Dorothy ….. realised early on into her retirement that she and her husband, Alan, did not have enough income to live the sort of life they had anticipated. Despite having a workplace pension and the state pension, the 75-year-old was concerned that the standard of life they were used to would not be achievable with the amount coming in. She said: “In my fifties, I was the sole income earner for our family of four, with a mortgage and two teenagers to put through university. I’d had a chequered work history and thought my tiny pension pots might add up to a pension large enough to enable me to retire. I’d set up an appointment with a pension adviser and after he reviewed the information, he shook his head and informed me that they didn’t add up to much. Definitely not what we wanted. He said that I needed to keep working and I’d be able to retire at 85.”

Dividends can be more reliable than share prices as they’re driven by the companies performance itself and not by the whim of investors.

As part of a total return / reinvestment strategy, this income could be reinvested into income assets or back into the equity market depending on the relative valuations.

The emotional benefits of dividend re-investment. In fact, with this investment strategy you can actually welcome falling share prices.

How To Boost Your Cash Yield At Fidelity, Vanguard, Chase And Schwab

By William Baldwin, Senior Contributor

Inflation and high interest rates aren’t going away. Don’t let your checking account rob you of a decent return on liquid assets.

Forget bank CD rates for a moment. If you want more interest, look at something under your nose: the bank account you use to collect a paycheck and pay bills.

Chances are you are earning something in the neighborhood of zilch on your liquid assets. You can fix this. You can get 4%.

Below are four remedies to pick from, one of them, interestingly, coming from a bank that participates in the usual checking robbery. Alongside those recommendations you will see tips on protecting your money from thieves.

The problem: You need a pile of cash to cover checks and other debits, a pile big enough to eliminate the risk of a bounced payment. If your bounce-proof sum averages $15,000, $600 a year in potential interest is leaking out of your pocket. With a bit of effort you can capture this interest.

Each of the four solutions has two parts. You set up a transaction account that has a fairly low balance and attach to it an investment account that has a large sum. The large pot goes into either a money market mutual fund or an exchange-traded fund that acts like a money market.

The transaction account does most of the things you expect from a bank. It takes in electronic payments of paychecks, Social Security benefits and the like; it makes electronic disbursements for utility bills, full payment of credit card balances and the like; it can be used to send money electronically to a tax collector or another financial account.

The investment account holds most of your short-term assets. It could also hold all of your other stocks and bonds.

We’re talking about taxable accounts here. Retirement accounts are a different ball of wax. Also, the discussion is aimed at people who pay off credit card balances in full. If you carry a card balance, seek advice elsewhere.

Solution #1: Fidelity Investments

Open two accounts, a brokerage account and what Fidelity calls a Cash Management Account. The CMA does all the everyday debits and credits and pays close to 4% interest on the Government Money Market available there. Take a pass on Fidelity’s FDIC-insured account, which has a crummy yield. (See “FDIC—Who Needs It?”)

The brokerage account has lots of investment options, including a Treasury-only money market fund. Aim to maintain a fairly small balance in the CMA and a large sum in the brokerage account.

Your two Fidelity accounts can be hot-linked with a “self-funded overdraft protection,” whereby the CMA automatically draws on the brokerage account’s money fund to keep its balance from dropping below $0 (or, if you prefer, a target balance amount). Order checks for the brokerage money market so that you have the option of paying big bills, such as for estimated taxes, via the mail, earning a few extra days’ interest.

While you’re at it, get a Fidelity Visa card, which rebates 2%.

Advantages: Fidelity’s 216 walk-in branches and its excellent platform for trading stocks, Treasury bonds and exchange-traded funds.

Disadvantage: no cashier’s checks.

What About The Thieves?

Fidelity, Chase and Schwab will be happy to attach a debit card to your transaction account. Chase has its own automatic teller network; Fidelity and Schwab will reimburse you for ATM fees. My advice is to decline the card. Vanguard doesn’t have a debit card but offers links to Venmo and PayPal. Avoid such links.

Financial technology provides wondrous convenience to you. It’s also convenient for pickpockets and North Korean hackers.

Protect your life savings from the thieves. In addition to the main financial relationship with one of the four institutions described above, open an account somewhere else, call it Acme Bank & Trust, for walking around money. At Acme, get a debit card to use at ATMs. Use Acme to fund your Venmo, PayPal, GooglePay and ApplePay accounts.

Feed Acme via wire transfers from your brokerage. Someone hacking into Acme won’t have access to the brokerage account.

Further safety steps: Opt for two-factor authorization on financial accounts and email accounts; never use your phone to look at your brokerage account; don’t let your browser save the password for a financial account; access the brokerage account only from home or a very secure Wifi.

