The Board of Octopus Renewables Infrastructure Trust plc is pleased to declare an interim dividend in respect of the period from 1 January 2025 to 31 March 2025 of 1.54 pence per ordinary share, payable on 30 May 2025 to shareholders on the register at 16 May 2025 (the “Q1 2025 Dividend”). The Q1 2025 declared payment is in line with the Company’s dividend target for the financial year from 1 January 2025 to 31 December 2025 (“FY 2025”) of 6.17 pence per Ordinary Share*. The ex-dividend date will be 15 May 2025.

The Company has a progressive dividend policy and the dividend target for FY 2025 represents an increase of 2.5% over FY 2024’s dividend, in line with the increase to the Consumer Price Index (CPI) for the 12 months to 31 December 2024. This marks the fourth consecutive year the Company has increased its target in line with inflation.

Wall Street Missed This. We Didn’t (We’re Cashing in With 7% Dividends)

Brett Owens, Chief Investment Strategist Updated: May 6, 2025

It’s no secret this economy is slowing—at least in the near term. That’s given us contrarians a (time-limited!) buy window on the “dividend twofer” we’re going to dive into today.

One of the tickers we’ll talk about below pays a sturdy 7% now. The other yields 4.9% and sports a source of upside no one has noticed (except us, of course!).

Both are utility plays, which tend to rise as the economy slows, lowering interest rates as it does. Let’s get into this opportunity, starting with last week’s GDP report, which said, yes, the US economy did shrink to start the year.

Slowdown Adds to Utilities’ Upside

Sure, GDP growth slowed in the first quarter, to the tune of 0.3%. But the underlying numbers were actually more bullish than the headlines suggested.

That’s because the pullback was in large part due to a spike in imports as retailers stocked up ahead of Trump’s tariffs—and imports are calculated as a drag on GDP. That trend is likely to fade. Government spending also dropped in light of DOGE cuts, while consumer spending largely held up.

We’ll take a GDP dip caused by temporary factors like import spikes ahead of tariffs and a likely one-off drop in government spending.

But the truth is, a slowdown (even if a mild one) is likely. More evidence came in last week’s initial jobless claims, which came in at 241,000 for the week ended April 26, above the 225,000 expected.

“Trump Put” on Interest Rates Works in Our Favor

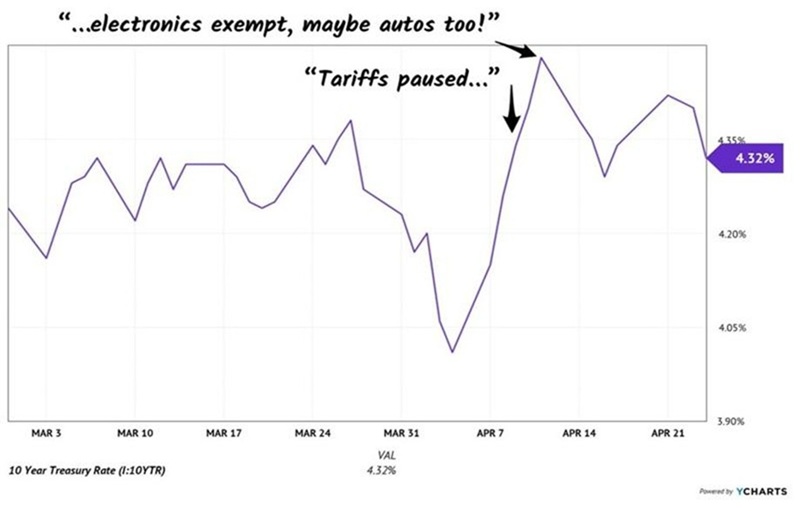

This tariff situation is changing daily (hourly?), with the “Liberation Day” levies on, then off. Then electronics were exempt from China tariffs. And more recently, levies from car parts were waived for vehicles built in the US.

More dovish moves are likely on the trade front. But wherever we land, tariffs will be higher than they were pre-January 20. They’re a key part of Treasury Secretary Scott Bessent’s three-part plan to bring down interest rates:

Tariffs, to slow growth (and with it inflation).

Deregulation, to help offset the tariff drag, and …

Drilling, to bring down energy prices.

But as we’ve written before, Bessent is focused on the 10-year Treasury rate, benchmark for business and consumer loans of all types.

