A £100,000 pension pot could now secure a significantly higher income in retirement, as improved annuity rates offer better value for those seeking guaranteed lifelong payments.

The latest data shows a 65-year-old with a £100,000 pension pot can secure an annual income of up to £7,814 from a single life level annuity with a five-year guarantee. This compares to just £5,724 per year from an annuity that increases by three per cent annually.

This substantial difference of over £2,000 per year in initial income explains why level annuities remain the most popular choice among retirees. The immediate financial benefit is compelling, particularly for those prioritising higher income in the early years of retirement.

The vast majority of annuity purchases are level products that don’t increase over time, according to Hargreaves Lansdown.

Pensioners face a crucial decision when purchasing annuities, with new data revealing stark differences between level and inflation-linked options.

The choice between higher initial income or inflation protection represents one of the most important financial trade-offs for retirees.

While level annuities offer substantially more income in the early years of retirement, inflation-linked alternatives provide increasing payments that may prove valuable over a potentially lengthy retirement period.

This decision has long-term implications for pensioners’ financial security and purchasing power.

Helen Morrissey, head of retirement analysis at Hargreaves Lansdown, cautions against focusing solely on initial income.

She said: “However, with retirement potentially lasting twenty years or more the issue of inflation does need to be taken into account.

If you take out an annuity, you have to hand over all your hard earned.

It’s a gamble with your future as you do not know what interest rates will be when you wish to retire. If you were unlucky, you could be offered

Canada Life figures show the 65-year-old with a £100,000 pension pot could buy an annuity linked to the retail price index (RPI) that would generate a starting annual income of £3,896. That’s up from £2,195 in the New Year following a 77% spike in rates this year. Oct 22

Don’t let that be you, unless when you retire interest rates have spiked and then it could be an option.

Michael Foster, Investment Strategist Updated: May 19, 2025

Can we still call ourselves contrarians if we buy into “mainstream” trends like the stunning growth of AI? Of course we can.

Today we’re going to do just that. But of course we’re not picking up obvious names like NVIDIA (NVDA). Instead we’re looking to an 8%-paying fund I see having even more upside than the “go-to” AI stocks everyone else is buying.

For Profitable Contrarian Investing, Think “Oblique,” Not “Direct”

The technique we’re going to use here is a very underappreciated concept called “oblique investing.”

Sounds a bit dry, I know, but it’s anything but. The idea here is, roughly speaking, to invest in big forces driving the market and shifting the economy over the foreseeable future.

Obvious, right? There’s more here, though, because, of course, doing this directly by investing in the trend itself means you’ll likely overpay, since the market has already picked up on it.

So instead, we’re going to look to stocks (and funds!) that are well-positioned to ride the trend higher but aren’t the obvious names in their sectors.

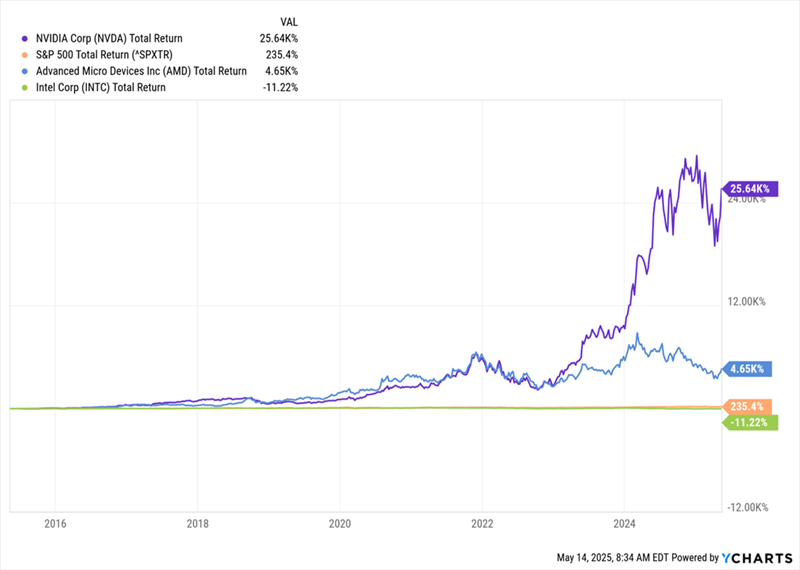

NVIDIA Was a Prime “Oblique” Investment in the Last Decade …

It’s best to look at this through an example: In the mid-2010s, technology’s rise to dominance over other sectors was a clear trend. So anyone who bought the “big three” semiconductor stocks—NVIDIA, Advanced Micro Devices (AMD) and Intel (INTC)—would have easily beaten the S&P 500 on average.

