3 “Secret” Funds That Could Let You Retire Earlier Than You Think

Michael Foster, Investment Strategist Updated: June 19, 2025

Few things ease financial worry like knowing you can walk away from work anytime you want.

Closed-end funds (CEFs) give us just that kind of security—and we talk about that a lot in my weekly articles and in my CEF Insider service. With yields of 8%, 9% and more, CEFs generate huge payouts that could let you retire earlier than you think.

It’s such a powerful—and overlooked—way to invest that it’s worth revisiting again today. We’ll color our discussion by looking at how some typical American retirees could retire with CEFs.

And we’re going to work in some real-life numbers, too.

I can’t stress enough that we’re not doing anything exotic to grab these yields: One of these three CEFs invests in S&P 500 stocks. The others are almost as familiar, holding corporate bonds and publicly traded real estate investment trusts (REITs).

More on these funds in a moment. First, let’s look at some real figures to see how much income investors could potentially book from CEFs.

Retirees Are Doing Better Than You Think (and Could Do Better Still)

The numbers say something startling: The average retiree is doing well, with the 65-to-74-year-old cohort sporting an average net worth of $1.79 million in 2022, with some of that being in their primary residence. Since that was a lousy year for markets, that net worth is probably higher now.

Of course, not everyone is doing well. Because many haven’t been able to save as much as the top tier, the median retiree has a net worth of about $409,900. This means they need to rely on Social Security.

However, even a less-wealthy retiree could have a comfortable retirement with the three funds I’m about to show you—and we’ll get to those in just a moment.

But first, let’s talk about our average retiree, with that $1.79-million net worth.

They probably have at least some of their wealth in S&P 500 index funds, which yield around 1.3%. That translates into $2,000 in monthly income if they had the full $1.79 million available to invest (an assumption we’ll make as we move through this article).

They could get much more through the three funds we’ll discuss next—all of which will be familiar to CEF Insider readers.

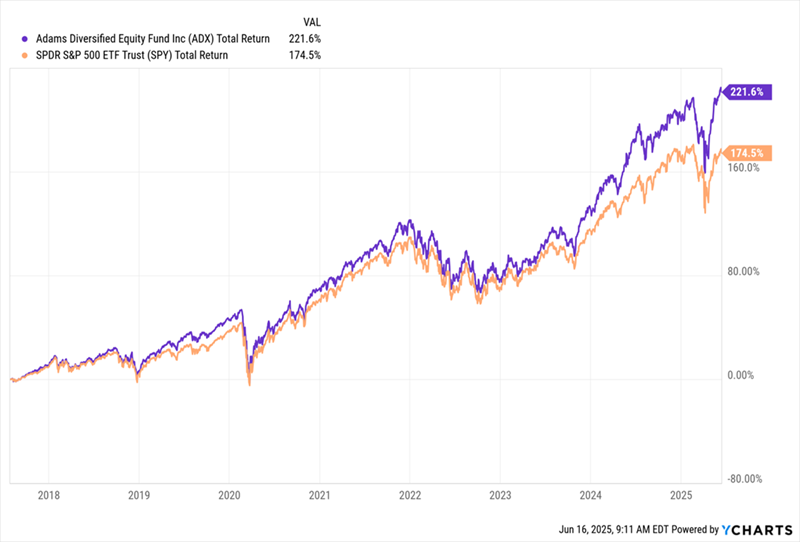

“Financial Freedom” Buy No. 1: Adams Diversified Equity Fund (ADX)

The Adams Diversified Equity Fund (ADX) yields 8.8% and holds well-known stocks like Apple (AAPL), Microsoft (MSFT) and Visa (V). It’s also one of the world’s oldest funds, having launched in 1929, days before that year’s market crash.

Moreover, ADX has a history of strong returns: It has crushed the S&P 500 for decades, including our holding period at CEF Insider, which began nearly eight years ago, on July 28, 2017.

ADX Demolishes the Index, Returns 222% for CEF Insider

Despite that outperformance, ADX has a 7.5% discount to NAV that has been closing since the middle of 2024 but still remains quite wide. One other thing to bear in mind: ADX commits to paying 8% of NAV out per year as dividends, paid quarterly, so the payout does float as its portfolio value fluctuates.