Case in point: When the yield on the 10-year famously spiked in early April, Trump (no doubt hearing Bessent’s pleas) put the bulk of the Liberation Day tariffs on pause.

In other words, we’ve finally found the “Trump Put” for stocks—but it isn’t in the stock market. It’s in the bond market!

That push for lower rates is a rare policy-driven tailwind we’re happy to take advantage of. And as we’ll see below, high-yielding utility stocks are a great way to do so.

The 10-year knows the story on the latest economic numbers, too. Because beyond the GDP report, the personal consumption expenditures (PCE) index, the Fed’s favorite inflation gauge, also came out last week. And it actually dipped from a year ago, to 2.3% from 2.7%.

Ten-year Treasury rates fell in response—as you’d expect from a bond market anticipating an economic slowdown.

A slowdown is not great news, of course, but there is a silver lining for us: It gives us the chance to buy those two high-yielding utilities now, before their next leg up.

Utility Pick No. 1: Reaves Utility Income Fund (UTG)

We’ve talked about the Reaves Utility Income Fund (UTG) many times before, and with good reason. It’s returned a sweet 41% for members of my Contrarian Income Report service since we added it to our portfolio in June 2023—less than two years ago.

As the name says, UTG holds utility stocks—mainly top US names like Entergy Corp. (ETR), Xcel Energy (XEL) and CenterPoint Energy (CNP), as well as “utility-like” firms such as pipeline operator Enterprise Products Partners (EPD).

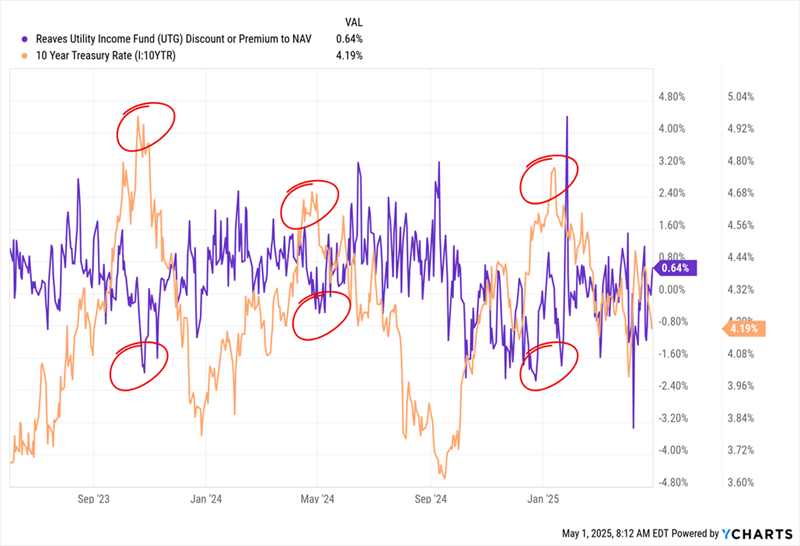

Let’s take a look at that holding period for a second; it clearly shows that every time the 10-year rate tops and moves lower, UTG goes from trading at a discount to net asset value (NAV)—the key valuation metric for CEFs—back to premium territory:

UTG’s Discount (or Premium!) Lets Us “Surf” the 10-Year Rate

With a slowdown ahead, I expect UTG’s current par valuation to move into premium territory. That amounts to gains to go with the fund’s 7% dividend—a payout that rolls in monthly, is rock-steady—and even offers a hint of growth (and special dividends):

That “recession-resistant” income stream, potential for a higher premium (and gains) as the economy slows, and lower volatility (UTG sports a “beta” rating of 0.84, meaning it’s 16% less volatile than the S&P 500), make it a smart buy now.

Utility Pick No. 2: Dominion Energy (D)

If you’re looking to go the single-stock route, consider Virginia-based Dominion Energy (D), which provides electricity to 3.6 million homes and businesses in Virginia (hold that thought!), North Carolina and South Carolina. It also pipes natural gas to about 500,000 users in South Carolina. The stock yields 4.9%.