Solution #2: Vanguard

Open what Vanguard calls a Cash Plus account. Cash Plus handles the everyday electronic transactions and pays 3.65% on an FDIC-insured balance. Keep a small amount in the FDIC account and a large sum invested in the Vanguard Treasury Money Market. Shares of that fund are one of the few securities permitted in Cash Plus, so a brokerage account is not necessary, but it’s a good idea to build in some flexibility, so open a brokerage account as well.

You can transfer between the two accounts but there’s no hot link, so you have to keep an eye on the balances. After a year is up you are eligible for check writing. Order checks for the money fund and use them for big-ticket items like college tuition and estimated taxes.

Vanguard runs leaner than Fidelity. With lower expense ratios on its money funds, its yields are better, but when you call for help you’ll spend more time on hold.

Advantage: Good interest rates, except on the Cash Plus balance.

Disadvantages: no branches, no cashier’s checks, mediocre customer service.

Solution #3: J.P. Morgan Chase

Open a checking account. Then open a self-directed, zero-commission brokerage account. Transfer into the brokerage at least $250,000 of assets, which can be stocks you bought long ago (you don’t have to sell anything). This will qualify you for a $700 new-customer bonus and protect you from nuisance fees on the checking account.

In the brokerage account keep a large sum invested in a Treasury bill exchange-traded fund. Keep as little as possible in the checking account, which pays 0.01% interest.

Use the checking account for the usual direct deposits, automatic debits, paper checks and access to the Zelle bill-paying network. When the checking balance runs low, sell some of the ETF. On the next business day, transfer the proceeds into checking.

You can eliminate the one-day lag by stashing money in a liquid savings account ($50,000 minimum to open), but this pays only 3.6%, is subject to state tax and doesn’t absolve you of the obligation to move money from the brokerage account to the checking account.

The loss of interest on the transaction account makes this an expensive solution. But you get a huge network of branches and ATMs, access to cashier’s checks (needed to buy a car or house) and a banking relationship that may be useful if you want a mortgage or business loan.

You might find similar offers at other nationwide banks.

Advantage: traditional banking with face-to-face service.

Disadvantage: less interest income.

Solution #4: Charles Schwab

Schwab, a forerunner in discount brokerage, has a bank subsidiary that can do what banks usually do. As at Chase, you open both a brokerage account and a checking account. As at Chase, the yield on the checking account is negligible (0.05%). The main difference is that Schwab has an attractive Treasury money-market mutual fund.

Schwab offers bounce protection: In case of an overdraft, the checking account can draw on a margin loan from the brokerage account. But it’s up to you to clear the (expensive) margin loan by selling money fund shares.

A Treasury mutual fund will be better for you than a T-bill ETF if you are going to be making frequent transfers between the brokerage account and the checking account. The ETF has a transaction cost in the form of a bid/ask spread, while the mutual fund has no transaction cost. The mutual fund option does not, however, spare you the one-day wait between cashing out and getting access to the proceeds.

Advantages: banking services, including cashier’s checks, and branches in 45 states.

Disadvantage: less interest income than at Fidelity or Vanguard.

FDIC—Who Needs It?

A popular choice for people using a broker for their banking is an account covered by the Federal Deposit Insurance Corporation. It’s a bad choice, for two reasons. The yield is likely to be low and the interest is subject to state income tax.

Better: Keep a minimal sum in the transaction account, the one that takes direct deposit of your paycheck and handles automated payments of utility and credit card bills. Store most of your liquid assets in a U.S. Treasury fund. When the transaction account runs low, fuel it from the Treasury fund. When it’s flush, send money the other way.

A fund invested in short-term U.S. Treasury paper has no more credit risk than a bank account backed by the FDIC. The only reason the FDIC is safe is that it is in turn backed by that same U.S. Treasury.

For the Treasury fund, you can use a Treasury-only money-market at Vanguard, Fidelity or Schwab (see table for yields). If your broker isn’t one of those, use an exchange-traded fund that owns the same kind of Treasury bills and notes. Two good ETF choices: SPDR Bloomberg 1-3 Month T-Bill (ticker: BIL), and Vanguard 0-3 Month Treasury Bill (VBIL).

The price of the SPDR product climbs a penny a day (rounding here); after a month it disgorges a 30-cent dividend and the price collapses by 30 cents. With the ETF, but not with a money-market fund, you’ll suffer a transaction cost in the form of a bid/ask spread on the fund shares. For the two I cited it comes to $1.10 – $1.30 per $10,000 round trip. Also with the ETF: You don’t get your hands on the cash until the day following a sale of ETF shares. In some cases, such as when you use a check to draw on a money-market fund, the money market fund doesn’t entail a one-day wait.

