I’m going to make an opening purchase in TG26 of 2k. Remember if held outside a tax free wrapper you need a low coupon.

Cash left to invest £837 plus dividends for June of £1,329.00. Either 2k to be pair traded with the gilt or added to the gilt depending on markets at the end of this month.

Its like you learn my mind! You appear to know a lot approximately this, such as you wrote the e-book in it or something. I feel that you simply can do with a few p.c. to power the message home a little bit, however other than that, this is fantastic blog. A great read. I’ll definitely be back.

I’m considering writing a low cost e-book as a sort of work book/reference book.

When markets fell because of Covid the price low for AEW was

55p the dividend was 8p a yield of 14.5%

You would receive this dividend, as long as it wasn’t cut for as long as you owned the share. You would have also achieved the holy grail of investing

in that you could have taken out your stake and re-invested in another high yielder whilst receiving income at a zero, zilch cost.

Also you would be receiving income on the dividends re-invested.

The dividend has been paid at a rate of 8p per year since then.

The current yield: share price 103p dividend 8p a yield 7.7%

As nearly all shares fell at the same time, unless you decided to sell, which in hindsight is easy but in real time much more difficult, you wouldn’t have the funds to bag a ‘bargain’ Trust.

You need a rainy day fund, pair traded with a higher yielder to maintain a yield of 7%. So the Snowball will start a rainy day fund by investing 2k into a UK Government gilt, hoping that the market doesn’t crash until the amount squirreled away is a lot higher.

The Board of Directors of the Company has declared an interim dividend of 0.55 pence per share for the three-month period to 31 March 2025. The dividend will be paid on 17 July 2025 to shareholders on the register as at 20 June 2025. The ex-dividend date is 19 June 2025. The 0.55 pence per share dividend represents the net revenue return earned by the Company for the three-month period to 31 March 2025.

In future periods, the Company will move to annual distributions with the next dividend declaration likely to be announced in February 2026, then every year thereafter. The dividends will not be less than 85% of net revenue return of the period distributed, as previously disclosed.

DIY Investor Diary: how I’m aiming for £10,000 annual income from my ISA

Kyle Caldwell speaks to an investor aiming to use income from his ISA to help fund his retirement, including trips abroad to watch cricket.

24th April 2024

by Kyle Caldwell from interactive investor

In our DIY Investor Diary series, we speak to interactive investor customers.

For many investors thinking about using ISAs or SIPPs to help fund retirement, the aim will be to secure a reliable and regular income from their investments without inflicting too much harm on the capital.

This is the plan of the latest DIY Investor to feature in our series showcasing how interactive investor customers invest. The 61-year-old mining engineer is aiming to generate £10,000 of income from his ISA to help fund retirement, including trips abroad to watch cricket.

He also has a SIPP, which is currently a smaller pot than his ISA, and he will receive both a defined benefit pension and defined contribution pension on retirement.

He says: “I’m looking to generate £10,000 a year from the ISA, of which I have around £200,000 invested. I’m aiming to take just the natural yield, so I’m looking for the ISA to yield around 5%, which is what it’s delivering at the moment.”

Drawing only the income produced by funds or investment trusts’ underlying investments – the natural yield – is a prudent way to reduce risk during retirement. This is because in a scenario where stock markets fall sharply, it is more difficult for a retirement fund’s capital value to recover after if you are withdrawing more than the natural yield.

Our investor’s ISA has 11 holdings made up of 10 investment trusts and one fund. The investment trusts span a range of countries, sectors and asset classes to provide diversification, which helps to reduce risk.

account for a quarter of the ISA. Both trusts have yields of just over 5% and are solid income payers, with long track records of consistently increasing dividends year in, year out. City of London has increased payouts every year since 1966, while Merchants Trust has upped payouts for 41 years in a row.

Around 30% is held in three global equity income funds:

Murray International Ord MYI, Henderson International Income (LSE:HINT) and Bankers Ord BNKR

One thing to bear in mind with global income funds and trusts is that some have low yields, of below 3%, due to having a large exposure to the US stock market, which is more growth than income-focused. However, two of the three trusts held by this DIY investor, Murray International and Henderson International Income, buck the trend by being less wedded to the US. Both trusts have dividend yields of around 4.5%.

