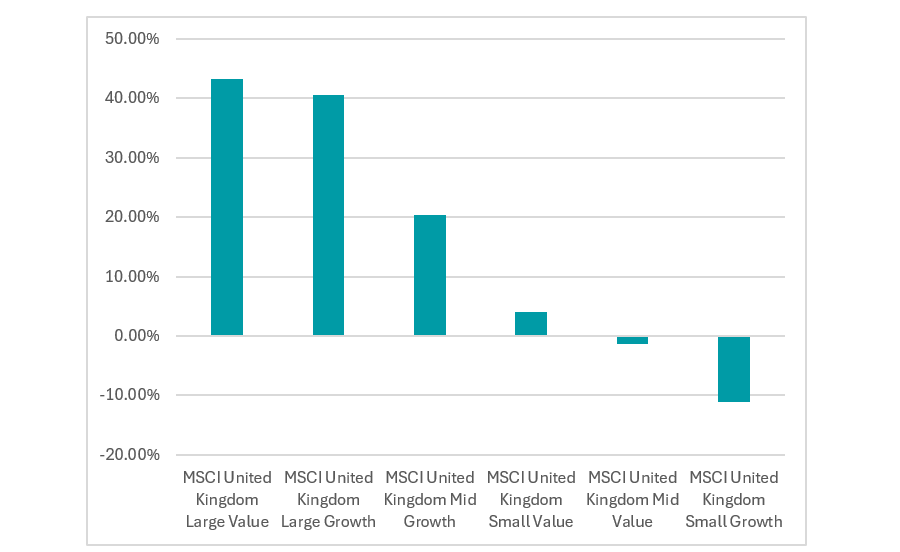

Turning to investment styles, large-caps again triumphed, with MSCI United Kingdom Large Value and MSCI United Kingdom Large Growth topping the chart with a return of 43.3% and 40.5%, respectively, suggesting style was less of a factor than market capitalisation.

However, value was the clear winner across the entire market spectrum, with the style also outperforming in the small-cap space (the MSCI United Kingdom Small Value was up by 4.1%, while the growth index tanked by 11.2%). The only exception was in mid-caps, where this trend reversed.

Performance of indices since 2020

Source: FE Analytics.

Active vs passive

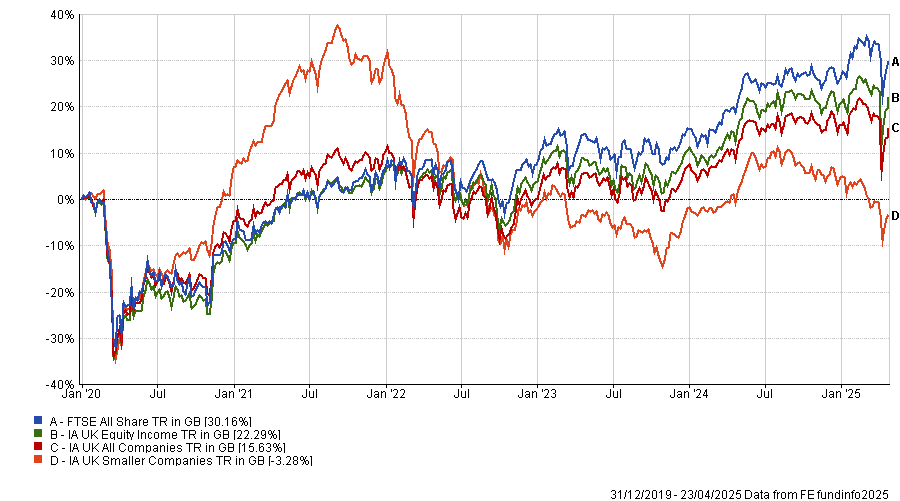

Having established that a large-cap value fund was the best way to invest in the UK over the past five years, how did active funds perform versus their passive counterparts?

Across all three IA UK equity sectors, the average fund failed to beat the most common UK benchmark – the FTSE All Share – which surged 30.2% since the start of 2020. The IA UK Equity Income sector average came closest to this result, up 22.3%, while the IA UK All Companies sector peer group is up by 15.6% and the IA UK Smaller Companies sector lost 3.3%.

Performance of IA Sectors vs the benchmark since 2020

Source: FE Analytics.

This poor performance from active funds reflects the dominance of large stocks in the index, such as pharmaceutical giant AstraZeneca and oil titan Shell. While active managers may hold allocations towards these stocks, they may struggle to be overweight due to their weighting in the index.

Instead, active managers tend to hunt for shares further down the market-cap spectrum, impacting their performance against the market.

In total, 19% of the IA UK All Companies sector has beaten the FTSE All-Share, while 23% of the IA UK Equity Income sector achieved the feat. In the small-cap arena, 22% were ahead of the Deutsche Numis Smaller Companies Excluding Investment Companies index (a more relevant benchmark), while three funds were able to beat the FTSE All Share.