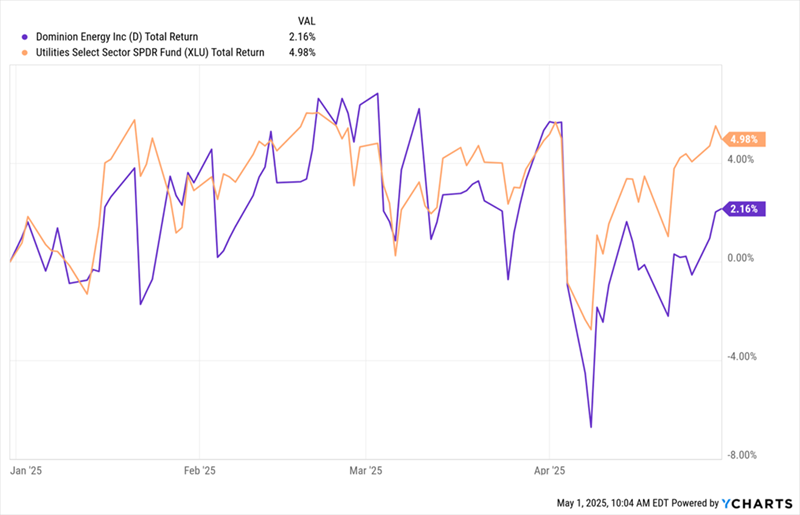

Utilities have been among the few sectors to hold their own this year, and D has done the same—though it has trailed the sector (shown below in orange by the benchmark utility index fund, XLU):

D’s “Utility Lag” Is the First Sign It’s a Bargain …

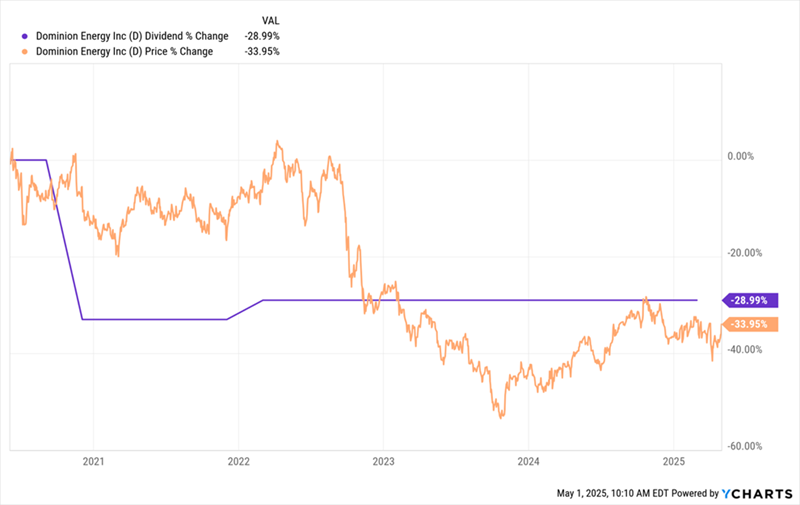

Long-time readers will know that this is because D is still in the “dividend doghouse” for a cut management brought in back in 2020 (showing just how long dividend investors’ memories are!)

The reason back then was too much debt. But here’s the thing: Unless management is a complete clown show (which D’s is certainly not), the safest dividend is often the one that’s been recently cut. And D has more than served its payout penance, with the dividend holding its own (and even being hiked once) since.

Nonetheless, the company’s share price fell behind the payout once the cut was made. Given the tendency for share prices to track dividend growth higher, that lag is the second sign we’re getting a deal here:

Lagging Share Price Is Our Second “Bargain Barometer” …

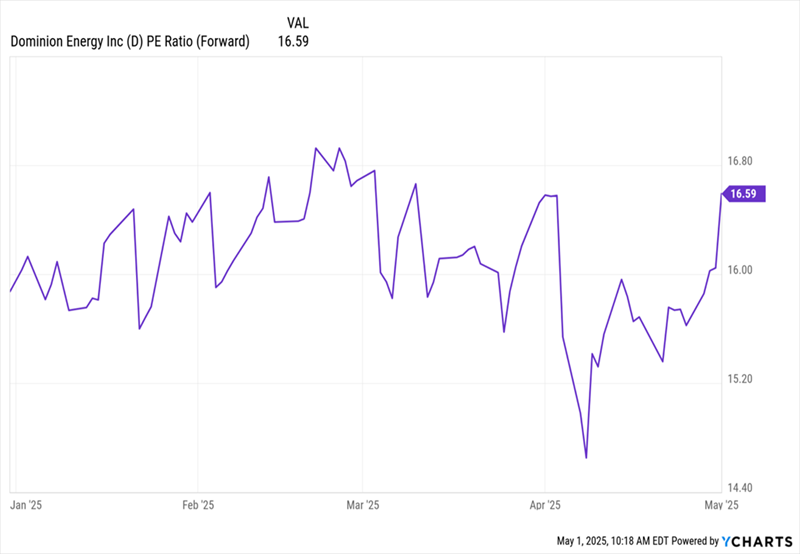

Lastly on the bargain front, D trades at 16.6-times forward earnings, below its five-year average of 19.3—though a strong earnings report last week has pushed that up, making our buy here a bit more urgent.