Our investor says: “Rather than picking countries or themes myself, I prefer to pick investment trusts that are ‘dividend heroes’, due to them having longstanding track records of growing their dividends every year.

“One area I do not have too much exposure to is the US. To me, everything seems a bit too rosy, and I am cautious on whether the US technology stocks can continue their strong run of performance.”

He adds that investment trusts’ ability to “retain money for rainy days is a good feature and I like the accountability to shareholders”, which is why he prefers trusts over funds.

Under the investment trust structure, 15% of income generated each year from the underlying investments can be held back to be used in future years. Due to this, 20 investment trusts have raised their dividends for more than 20 years. Incontrast, funds do not have this “get-out-of-jail-free card” and have to pay all the income generated back to investors each year. Therefore, when there’s an income shortfall, such as during the Covid-19 pandemic, a dividend cut is pretty much inevitable for funds.

The rest of the DIY Investor’s portfolio has exposure to property, bonds and infrastructure. This includes two defensive strategies: Capital Gearing Ord

and Royal London Short Term Money Market. As well as holding both to reduce risk, our DIY Investor views the duo as cash-like investments and, therefore, they will be the first to be sold if he needs to dip into his ISA ahead of retirement.

The SIPP’s smaller size may change in the coming years, as there is the option for the DIY investor to top it up if he takes the 25% tax-free lump sum from his pension. If it is topped up, he will also look to generate £10,000 a year from his SIPP.

Eleven investment trusts are in the SIPP, which he says are “a bit more riskier” overall due to his plan to take money out of the ISA first. This makes sense from an inheritance tax (IHT) perspective, as ISA money typical forms part of an individual’s estate for IHT. Whereas, pension assets aren’t usually subject to IHT. Another attraction is that pension money passed on from those who die before 75 is tax-free. For those who die at 75 or later, the beneficiaries will pay income tax on withdrawals.

While the focus is now on using the ISA and SIPP to help fund his retirement, he had previously invested to help fund property purchases. At this point, he invested in funds as he was not aware of investment trusts. However, he became more familiar of trusts from reading Money Observer magazine and interactive investor’s editorial content. One piece of particular interest is the yearly £10,000 investment trust income challenge.

He says: “As part of my research, I’m looking for ideas and pointers to narrow down the vast number of funds. I only invest in things I understand, which is why I wouldn’t invest in cryptocurrency.”

His top tips for fellow investors include doing your research, investing monthly and being patient.

He says: “Drip-feeding on a monthly basis means you haven’t had the money available to spend elsewhere, which means you learn to live without it. And if you do it for long enough, you’ll see the money grow.

“Being patient is also very important. After all, investing is for the long term – it is not a football accumulator. I’ve seen a few ‘bumps in the road’ since I’ve been investing. However, they usually present investing opportunities if you have a cash buffer to deploy.

“I would also add that it’s important to have a clear objective about what you are seeking to achieve from investing. Doing so, will make clear which types of investments to focus on.”

Note: since this article was published JLEN is now FGEN and HINT has ben rolled over into JGGI.

The average UK house price has surged by 74% or more than GBP150,000 over the past 20 years, according to the property website Zoopla. Across the past two decades, the typical property value has risen from GBP113,900 to GBP268,200, Zoopla said. London has seen average house prices more than double over the past 20 years. The south-east and eastern England have also seen a particularly big jump in house prices, with average property values rising by 87% in both regions over the past 20 years. By contrast, house prices in the north-east of England have risen by 39% during the period.

Pictet strategists reveal the adverse trends in equity markets that investors will face over the next half a decade.

09 June 2025

Pictet strategists reveal the adverse trends in equity markets that investors will face over the next half a decade.

By Matteo Anelli

Deputy editor, Trustnet

Equity investors should expect to make half the returns they have become accustomed to over the past decade and a half, as markets will be challenged on several different fronts in the years to come, according to Pictet Asset Management senior multi-asset strategist Arun Sai.

“Both on earnings and on multiples, the primary drivers of growth tell us that returns are going to be much weaker for equities. It’s going to be as much as half of the past five to 10 years,” he said.

“Returns over the next five years for global equities will be around 5% rather than the 10% we have got used to.”

This all comes down to Sai’s view that the key driver of equity returns over the past 20 years has been a “bizarre” structural uptrend in profit margins – a consequence of globalisation.

