If you are considering adding any Investment Trust to your Snowball, the first check is to see if they have paid a gently rising dividend.

Check the dividend fcast if there is broker coverage, buy and sell advice is of interest only but extra caution if the consensus is a SELL.

Fourth Interim Dividend Declaration

NextEnergy Solar Fund, a leading specialist investor in solar energy and energy storage, is pleased to announce its fourth interim dividend of 2.11p per Ordinary Share for the quarter ended 31 March 2025.

The fourth interim dividend of 2.11p per Ordinary Share will be paid on 30 June 2025 to Ordinary Shareholders on the register as at the close of business on 23 May 2025. The ex-dividend date is 22 May 2025.

This dividend announcement brings the total declared dividends for the financial year ended 31 March 2025 to 8.43p per Ordinary Share and represents the Company’s eleventh successive year of successfully meeting its dividend guidance.

Check what the company says about the current dividend and any guidance on future dividends.

If you are content that dividends are ‘secure’ although no dividend is one hundred percent secure and you like the yield of

Price 66.5p. Dividend 8.43p = Current yield 12.5%

You know that if the dividend is ‘secure’ your capital will be returned in 8 years and you will have a share that pays you income at a cost of zero, zilch, nothing.

Also as the dividends are re-invested you will receive income from the re-invested cash and your total yield would be ??????????

The next xd date is the end of August.

After researching similar high yielding Trusts, you may or may not decide to buy.

2 mega-cheap dividend shares to consider this summer, 1 with a 12.7% yield! Investors don’t need to spend a fortune on dividend shares to target a large and reliable passive income, as these top stocks show.

Posted by Royston Wild Published 4 June

NESF SUPR

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

Read More You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Looking to make a big passive income at low cost? Here are two great dividend shares worth thinking about as the summer season kicks off.

Supermarket Income REIT Real estate investment trust (REIT) Supermarket Income REIT (LSE:SUPR) trades at a near-10% discount to its net asset value (NAV) per share. It also carries a large 7.6% forward dividend yield.

While it’s sensitive to interest rate changes, I still think it’s potentially a great low-risk way to source a second income. And especially at today’s prices.

As the name implies, this property stock provides exposure to the ultra-stable food retail market. But this isn’t all: by focusing on the industry’s leading players — ‘Big Four’ operators Tesco and Sainsbury‘s are just a couple of big hitters on its books — rent collection and occupancy issues are rarely an issue.

What’s more, by focusing on omnichannel stores, Supermarket Income draws out the threat posed by online grocery to future earnings.

As a REIT, the business is obliged to pay at least 90% of its annual rental profits out by way of dividends.

As I mentioned, the stock is vulnerable to interest rate changes that push up borrowing costs and depress asset values. But on balance I think it’s a great way to consider sourcing a long-term income.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

NextEnergy Solar Fund With a 12.7% forward dividend yield, NextEnergy Solar Fund (LSE:NESF) is the third-highest-yielding UK investment trust today. I think it has tremendous long-term potential as demand for green energy heats up.

It’s not just the rush to net zero that’s driving renewable energy growth. Rising concerns over energy security (worsened by the Russia-Ukraine war) are also propelling investment into sustainable sources and making capacity extensions more cost effective.

NextEnergy Solar has 101 assets spread across Europe, The Americas and Asia, providing solid geographic diversification. Roughly 85% of its sites are located in the UK too, where the government’s renewable energy policy is especially favourable for operators.

On top as packing that huge yield, the trust’s shares trade at a near-30% discount to their NAV per share. This represents great value in my view.

Like Supermarket Income, NextEnergy solar is highly sensitive to rises in interest rates. But this isn’t all, as changes to favourable green investment policy could also impact future profits. Recent changes in the US show that supportive government initiatives can be subject to change.

However, I believe these risks are more than reflected in the cheapness of the fund’s shares. On balance it’s still a solid passive income stock to consider.

Asked by: Dr. Jarred Rath Jr. | Last update: February 15, 2025

How the Rule of 72 Works. For example, the Rule of 72 states that $1 invested at an annual fixed interest rate of 10% would take 7.2 years ((72 ÷ 10) = 7.2) to grow to $2. In reality, a 10% investment will take 7.3 years to double (1.107.3 = 2). The Rule of 72 is reasonably accurate for low rates of return.

