High-dividend ETFs offer instant diversification and potential income.

The investing information provided on this page is for educational purposes only. NerdWallet, Inc. does not offer advisory or brokerage services, nor does it recommend or advise investors to buy or sell particular stocks, securities or other investments.

Updated May 21, 2025

Fact Checked

Written by Alana Benson

Lead Writer+ more

Reviewed by Tiffany Kent

Certified financial planner

Edited by Arielle O’Shea

Head of Content, Investing & Taxes

Co-written by Kevin Voigt

Contributing Writer

Dividends can be a powerful source of income, and during times of stock market volatility, dividend-paying companies may even be more stable than their growth-stock peers. To generate income, some investors harness dividends by investing in dividend stocks individually, but there’s another option for those who want to save some time and energy: high-dividend ETFs.

7 high-dividend ETFs

Below is a list of seven large-cap U.S. dividend ETFs, ordered by annual dividend yield. Note that some high dividend ETFs may come with higher risk (rather than the stability some dividend investors are looking for). Always read the fine print, investigate dividends that seem too good to be true and look at the components of the ETF to determine if it fits in your portfolio.

The best high-dividend ETF is Invesco KBW Premium Yield Equity REIT ETF (KBWY), which currently has a dividend yield of 9.93%. This is based on our screen of U.S. equity ETFs, which excludes inverse, leveraged and actively managed ETFs and any with expense ratios over 0.5%.

Ticker

Company

Dividend Yield

KBWY

Invesco KBW Premium Yield Equity REIT ETF

9.93%

XSHD

Invesco S&P SmallCap High Dividend Low Volatility ETF

7.48%

NUDV

Nuveen ESG Dividend ETF

5.66%

DIV

Global X SuperDividend U.S. ETF

5.61%

SPYD

SPDR Portfolio S&P 500 High Dividend ETF

4.48%

RDIV

Invesco S&P Ultra Dividend Revenue ETF

4.15%

SCHD

Schwab US Dividend Equity ETF

3.96%

Source: Finviz. ETF data is current as of May. 21, 2025, and is intended for informational purposes only.

High-dividend ETFs may generate income

Dividend-paying ETFs can be a great tool for those looking to increase cash flow and diversify their investments. They offer a simple solution to getting exposure to a specific investing niche — in this case, stocks that pay a regular dividend.

You can use those dividends to pad your income as many retirees do. You can also reinvest those dividends back into the fund to better take advantage of compound interest and grow your investment portfolio. Whatever you choose, dividend-paying ETFs make it easy to add a large variety of investments to your portfolio all at once.

9 Highest-Yielding Monthly Dividend Stocks for May

Monthly dividend stocks like ARR and AGNC can provide investors with frequent payments — but those payments aren’t always sustainable. Here’s what to know.

The investing information provided on this page is for educational purposes only. NerdWallet, Inc. does not offer advisory or brokerage services, nor does it recommend or advise investors to buy or sell particular stocks, securities or other investments.

Updated May 2, 2025

Written by Sam Taube

Lead Writer

Edited by Chris Davis

Managing Editor

Nerdy takeaways

Monthly dividend stocks are shares of publicly-traded companies that pay dividends on a monthly frequency.

Many monthly dividend stocks have potentially-unsustainable dividends, and may not be able to continue their payouts indefinitely.

Some ETFs pay dividends monthly, although they may not be composed of monthly dividend stocks.

After years of high inflation, many Americans — retirees in particular — could use a little extra cash every month. Monthly dividend stocks are one investment that can provide it. And for dividend investors, there’s even a silver lining to the stock market volatility we’ve seen in 2025: it has pushed the yields on many dividend stocks up into the double-digits.

Top 9 monthly dividend stocks by yield

Below is a list of the 9 highest-yielding monthly dividend stocks with market capitalizations of at least $1 billion and payout ratios below 100%, meaning they are paying out less in dividends per share than they are bringing in in earnings per share (EPS).

They are ordered by forward dividend yield, which is calculated by dividing the sum of a company’s projected dividend payouts over the next year by its current share price.

Tip: You can use the dividend yields below to fill out our dividend calculator and estimate future gains for a particular stock.