Although globalisation is “not going to reverse”, it will be “more nuanced”, he said, continuing for services, plateauing on goods and reversing on capital – all of which will lead to lower margins.

His way to tackle that is to “allocate deliberately to non-US champions, mid-cap stocks and European assets”.

Challenged US leaders

The US will be particularly affected. US tariffs, tax increases and weaker consumer demand will push global equities into a profit downturn, just as investors will grow more wary of inflation volatility and less inclined to pay a premium for stocks from a country that is losing momentum and soft power amid divisive policies.

There will be no US exceptionalism to come to the rescue, said Sai, not even its superiority in tech.

“There is no question that the US is the leader in tech across several dimensions, but are the moats around tech companies as deep as we thought they were a year ago? Perhaps not,” he said.

Sai used the example of Chinese artificial intelligence (AI) firm DeepSeek, which challenged Open AI’s ChatGPT at the start of the year. But this isn’t the only champion whose leadership is “not quite eroding, but at least being challenged”.

The US does not have a monopoly on innovation, Sai stressed.

“There are champions everywhere that benefit from the same kind of winner-takes-all trend, but trade on much lower multiples,” he said. “While retaining your investments in the winners, some amount of exposure to these other companies makes sense and diversifies you away from very crowded positions.”

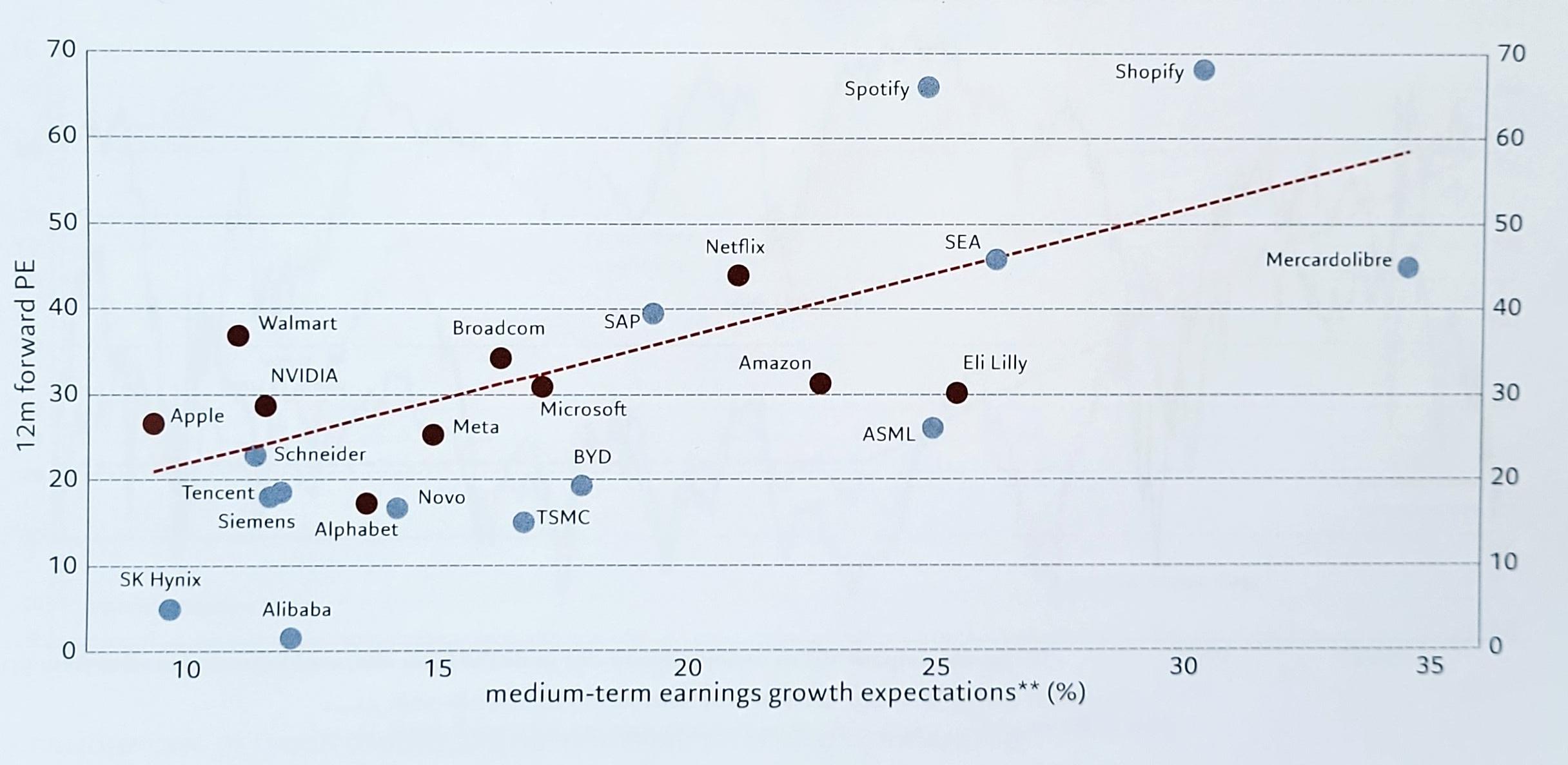

Below is a chart of such companies, showing the price-versus-growth expectations of US champions (in brown) and non-US champions (in blue).

US versus non-US leader by 12 months forward P/E ratio Source: Refinitiv, Pictet Asset Management. As of 30 May 2025.

“The blue dots are either as critical to some of these secular growth stories, or as good as some of the US winners,” Sai said. For example, he argued that the growth potential of Brazilian e-commerce company MercadoLibre is comparable to that of Amazon.

“There are a number of these players that have been left behind in the whole US exceptionalism narrative.”

To illustrate the transformation driving this winner-takes-all dynamic, Sai pointed to John Deere – a 200-year-old US tractor manufacturer that has reinvented itself as a high-tech solutions provider.

“We’re not abandoning that dynamic,” he said, “but on the margin we’re shifting toward non-US champions that are tapping into similar forces but trade at more reasonable valuations.”

Mid-caps on the rise

Not only did Sai suggest moving away from US leaders, he also argued that the large-cap space overall is getting overcrowded.