What is the 7 year compounding rule?

Using the Rule of 72, you can realize the power of compounding interest and better plan for future financial goals. If $5,000 was invested with an annual growth rate of 10%, the original investment would double to $10,000 in 7.2 years. After 7.2 years $10,000 doubles to $20,000.

How long would it take for you to double your money from $9000 to $20,000 if you will earn 12% interest?

The rule is this: 72 divided by the interest rate number equals the number of years for the investment to double in size. For example, if the interest rate is 12%, you would divide 72 by 12 to get 6. This means that the investment will take about 6 years to double with a 12% fixed annual interest rate.

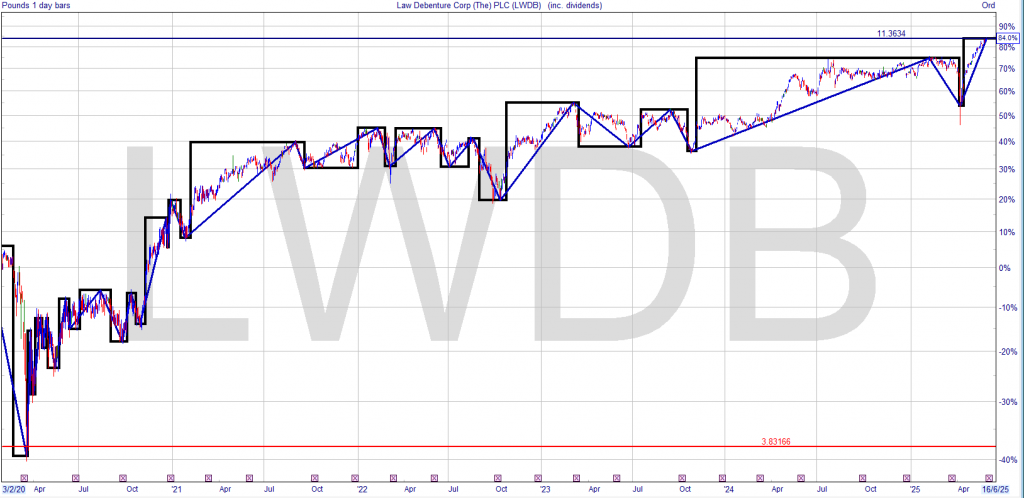

With darkening investment skies, I am considering investing this month’s earned income, including current cash around 3k into a pair trading strategy.

An Investment Trust that pays a dividend around ten percent and a UK Government Gilt paying around 4%. Although this would be a small drag on overall performance, it would still maintain a blended yield of seven percent.

The Government Gilt to be held until/if/when the next market crash happens and the gilt would then be sold and re-invested into a Dividend Hero share.

LWDB is a coveted Trust but if the drop was not substantial it could possibly replace the safe investment of the Government Gilt. Current yield 3.47%, so a lot of water would need to flow under a lot of bridges.

How much will you need in your pension pot to fund your retirement lifestyle?

The PLSA highlights that the full annual new state pension – currently £11,973 – will help fund much of the minimum standard but you will need a larger pension pot to buy an annuity or earn enough from drawdown for a moderate or comfortable retirement.

Analysis by Quilter for MoneyWeek suggests that a single person would need a pension pot worth £459,000 to get a moderate level of income from an annuity, rising to £738,000 for a comfortable retirement.

A couple would need £515,000 to purchase an annuity for a moderate lifestyle and £929,000 for a comfortable one.

This assumes an annuity rate of 5.34% for a single person and 4.79% for a couple.

The amount you need to put away in a pension to build a pot worth £738,000 will depend how far away you are from retirement.

If you have 40 years to save, then you would only need to put away £7,4677 per year, according to Quilter.

But that rises to £12,652 over 30 years and £23,830 over 20.

This assumes a 4% annual real return.

“What the figures continue to show is that it will take a concerted effort to achieve a pension pot required to meet the difference between the income level indicated by the standard and that provided from the full state pension,” says Jon Greer, head of retirement policy at Quilter.