The objective with any Treasury fund is to keep your state tax collector’s mitts off the interest. If you live in no-income-tax Texas or Florida, this is irrelevant. If you live in a high-tax state, it matters. State tax can shave 20 to 50 basis points (0.2 to 0.5 percentage point) off the return on a money-market fund.

Watch out. There are funds with “Treasury” in the name that invest in repurchase agreements, which are not eligible for exemption from state tax. Three states have an additional hurdle, relating to asset percentages

Here’s How Much Warren Buffett Has Earned From Coca-Cola’s Dividend By Will Healy – Jan 27, 2023

The stock has hiked its payout annually for 60 years, a factor that greatly benefited investors such as Buffett.

After 35 years, payouts add up with this dividend growth stock.

One of the more notable investments in acclaimed investor Warren Buffett’s career was Coca-Cola (KO 0.53%). Buffett is a longtime fan of its signature drink, a factor that likely helped inspire the 9% stake that his company, Berkshire Hathaway (BRK.A 1.99%) (BRK.B 1.76%), took in the beverage giant in 1988.

But despite the gains made over 35 years, the investment has arguably earned more attention for Buffett as a dividend stock. Investors should capitalize on that attention, as it offers a lesson about the benefits of dividend growth and shows how payouts play a potential role in driving a long-term investment strategy.

Berkshire’s dividend income from Coca-Cola Berkshire owns 400 million shares of Coca-Cola stock. Consequently, the $1.76 per share annual dividend earns new buyers a cash return of around 2.9%, well above the 1.7% return of the S&P 500.

But both are a pittance of Berkshire’s yield in Coca-Cola. In 2022, Berkshire received $704 million in dividend income from Coca-Cola. On an original investment of $1.3 billion, that amounted to a yearly return of 54% !

That return is so high because Berkshire bought most of its Coca-Cola shares in 1988 and 1989, beginning the purchases soon after the 1987 stock market crash. Moreover, Coca-Cola has maintained a 60-year streak of payout hikes, making it a Dividend King. Hence, those 35 years of payouts have earned Berkshire nearly $10.2 billion in dividend income from this stock!

Putting the Coca-Cola investment into perspective Although that sounds like an impressive return on a $1.3 billion investment, some factors may discount the significance and appeal of Coca-Cola’s dividend. For one, Berkshire’s stake in Coca-Cola is now worth just over $24 billion. That means that stock price growth drove the majority of Berkshire’s total return in this stock, not dividends.

Investors should also remember that Coca-Cola stock is likely not a buy at this stage. An implicit confirmation of that feeling appears to come from Buffett himself, as Berkshire bought its last stake in the company in 1994. Even then, the dividend could be the only reason Buffett’s team treated this stock as a hold rather than a sell.

Resilient fund has helped to turn defence into an investment art form

Story by Jeff Prestridge

Investment trust STS Global Income & Growth is not designed to shoot out the lights. Far from it.

It’s a conservative investment approach which has worked so far. Since November 2020 it has generated a return – a mix of capital and income growth – in excess of 35 per cent.

While this is below the average 43 per cent return for its global equity income peer group, senior fund manager James Harries says the £287 million trust is doing exactly what the portfolio was set up to do – steering a steady course through ups and downs. He runs it with colleague Tomasz Boniek.

‘We want STS Global Income & Growth to be a high quality, low volatility trust in the global equity income space,’ says Harries.

‘That means running a concentrated portfolio of exceptional, resilient companies which are capable of generating sufficient income to support growing dividends. We see our core shareholders as having a requirement for income while not wishing to see their capital depleted – that is what we are trying our hardest to deliver.’

STS GLOBAL INCOME & GROWTH TRUST: Resilient fund has helped to turn defence into an investment art form

In terms of income, the trust’s annual dividend is moving in the right direction.

Three years should become four in the next few weeks or so when the trust reports its final quarterly dividend payment for the financial year ending March 31 (dividends paid so far this year total 4.758p).

As far as capital depletion is concerned, it has been far more resilient than its peers recently.

Over the past six months the trust has recorded a gain of 5 per cent compared with the 3.2 per cent loss by the average for its peer group. At other times when markets have declined – for example, at the start of the Ukraine war in 2022 and later in the same year when interest rates rose suddenly– it has proved equally resilient.

The trust is currently invested across 31 companies, with its only exposure to the ‘magnificent seven’ US stocks – Alphabet, Amazon, Apple, Meta, Microsoft,Nvidia and Tesla – being in Microsoft.

STS GLOBAL INCOME & GROWTH TRUST: Resilient fund has helped to turn defence into an investment art form

In recent months the trust has taken stakes in a number of new stocks. These include Spanish IT company Amadeus, UK pest control specialist Rentokil, German tech company Siemens and US sportswear giant Nike.

Harries says: ‘Nike’s shares are a third of the value they were trading at in late November 2021. The company may have to shift some of its production away from Vietnam if Trump’s tariffs remain in place, but it has sufficient pricing power to withstand what the President puts in its way.