Company name

Forward dividend yield (annual)

Armour Residential REIT (ARR)

17.52%

AGNC Investment Corp. (AGNC)

16.25%

Ellington Financial (EFC)

12.01%

Apple Hospitality REIT (APLE)

8.07%

EPR Properties (EPR)

7.09%

Realty Income Corp. (O)

5.63%

Main Street Capital Corp. (MAIN)

5.62%

SL Green Realty Corp. (SLG)

5.60%

Stag Industrial, Inc. (STAG)

4.41%

Source: Dividend.com. Stock data is current as of May 2, 2025, and is for informational purposes only.

What are monthly dividend stocks?

Monthly dividend stocks are a subcategory of dividend stocks: shares of publicly-traded companies that pay a portion of their profits to shareholders.

Many dividend stocks pay out dividends quarterly or annually, but monthly dividend stocks, as their name implies, pay out every month.

Pros and cons of monthly dividend stocks

The biggest advantage of monthly dividend stocks is the frequent, and often substantial, payments they provide. Some of the stocks listed above have yields more than twice as high as the 10-year Treasury note. And while Treasury bond holders only get paid twice a year, monthly dividend stock holders get paid every month.

Proposed Asset Realisation Strategy and Change in Investment Management Fee

In the Company’s annual results announcement dated 3 April 2025, the board of directors of the Company (the “Board”) noted that it was examining all options for repaying the trust that the Company’s shareholders (the “Shareholders”) have placed in the Company over the past four years since the Company’s initial public offering (“IPO”). The Board, directly and through its corporate broker, Numis Securities Limited (“Deutsche Numis”) has engaged with a significant proportion of the Shareholders over the past six months. While no one option was favoured by all Shareholders, the feedback from the majority of Shareholders was a desire for the Company to return capital via a sale of the Company’s portfolio of assets (the “Portfolio”) with a view to maximising value. Shareholders were rightly cognisant of the balance between expedited returns of capital and damaging the long-term value of the Portfolio through untimely sales.

As such, the Board today announces that it intends to commence an asset realisation strategy (the “Proposed Asset Realisation Strategy”) which will require a change to the Company’s investment policy. The Proposed Asset Realisation Strategy will involve mandating the Company’s current alternative investment fund manager (“AIFM”), Victory Hill Capital Partners LLP (“Victory Hill”), to sell the Portfolio in a timely manner with a view to maximising value. The Board is firmly of the opinion that it is in Shareholders’ best interests to retain Victory Hill to deliver the Proposed Asset Realisation Strategy. It is with that in mind that the Board has sought to align and incentivise Victory Hill to manage the Portfolio on this basis.

The Board and Victory Hill note that some Portfolio assets are in a better position to be sold than others given their operational maturity. Some Portfolio assets need further management before they can be sold at a value that the Board and Victory Hill believe would be acceptable to Shareholders, although it is also within the Proposed Asset Realisation Strategy for the Company to consider offers for all of the Portfolio assets to be sold as a whole. In any case, the Board anticipates, having taken advice from Victory Hill, that the Proposed Asset Realisation Strategy will be completed in no longer than 3 years, by which point all capital will have been returned to Shareholders, and the Company would de-list and be liquidated (the period running for 3 years from the date that resolutions to be put to Shareholders to approve and implement the Proposed Asset Realisation Strategy (the “Resolutions”) are passed, being the “Realisation Period”). The Board will consider methods to return cash to Shareholders as realisations are made over time. Cash will be returned to Shareholders as and when the Company holds enough cash from the sale of Portfolio assets to justify the cost of effecting a return to Shareholders.

Advantages of the Proposed Asset Realisation Strategy and Change in Investment Management Fee

The Board understands that the persistent deep discount that ENRG’s shares (the “Shares”) trade at relative to its NAV is, in part, an indication that investors currently do not value exposure to uncorrelated, highly cash generative assets, such as those forming the Portfolio. The Board notes that while a minority of Shareholders wish to see the Company continue with its current strategy, the clear majority of Shareholders support an asset realisation strategy such as the one proposed.

The Board believes the Proposed Asset Realisation Strategy and change in investment management fee (described in more detail in the section below) are in the best interests of Shareholders for the further key reasons:

· Satisfying Shareholder demands for return of capital: the majority of Shareholders are as frustrated as the Board with the Company’s Share price discount to NAV. The discount issues are sector-wide and Shareholders are understandably seeking capital returns at the highest achievable value, and in as short a time frame as possible. The Board believes the Proposed Asset Realisation Strategy is the best and most realistic route to this outcome.