“If you had the luxury of taking a 30-year investment horizon, then all you would do is bet on the median stock, not on the winners,” he said. “That is because, over time, the median stock catches up to the winners. You always sell the winners and buy the median stock.”

Unfortunately, no investors can think that far ahead, so Sai suggested to hedge your bets: staying with the winners and allocating deliberately to what he called the “feed” stock.

“We think of this as mid-cap stocks. Investors should take an equal-weighted exposure to markets, rather than just focus on the mega-caps,” he said. “This gives them exposure to some of the next generation of winners, which will begin to play out in the next five years or so.”

The European advantage

Pictet chief strategist Luca Paolini mentioned another trend: there will be a “very minimal difference” between US and European GDP growth in a scenario where growth will normalise across developed countries.

“The US will always be a much more dynamic place to do business than in Europe. We are not saying sell everything in the US and come to the European heaven,” he said.

“Europe is not going to move significantly, but it is going to improve from a period of stagnation that has lasted for the past decade.”

Investors, especially if they are based in Europe, should also “think twice” about having a permanent, structural overweight to the US and would be better off putting their money to work at home.

“What we tend to forget is that, for Britons and Europeans investing abroad in equities, roughly 30% or 40% of total returns come from currency movements,” he said.

“The currency risk is not that relevant normally, but if you have low returns and low dispersion, like we will, one of the critical factors in achieving your expected returns is to get the currency right.”

DIY Investor Diary: this rule takes the emotion out of investment decisions

In the next instalment of our DIY Investor Diary series, Kyle Caldwell speaks to an investor who has a strict discipline of taking profits and cutting losses.

20th February 2024

by Kyle Caldwell from interactive investor

One investment pitfall is becoming too emotionally attached to a share, fund or investment trust whether it is a winner or a loser.

For the winners, investors risk becoming complacent having potentially “fallen in love” with the returns made in the past. However, there is no guarantee a top-performing company or fund will continue making hay in future years.

It’s important to take a step back and assess why an investment winner has been performing well. A fund, for example, could have been boosted by the region, area of the market, or investment style being in favour, which may not persist indefinitely.