… And Its Below-Average (But Rising) P/E Is the Third

Frankly, it’s about time investors started to forgive and forget. For one of the main reasons why, let’s swing back to Virginia, D’s home state. As you may know, Virginia is ground zero for the data-center boom that’s supporting AI’s ongoing growth.

And it’s not just AI: Electric cars continue to hit the road, too. And more consumers are looking to heat pumps—a shift that’s baked in, no matter what happens in Washington. Dominion is likewise projecting a doubling of demand for its power by 2039.

The company is also relatively insulated from tariffs. It does expect to pay around $123 million in steel and aluminum levies on its Coastal Virginia Offshore Wind project. But that’s a small slice of the project’s $10.8-billion price tag and the $4.1 billion of revenue D generated in Q1 alone. And of course, the tariffs could always be cut or removed.

Which investment trusts could benefit from lower interest rates?

As vehicles for long-term investments, many investment trusts were hit when interest rates rose in 2022. With interest rates expected to fall by the end of the year, could now be the time to invest in one of these unloved sectors?

(Image credit: Craig Hastings via Getty Images)

By Dan McEvoy

Investment trust investors will have seen their discounts widen over recent years, and this is largely due to the rapid increase in interest rates that began in 2022.

The Bank of England’s Monetary Policy Committee (MPC) holds its next interest rates meeting this Thursday, and most analysts are forecasting that it will cut rates. The main debate is over the size of the cut, with consensus settling around a 25 basis point (bps) cut but some analysts thinking the MPC will go further and cut rates by fifty bps.

Even if the MPC holds rates steady at this meeting, the trajectory at present is downwards. While an inflationary shock could change the picture, it’s expected that interest rates will be lower at the end of the year than they are right now – perhaps as low as 3.25%.

Stay ahead of the curve with MoneyWeek magazine and enjoy the latest financial news and expert analysis, plus 60% off after your trial.

Rising interest rates hit some sectors, such as property or renewable energy infrastructure, particularly hard. But now, with rates starting to fall, “many analysts believe their prospects are looking brighter and there has been a surge of M&A activity in these sectors,” says Annabel Brodie-Smith, communications director at the Association of Investment Companies (AIC).

The AIC, which represents around 300 of the UK’s investment trusts, has polled analysts and investment trust experts about the sectors that they believe could benefit from an environment of falling interest rates. Here, MoneyWeek dives into their findings to highlight the sectors and trusts that could be set to gain if interest rates fall.

Infrastructure

Infrastructure investments could benefit in a lower-rate environment. Infrastructure projects tend to be very long-term investments, and as such investment trusts make a particularly effective means of gaining exposure.

When valuing an infrastructure investment, most professional investors use a formula called net present value to calculate how much a given project is worth today. One of the key inputs in this formula is the interest rate: the higher this is, the greater the present value of a long-term project is discounted (because higher interest rates mean that safer assets like bonds offer higher returns over time).

So falling interest rates serve to increase the present value of long-term infrastructure assets by reducing the discounting effect of interest rates.

“This discount rate effect would be more meaningful for longer life, lower risk ‘core’ economic infrastructure assets such as water, energy, transport and accommodation investments,” says Ashley Thomas, analyst at Winterflood Securities.

Thomas recommends HICL Infrastructure (LON:HICL) which invests predominantly in these areas and has 65% of its portfolio invested in the UK.

Alternatively, Thomas highlights BBGI Global Infrastructure (LON:BBGI) which invests in similar sectors but with a more global outlook, as only 33% of assets are UK-based.

Markuz Jaffe, analyst at Peel Hunt, and Colette Ord, head of real estate, infrastructure and renewable funds research at Deutsche Numis, both highlight International Public Partnerships (LON:INPP).