· Victory Hill is the right investment manager to deliver maximum returns to Shareholders: the Board believes that Victory Hill is the best investment manager to deliver a successful realisation of the geographically and technologically diverse Portfolio while continuing to manage the Portfolio on a day-to-day basis throughout the Realisation Period. The Board also believes that successful implementation of the Proposed Asset Realisation Strategy will depend on having the support of the operating partners in relation to the Portfolio assets, which is much more likely with Victory Hill’s guidance given their ongoing strategic relationships. Retaining Victory Hill limits any disruption in the asset management progress within the Portfolio and allows the Company to begin the Proposed Asset Realisation Strategy shortly following the required Shareholders’ approvals.

· Victory Hill will be appropriately incentivised to dispose of the Portfolio in its entirety and deliver the highest achievable returns to Shareholders: Victory Hill’s business, like ENRG’s, will fundamentally change as a result of the Proposed Asset Realisation Strategy. The introduction of the Performance Fee (defined and explained in more detail in the section below) clearly aligns Victory Hill’s interests with the Board’s and Shareholders’ to sell the Portfolio in as short a time frame as possible, at the highest possible value within that timeframe. The Performance Fee will only become payable to Victory Hill if the entire Portfolio has been realised (save for any reserved temporary investments) and Shareholders have received their full (net of fees, costs, expenses, taxes, other liabilities and any reserves needed in order to achieve an orderly winding-up of the Company) cash returns above a hurdle rate based on the Company’s NAV, explained in more detail in the section below. The Board believes this reduces the risk of part of the Portfolio remaining unsold at the end of the Realisation Period and incentivises Victory Hill to sell the Portfolio in as short a time period as possible.

· Net returns could represent a material uplift to the current share price: Given Victory Hill is incentivised to aim for asset sales at the highest value possible (see hurdle levels, based on the NAV, in the section below) within the Realisation Period, and the Shares currently trade on a 44% discount to NAV (as at the close of business on 21 May 2025), there is scope for Shareholders to benefit from material share price returns in excess of the current share price if Victory Hill is to achieve a Performance Fee. The Board is hopeful that the Proposed Asset Realisation Strategy could result in a reasonable NAV total return for Shareholders that invested at IPO, albeit not the type of return that it would have initially hoped at IPO and that could potentially be achieved with a continuation of the Company’s current strategy.

Proposed Change in Investment Management Fee

In acknowledging that Victory Hill’s portfolio management role will fundamentally change, the Board has agreed in principle with Victory Hill to revise the fees payable under the alternative investment fund management agreement between the Company and Victory Hill (the “AIFM Agreement”) with effect from the passing of the Resolutions. The general meeting (the “General Meeting”) at which the Resolutions will be sought is expected to be held in August 2025 (see “Expected Timetable” section below). Principally, and as supported by Shareholders’ feedback, the Board believes that the proposed performance fee structure will align Victory Hill’s interests with the interests of Shareholders to complete the Proposed Asset Realisation Strategy whilst seeking the maximum achievable values, at the point of realisation, in a timely fashion.

The key proposed changes to the fees payable to Victory Hill under the AIFM Agreement are set out below and

further detail on proposed changes to the AIFM Agreement will be provided in a circular to Shareholders (the “Circular”) to be published in due course that will convene the General Meeting.

Current investment management fee

Victory Hill currently receives an annual investment management fee calculated as a percentage of the Company’s net asset value (calculated in accordance with the terms of the AIFM Agreement) (“NAV”) as follows:

· 1% on the first £250m of NAV;

· 0.9% on NAV in excess of £250m and up to and including £500m; and

· 0.8% on NAV in excess of £500m,

(the “Current Fee”).[1] The Current Fee is payable exclusive of value added tax.

Proposed investment management fee

The Board is proposing to change the Current Fee with effect from the date that the Resolutions are passed to:

· a base fee (the “Base Fee”) of £4.25m per annum, for the Realisation Period. For the avoidance of doubt, the Base Fee will cease to be payable if the Company terminates Victory Hill’s appointment as AIFM for convenience (i.e. otherwise than for cause) on giving Victory Hill 12 months’ written notice (the “Notice Period”) in accordance with the terms of the AIFM Agreement. For example, if the Company terminates Victory Hill’s appointment in the first year, then Victory Hill will only be entitled under the existing provisions of the AIFM Agreement to receive up to 12 months’ worth of Base Fee and not for the full Realisation Period; and