‘At the end of the day, it remains a quality business – and that is what I am interested in holding under the bonnet of STS Global Income & Growth.’

STS currently yields 2.72%, so currently of no interest for the Snowball.

How the “Smart Money” Is Playing US Stocks Now (for 9.5% Dividends)

Michael Foster, Investment Strategist

Are US stocks set to lose out to the rest of the world forever ? That’s what the press would have us believe. But we contrarian dividend investors are looking at this from a different angle.

Our strategy? Buy America when the rest of the world is selling.

It’s worked before, and we have every reason to believe it will work now, too. So let’s talk about it—and the best way to position ourselves for US stocks’ next leg up, with a healthy dividend payout on the side.

Press Panics, US Stocks Bounce

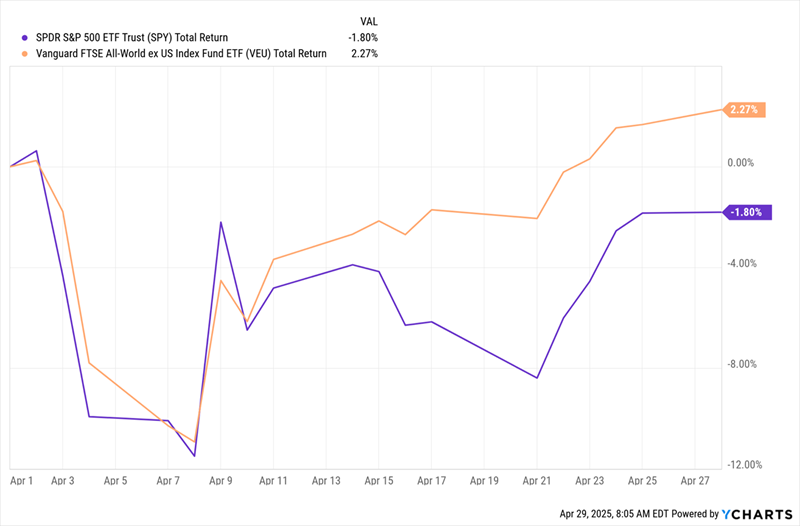

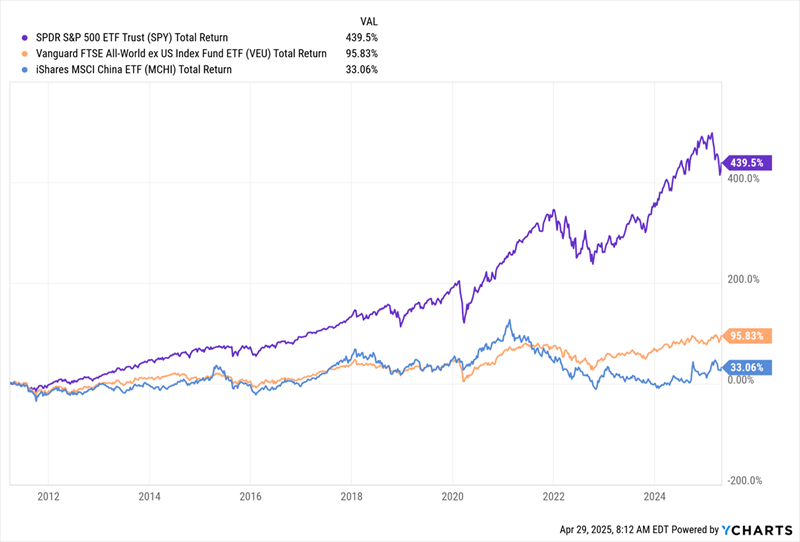

It’s funny, but not surprising, that the moment “sell America” became a headline earlier this year, US stocks started to recover. That said, they are still behind the rest of the world, as we can see by the performance of a popular S&P 500 index fund (in purple below) compared to the Vanguard FTSE All-World ex-US ETF (VEU), in orange.

US Stocks Dip, Start to Bounce Back

Note that both US and global stocks fell about the same amount when the Trump administration announced big global tariffs on April 2. But global stocks recovered more quickly in the following days. And then, last week, US stocks started to catch up.

History tells us that they’re likely to do much more than catch up in the long run.