Buying the Trend Pays Off Handsomely

As we can see, big gains from AMD (in blue) and NVIDIA (in purple) more than offset losses on Intel (in green).

However, back then, buying NVIDIA, which was best known for making graphics cards for gamers, seemed like a losing move compared to Intel, which made the CPUs in almost every computer. Even Apple (AAPL) had switched to Intel processors.

In other words, the “obvious” investment in the future did not play out, while the closely related, but not directly plausible—or “oblique,” if you will—story did play out.

… But It’s Anything But Today

Fast-forward to today and we’re looking at another trend in the process of rewriting tech—and many aspects of society as a whole: AI.

Here too, NVIDIA is the major player, with its chips powering the AI trend, much like Intel’s chips powered the rise of tech more generally in the 2010s.

Thanks first to its gains from powering the tech sector and then to its AI dominance, NVIDIA has grown to become the second-largest stock in the S&P 500. The numbers are staggering: Over the last 10 years, NVIDIA went from being 0.063% of the S&P 500 to 5.8% now.

And as I write this, following the tariff selloff, investors are starting to turn back to the story of US economic growth driven by, you guessed it, technology such as AI.

And so NVIDIA is starting to recover, but its ceiling is much lower than it was in the past. It’s already risen some 25,000%+ in the last 10 years, and another 25,000%+ gain over the next decade is simply not in the cards.

Where does that leave us? Obviously, we want to invest in AI’s ongoing growth, but we don’t want to get into a crowded trade.

Enter AIO: A Top “Oblique” AI Pick

That brings me to a closed-end fund (CEF) called the Virtus Artificial Intelligence & Technology Opportunities Fund (AIO), which we once held in my CEF Insider service. CEFs are, of course, wildly underappreciated, so to say AIO is “oblique” compared to NVIDIA might be the king of understatements!

Nonetheless, this 8%-yielding fund (more on the payout in a moment) does hold NVIDIA, so we get some exposure to the company’s ongoing growth (which will continue, even if it doesn’t hit those 25,000% gains of the past). We’re getting the other “usual suspects” in AI, too, including Meta Platforms (META).

But the real key to AIO’s “oblique” appeal is that it also holds firms that benefit by using AI in their day-to-day businesses, like drug maker Eli Lilly & Co. (LLY), insurer Progressive Corp. (PGR) and heavy-equipment maker Deere & Co. (DE). Firms like these are key to profitable AI investing because it’s likely to be the users of this tech—not the providers—that reap the biggest profits from it.

While it’s best known for its chatbot, AI leader OpenAI also has many enterprise clients, including John Deere.

In short, Deere uses AI to make its products more efficient, such as its herbicide spray, which uses fewer chemicals than competitors’ offerings. That results in healthier, cheaper products, said Justin Rose, Deere’s president of lifecycle solutions, supply management and customer success, in his recent conversation with OpenAI. (If you’re into farming, the entire interview is worth reading.)

Of course, these are far from obvious cases of AI integration, so they’re not priced into stocks like Deere yet, and that is exactly why AIO is holding them. Same goes for Progressive using AI to lower its marketing costs and Eli Lilly using AI to discover new drugs. AIO is collecting these “hidden” AI plays for investors to hold for the long haul.

Finally, there’s that 8% dividend, which has held steady since AIO’s launch. Investors have picked up a couple of nice special dividends, too.

This, by the way, is yet another benefit of “oblique” CEFs: high (and often monthly paid) dividends you have zero hope of getting from a mainstream tech name like NVIDIA.

What Investors Get Wrong About CEF Fees (and Miss Out on 8%+ Yields)

Michael Foster, Investment Strategist Updated: May 26, 2025

Plenty of investors miss out on the huge yields (often north of 8%) that closed-end funds (CEFs) offer. There’s one simple reason why: They get way too hung up on management fees.

We’re going to look at a few reasons why that is today—and one easy way you can make those fees disappear entirely.