· a performance fee (the “Performance Fee”) on the terms set out below,

(the Base Fee and the Performance Fee being together the “Proposed Fee”).[2]

The Performance Fee will be the Performance Percentage (defined below) of all realisation proceeds (the “Realisation Proceeds”) of Portfolio assets plus any dividends paid during the Realisation Period that are in excess of a hurdle (the “Hurdle”) based on the proportion of the Company’s most recently published NAV prior to the date that the Circular is published (the “Reference NAV”) applicable to the relevant Portfolio assets. The Hurdle shall apply during the Realisation Period, based on the year during the Realisation Period in which an asset is deemed sold, as follows:

· Year 1: 85% of Reference NAV

· Year 2: 90% of Reference NAV

· Year 3: 100% of Reference NAV.

Performance against the Hurdle will be assessed at the point at which a legally binding contract has been entered into by the relevant member of the Company’s group to dispose of the relevant Portfolio asset.

The Performance Fee will only become payable to Victory Hill (i) if the entire Portfolio has been realised (save for any reserved temporary investments); (ii) if the aggregate amount of Realisation Proceeds returnable to Shareholders (“Total Returns”) are at least 85% of the Reference NAV; and (iii) once Shareholders have received their full (net of fees, costs, expenses, taxes, other liabilities and any reserves needed in order to achieve an orderly winding-up of the Company) cash returns.

The “Performance Percentage” will be:

· 0%, if the Portfolio is not realised within the Realisation Period or Total Returns are less than 85% of the Reference NAV;

· 15%, if Total Returns are equal to or exceed 85% of the Reference NAV;

· 17.5%, if Total Returns are equal to or exceed 90% of the Reference NAV; or

· 20%, if Total Returns are equal to or exceed 95% of the Reference NAV.

The Performance Fee will be calculated and accrued on the earlier to occur of the (i) end of the Realisation Period; and (ii) point at which a legally binding contract has been entered into by the relevant member of the Company’s group to dispose of the final unrealised asset forming part of the Portfolio. The Proposed Fee is payable exclusive of value added tax.

In the event that the entire Portfolio has not been realised at the end of the Realisation Period the Board shall consider at that point what might be best for the future of the Company, which might involve proposals for Shareholders to vote on the continuation of the Company, or to vote on the voluntary liquidation, unitisation, reorganisation or other reconstruction of the Company.

The proposed changes to the fee arrangements within the AIFM Agreement will be deemed a related party transaction under the UK Listing Rules (“UKLR”), and are subject to Shareholders’ approval by ordinary resolution. The Board will also require a fair and reasonable opinion from Deutsche Numis, as sponsor of the Company.

Reasons why the Board believes key elements of the Proposed Fee are in the best interests of Shareholders

· 3-year time horizon balances objectives: the Board and Victory Hill believe that certain assets in the Portfolio may be sold at a suitable value much sooner than 3 years. However, given the Company’s assets are at different stages of operational maturity, it is likely that some assets may take up to 3 years to sell at a price that would satisfy the Board’s view of value. The 3-year time horizon should allow Victory Hill to manage the assets into a sales process considerately without immediately becoming a ‘forced seller’. The Board and Victory Hill are confident that the Portfolio can be realised over a period of 3 years without exposing Shareholders to new asset-specific risks. The Board, as advised by Victory Hill, believes that a shorter time period than 3 years, is likely to lower the anticipated risk-adjusted return to Shareholders.

The current list for a replacement share for VPC, has ENRG sailed without the Snowball onboard ?

PERSONAL FINANCE Dividend ETFs Explained: A Smart Way to Earn While You Invest

Dividend ETFs offer steady income through regular payouts while maintaining diversification They are ideal for passive investors seeking long-term growth and consistent returns. Dividend ETFs reduce risk by spreading investment across multiple companies that share profits.

Generating passive income while building long-term financial security is one of the most appealing goals for investors. For those looking to strike a balance between portfolio growth and cash flow, dividend exchange-traded funds (ETFs) offer an efficient, low-maintenance solution

Unlike traditional stocks, which may or may not provide dividends consistently, dividend ETFs focus specifically on income-producing assets. They give you exposure to a wide variety of companies that share profits with investors, without the complexity of analyzing individual stocks.

Whether you’re planning for retirement, diversifying your income sources, or looking for a less volatile investment path, dividend ETFs combine income generation, diversification, and simplicity all through a single investment.