“Financial Freedom” Buy No. 2: Nuveen Core Plus Impact Fund (NPCT)

Next is the Nuveen Core Plus Impact Fund (NPCT), a 12.2%-yielding corporate-bond fund. Its discount has been shrinking in the last few years, from over 15% to around 4.1% today.

NPCT Gets Attention

Again, the portfolio shows why: NPCT’s managers have picked up bonds from low-risk issuers, including utilities like Brooklyn Union Gas and financial institutions like Standard Chartered and PNC Financial Services Group.

More importantly, they’ve taken advantage of higher interest rates to lock in high-yielding bonds with long durations, with an average leverage-adjusted duration of 8.4 years. (This measure takes the effect of the fund’s borrowing into account, making it a more accurate description of rate sensitivity.)

That stands to pay off when rates decline, cutting yields on newly issued bonds and boosting the value of already-issued, higher-yielding bonds like the ones NPCT owns.

“Financial Freedom” Buy No. 3: Nuveen Real Asset Income and Growth Fund (JRI)

Let’s wrap with the 12.3%-yielding Nuveen Real Asset Income and Growth Fund (JRI). Its portfolio features powerhouse REITs like shopping-mall landlord Simon Property Group (SPG) and Omega Healthcare Investors (OHI), which profits from the aging population by financing assisted-living and skilled-nursing facilities.

The fund has seen its discount shrink to 3.1% from the 15% level it was at in mid-2023, even after the pandemic hit REITs hard, and that discount continues to have upward momentum.

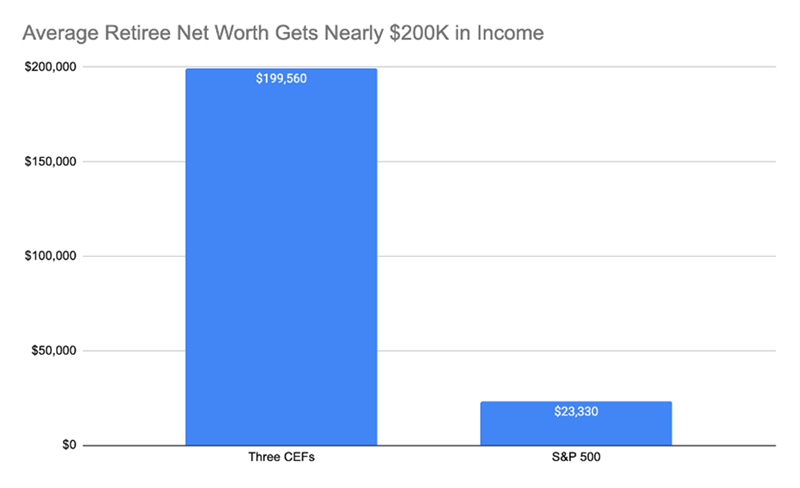

An 11%-Paying “Mini-Portfolio” That Pays the Bills (and Then Some)

Put those three CEFs together and you have a “mini-portfolio” yielding 11.1% on average. Here’s how that income stream looks with $1.79 million invested.