But first, just how high are the fees we’re talking about? Well, the average fee for all CEFs tracked by my CEF Insider service is 2.95% of assets. In contrast, the largest ETF on the planet, the SPDR S&P 500 ETF Trust (SPY), has a fee of just 0.09%.

So, to be sure, we are talking about a big gap here.

But although CEFs’ fees are much higher, there are many reasons why we shouldn’t put too much weight on them when making buying decisions. Let’s talk about those now.

CEFs Let Us Diversify—and Get Smart, Active Management

SPY holds every stock in the S&P 500—in other words, the 500 large-cap companies that represent the biggest public firms in America. And while these stocks do well in good times, they can have rough runs, like we saw in April, for example.

That’s why we want to make sure we’re investing in assets beyond stocks, like corporate bonds. CEFs let us do that, and they give us access to smart human managers (not to mention high dividends), too.

An actual person at the helm is vital in a lot of these asset classes, and in particular corporate bonds, because deep connections are key to getting access to the best new issues.

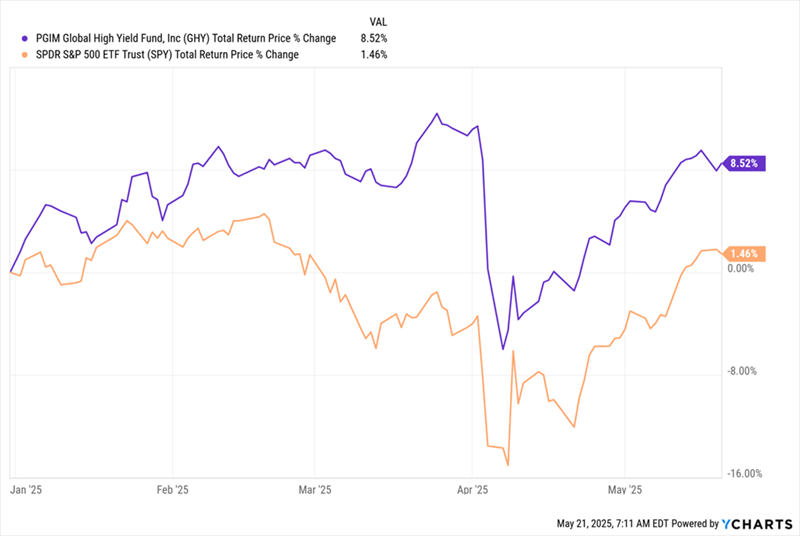

We all know deep down that diversification works. But using CEFs to do it really can take things to another level, thanks in part to their high dividends. Look at the performance of the PGIM Global High Yield Fund (GHY), in purple below, since the start of 2025 to the time of this writing. GHY is a CEF Insider holding that yields an outsized 9.8%.

GHY Is the Poster Child For CEF Diversification

As you can see, GHY outran SPY (in orange) while diversifying its shareholders beyond stocks and the US, too. In addition, the bond CEF barely fell below breakeven in April, while stocks were down 15%.

And bear in mind, as well, that these numbers are net of fees. Speaking of which, GHY’s fees are far higher than those of SPY (1.5% of assets compared to 0.09%)

All that said, some CEFs do focus on S&P 500 companies, and still have higher fees, which brings me to my second point…

CEFs Have a Wide Range of Fees

GHY, as mentioned, has total expenses of 1.5%, better than the CEF average but still quite high. Compare that to the Nuveen S&P 500 Dynamic Overwrite Fund (SPXX), an S&P 500–focused CEF whose fees are much less, at 0.97%.

But wait, if SPXX is focused on US large caps, why are its fees around 10 times those of SPY? It’s largely because SPXX also sells call options on its holdings—or rights for investors to buy them at a fixed date and price in the future. The fund gets paid for these rights (and uses those fees to help fund its 7.7% dividend).

There’s some cost and work attached to that strategy, hence the higher fees. But it’s a small price to pay to get a dividend that’s nearly six times that of SPY.