“The earlier that savers understand the difference, then the easier it will be to plan how to achieve it – or achieve the target that’s personal to you. Unfortunately, no one is going to do it for you.”

AJ Bell estimates that to obtain these standards in drawdown, a single person would need a pension pot worth £490,000 for a moderate lifestyle or £790,000 for a comfortable one.

This rises to £515,000 for couples wanting a moderate lifestyle and £890,000 for those seeking a comfortable standard.

The figures are based on annual investment returns of 4% after charges, that income rises by 2% per year and the pot lasts for 25 years.

“Spikes in inflation have clearly made that task harder but there is no magic bullet when it comes to building a retirement pot that matches your goals and spending plans,” says Tom Selby, head of retirement policy at AJ Bell.

“The key is to save as much as you can from as early as possible, taking advantage of the upfront boost of pension tax relief, tax-free investment growth and, where available, employer contributions. While the fund sizes needed to achieve a moderate or comfortable standard of living might be intimidating, making a realistic budget and setting up a regular savings plan can make the task a lot less painful.”

A couple would need £515,000 to purchase an annuity for a moderate lifestyle and £929,000 for a comfortable one.

This assumes an annuity rate of 5.34% for a single person and 4.79% for a couple.

Of course when you retire the annuity rate could be higher or lower, that’s the gamble you take with your retirement.

The income for a moderate lifestyle based on an annuity of 5%, would be

£25,750. Whilst you may not plan on having a pot of £515,00 could you make a plan using a dividend re-investment Snowball for a similar amount ?

Remember you would keep all your capital rather than gifting it to an Insurance Company.

· No material disposals in the near term, sales of growth assets planned in the mid-term

· New adjusted fee structure agreed with the investment manager

· Resilient NAV, record cash generation and increased dividend target

· Publication of Annual Report in June to include a full update on strategic priorities

The Board of FGEN, a leading investor in private environmental infrastructure assets across the UK and mainland Europe, today provides an update on the Company’s unaudited March 2025 Net Asset Value (“NAV”), dividend and strategy.

Performance highlights

· NAV total return of 1.0% in the three months to 31 March 2025, and 0.6% in the financial year to 31 March 2025.

· NAV of £678.7 million as of 31 March 2025 (£695.4 million as of 31 December 2024). NAV per share of 106.5 pence down from 107.4 pence in December 2024 (-0.8%).

· Delivering on dividend commitment: Final quarterly dividend of 1.95 pence in line with the Company’s target.

· Record cash generation from the portfolio, supporting sustainable dividend coverage of 1.32x.

· Targeting an11th consecutive annual increase in the dividend: dividend target of 7.96 pence per share for the year to 31 March 2026, a 2% uplift on FY 2025.

· Active discount control through the repurchase of 9,746,891 shares in the quarter ended 31 March 2025. Total buybacks since 15 August 2024 of £19.2 million and the extension of the programme to £30 million announced in March 2025.

Ed Warner, Chair of FGEN, said:

“FGEN’s portfolio continues to perform to plan, delivering record cash generation, a resilient NAV and a well-covered and growing dividend. This robust foundation confirms that the operational part of the portfolio delivers significant value in the near-term, while growth assets carry meaningful upside potential in the future. The ongoing reduction in gearing, share buybacks and recent asset disposals alongside an adjusted fee structure announced today strengthen FGEN’s position for the future.

“As part of the Board’s determination to do everything to maximise shareholder value, it has considered a full range of strategic options with independent advisors. The Board concluded that the long-term prospects of the Company and shareholder interests are best served through the proactive management of the existing portfolio. The Company will follow a re-focused investment strategy, prioritising a core portfolio of environmental infrastructure assets with long-term stable cash flows delivering predictable income alongside opportunities for growth.

“In the medium term, the Company is seeking to deliver capital appreciation through the disposals of its growth assets and as such, no material asset disposals are expected in the near-term. We look forward to presenting our strategic priorities at the fullyear results in June where we will set out the substantial, long-term investment opportunity for environmental infrastructure.”

Re-focused investment strategy

With the support of independent advisors, the Board rigorously evaluated a full range of strategic alternatives for the Company, including a managed wind-down, a targeted divestment approach, the continuation of the current investment strategy, and potential mergers and acquisitions.