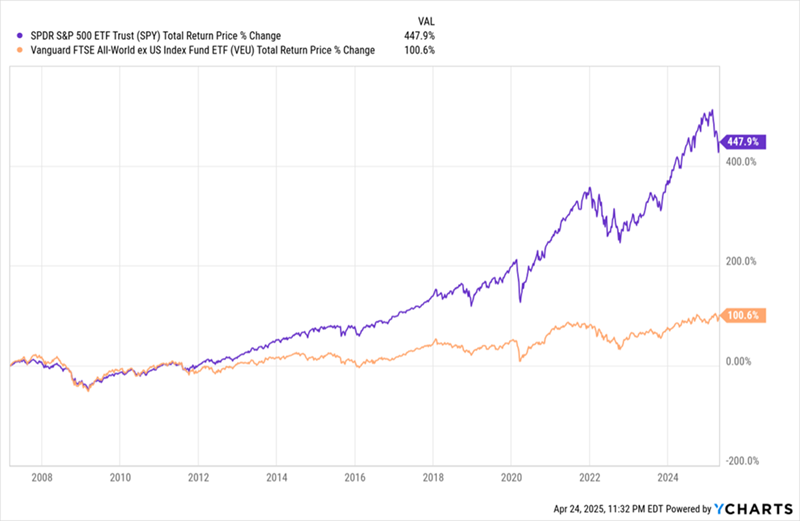

US Stocks Outpace the Rest of the World Over Time

Going back to VEU’s IPO in 2007, the S&P 500 has returned 9.9% per year on average, as of this writing, while VEU returned just 3.9% annualized.

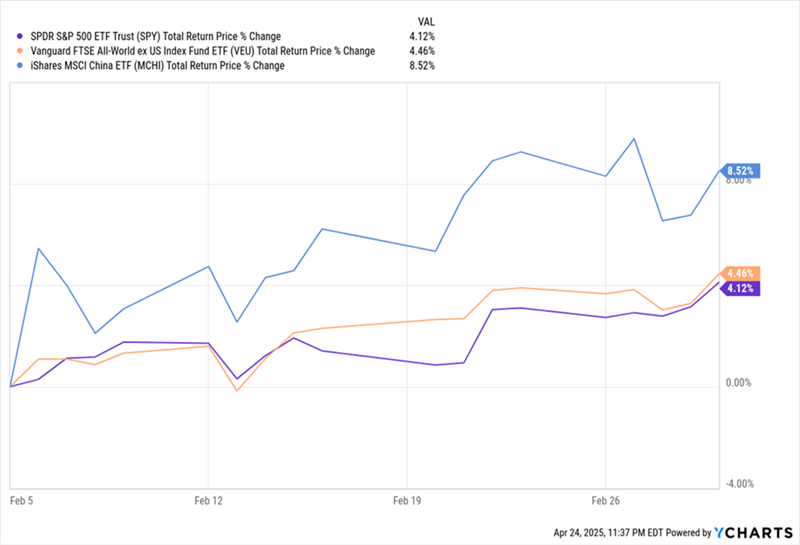

This shows why buying US stocks when they lag is a winning move in the long run. We can see that more clearly when we go back to the last time the world soured on US stocks in favor of foreign alternatives, which was a bit over a year ago in February 2024.

Back then, Reuters wrote, “Investors dumped US shares, bought China in week to Wednesday.” At the time, Chinese stocks—shown in blue below by the performance of the iShares MSCI China ETF (MCHI)—were more than doubling their US cousins (in purple), which were themselves lagging global stocks (in orange) by a bit.

The Last Time America Disappointed

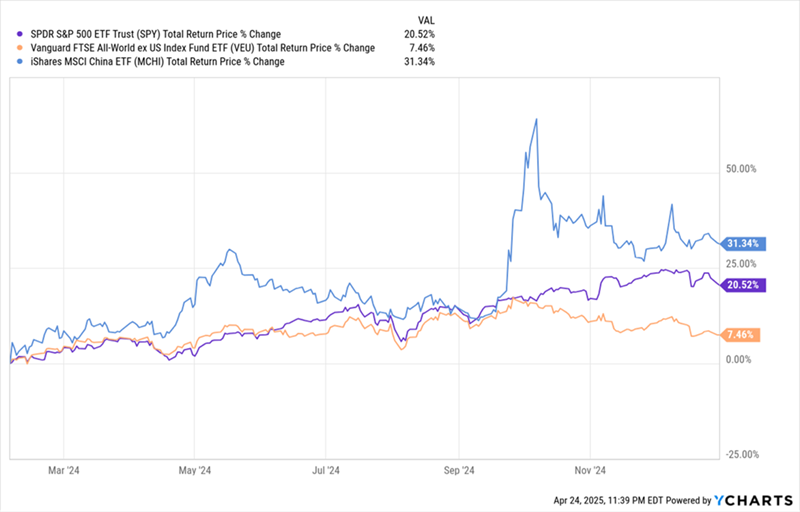

As we can see below by looking at Chinese stocks, that country’s markets did hold their value for the rest of 2024, but US stocks surpassed those of the rest of the world and started to close the gap with Chinese stocks by the end of the year.