Ord argues that the 22% discount it currently trades at doesn’t reflect its portfolio’s return potential, and points out that “the current dividend yield of 7.7% is fully covered by earnings, and even if no further investments are made, the company could pay a growing dividend for at least a further 20 years”.

“The portfolio is around 73% weighted to the UK and some of the investments benefit from government-backed cash flows, so there is a beneficial link to reductions in gilt yields, and any impact this might have on underlying asset pricing,” adds Jaffe.

Renewable energy

Energy is of course a sub-set of the broader infrastructure sector, but renewable energy investments in particular suffered when interest rates started rising in 2022, and as such could be big beneficiaries as interest rates fall.

Bluefield Solar Income Fund (LON:BSIF) is another of Winterflood’s picks highlighted by Thomas as a renewable energy infrastructure pure play. 100% of its investments are UK-based.

One of the most popular renewable energy investment trusts is Greencoat UK Wind (LON:UKW), which “offers a pure play on the UK wind sector… and has built a strong track record of cash generation”, according to Jaffe.

Jaffe highlights that UKW’s board recently committed an extra £100 million to its share buyback program to take the total to £200 million, “one of the largest in the listed infrastructure investment company universe”. He also highlights the trust’s 22% discount to its end-of-March NAV, and 8.8% yield.

For an even deeper discount and greater yield, consider Foresight Solar Fund (LON:FSFL). This is currently trading at a 30% discount to NAV and offering a 10% yield.

The trust “offers exposure to a portfolio of solar assets located across the UK, Spain and Australia, with a development pipeline of Spanish battery energy storage system (BESS) and more solar projects,” says Rachel May, research analyst at Shore Capital.

“The board has been extremely proactive in its attempts to narrow the discount having recently announced that a further 75MW of projects have been identified for disposal,” May adds, highlighting the ongoing sales process for tis Australian portfolio and the sale of a 50% stake in its Spanish holdings at a 21% premium to book value.

Property

Real estate investment trusts (REITs) are a mainstay among investment trust and property investors. Low interest rates are generally good news for the property market: they reduce mortgage rates, thereby increasing demand for property and pushing up property prices.

It is worth bearing in mind too that a distinctive feature of investment trusts is that they can borrow money to leverage their investments, a practice called “gearing”. This debt is also subject to interest rate changes, and investment trusts with variable-rate debt can stand to benefit when interest rates fall.

“A cut in e Bank of England base rate correspond with a reduction in the sterling overnight index average rate, or SONIA, reducing debt costs for funds with unhedged floating rate debt using SONIA as a reference rate,” explains Emma Bird, head of investment trusts research at Winterflood Securities.

As such, Bird recommends Custodian Property Income REIT (LON:CREI). 18% of its debt is subject to a variable, SONIA-linked rate, so the trust “should therefore see reduced debt costs and subsequently higher earnings as SONIA falls”.

Growth assets

Companies that are positioned for long-term growth are also hit by higher interest rates, for similar reasons to companies in the sectors above: namely, their returns are likely to take a long time to come around, and as such higher rates decrease their attractiveness relative to safer investments like gilts.

Growth assets could take the form of early-stage companies, which are likely to be private. For exposure to these, Jaffe recommends HarbourVest Global Private Equity (LON:HVPE) which uses a fund-of-funds structure to offer exposure to global private companies.

HVPE’s discount increased from 15% in early 2022 to over 50% by October the same year. It is currently around 43%, but Jaffe says that the trust is taking steps to address this.

“The distribution pool, which supports buyback activity, has seen its allocation doubled from 15% to 30%, the investment structure is to be simplified via a dedicated separately managed account with HarbourVest Partners, and a continuation vote is being introduced for the 2026 AGM,” he says.

There are also nascent industries that could take many years to recuperate significant sunk costs, but for some of them, not even the sky will be the limit from there.

Ord picks out Seraphim Space Investment Trust (LON:SSIT) and its portfolio of space technology companies.

Lower interest rates could well improve sentiment around its capital-intensive portfolio of companies, but “perhaps more significant than the change in interest rates is a focus on defence spending,” she says.

This 10-stock ISA portfolio could yield £1,380 in passive income a year

Here’s a portfolio of dividend shares that could produce £115 of monthly passive income for investors who maximise their ISA contribution limit.