In a similar vein, many investors find it hard to cut losses when an investment is underperforming. Some of this is rooted in behavioural finance biases, which cause investors to make irrational decisions based on emotion. Inertia, a tendency to maintain the status quo, is one example of a behavioural bias that can affect investment decisions. Inertia is part of the “endowment effect”, where an investor puts a higher value on something they own, so they are more reluctant to sell.

The latest interactive investor customer to feature in our DIY Investor Diary series seeks to take the emotion out of investing by enforcing a strict discipline of applying a “stop loss” of 15%.

The investor, who prior to retirement was a financial adviser, explains: “If, for example, I buy something at £1, I will sell it if it drops to 85p. Conversely, if it hits £1.50 and drops 15% from its all-time high, then I will also sell it if it falls to £1.27.”

To keep track of how his investments are faring, the investor has created a spreadsheet. He says: “I record the date of purchase, the epic (a shortcut for the name of the investment) buy price, current price, highest price ever achieved, present percentage gain or loss, the highest percentage gain, and finally the date it happened.”

He is a very active trader and a follower of the momentum style of investing.

Momentum investing is a strategy that taps into investors’ psychology. Some investors will refuse to buy a particular share or fund until they see an uptick in performance, as they want their inclination to buy to be validated by the market as a whole. Then, if that company or fund starts to rise decisively, investors who initially sat on the sidelines start to fear missing out on an opportunity to make money. They then buy, leading to momentum being retained.

However, this approach is only for those with the time and dedication to keep on top of their investments on a daily basis. Moreover, trading frequently can eat into overall returns.

The investor says: “I am a believer in momentum. I am trying to catch a wave and find investments that are starting to have a good run of performance. I study performance figures over one, three and six months, look at which shares, funds and investment trusts are starting to move, and consider the reasons why they are going up.”

He has both a self-invested personal pension (SIPP) and a stocks and shares ISA. The SIPP holds a mixture of shares, funds and investment trusts, while the ISA contains AIM shares that typically qualify for Business Property Relief. Such shares are exempt from inheritance tax (IHT) if they’ve been held for more than two years. The plan is for both the pension and the AIM ISA to be gifted to his four children.

In the SIPP, the six funds held are Comgest Growth America, L&G Global Technology Index, TM Natixis Loomis Sayles US Equity Leaders, Nomura Funds Japan Strategic Value, Pictet Robotics and GAM Disruptive Growth. The latter two are new holdings, introduced at the start of 2024.

Three investment trusts are held at present.

3i Group Ord

Ashoka India Equity Investment Ord

and India Capital Growth Ord IGC1.14%.

Despite currently holding fewer trusts than funds, the investor says he favours investment trusts due to their structural differences.

He says: “Investment trusts have a board of directors who can, and have, taken the investment mandate from an investment company and awarded it to another if they feel that there is underperformance or poor management.

“As regards dividends, they can withhold income and carry it forward to the next year, something that their collective cousins can’t do. Often it is possible to buy the investment trust at a discount to its net asset value. Again, this is something denied to funds.

“[Trusts] can gear (borrow) to magnify returns, but this can work against them in falling markets.

“Finally, you can deal instantly, whereas prices change only once a day with funds. If the market is either falling or rising rapidly, you have to wait until the following day to deal in funds, by which time prices may have moved badly against you.”

In addition, some exchange-traded funds (ETFs) are owned, including

Amundi IS Nasdaq-100 ETF-C USD GBP

Amundi Russell 1000 Growth ETF,

Invesco EQQQ NASDAQ-100 ETF GBP

Invesco Technology S&P US Sel Sec ETF GBP

iShares S&P 500 Info Tech Sect ETF$Acc GBP

IITU0 and ETC Group Global Metaverse ETF.

Given the yearly fund charge for passive funds is much lower than active funds, our DIY Investor says he’s drawn to passive strategies in areas that are heavily researched, meaning it is harder for active fund managers to gain an edge.

He says: “It has to be a special actively managed fund to get my attention.”

Key lessons learnt over the years include being both patient and humble. He notes: “One of my mottos is that success or failure in life is never final. It’s very chastening because it stops you from becoming complacent if things are going well, and it’s uplifting that even if things are bad, [things] can and will change.

“When applied to investment, don’t get cocky just because your investments seem to be flourishing, and don’t despair if they are suffering. Nothing lasts forever. Most investments enjoy a hot spell, but they can also endure lean times.