Following this review, the Board has concluded that the long-term prospects of the Company and shareholder interests are best served through the proactive management of the existing portfolio, and a refocused investment strategy that reflects the structural changes in macro-economic conditions since 2022, characterised by increased levels of market volatility and higher return expectations in an elevated rate environment.

Given this context, future investment activity will be disciplined, seeking to maintain a balanced risk-return profile and prioritising core infrastructure assets and businesses that offer long term stable cash flows, secured revenues and inflation linkage. FGEN will focus on renewable energy generation – solar, wind, anaerobic digestion, biomass and hydro – alongside other energy infrastructure including long and short duration storage, low-carbon heat, cleaner transportation, and sustainable resource management across the waste and water sectors.

Within that, the Company will invest in growth assets in mature, lower-risk sectors which provide opportunities for capital growth, including construction-stage and late-stage development projects.

As part of the Company’s objective to strike a careful balance between generating income to support a growing dividend and delivering medium-term value creation, the Company will not target further material disposals of its well-established assets in the near-term. FGEN intends to exit from the existing growth assets in the portfolio in the medium-term once they have fully ramped up, with good progress being made on those assets in line with expectations. Rjukan is now in the final stages of construction with first harvest targeted for July, further offtake agreements have been signed at the Glasshouse facility as operations continue to ramp up, and the restructuring across the CNG platform better positions the overall venture for growth as the rollout of stations continues and volumes of gas dispensed increase.

In line with strict return criteria, the Company will continue to monitor market conditions and assess opportunities as they arise.

Further detail on strategic priorities will be provided at the FY 2025 results webinar in June.

Investment manager fee structure update

The Board is very conscious of the need to deliver excellent value for shareholders as well as excellent returns over the long term. To that end, last year both the basis for calculation of investment management fees was changed to net asset value, and the fee rate charged was also reduced. Now, we can announce that the basis of calculating fees is further adjusted to better align the interests of the investment manager, Foresight Group LLP, with those of shareholders.

From a proposed date of 1 October 2025, fees will be calculated 50% based on net asset value and 50% on market capitalisation (the latter element capped at net asset value). This is estimated to provide an annualised saving of over £800k on the current NAV-based fee arrangement, a c. 13% reduction. Since 30th September 2024, prior to the previous change, this 50:50 blended fee arrangement will result in FGEN reducing investment management fees by c. 34%.

While the Board is pleased to deliver this change, which represents a material reduction in operating costs, it is strongly committed to exploring all possible ways in which the cost of managing FGEN can be lowered further in the future to the benefit of the Company’s shareholders.

NAV performance

NAV per share

NAV at 31 December 2024

107.4p

Dividends paid in the period

-2.0p

Power price forecasts

-0.1p

Portfolio performance

-0.6p

Review of maintenance expenditure

-0.7p

Uplift from share buy-back programme

0.5p

Other movements (including discount rate unwind less fund overheads)

2.0p

NAV at 31 March 2025

106.5p

Valuation factors

Power price forecasts

The Company’s high degree of contracted revenues and controlled exposure to merchant power prices through selective asset diversification provides a low exposure to fluctuations in market pricing. As a result, the Company experienced a low NAV per share impact of -0.1 pence in the period to 31 March 2025.

Portfolio performance

Portfolio performance was below forecast for the three-month period ended 31 March 2025, primarily due to a period of lower-than-expected solar irradiance and wind speeds, as well as downtime due to an unplanned outage at the Company’s Italian energy-from-waste investment.

FGEN’s diversification strategy means the fund is resilient against unpredictable weather patterns, with a 10th consecutive year of record cash distributions received from the portfolio – driving a full year 2025 dividend cover of 1.32x, marginally exceeding guidance issued in the 30 September 2024 report (“above 1.20x”).

Review of maintenance expenditure

As part of the regular review of maintenance requirements across the portfolio, budgets have been increased across the foodwaste anaerobic digestion facilities at Bio Collectors and Codford Biogas, leading to a reduction in NAV per share of -0.7 pence.

Capital allocation and discount management

The board remains acutely aware of the challenging backdrop that affects the Renewable Infrastructure sector and the Company, with the sector continuing to trade at a material discount to NAV. An active discount management strategy has been implemented during the period, supported by disciplined capital allocation measures incorporating asset disposals, repayment of debt and share buybacks.