Source: CEF Insider

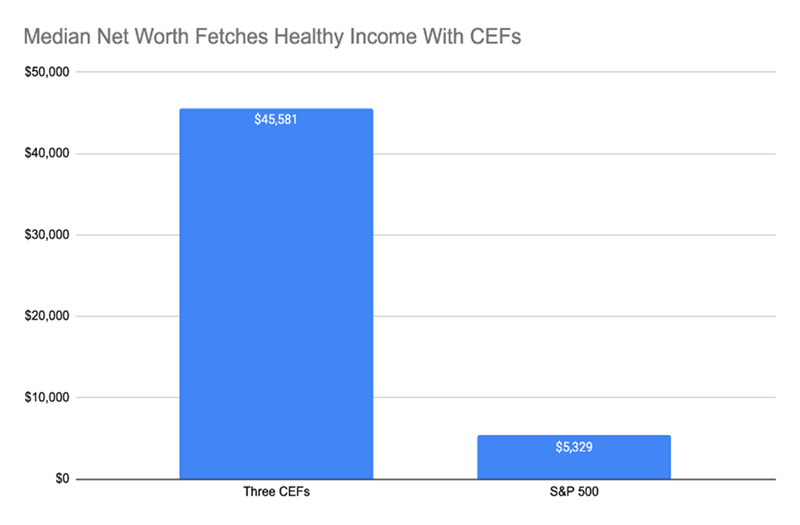

As you can see, with these CEFs, the average retiree’s net worth could fetch around $200,000 in annual income, or $16,630 per month. What about the median, though? Well, their $409,900 would bring in a nice income stream, too.

Source: CEF Insider

Now we’ve got $3,798 per month, a smidge higher than the median income for US workers (which is $3,518 per month, again per the Federal Reserve). Add the median $2,000 per month in Social Security benefits, and that turns into nearly $6,000 a month.

The beautiful thing about CEFs is they’re open to everybody—not just the rich (though these incredible income funds are certainly favorites of the billionaire set).

CEFs aren’t just for retirees, either. Got a job you love? That’s fine—keep at it and use your CEF dividends to reno your home, take more time off or help out the kids. It’s all up to you.

8.5% dividend yield! Should investors consider buying this high-income FTSE stock today ? Story by Zaven Boyrazian, MSc

The Motley Fool FTSE stocks have had a great run in 2025. In fact, the FTSE All-Share index is on the verge of delivering double-digit returns since the year kicked off, and we’re only six months in. Of course, not every business has enjoyed an upward streak, like Greencoat UK Wind (LSE:UKW), which is actually down by almost 10% since January.

However, despite the lack of positive sentiment from investors, management’s maintained dividends with plans to start hiking them even further as we move into 2026. As a result, investors can now lock in a staggering 8.5% dividend yield – one of the highest on the market that’s set to grow even further.

The bull case Being an owner of a vast wind farm portfolio has its perks. With the government pushing for a Net Zero energy grid by 2030, demand for wind power, along with other renewables, is on the rise. Higher interest rates have certainly been testing. But, management’s proactive approach to addressing balance sheet leverage has enabled dividends to keep flowing to investors even with falling energy prices.

Across its 49 wind farms, the company is now generating close to 2% of the UK’s total energy demand. And with further investments planned, its current generating capacity appears set to expand as the firm targets £1bn in net cash generation between 2025 and 2030.

In terms of dividends, that means shareholder payouts will rise from 10p in 2025 to 12.3p by the end of the decade. And that’s under the assumption that its average wholesale price of electricity stays between £66 and £57 per megawatt-hour (MWh) over the next five years. That’s a modest assumption compared to the current rate of £81.45/MWh as per June forward contracts.

In other words, providing that energy prices don’t collapse below management’s conservative forecast, this FTSE dividend seems to be sustainable.

The bear case Even if energy prices fall in line with expectations, there are plenty of other challenges Greencoat has to tackle. Most notable is the threat of interest rates. While they’re slowly falling, a reversal of this trajectory would add severe pressure to the group’s financial health, especially if energy prices don’t rise alongside it.

At the same time, the company’s at the mercy of the weather. Lower wind speeds have already caused the group’s energy generation performance to come in 11% under budget in both 2023 and 2024. And if this pattern continues, that means less free cash flow generation to service debts and pay out dividends.

But let’s assume everything does go to plan. Wind speeds pick up, energy prices rise, and interest rates get cut. Even in this scenario, the group’s still subject to limited growth potential as a result of the previously mentioned Electricity Generators Levy.

The bottom line With the bear case in mind, it’s easy to understand why Greencoat’s lost much of its appeal compared to a few years ago. Yet, despite these challenges and limitations, I remain bullish overall.

The FTSE stock’s trading 21% below its net asset value – a discount that even management’s begun capitalising on with share buyback schemes. Pairing that with a juicy 8.5% dividend yield that looks primed to grow even higher over the next five years, makes this an income stock worth considering, in my mind.