What Are Dividend ETFs? Dividend ETFs are investment funds traded on public stock exchanges, designed to hold a basket of companies that regularly pay out dividends. These are typically large, established businesses with healthy cash flow, a history of profitability, and a commitment to shareholder returns.

Rather than picking and managing a handful of dividend-paying stocks, an ETF allows investors to gain exposure to dozens (or even hundreds) of such companies through one purchase. These funds are usually built around criteria like dividend yield, payout consistency, and dividend growth history.

How They Work Investors buy shares of the ETF, just like they would with individual stocks.

The fund invests in companies known for paying dividends.

As those companies distribute dividends, the ETF collects them and passes the income to shareholders, often quarterly.

This model creates a reliable stream of income while offering the liquidity of stocks and the diversification of mutual funds.

Benefits of Dividend ETFs Dividend ETFs provide a wide range of benefits, particularly for investors focused on long-term wealth building with an income component. Here’s a closer look at what makes them so appealing:

🟩 1. Consistent Cash Flow One of the biggest attractions of dividend ETFs is the predictable income stream. Whether you’re living off your investments or simply reinvesting the payouts, knowing that money is coming in on a regular basis often quarterly adds financial stability.

🟦 2. Built-In Diversification Buying one dividend ETF can give you exposure to hundreds of companies across different sectors. This reduces your dependence on the performance of any single company, helping cushion losses if one stock underperforms.

🟨 3. Lower Volatility and Higher Resilience Dividend-paying companies tend to be more mature and financially sound. This makes them less sensitive to market swings and more likely to hold their value during downturns. Investors often view these companies as “defensive” holdings.

🟧 4. Compounding Returns Through Reinvestment If you choose to reinvest the dividends automatically, you can benefit from compound growth earning returns on your returns. Over time, this can significantly enhance your total wealth, especially if you’re investing over decades.

🟫 5. Minimal Fees and Easy to Manage Most dividend ETFs charge low expense ratios, especially compared to actively managed mutual funds. Plus, they require no stock-picking or regular monitoring, making them ideal for “set it and forget it” investors.

Real-World Examples and Strategies 🔹 Top Dividend ETFs Vanguard Dividend Appreciation ETF (VIG) Focuses on U.S. companies that have increased dividends for at least 10 consecutive years. Ideal for conservative investors seeking quality and consistency.

iShares Select Dividend ETF (DVY) Targets high-yield dividend stocks across various sectors. Good for investors prioritizing immediate cash flow.

Schwab U.S. Dividend Equity ETF (SCHD) Blends strong performance, stable dividends, and low fees. Known for its robust methodology and long-term reliability.

Global X SuperDividend ETF (SDIV) Invests in high-yield companies worldwide. Offers global diversification with a focus on monthly income.

SPDR S&P Dividend ETF (SDY) Includes companies from the S&P 1500 that have raised dividends consistently for 20+ years. Strong for long-term dividend growth.

Potential Strategies: Build a Core Portfolio Foundation Select 1–2 high-quality dividend ETFs and make them the centerpiece of your investment plan. This creates a strong, income-focused base for your portfolio.

Blend Yield with Growth Combine high-yield ETFs with dividend-growth ETFs to balance current income with future appreciation.

Use DRIP (Dividend Reinvestment Plans) Instead of withdrawing the dividends, enroll in an automatic reinvestment plan to grow your holdings over time and accelerate compounding.

Global Diversification Don’t limit yourself to domestic ETFs. Adding international dividend funds can hedge against country-specific risks and provide additional opportunities.

Rebalance Periodically Review your holdings annually to ensure the fund’s dividend focus and underlying companies still align with your goals and risk tolerance.

Risks and Considerations Although dividend ETFs are generally considered conservative, they are not without risks. Here are a few points to keep in mind:

⚠️ 1. Dividend Cuts or Suspensions Even reliable companies can reduce or eliminate dividends in tough times (e.g., recessions, industry disruptions). This can lower your expected income.

⚠️ 2. Limited Growth in High-Yield Funds Some ETFs prioritize high-yield companies, which may have less room for capital appreciation. These businesses often face slow growth or operate in mature industries.

⚠️ 3. Sector Concentration Many dividend ETFs are heavily weighted toward financials, utilities, or consumer staples industries traditionally associated with dividend payments. This can expose you to sector-specific downturns.

⚠️ 4. Inflation Risk If dividend growth doesn’t keep pace with inflation, the real value of your income can erode over time. That’s why it’s important to consider dividend-growth strategies, not just high yield.