Gearing

In line with the Company’s stated approach to capital allocation, FGEN continues to maintain one of the lowest levels of gearing in the sector. As at 31 March 2025 total gearing was 28.7%, with the Company’s Revolving Credit Facility (“RCF”) £99.3 million drawn.

Post year end, the Company reduced the size of its RCF from £200 million to £150 million, providing an annual cost saving of £0.4 million. The remaining RCF continues to provide ample headroom to cover outstanding portfolio commitments and value enhancement projects as well as the remaining payments for the Company’s well progressed construction and early-stage operational investments.

Share buyback programme

As part of the ongoing share buyback programme, the Company purchased 9,746,891 shares in the quarter, increasing the NAV per share by 0.5 pence. Since its inception on 15 August 2024, the initial buyback programme has returned a total of £19.2 million to shareholders by 31 March 2025. The Company also announced on 31 March 2025 its intention to extend the buyback programme to a total maximum aggregate consideration of £30 million, via a further £10 million being allocated to the buyback programme funded from the Company’s own resources in accordance with its stated approach to capital allocation.

Dividend

Following the earlier announcement of a final quarterly interim dividend of 1.95 pence per share for the period from 1 January 2025 to 31 March 2025, the Company will have paid a total of 7.80 pence per share in respect of the year ended 31 March 2025, in line with the dividend target set out at the start of the year.

Financial performance of the portfolio continues to be strong, with dividend cover of 1.32x for the year to 31 March 2025, and the Board is pleased to announce an 11th consecutive annual increase in the dividend target to 7.96 pence per share for the year to 31 March 2026, a 2% uplift on FY 2025. This dividend represents a yield of 10.4% on the closing share price at 2 June 2025.

Big, Beautiful Bond Yields Up to 11%: For Contrarians Only

Brett Owens, Chief Investment Strategist Updated: May 28, 2025

The “big, beautiful bill” has turned into a bitter pill for bonds. As you’ve undoubtedly heard, bond buyers aren’t exactly thrilled about lending more money to a $36 trillion debtor that’s digging itself deeper into a financial ditch.

Prior to the proposed “One Big Beautiful Bill Act” (OBBBA), the Congressional Budget Office (CBO)—famous for crunching numbers through rose-colored glasses—already projected a $1.9 trillion deficit for 2025. Now, the CBO estimates that the current House-passed version of OBBBA will add an extra $3.8 trillion to the national debt over the next decade.

This leaves Uncle Sam staring into a $40 trillion hole, deepening by roughly $2 trillion each year.

Treasury bond yields spiked recently as buyers vanished. Last Wednesday, a seven-week stock rally reversed midday when the U.S. struggled through a weak $16 billion auction of 20-year bonds. The tepid demand for these long-dated Treasuries confirmed what many already thought—with Uncle Sam spending like a drunken sailor, who’d lend him more?

Thus, the popular mainstream conclusion: The U.S. has entered its final “doom loop” debtor stage. Rates are rising as bond investors demand higher compensation to offset the credit risk posed by Uncle Sam’s ugly finances (you know, $40 trillion…).

Higher rates increase the country’s financing costs, which worsens the debt situation, which leads investors to demand even higher rates, and so forth. This implies we should avoid bonds entirely.

To borrow a concept from billionaire investment manager Howard Marks, this is a “first level” interpretation. It is accurate on paper but misses the nuances.

In a truly free market, the “bond doom loop” narrative would be valid. But in the real world that you and I inhabit, my fellow contrarians, we must elevate our thinking to the second level for more nuanced consideration.

Here, we recognize the “Quiet QE” the U.S. Treasury began under then-Secretary Janet Yellen. She subtly influenced the bond market by issuing short-term debt rather than long-dated Treasuries. This maneuver reduced the supply of long-term bonds, thereby suppressing long-term yields. (The same number of buyers chased fewer long-dated bonds, pushing prices higher and yields lower.)

This strategic pivot was significant. At the end of 2019, short-term bills represented just 15% of marketable U.S. debt. By 2024, Yellen funded 75% of the deficit via the short end of the yield curve.