Posted by

Charlie Carman

PHP

Image source: Getty Images

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Diversification is a crucial consideration for passive income investors.. Since companies can cut or halt dividend payments at any moment, it’s important not to have all your eggs in one basket.

There’s no magic rule about the minimum number of dividend stocks required for a diversified portfolio. However, 10 shares or more is a good starting point. At this level of variety, there’s reduced exposure to the specific risks associated with any single company.

With that in mind, here’s a sample Stocks and Shares ISA portfolio investors could consider building to aim for £1,380 in annual passive income.

High-yield dividend shares

To reach this dividend income goal from a £20k ISA, investors would need a 6.9% yield across their holdings. Given that the FTSE 100 average is only 3.6%, buying high-yield stocks will be required. A simple index tracker would fall well short.

To illustrate the kinds of stocks I’m talking about, investing £2,000 in each of the UK companies listed below would hit the passive income target. I’ve selected this sample portfolio from FTSE 100 and FTSE 250 shares. In the spirit of diversification, it covers different areas of the market, from banking to pharmaceuticals, media to water, and beyond.

Stock

Dividend yield

Aviva

6.63%

BP

6.51%

British American Tobacco

7.52%

GSK

4.48%

HSBC

6.17%

ITV

6.35%

Johnson Matthey

6.35%

Legal & General

8.55%

Primary Health Properties

6.95%

Sainsbury’s

5.18%

Severn Trent

4.30%

I reckon it’s a credible mix of quality dividend stocks, giving prospective investors plenty to chew over. Furthermore, I didn’t blindly pick the highest yields I could find, which is a common mistake for novice stock pickers.

Buying shares based on their yields alone overlooks other essential qualities, such as dividend cover, distribution histories, and the fundamental health of the business behind the headline yield figure.

That’s not to say these firms pay sure-fire dividends. There’s no such thing. But it’s a nice snapshot of top UK dividend shares to consider buying, and I hold some myself.

A lesser-known FTSE 250 stock

One of my choices that may be less familiar to readers is Primary Health Properties (LSE:PHP). With 29 consecutive years of dividend increases to its name and a yield just shy of 7%, this real estate investment trust (REIT) should capture the attention of passive income investors.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

The company’s portfolio is concentrated in long-term leasehold and freehold interests in modern primary healthcare facilities. A recent £22.6bn funding increase for NHS England is a big tailwind for the REIT, considering 89% of its rent roll comes from government bodies. Coupled with anticipated interest rate cuts, macro conditions look encouraging for share price growth.

I also like the steady upward trajectory of Primary Health Properties’ financial results. Net rental income and adjusted earnings per share have improved year on year for at least five years. Growth opportunities in Ireland are another attractive point. The Emerald Isle is the company’s “preferred area of investment” today.

Admittedly, the balance sheet could be in better shape. Net debt of £1.32bn looks uncomfortably high measured against a market cap of £1.35bn. This raises questions over the dividend’s sustainability. Nonetheless, on balance, I think favourable market fundamentals mean the future looks bright for this income stock.

PHP currently up 18% from its recent low, so a lot of people sitting on a decent profit, so that could mean profiting taking may hit the share if there is bad market news.

If we use UKW as the working example, they go xd next week

The fcast dividend is 2.6p, if you buy before the xd date, you will earn 5 dividends in just over a year.

Current price 117p Fcast Dividend 2.6p

5 Dividends earned 13p – a yield of roughly 11%

If the share price has increased, you take your profit and try to do it with another Trust.

If not you could keep taking the dividends, which will be re-invested to earn more dividends to be re-invested.

All baby steps. The above is not a recommendation to buy but obviously the main criteria of the Trust you choose, apart from the yield, is the dividend ‘secure’ although no dividend is 100% secure.

AEW UK REIT PLC ex-dividend date Aquila Energy Efficiency Trust PLC special ex-dividend date Artemis UK Future Leaders PLC ex-dividend date Chenavari Toro Income Fund Ltd ex-dividend date CVC Income & Growth Ltd EUR ex-dividend date CVC Income & Growth Ltd GBP ex-dividend date Fidelity Special Values PLC ex-dividend date GCP Infrastructure Investments Ltd ex-dividend date Marwyn Value Investors Ltd ex-dividend date Partners Group Private Equity Ltd ex-dividend date Petershill Partners PLC ex-dividend date

Community Healthcare Trust Incorporated (NYSE: CHCT) is a U.S.-based real estate investment trust (REIT) specializing in owning and managing income-producing healthcare properties, primarily outpatient facilities, across the United States. As of December 31, 2024, the company had invested approximately $1.2 billion in 200 properties spanning 36 states, totaling about 4.4 million square feet. Yahoo Finance+2StockAnalysis

📊 Stock Overview

Community Healthcare Trust Inc (CHCT)

$17.01

Year Low14.76

Year High27.62

As of May 3, 2025, CHCT’s stock price stands at $17.01, reflecting a 0.89% increase from the previous close. The stock’s 52-week range is between $14.76 and $27.62.