Conclusion: Buy a large-cap tracker

The data indicates the best way to invest in the UK during times of market dislocation is just to buy a large-cap tracker. At least, that is what would have worked over the past five years.

In this regard, investors are spoilt for choice, with many firms now offering a range of passive index trackers which have proven very popular amongst investors. For example,the Vanguard FTSE UK All Share Index UK Unit trust has more than £14bn in assets under management, making it the largest and most popular fund in the IA UK All Companies sector. It tracks the FTSE All Share for an ongoing charges figure (OCF) of 0.06%, making it one of the cheapest funds on the market.

However, this is not to say active management does not have a place. While the average active fund failed to beat the market, some did manage to deliver.

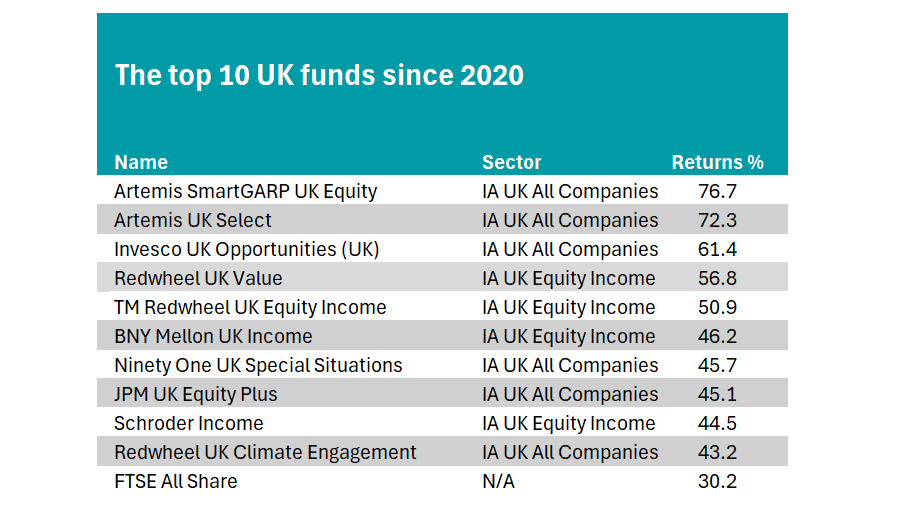

The table below shows the 10 best-performing funds in the UK market since the beginning of 2020, all of which beat the FTSE All Share. Six funds are in the IA UK All Companies sector, while four are in the IA UK Equity Income sector.

Source: FE Analytics

Top of the list is the Artemis SmartGARP UK Equity fund (growth at a reasonable price). Managed by experienced stockpicker Philip Wolstencroft, Shell and GSK are the only two holdings in its top 10 that are also in the top 10 of the FTSE All Share. Otherwise, it is very different to the standard tracker.

It is followed by another strategy from the Artemis team, Ed Legget and Ambrose Faulks’ Artemis UK Select fund. It has significant allocations towards three of the FTSE All Share’s largest constituents – Shell, HSBC and Rolls-Royce.

Income.

Three strategies from the team of Ian Lance and Nick Purves also beat the benchmark – Redwheel UK Value, Redwheel UK Equity Income and Redwheel UK Climate Engagement.

Other funds to qualify include: Invesco UK Opportunities fund, Ninety One UK Special Situations, JPM UK Equity Plus, Schroders Income and BNY Mellon UK Income.

OR

We continue to look back to the future, so the next time Mr. Market gives you the chance you will be prepared.

Or how to Get rich without taking high risks with your hard earned.

Note how the dividend was trimmed after the covid crash but it wasn’t a reason to sell.

Dividend 10.28p. Price shown on chart 127p a yield of 8%.

Note: chart price not including dividends.

You would have achieved the Holy Grail of Investing in that you could take out your stake and re-invest in another higher yielder and have a share in you Snowball providing income at a cost of zero, zilch, nothing.

Most probably the safest dividend in the Investment Trust Universe, dividends are not re-invested into CTY but re-invested into the higher yielding shares in your portfolio.

If you had bought the yield around the covid low, the yield was around 6% which has gently increased to 6.75%.

Chart: Not Including dividends.

The current yield is 4.47% so if you pair traded with a higher yielder a blended yield of 7%. With a ‘safer’ dividend you could accept a lower blended yield.

Still some time before you achieve the holy grail of investing, where you can take out your stake and have a share producing income at zero, zilch, cost.

If you had invested 10k, you would have earned very roughly £2,500 in dividends which would be earning more dividends, for your Snowball, re-invested in a higher yielder.

The current dividend would be around £675.00 p.a.

© 2026 Passive Income Live

Theme by Anders Noren — Up ↑