Conclusion Dividend ETFs offer a powerful combination of income, diversification, and long-term potential. They’re an excellent fit for investors seeking steady cash flow without the hassle of managing a basket of individual stocks. Whether you’re in retirement, building wealth, or just beginning your investing journey, they can serve as a reliable building block for any portfolio.

By blending consistency with flexibility, these funds help you stay the course even when markets become turbulent. Source: https://moneypulses.com/dividend-etfs-explained-a-smart-way-to-earn-while-you-invest

The Snowball currently has one ETF in its portfolio, SDIP which pays a monthly dividend which is re-invested back into the Snowball.

The Snowball currently favours a belt and braces plan by investing in Investment Trusts that pay an above market yield trading at a discount to NAV.

If in future, which will most probably be a long time ahead, the discounts narrow, the Snowball may consider buying more ETF’s if they trade above a yield of 7%.

7% is the target as that doubles your income, by compounding, every ten years.

One way of lowering your risk, is to pair trade a high yielder with a Dividend Hero Trust such as CTY, MRCH, etc., a money market account, or a government gilt if trading below it’s issue price and held to maturity.

If you’re seeking closed-end funds (CEFs) with secure yields above 6% in 2025, several options across various sectors offer attractive income opportunities. Here are five notable CEFs to consider:

1. AllianceBernstein Global High Income Fund (NYSE: AWF)

Yield: Approximately 6.9%

Focus: Primarily invests in corporate debt securities, including lower-rated corporate bonds, with a diversified portfolio of over 1,200 holdings.

If you’re seeking investment trusts offering secure yields above 6% in 2025, several options across equity income, infrastructure, and real estate sectors stand out. These trusts combine high dividend payouts with diversified portfolios and, in many cases, a strong track record of consistent income. Here are five notable examples:

Overview: FGEN invests in a diversified portfolio of environmental infrastructure assets, including renewable energy projects across Europe. Its focus on sustainable investments provides both income and growth potential. This is Money+2The Motley Fool+2Barron’s+2

4. SDCL Energy Efficiency Income Trust (LSE: SEIT)

These investment trusts offer attractive yields and have strategies aimed at sustaining income over the long term. However, it’s essential to consider factors such as portfolio diversification, management quality, and market conditions when evaluating these options.

Moody’s Downgrade is Downright Bullish for These Dividends Up to 8.6%

Brett Owens, Chief Investment Strategist Updated: May 21, 2025

As I’m sure you have heard, Moody’s downgraded US debt last weekend.

The stock market panic that ensued lasted for, oh, about an hour of trading.

Why did this already get shrugged off? It’s a classic empty-calorie headline. The practical impact of the downgrade to top holders of Treasuries—banks and pension funds—is nil.

Treasuries are still classified as top-grade collateral, which means banks can continue to leverage these securities. T-bills are just as good as cash for bank reserves, as they were before the downgrade. No need to scramble for new collateral.

And Treasuries still have investment-grade status, which means pension funds don’t have to make any moves. Current asset allocations are just fine. It is “business as usual” at major financial institutions after the dramatic downgrade news.

Of course, the federal deficit is humungous and unlikely to ever be paid back. In real terms, that is. Nominally, the repayment will happen. An important distinction! Creditors will ultimately receive depreciated dollars due to inflation.

In other words, the $36 trillion owed to Treasury bond holders likely gets repaid in nominal (the actual number that includes inflation) versus real (inflation adjusted) terms. So creditors will receive the number of dollars borrowed plus interest, but those will be depreciated dollars—bucks themselves that due to inflation will be worth less than today.

Which means the key to successful retirement investing will be diversifying away from US dollars and into “hard asset” plays. We’ll discuss two today that will appreciate as the dollar declines. One yields 8.6%!