📈 Financial Highlights

Market Capitalization: Approximately $454.8 million

CHCT offers a dividend yield of 11.1% with a payout ratio of 105%. The next ex-dividend date is May 9, 2025, and the dividend is payable on May 23, 2025.

🔍 Analyst Insights

Analysts have a “Buy” consensus rating for CHCT, with a 12-month price target of $21.25, indicating a potential upside of approximately 24.9%. StockAnalysis

For more detailed information, you can visit the company’s official website: .

As of May 2025, here are ten of the highest-yielding U.S.-listed Real Estate Investment Trusts (REITs), offering dividend yields ranging from approximately 11% to over 20%. These REITs span various sectors, including mortgage-backed securities, healthcare, and specialty real estate.

Top 10 High-Yielding American REITs (May 2025)

Orchid Island Capital (ORC) Dividend Yield: 20.2% A mortgage REIT specializing in residential mortgage-backed securities.

Ellington Credit Co. (EARN) Dividend Yield: Approximately 14% Invests in mortgage-backed securities and related assets.

AGNC Investment Corp. (AGNC) Dividend Yield: 14.3% A prominent mortgage REIT with a focus on agency-backed securities.

Arbor Realty Trust (ABR) Dividend Yield: 12.5% Engages in real estate finance, including bridge and mezzanine loans.

Chimera Investment Corp. (CIM) Dividend Yield: 12.0% Invests in a diversified portfolio of mortgage assets.

New York Mortgage Trust (NYMT) Dividend Yield: 13.0% Focuses on residential mortgage loans and related investments.

Dynex Capital (DX) Dividend Yield: Approximately 12% Invests in mortgage-backed securities and loans.

Pennymac Mortgage Investment Trust (PMT) Dividend Yield: Approximately 11% Specializes in residential mortgage loans and related assets.

Community Healthcare Trust (CHCT) Dividend Yield: 11.0% Owns income-producing real estate properties in the healthcare sector.

These REITs offer attractive yields but come with varying risk profiles, particularly those heavily invested in mortgage-backed securities. It’s essential to conduct thorough due diligence and consider factors like dividend sustainability, interest rate sensitivity, and sector-specific risks before investing.

These 7 European And Asian Stocks Are Crushing It And Still Cheap

American exceptionalism in stocks has come to an abrupt end. Here’s where global fund managers are seeing the most opportunities.

Forbes Staff. Hank Tucker is a Forbes staff writer covering finance and investing.

London-based BAE Systems makes the Eurofighter Typhoon fighter jet and is benefitting from European nations turning away from U.S. defense contractors.AFP via Getty Images

Portfolio managers investing in non-U.S. stocks have been trying to get investors’ attention for years, pointing out that valuation multiples overseas have grown much cheaper than stocks in the U.S. since the Financial Crisis, and this year their patience has finally been rewarded.

The MSCI EAFE index, covering stocks in 21 developed markets excluding the U.S. and Canada, is up 7% this year, significantly outperforming the 7% decline for the S&P 500 index in the U.S. It represents a small dent in the decades-long disparity between the two—JPMorgan reports that from the second half of 2008 through the end of 2024, the S&P 500’s annualized total return was 11.9%, versus 3.6% for the MSCI EAFE. That amounts to a seven-fold return on investment for the former, while the international portfolio hasn’t even doubled.

Some of that dominance is because U.S. stocks have produced much stronger earnings growth, but some is also because the S&P 500’s average P/E multiple has swelled to 21.7x, while EAFE is only at 14.0x after starting in a similar position, according to the JPMorgan report. With fears swirling that tariffs and broader uncertainty will compress earnings in the U.S., international investors are hoping that gap can narrow even more.