US Stocks Take Off, Close in on Chinese Equities

And in the longer run, Chinese stocks trail. If we go back to MCHI’s IPO in 2011, we see that it has badly lagged US and global stocks, being almost flat:

US Still Leads for Long-Term Wealth Creation

So, time and time again we see the same pattern:

When US stocks are underperforming, we get a chance to buy them at a discount relative to their global peers.

The underperformance might last for a while, but over timespans lasting decades or longer, American assets outperform.

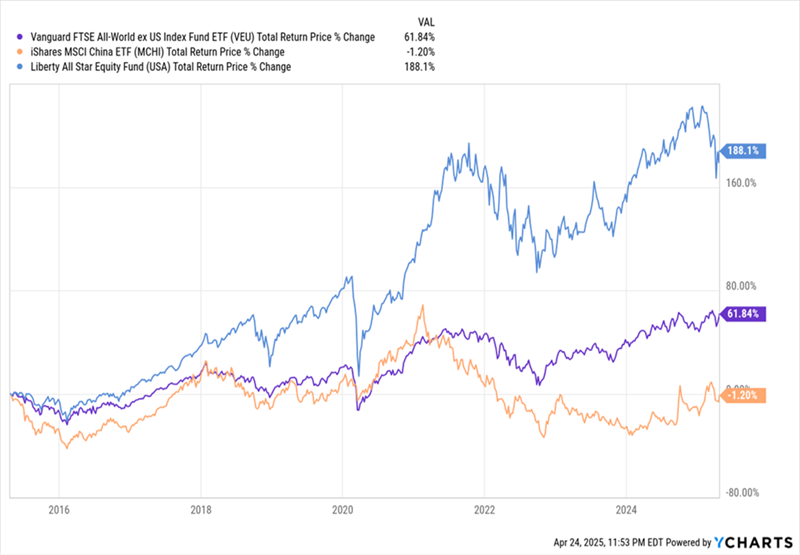

For us long-term investors, then, it makes sense to take advantage of the recent lag in US stocks to buy—and position ourselves for a bigger return over the long haul. One of the best ways to do so is through a closed-end fund (CEF) called the Liberty All Star Equity Fund (USA), which yields a rich 9.5% as I write this.

USA holds well-known US large caps in a diversified portfolio, with Microsoft (MSFT), Amazon.com (AMZN), Visa (V), Capital One (COP) and many others as top positions.

The fund also focuses on firms with strong cash flow, “moats” in their business models that help them fend off competitors, and histories of strong returns. It also “translates” those profits into that huge income stream for investors who buy now.

Moreover, USA (in blue below) has outrun global and Chinese stocks in the last decade.

USA Beats China and the Rest of the World

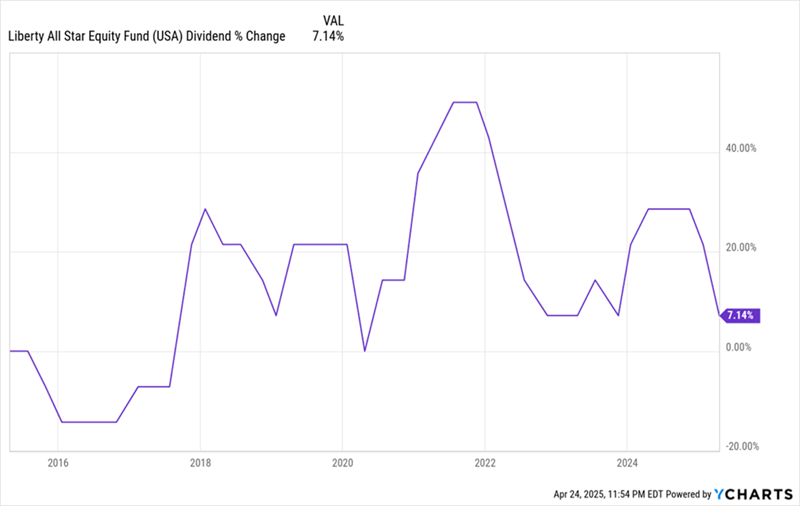

USA’s big dividend didn’t just hold steady over this period, it grew, as the fund pays out a percentage of its net asset value (NAV, or the value of its underlying portfolio) as dividends.

USA’s Payouts Grow

By investing in USA, we’re getting a huge and reliable income stream that stands the test of time. And now that the market has sold off, there’s an opportunity to buy before we go back to the norm of American outperformance.

Which brings me to the fund’s discount to NAV: As I write this, USA trades around par. That makes it a good trade now. But if you want to maximize the gains you collect in addition to that huge 9.5% dividend, it could pay to wait for the next dip—and the chance to buy at a discount.

My core contention for some time has been that UK interest rates are too high. They are punitive, with positive real rates well over the inflation rate. This might be necessary if the UK economy was expanding too fast, but we are far from that happy outcome, with the GDP growth rate well under the long-term average.