CEFs Offer Higher Income

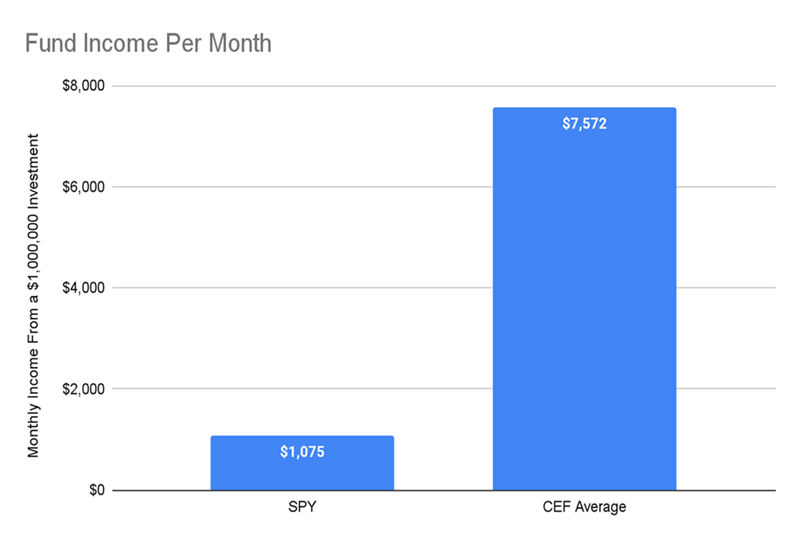

Currently, all CEFs covered by CEF Insider have an average yield of 9.1%, while SPY, as mentioned, yields 1.3%. In other words, a million dollars spread across all CEFs would get you over $90,000 in annual income, or $7,572 a month, versus less than $13,000, or about $1,075 monthly, from SPY.

Source: CEF Insider

This is why many investors use CEFs to fund an early, or partial, retirement; if it takes $682,286 in savings to replace the average paycheck in America (as measured by the Bureau of Labor cs’ median weekly earnings survey) CEFs but a staggering $4.8 million saved with SPY, you can see why CEFs could attract more attention—and thus, CEF issuers can charge higher fees.

CEF Discounts Can Make Your Fees Vanish

Now, here’s the kicker: CEFs have an unusual structure that means they often trade for less than their assets are actually worth.

Let’s say you have a CEF that has $100,000 spread across shares of NVIDIA (NVDA), Apple (AAPL) and Amazon.com (AMZN), among others, and the CEF has 10,000 shares in total. Each share is worth $10. Easy enough.

But CEFs are, as the name says, closed. That means CEF issuers can’t issue new shares to new investors, so all of the shares trade on the public market, like stocks, and their market prices fluctuate based on investor demand, sometimes diverging from the actual value of the underlying holdings.

If that demand is higher than the actual market value of the CEF, it’ll trade at a premium to its portfolio’s net asset value, or NAV; if lower, it’ll trade at a discount.

On average, CEFs trade at a 6% discount, according to CEF Insider data.

So if your CEF trades at a discount wider than its annual management fee, the discount can effectively offset the cost of that fee. And bear in mind that some CEFs are steeply discounted, with discounts of 10% or more.

It’s worth pointing out that the fees are taken out of the CEF’s portfolio by managers automatically as a matter of course; investors don’t have to mail off a check.

Let’s wrap with a quick recap, then: CEFs give you access to discounted, high-quality assets, far higher income than most ETFs, and they give you a high-income, low-cost way to diversify, too.

Plus, the best CEFs outperform their benchmarks—including the S&P 500. This is why CEFs are a passive income weapon that many wealthy investors are happy to keep in their arsenal.

As we just saw, most investors avoid CEFs because they think the fees are too high.

Big mistake. It means missing out on much higher yields than you’d get on garden-variety ETFs like SPY—often 7%, 8%, even 9%+. Plus, as we just discussed, many CEFs also trade at steep discounts that can cancel out those fees.

Good day!Meet your filing deadlines for excise tax return UAE with our professional support. Avoid penalties and ensure accuracy every quarter. We file your excise tax return UAE through the official FTA system. Trust us to manage your obligations. Contact us before your next deadline. All information is available via the link – https://telegra.ph/Excise–Other-Taxes-in-the-UAE-04-16VAT on medical services in UAE is mostly exempt but some supplies are taxable. Healthcare providers should check VAT on medical services in UAE rules carefully. Consulting VAT experts helps manage VAT on medical services in UAE. Avoid mistakes in VAT on medical services in UAE. Stay compliant with VAT on medical services in UAE. All information is available via the link – https://telegra.ph/VAT-Services-in-the-UAE-04-16 tax uae 2025 on tourism services, open bank account uae non resident, how can i open a bank account in uae car services have vat in uae, documents to open bank account in uae, uae tax registration service Good luck!