Two summers ago at Contrarian Outlook, we identified this Quiet QE interplay between Yellen and Fed Chair Jay Powell. Renowned economist Nouriel Roubini published a paper 12 months later identifying this “activist Treasury issuance” (ATI) as Uncle Sam’s favorite plumbing tweak.

Roubini confirmed the U.S. Treasury is, shall we say, finessing debt issuance to nudge longer-term rates lower than they’d naturally be. Without ATI, the 10-year Treasury yield would be 30 to 50 basis points higher—equivalent to up to two rate hikes in the Fed Funds rate.

In other words, the 10-year yield would top 5% today if not for Quiet QE. And the cost of borrowing for business (lending rates) and individuals (mortgage rates) would be notably higher.

Current Treasury Secretary Scott Bessent publicly criticized this tactic but has quietly continued it. Year-to-date, the Treasury has financed 80% of its funding needs through short-term issuance. If we witness more weak auctions like last week’s, Bessent could very well lean even harder into lower cost short-term borrowing.

Short-term rates are influenced primarily by the Federal Reserve rather than the broader bond market. And Jay Powell’s term ends in less than a year, when President Trump will likely appoint an ally like Kevin Warsh, Kevin Hassett, or Judy Shelton, who will cooperate with the administration to lower the Fed Funds rate.

A lower Fed rate will in turn reduce short-term Treasury yields. With 80% of issuance short term, this will significantly lower debt-service costs. In fact, this is already happening. Fellow financial author Mel Mattison notes that total interest on the public debt is declining year-over-year despite a ballooning deficit!

Mel reminds us that Powell didn’t start cutting the Fed Funds Rate until last September. So, this fall the decline in interest payments will really start showing up in the year-over-year data. More evidence against the case of the “interest rate doom loopers.”

Does this fix the giant US debt problem? Of course not. But Mel’s point is that our politicians and central bankers have “creative options” at their disposal. Vanilla investors tend to glance at the surface and move on. But we careful contrarians appreciate the nuances and gear our income portfolios accordingly.

The somewhat-secret swap to short-term debt should bring a ceiling on long-term yields. Bessent, after all, is not going to tolerate a higher 10-year yield that boosts interest on the debt. He wants a cap on long rates, which will provide a floor beneath the bond market. He’ll get one by limiting long-dated bond supply.

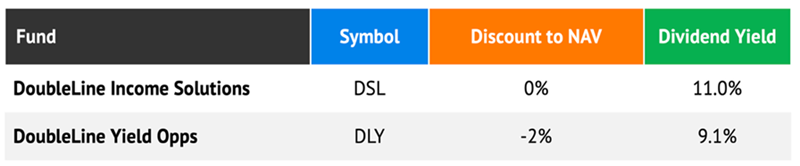

Viewed through this lens, our DoubleLine bond funds look attractive here. If long rates are near a high watermark, then the prices of the paper owned by DoubleLine will enjoy a yield-driven tailwind. DoubleLine Yield Opportunities Fund (DLY) yields 9.1% and trades at a 2% discount to its net asset value (NAV), while DoubleLine Income Solutions Fund (DSL) pays an 11% yield and trades at par.

These two bond portfolios are also supported by a strengthening economy. The negative first-quarter GDP print was likely the most bullish development for the real economy. Trump and Bessent will make sure we don’t experience negative GDP growth in the second quarter.

Consecutive negative quarters would officially signal a recession. They don’t want this scarlet letter heading towards the midterms. Trump and Bessent no longer need an economic slowdown to push long-term yields lower—they’ll simply work with the short end of the bond market from here.

Political pressure on Powell, the “lame duck” , will ease. As will pressure on the long end of the curve.

Let’s ignore the mainstream Chicken Littles declaring the end of bonds. These “first level” thinkers overlook the power of coordinated Treasury and Fed policy. Here at Contrarian Outlook we recognize the monetary “creativity”—and profit from it. Let’s keep enjoying these DoubleLine monthly payers yielding up to 11%.

For income investors who know where to look, there are more monthly dividend payers—yielding 8%+ annually—with underappreciated nuances. These dividend deals are available because, quite frankly, most individual investors (and money managers) don’t do their homework.