Asset management giants like Vanguard, BlackRock and Franklin Templeton offer dozens of low-cost international funds to choose from. Active managers that are outperforming the indexers are primarily doing so by zeroing in on European defense stocks and domestically-focused companies that are perceived to be insulated from the effects of Trump’s tariffs in nations like Japan and China.

“We’re at the lowest relative weight of the U.S. in quite some time,” says Travis Prentice, chief investment officer of the Informed Momentum Company, which manages $2.5 billion in momentum-based strategies. “In aerospace and defense, particularly in Europe, momentum not only persisted, but accelerated through all this tariff turmoil.”

Graeme Forster, a portfolio manager at Orbis overseeing $4.5 billion in its International equity strategy, agrees, singling out airplane engine maker Rolls-Royce, London-based BAE Systems, Europe’s largest defense contractor, and German defense firm Rheinmetall as good bets. Orbis’ international strategy has returned 10.8% annually since inception at the end of 2008, beating its index by four percentage points, and produced a 10% return net of fees in the first quarter this year.

Rolls-Royce and BAE Systems are each up more than 30% this year already. Rheinmetall has soared 150% thanks largely to the German parliament’s commitment in March to create a fund to spend more than $500 million on defense and infrastructure over 12 years, a stark departure from the nation’s longstanding frugal spending policies.

Trump has been critical of NATO on several occasions, attacking European nations for not paying enough to support the alliance, and paused U.S. military aid to Ukraine in March. That prompted the European Commission to unveil a “Readiness 2030” plan in March enabling $900 million in spending to defend Ukraine and protect themselves from Russia’s aggression. Ursula von der Leyen, the European Commission’s president, cautioned that “the security architecture that we relied on can no longer be taken for granted” and urged nations to “buy more European.” That’s contributed to U.S. defense firm Lockheed Martin, which makes F-35 fighter jets, sinking 15% since Trump’s election, while BAE Systems, which also produces fighter jets, has soared.

“Sometimes there’s news and sometimes there’s noise, and we’ve always had to figure out how to sift through it, but 2025 has been a particularly newsy year,” says Alaina Anderson, portfolio manager for William Blair’s $1.1 billion International Leaders Fund, which recently added positions in BAE Systems and French cybersecurity and defense firm Thales. “It’s been news that speaks to a change in the structure of markets, the nature of relationships between countries and the durability of long-established institutions.”

Anderson’s fund is also adding positions in China despite its status as the chief target of Trump’s trade war, focusing on stocks like Trip.com, the country’s largest online travel company with more than 50% market share within China. “We think there’s low geopolitical risk in that name, given that it’s really domestic-driven consumption,” says Anderson, with the stock up 50% since last August.

Despite Trump’s pressure in ratcheting up tariffs on China to as much as 145%, the Shanghai Composite index has lost a mere 1.6% in 2025. Prentice references Beijing-based electronics firm Xiaomi as one stock with momentum after tripling in the past year. It sells everything from smartphones to electric vehicles and could be poised to benefit if America’s largest tech companies face harsher tariffs on imports into China.

Orbis’ Forster is more enthralled by opportunities in neighboring Japan, where the Nikkei 225 has roughly mirrored the S&P 500’s losses so far this year. The yen has weakened substantially in the last five years, helping Japanese companies hire skilled workers cheaply in U.S. dollar terms, and Forster thinks the prospect of higher interest rates, which the Bank of Japan raised in January to their highest level in 17 years, could counterintuitively stimulate growth.

“Everyone is a massive saver there. Everyone’s paid off their mortgages and they’ve got a ton of money, and it just sits in bank accounts earning zero,” says Forster. From 2016 until last year, Japan had negative interest rates in place, but with inflation finally returning, the rate hikes could make the yen stronger, ease import costs and improve margins for retailers and domestic businesses.

Forster likes real estate firm Mitsubishi Estate’s stock, with a valuable portfolio of real estate which trades at about half of its fair value, Orbis estimates. The developer owns most of the property surrounding Tokyo’s famed Imperial Palace—its stock performance has been middling for decades, but it’s rallied 25% so far this year, with rents rising meaningfully for the first time since Japan’s 1989 market crash.

“The nice thing about a real estate business is as they push up rent, it’s not a wage-heavy business, so they’re not getting squeezed on the cost side,” says Forster. “That could be very sustainable, because real estate is quite cheap in Japan, and you’re getting it at half price.”