We’ve seen UK interest rates come down by a smidgeon, but they could still go a lot lower if inflation fears started receding. That might be a growing possibility post-Trump and his tariffs. However we look at it, the immediate impact of these tariffs on the UK economy will be contractionary, i.e., there’s a chance we could experience a slowdown in growth. Gas prices are also decreasing (a significant issue for UK energy prices) and most businesses have rammed through any price increases they had planned after the increase in labour costs (courtesy of the NI changes).

Crucially, Five-year swap rates—a key metric used by mortgage companies—have started to edge lower and currently stand at around 3.7%. UK 2-year gilt yields have also recently pushed below 4%, though they are now a tad above that level again.

I believe the chances of UK interest rates dropping to 4% or lower more than twice have significantly increased—I would now estimate that probability to be above 50%. If this is the case, it’s reasonable to expect the 5-year swap rate to decrease significantly to around 3%, and the UK 2-year gilt rate to approach 3.5%.

Many investors will intensify their search for income-based investments at these levels, with most attention on UK alternative investment trusts. Because of a massive sell-off in these alternative funds, yields of well more than 8% are very common. That implies that if UK 2-year gilts fall below a 3.5% yield, a portfolio of carefully chosen alternative funds could provide an excess yield of over 5%, i.e. 8.5% minus 3.5%. Crucially, many of these funds are now trading at discounts well in excess of their medium-term average.

Cue the table below, which maps out a model alternative portfolio of five alternative income funds, all of which, in effect, lend money to other businesses. Each of these funds – bar CQS New City High Yield – invests in slightly complex transactions, be they asset-backed securities or infrastructure loans. As an aside CQS invests in relatively simple-to-understand corporate bonds with a higher yield – see below. That makes these funds difficult for most investors to understand, but I think these five funds look compelling for adventurous types. However, some, such as Sequoia and BioPharma, are more compelling than others.

I suggest these fine funds only as a starting point for research, but below I’ve added a quick pen portrait summary of each fund. The usual caveats apply: these funds are complex, pricing can be volatile, bid-offer spreads can be wide and you need to be adventurous enough to do your own research. Most of the funds also trade at chunky discounts to their net asset value.

TwentyFour Income. This well-established, decent-sized fund invests in asset-backed, mortgage-related securities. Its track record is solid if unspectacular, churning out an annualised 8% return since inception, and its yield is a sustainable 9.3%. It recently declared its final dividend of 5.07p, bringing the total for the year to 11.07p (FY24: 9.96p), a record balance and full-year dividend. The company currently pays shareholders 2 pence/quarter, in line with its target for the year, with the final balancing dividend announced after the 31 March year-end. So, what does TwentyFour Income invest in? In straightforward terms, this London-listed fund targets less liquid, higher-yielding UK and European asset-backed securities (ABS). This part of the fixed-income market remains largely overlooked, and fund managers believe it represents attractive relative value.

BioPharma Credit. A truly unusual fund, but one with an excellent track record – and big enough to provide real liquidity for investors. BioPharma lends money mostly to publicly listed life sciences businesses struggling to raise equity funding (pretty much all listed biotechs struggle to raise equity capital) to help fund obvious growth opportunities i.e launching a new suite of drugs or medical products. BioPharma lends the money at decent rates – nearly always in the double digits and then sits senior in the capital structure. Crucially, though it has a fantastic track record of getting its money back – too many loan funds have sunk because of high default rates. Many of BioPharma’s borrowers, by contrast, pay the money back early, because of a takeover. That triggers early repayment fees, which add to the total return. It also helps that BioPharma has a very active discount control mechanism designed to get a discount below 5% as quickly as possible.

CQS New City High Yield. Managed by Ian ‘Marco’ Francis at CQS, this corporate bond fund has a long track record and a very loyal fan base amongst wealth managers. Like its nearest peer Invesco Bond Income Plus, it buys into higher-yielding corporate bonds but is careful about what it buys. Ian has a focus on providing investors with a high dividend yield, achieved through a diversified portfolio of 140 holdings predominately in high yield. Fixed Income represents 75% of assets, with 25% in Convertibles, Equities and Preference shares. Helpfully the fund has traded either at par or at a premium for much of its life.

Fair Oaks Income. This investment is more for experienced investors who understand structured finance, particularly collateralised loan obligations (CLOS). Fair Oaks focuses on debt structures where the riskiest layer, equity, is positioned below a series of risk-rated loans, starting with the safest AAA-rated loans. That sounds risky and in a deep recession it might well prove to be, but because the manager frequently sponsors and manages the pool of loans via a CLO, it understands the risk profile of the borrowers very well. And to date, its returns have been very impressive. Declining interest rates, perhaps because of a slowdown, could be a double-edged sword. It could lower the risk of defaults and prompt more refinancing. Still, it could also imply an impending recession in which those defaults (currently very low) could erupt into a financial crisis. But to date, Fair Oaks has navigated higher rates for a longer environment very well, and this is a hugely popular fund with many wealth managers.