Capital expenditure programme update and highlights:

As previously announced the Company has identified c. 20 sites where there are clear value add opportunities. These may include planning applications being submitted to change the use to alternatives such as student accommodation, residential or hotel use ahead of a sale, to maximise value for shareholders. It is anticipated that this programme will deliver good shareholder value over the medium term.

In addition, currently the total capital expenditure investment amounts to £23.9m:

· 11 capital projects underway for £8.5m

· 9 projects scheduled to commence on-site works by the end of H1 ’25 for £6.4m

· 10 projects that have been identified for £9.0m

Q1 2025 Dividend Declaration

The Company declares that it will pay a dividend of 2.50 pence per share (“pps”) for the period 1 January 2025 to 31 March 2025, (1 January 2024 to 31 March 2024: 1.20pps**). The entire dividend will be paid as a REIT property income distribution (“PID”).

As you can see from the Level 2 table above the spread can widen alarmingly. Current quote xd on the 22/05 payable 11/07

You can normally deal within the spread but if the brown stuff hits the fan you would be locked into the position, so the dividends would be crucial to you holding on.

Current expected dividend 10p. Current price to buy 115p a yield of 8.75%

abrdn Equity Income Trust PLC ex-dividend date abrdn European Logistics Income PLC ex-dividend date Alliance Witan PLC ex-dividend date Downing Renewables & Infrastructure Trust PLC ex-dividend date Fair Oaks Income Ltd ex-dividend date Fair Oaks Income Realisation Ltd ex-dividend date Great Portland Estates PLC ex-dividend date Henderson European Trust PLC ex-dividend date LondonMetric Property PLC ex-dividend date Premier Miton Global Renewables Trust PLC ex-dividend date Social Housing REIT PLC ex-dividend date Temple Bar Investment Trust PLC ex-dividend date

As with many lists, errors can occur, so check the dates before pushing on any Trust.

A rebound in UK’s commercial property – should you invest?

UK commercial property’s three-year bear market finally appears to be over, says Max King

(Image credit: Getty Images)

By Max King

published 4 days ago

It has been a long winter for the UK’s commercial property sector, but at last it seems spring is in the air. Savills reports the vacancy rate in the City and West End of London office property market has fallen from a peak of 9.5% in late 2023 to 7.4%, although it is still comfortably above the long-term average of 5.9%.

The rate of growth in online shopping has slowed to the mid-30s in percentage terms, including food, and shopping centres have learned to adapt. Customers see them as a destination. They want to browse in shops, visit cafes and restaurants, and go bowling. Retailers have learned that returns from online shoppers are expensive to handle, so shops are now not just sales outlets, but also showrooms for buying online.

In late 2024, Land Securities paid £490 million for the Liverpool One shopping centre, “one of the premier shopping centres in the UK”, it says. It expects to generate an income return of 7.5% and to grow that figure “meaningfully” over the next few years.

Stay ahead of the curve with MoneyWeek magazine and enjoy the latest financial news and expert analysis, plus 60% off after your trial.

A lot of capital has gone into “big-box” distribution hubs, so rental growth is likely to slow in that subsector, says Nick Montgomery, the manager of the Schroder Real Estate Investment Trust (LSE: SREI). But there is a supply shortage of estates with multi-let industrial and distribution units. Meanwhile, the market for the “alternative” property sector, including hotels, self-storage, residential and student accommodation, is mostly healthy.

“There have been plenty of false dawns since the market peaked in late 2022,” says his colleague Richard Gotla, “so it feels a bit like Groundhog Day.

Values have fallen 20%-25% since the peak – less than the 40%-45% [in 2009], but there has been less debt in the sector than then. In addition, rental values were flat then but have risen 10% since late 2022.”

London has returned to the office

Gotla says that “the big story is how little development there has been in recent years”, although it doesn’t seem that way in central London. The return to the office has been more advanced in London than in the regions, but the demands of occupiers have changed. Tenants want more facilities, better energy efficiency and cafes, rather than a small kitchen with a kettle, a microwave and a vending machine.

However, construction costs have gone up sharply, and buildings quickly become obsolete: “they start to depreciate when the builders leave”, says Gotla. With initial rent-free periods of up to three years, leases of up to ten and obsolescence thereafter, “it has become very difficult for developers to make the numbers work”. As a result, rents “are going nuts: £150 per square foot in the City, £250 in the West End”.