“Just to emphasise the point, when practising as an Independent Financial Adviser I had several “bankers” such as Lindsell Train Ord Worldwide Healthcare Ord and TR Property Ord TRY but in the six years since I retired they have gone nowhere.

“Investments are only a vehicle or means to an end, so don’t get emotionally attached to them. Some people can’t sell even when something is floundering because it would confirm that their judgement might have been wrong. I have often sold a holding and bought back in again at a future date.”

9% plus yields: how to navigate this investment trust sector.

Falling interest rates could provide a good entry point into renewable energy infrastructure trusts with their near double-digit yields, says Jennifer Hill.

9th June 2025

by Jennifer Hill from interactive investor

In the investment world, few sectors have experienced as sharp a reversal as renewable energy infrastructure trusts. Once buoyed by strong investor demand, these vehicles – powered by sun, wind, and waves – offered the appeal of clean energy alongside reliable, high-yield income.

But as interest rates climbed and sentiment turned cautious, the sector’s once-steady premiums to net asset value (NAV) gave way to steep discounts – from an average 7.2% premium at the end of 2021 to a 34.1% discount at the end of April this year.

“The renewable infrastructure sector has certainly been through the mill – wind or otherwise,” says David Liddell, a director at IpsoFacto Investor. “It’s important to note that the disastrous share price performance of many of these trusts has mainly been the result of this de-rating, rather than necessarily a fundamental loss in underlying value.”

With interest rates cut again last month to 4.25%, is now the time for investors to reconsider the sector and its weighted average yield of 9.4%?

Headwinds

A perfect storm of challenges triggered the sector’s sharp de-rating. Chief among them were rising interest rates – making cash and bonds more appealing – and waning investor enthusiasm for renewables. These were compounded by a flood of new investment trust launches, government intervention, surging construction costs, and growing doubts over long-term viability.

William Heathcoat Amory, managing partner at Kepler Partners, cites Ørsted’s early May decision to cancel Hornsea 4 – a major UK offshore wind project – as a telling signal.

“The Hornsea 4 cancellation is illustrative of higher build costs and lack of transaction data, which has meant developers are less confident on returns,” he says.

An exodus of wealth managers hasn’t helped either. An obscure regulatory ruling on how costs are attributed has eroded the appeal of these trusts among fund-of-funds managers.

Ongoing consolidation within the wealth management industry has only added to the pressure. Nowadays for a wealth manager to consider an investment trust, the assets need to be around 300 million for it to have a sufficient amount of liquidity.

“A focus on liquidity, in part driven by the consolidation of wealth managers and the increasing use of model portfolios, means that many infrastructure investment companies that failed to reach scale are now off the radar for potential new investors,” says Numis analyst Colette Ord.

“At the end of 2024, we decided to exit most of the holdings,” says Jack Turner, head of ESG portfolio management. “The decision was based on doubts on when discounts would close but also the uncertainty on the success of underlying infrastructure projects, especially those linked to renewable technologies.”

Tailwinds

Others see green shoots – and an opportunity to buy at the bottom. For Ord, current pessimism is “excessive”, while Liddell and James Carthew, head of investment companies at QuotedData, describe the sector as “just too cheap” and “irrationally cheap”, respectively.

Ord highlights the disconnect between weak sentiment in listed markets and robust demand for infrastructure exposure in private equity and debt. “Banks continue to view the sector as a high-quality covenant, evidenced by the number of successful financings at both project and company level,” she adds.

Demand could be fuelled by as much as £50 billion in fresh investment under the government’s Plan for Change – an initiative involving the UK’s largest pension funds and aimed at boosting business and infrastructure.

Signatories to the agreement will commit 10% of their workplace pension portfolios to assets supporting economic growth, such as infrastructure, real estate and private equity, by 2030.

“At least half that will be directed specifically to UK-based investments, expected to generate £25 billion for the domestic economy by the end of the decade,” says Darius McDermott, managing director at FundCalibre, the fund research firm.

“And with the current level of global uncertainty, the UK looks an increasingly stable haven. We’re already beginning to see asset managers return to undervalued UK assets – particularly lower down the cap scale – which could mean falling discounts and rising capital returns for trust investors.”

There may be other longer-term political and economic forces at play, with Kepler’s Heathcoat Amory perceiving strong public support for renewable energy.