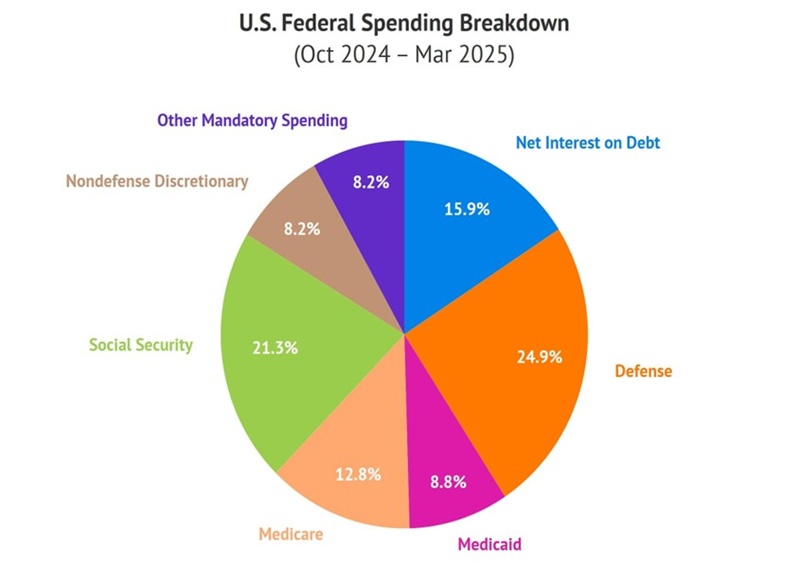

Why is the debt and path of the dollar an issue now when we’ve been on this debtor path as a country through many administrations for decades? Because we are teetering on the debt tipping point. The Social Security trust fund is projected to go negative by 2030, which will force the government to draw from general revenues.

Think DOGE is going to save the day? No. Most of the federal spending is untouchable. Messing with Social Security, Medicare or Medicaid is political suicide. Same with “other mandatory spending”—these are benefits that have been promised. Voters won’t have it any other way. And older people who receive Social Security and Medicare? They vote at the highest rate of any age group.

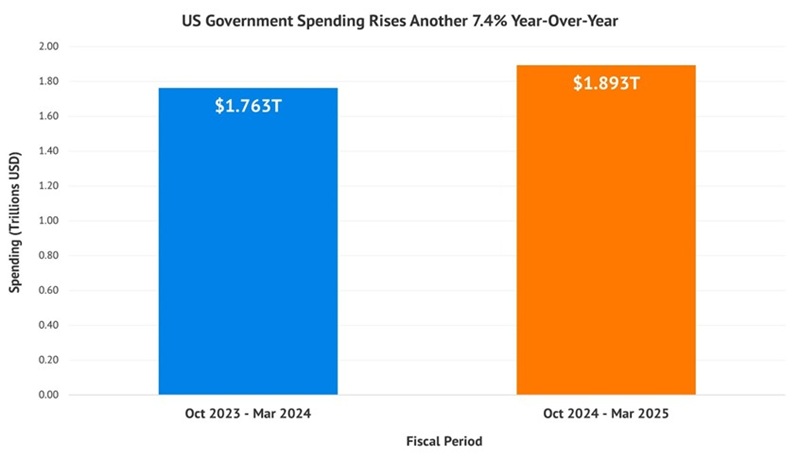

The net interest on our debt continues to climb. Defense spending seems “secure” given the current state of the world. Which leaves the modest nondefense discretionary slice, just 8.2% of the federal spending pie for DOGE to slice from:

With such a small austerity target, it’s no wonder that government spending is up 7.4% year-over-year for the first six months of this fiscal year (which began October 1, 2024):

Tax receipts, however, are not up 7.4%. These “revenues” are only up 3%. The US has a highly-indebted balance sheet with expenses growing faster than sales—not good.

If austerity via DOGE is not happening, then what is the alternative? Money printing. Jay Powell’s term is up one year from now. Trump will appoint a friendly face such as Kevin Warsh, Kevin Hassett or Judy Shelton who will work with the administration to (ahem) paper over some of these debt issues.

And by the way, Powell may be insistent on “higher for longer” rates, but he is not acting hawkish across the board. In fact, the market saw right through his “all bark, no bite” rhetoric at the last Fed meeting because his recent actions have spoken louder than his words.

If you’re wondering who is buying Treasuries at 4-some-percent in today’s environment, the answer should be no surprise—the Fed. Yup. Powell & Co. recently “stepped up” their buying an extra $20 billion per month!

With the Fed the new “whale” at the table, foreigners are (believe it or not) once again scrambling to buy Uncle Sam’s bonds. They briefly paused in tariff-laden April but have returned in a big way in May. We saw robust demand at the May 6 auction, with foreign investors buying 71.2% of the $42 billion in 10-year Treasury notes (up from an average of 67.6%).