This is pulling up the secondary market. Refurbishing a quality building in a good location is much cheaper, allowing landlords to offer shorter leases (around five years) at far lower rents. Refurbishments comprise a large part of Derwent London’s (LSE: DLN) portfolio, and it reports strong demand from tenants. The shares trade on a discount to net asset value (NAV) of 40%.

The shares of Great Portland Estates (LSE: GPE) trade on a discount of 30%, the trust having diluted NAV with a £350 million rights issue at a discount in May 2024. Such issues are never popular with investors, but they reflect managements’ enthusiasm about the outlook. In April, Norway’s sovereign wealth fund paid £570 million for a 25% stake in Shaftesbury Capital’s Covent Garden estate, validating its NAV and reducing its debt. The shares have since risen over 20%, but still trade at a discount of 30% – despite reporting strong performance last year with rental income up 6% and earnings 20% from its West End estate, primarily retail and leisure properties.

Sector giant Land Securities (LSE: LAND), with £10 billion of assets and a 30% discount to NAV, has been adding to the retail segment of its portfolio. Rival British Land (LSE: BLND), with £8.7 billion of assets, has focused on “campuses” such as Broadgate and Canada Water. These encompass offices, but also retail and leisure outlets, and the public spaces in between. A quarter of its assets are in retail parks and 10% in shopping centres. Its shares are on a discount of 30%.

SREI is much smaller, with net assets of £300 million, so it is not going to own any trophy assets. But its smaller size enables it to look for value in areas the larger investors ignore. Its shares trade at a 20% discount, but the yield, close to 7% and fully covered by earnings, is attractive. Moreover, rental income of £30 million is well below “reversionary rent” of £40 million – the rent its properties would command if re-let now. Less than 10% of the portfolio is in London and over 40% in the North, while multi-let industrial accounts for half the portfolio, offices a quarter and retail warehouses half of the rest. Although its debt is significant, 75% of it is locked in for 11 years at a cost of just 2.5% a year, so it has been little affected by higher rates, but will benefit markedly from an improving market.

Schroders forecasts a total annual return of 8%- 10% for UK real estate over the next four years, which would ensure both higher dividends and capital appreciation. The group is keen to add value to the portfolio from repurposing units on its estate and redeveloping tired buildings. Montgomery also sees opportunities in affordable housing in the inflation-linked income from hotels, “but it is more interesting to be an owner and operator than just an owner”.

Sentiment in the property market is vulnerable to higher gilt yields and global factors, he warns, but with interest rates likely to trail lower, there should be a recovery. “With a shortage of supply, we don’t need a surge in demand to see decent returns.” Share prices in the sector have started to discount such a recovery, but there should be much more to go for.

This article was first published in MoneyWeek’s magazine. Enjoy exclusive early access to news, opinion and analysis from our team of financial experts with a MoneyWeek subscription.

Belt and Braces Trusts, you would have earned above market dividend yields as you waited for the market to correct. If you can buy a pounds worth of physical assets at a discount and still receive income, it’s quite a compelling case.

If you are lucky and your Trust gets a bid, you can take your profit and try to do it all over again, shorting your time frame, the only shorting the blog recommends, if not you can re-invest the dividends back into your Snowball. As the prices rose the yields fell so not so many compelling Trusts left.

Howdy would you mind letting me know which web host you’re using? I’ve loaded your blog in 3 different browsers and I must say this blog loads a lot quicker then most. Can you suggest a good internet hosting provider at a reasonable price? Many thanks, I appreciate it!

WordPress via FastHosts, they offer a discount deal for the first few months.

When CTY fell to 300p the dividend was 19p. The buying yield 6.3p, with the current dividend 20.6p a gentle increase, you will receive the buying yield as long as you own the Trust, assuming the dividend isn’t cut.

The current price 473p a running yield of 4.35%, the price including earned dividends but not re-invested back into CTY 566p.

With the benefit of good ole hindsight, if the dividends had been reinvested back into CTY the price would be 600p.

In a few short years you would have achieved the holy grail of investing in that you could take out your stake and invest it in another high yielder and receive income at zero, zilch risk from a share in your Snowball.

Everything crossed for another market crash ? If not given time the share could double again, you could even take the risk of re-investing the dividends from CTY back into the trust, especially if the price had fallen.