“I think the UK populace other than Reform voters are in favour of a significant expansion in renewable power, so Hornsea 4 may in time be met by further political or financial support to get built out, which may help turn sentiment.”

In the short term, he adds, a slowdown in wind turbine development could benefit existing assets. “Less development buildout will reduce the pressure on long-term power prices, one of the inputs into valuations, which will be a tailwind at the margin.”

Short-term opportunity?

Fairview Investing director Ben Yearsley points to a “fascinating area with what could turn out to be a short-term opportunity”.

in a £1 billion deal that represents a premium to NAV, while in battery storage Harmony Energy Income Trust Ord is being acquired at a 5% discount to NAV and 35% premium to where shares had been trading.

Ord at Numis says it “sends strong signals on valuation”. She expects consolidation to continue while share prices trade at such wide discounts.

Given the amount of takeover activity, “will there be any interesting ones left in a year’s time or will it be only the dross left?” asks Yearsley.

The sector spans a diverse range of strategies – solar, wind, hydrogen, energy efficiency and energy storage. Some trusts focus on one area, while others combine multiple technologies to balance seasonal generation and market cycles.

Single-asset-class trusts are more likely to become takeover targets, says Carthew – a prospect that could help crystallise value for shareholders. But trusts with broader diversification may offer greater resilience against shifting weather patterns and regulatory pressure.

“Geographic and technology diversification has benefits,” says Ashley Thomas, an analyst at Winterflood Securities. “This is currently demonstrated by the weak wind speeds experienced year-to-date across Europe, which has impacted wind generation. In contrast, solar generation in the UK has been strong in March and April, but relatively weak in Spain and Australia.”

As renewable capacity expands, Thomas expects to see more pronounced intra-day price volatility, with solar pushing down prices during bright summer days and wind doing the same on breezy winter nights.

The potential of locational pricing being introduced into the UK, as well as general regulatory or political risk in certain geographies, also supports the case for diversification, he adds.

Best buys

For investors sitting on the sidelines, there is one overriding reason to consider infrastructure trusts.

“Yield is the obvious and relevant answer,” says Mike Neumann, bespoke investment management director at EQ Investors.

This, he adds, applies both to income seekers and growth-focused investors. Investors can increase the value of their shareholding by reinvesting dividends and achieve capital growth over time without any additional cash outlay.

Yearsley agrees: “While there’s a short-term opportunity for discount narrowing and capital gains, it’s a long-term income-producing story you’re really investing for.”

He says the “good opportunities” lie in trusts able to secure long-term power purchase agreements – which tends towards solar, wind and hydro – and those with dividends covered by cash flow. His top picks are Greencoat UK Wind and Downing Renewables & Infrastructure Ord

EQ is also a fan of Greencoat UK Wind, with its market capitalisation of £2.5 billion, -21.9% discount and yield of 8.9%. “It yields about twice that of a long-dated gilt and generates a significant level of cash even when wind resource is low,” says Neumann.

Carthew finds it harder to choose just one name. “It’s hard to pick – I own a few – but I love Downing Renewables mainly because of the hydro and battery storage potential, and to me, this feels like a relatively lower-risk investment,” he says.

The top pick for both Ollie Clark, deputy head of research at WH Ireland, and Liddell at IpsoFacto Investor is the Renewables Infrastructure Group, which is predominantly exposed to wind, with additional exposure to solar and a growing interest in energy storage through its acquisition of Fig Power.

Clark rates the trust’s “risk dynamics”, while its near £1.9 billion size and fully operational, “quality” portfolio should help it to capture inflows from liquidity-conscious investors. “Despite the near 10% yield and these attractive characteristics, TRIG still trades on a discount of -28.2%,” he says.

Liddell, meanwhile, appreciates TRIG’s long experience in the sector (since its launch in 2013) and its size, which allows it to sell assets to other institutional investors without compromising its own viability.

“TRIG has shown the way in raising cash through divestments, which have been at an average premium to valuations of 11%, giving some justification to the level of NAV,’ he adds.

focuses on reducing energy use through on-site generation and efficiency projects.

“Its holdings are diversified across sectors and geographies, with assets located in the UK, Europe, and North America,” says McDermott. The £480 million trust is trading on a -51.4% discount and yields 14.2%.