It takes a village to keep the Treasury yield down! And all hands are on deck. The Fed increasingly supports the Treasury market. Don’t listen to the naysayers who claim the Moody’s downgrade is going to crush the bond market—the administration, Treasury, and Fed are working together to keep the lid on bonds.

The US runs the world’s printing press, and Uncle Sam is using it to buy more of his own debt. This is why gold has glittered year to date, and why the yellow relic’s move higher is likely to continue.

Gold miners themselves have retreated modestly from mid-April levels. VanEck Gold Miners ETF (GDX) sits 8% off its recent all-time highs and is likely to bottom.

The fundamental backdrop for yellow metal miners couldn’t be better. Gold prices are high and oil prices are low—which means maximum profit margins.

That’s why we like GDX even though it yields a mere 1%. Its real potential lies in its price appreciation. While GDX is up 37% year-to-date—even after its recent pullback—investors will realize the only “way out” for the federal government is monetary inflation and they will drive up the price of gold even more.

Let’s close with a discounted way to invest in gold. GAMCO Global Gold, Natural Resources & Income Trust (GGN) is a closed-end fund trading at a 3% discount to net asset value (NAV) as I write. GGN’s “97 cents on the dollar” price tag is attractive.

About half of the fund’s portfolio sits in mining stocks—both gold and non-gold plays like iron miner Rio Tinto (RIO). The miners-at-large have some great earnings reports ahead of them thanks to low energy prices because oil, a key input cost for mining operations, is down 27% year-over-year.

This underfollowed, misunderstood fund should continue to grind higher as the government papers over its pile of debt. GGN will pay us 3 cents per month, every month, as our slow-motion monetary train crash unfolds. And that’s good for 8.6% per year.

3 super small-caps with 6%+ yields to consider for passive income

High yields can come in small packages! Roland Head looks at three niche companies with the potential to provide attractive passive income.

Posted by

Roland Head Published 21 May

Image source: Getty Images

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.Read More

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Investors looking for reliable passive income often focus on big FTSE 100 companies. Some of these giants can certainly be a good source of dividends. But the UK market’s also home to a number of smaller companies with a strong reputation for income.

Here, I’ll highlight three small-caps offering dividend yields of 6% or more – including two stocks from my own portfolio.

A recovery story?

Epwin (LSE: EPWN) produces housebuilding products such as doors, windows, cladding and decking. The last couple of years have been tough, due to slower conditions across the UK’s housing market. Fortunately, Epwin has remained profitable and in good financial health through this period, recently reporting increased annual profits.

The risk is that conditions could remain weak or even worsen if the UK suffers a recession. However, I think the picture could be improving. Recent government data showed a 17% increase in shipments from UK brick factories during the first quarter of this year.

Builders may order bricks for a new home before they order doors and windows. But if more bricks are being sold, I reckon there’s a good chance that more doors and windows will be needed over the next 12 months.

Epwin currently trades on eight times forecast earnings, with a 6% dividend yield. I reckon that’s worth considering.

A niche business yielding 8%

Currency management expert Record (LSE: REC) isn’t a household name. Some of its largest customers are Swiss pension funds. In total, the company’s customers trust it to provide currency hedging and related services for more than $100bn of underlying investments.

We can get an idea of the value attached to its services by looking at its accounts. Last year, Record reported a 27% operating margin, generating a return on equity of more than 30%. These excellent figures are fairly typical for this business.

When a company can consistently generate this kind of profitability, my experience is that it usually offers a service its customers value highly.

Perhaps the main risk is that historic growth has often been slow and inconsistent. Recent performance has improved, but there’s no guarantee this will continue. However, Record’s 8% dividend yield looks safe to me. It’s also high enough for me to be relaxed about the risk of slow growth.

A 9.9% yield!

Sabre Insurance (LSE: SBRE) is a niche operator in the UK motor insurance market, focusing on higher-risk drivers and lines such as motorcycle and taxi insurance.

The advantage of this model is that Sabre’s less exposed to competition from price comparison and large brands. The firm’s customers require more skilled underwriting, but profit margins are higher to reflect the extra risk.

As a potential investor, my main concern is that the company’s core market is relatively small. One area currently being targeted for growth is to offer cheaper insurance to less risky drivers, while also accepting slightly lower profit margins. This could work well – but there’s a lot more competition in this area, so careful judgement will be needed.

Broker forecasts for 2025 show Sabre with a dividend yield of 9.9%, covered by earnings. This business looks interesting to me and is on my list for further research. I think it could be worth considering for passive income.