Looking at the chart, you will see that you haven’t made any money since the start of the year, in fact you would have lost a little, whereas the Snowball has increased its income by around 6k, which when re-invested, will provide further income for next year of around £500, plus a small contribution for the rest of this year.

Ian Cowie: the sector on a roll and offering yields of 8%-plus This sector’s seen an upturn in performance, but many investors are steering clear. Our columnist considers whether this is a potential opportunity for contrarians.

19th June 2025

by Ian Cowie from interactive investor

Related Investments

AEWU, SREI

How do you fancy this for contrarian income-seekers ? A British investment trust sector that is so far out of fashion that the average fund offers a dividend yield of 8.1%, despite delivering total returns of 20% over the past year, but the shares continue to be priced -16% below their net asset value (NAV).

Invest with ii: SIPP Account | Stocks & Shares ISA

Better still, for those of us who prefer winners to averages, the top investment trust among 10 funds in this sector, currently yields above 7.7%, despite delivering total returns of 32% over the last year; albeit priced at a more meagre discount of -4%. You normally have to choose between income and growth, but lucky shareholders here have enjoyed both.

That’s enough of the tease intro: step forward AEW UK REIT Ord AEWU 0.77%

This £230 million fund also leads the Association of Investment Companies (AIC) “Property: UK Commercial” sector over the past five years and decade periods, when this real estate investment trust (REIT) delivered triple-digit total returns of 125% over both periods.

So, this little-known fund has notched up an impressive hat-trick to lead its sector over all three standard investment periods. While it’s important to remember that the past is not necessarily a guide to the future, it has clearly not been a value trap where the real price of a high income today is low or no capital growth tomorrow.

Named after its Boston-based founders Aldrich, Eastman and Waltch – hence AEW – the fund managers have earned their high annual fees of 1.6% by shrewdly tending a portfolio of smaller commercial properties; predominantly in the provinces. For example, its most valuable holding is the site for the Welsh packaging firm Plastipak in Gresford; followed by flexible offices in Northgate House in Bath; with 40 Queen Square, Bristol, not far behind.

The nearest AEWU gets to capital city glamour is London East Leisure Park in Dagenham. But relatively low property prices have pushed up rental yields and worked well for this fund.

Similarly, the second-best performer in this sector over the past year is Schroder Real Estate Invest Ord SREI 2.62%

a £485 million fund that yields nearly 6.6% with total returns over the past year, five years and decade of 29%, 119% and 57%. It is currently priced at a discount of nearly -19% to its NAV.

Once again, the underlying portfolio is based far from big city bright lights and high prices. SREI’s top holding is Stacey Bushes Industrial Estate at Milton Keynes; followed by Millshaw Park Industrial Estate in Leeds; then Stanley Green Trading Estate in Cheadle.

However, it’s not cheap, with eye-watering annual charges of 2.7%, they can point to increasing shareholders’ income by an impressive annual average of more than 11% over the past five years. By contrast, AEWU has failed to sustain any annual increase in dividends over the same period.

Which brings us back to how they managed to combine capital growth with high dividend income and remain priced at discounts to their NAVs, along with most of the other eight funds in the “Property: UK Commercial” sector.

Working from home, a social phenomenon so well-known that it became an acronym, WFH, plus the growth of online retail, have convinced many investors that business parks, offices and shopping malls are dead or dying assets.

Watch our video: why gold and defence shares will keep rising Should fund managers reveal their ‘skin in the game’? While the online retail trend doubtless has further to run, we may have already passed the high-water mark for WFH, now that fear of contagious diseases – such as Covid – recedes in the rear-view mirror. However irrational it might seem to insist that employees who spend all day online should do so in an office, rather than their own homes, the fact remains that many employers prefer it that way – and increasing numbers are insisting on it.

Amazon, Barclays, BlackRock and, this week, HSBC, are among big businesses currently trying to encourage or enforce the return to office work. So, it seems that reports of the death of the office or other workplaces have been exaggerated and commercial property could continue to deliver capital growth plus income for contrarian investors.

Ian Cowie is a freelance contributor and not a direct employee of interactive investor.