Sequoia Economic Infrastructure. This lending fund invests in infrastructure debt. SEQI’s portfolio is invested across 54 private debt investments (91% of the portfolio) and five infrastructure bonds. 60% of the portfolio comprises senior secured loans, and the portfolio has an annualised YTM of 9.87%, alongside a cash yield of 7.29% (excluding deposits). The weighted average portfolio life is 3.4 years, and the manager reckons that the short duration means that SEQI can take advantage of higher yields in the current rate environment. A few loans have defaulted, which has caused the share price to fall quite a bit in recent weeks – the shares currently trade on a c.17% discount, yielding 9.0%. Wealth managers widely hold the fund and it boasts a very active approach to portfolio valuation, with monthly third-party valuations. I sense that there’s limited downside given the fund’s active buyback policy.

David Stevenson

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.

One bright spot might be income – as share prices move up and down violently, the attractions of a regular income via dividends start to become more attractive. According to Octopus Investments’ bi-annual Dividend Barometer private investors should consider UK small and mid-cap companies for income.

Sticking with that dividend income theme, investment trusts that pay a regular dividend might also be looked on more favourably—there’s a long tail of deeply discounted trusts that have a long track record of paying generous dividends, based in part on strong cashflows and built-up shareholder reserves (which allow investors to smooth out the payout).

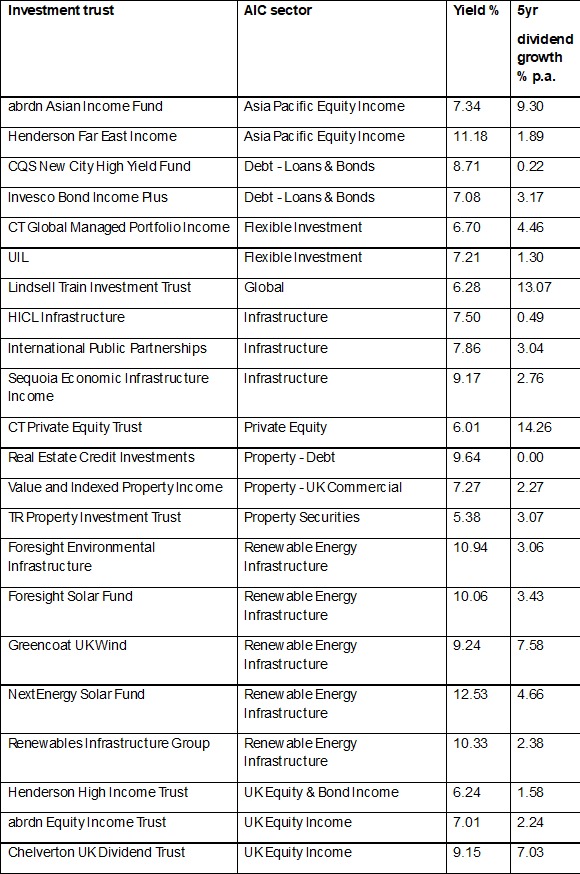

The Association of Investment Companies (AIC) has just released a useful list of 26 investment trusts that pay a yield of more than 5% and have not cut a dividend in the past ten years. That includes five trusts from the Renewable Energy Infrastructure sector, with yields ranging from 9.2% to 12.5%

Consistent income payers with yields of more than 5%

Low-volatility funds are providing respite

The focus on dividend income reflects an obvious truth – share prices might shoot up and down, but dividend cheques tend to pay out a stable amount. We’ll come back to that income point shortly, but what about the volatile share price bit of the equation? Is it possible to dial down the share price volatility by investing in shares through a fund like an exchange-traded fund (ETF) that only invests in more defensive, less volatile stocks? The answer is yes, and much of the time it’s a very successful wealth preservation strategy.

A good few years back, there was a sudden eruption of interest in what was called smart beta strategies. It sounds complicated, but it isn’t. Essentially, it’s saying you have two ways of passively tracking the (stock) market. The first is to buy into a tracker following a major index like the S&P 500 and be done with it!

The alternative is to say that the crowd, and thus markets, are not always perfectly efficient and that at some points, the market overindulges some trends (positive momentum stocks) and ignores others (value stocks). This gives rise to various market anomalies, as they are called, which range from value stocks through quality stocks to low-volatility strategies. These strategies all involve using technical and fundamental metrics to spot stocks that might be underappreciated and priced inaccurately by the market.