Global stock markets have had an incredible run since their April lows. Major indexes such as the S&P 500 and the FTSE 100 have flown to new all-time highs while some stocks like Palantir and Joby Aviation have risen more than 100%.

This level of enthusiasm for stocks has surprised a lot of people given that economic uncertainty remains high. And it begs the question – is it now only a matter of time until we see a stock market crash?

The truth about stock market crashes

The truth about stock market crashes Volatility in the stock market’s very common, but it’s not often that we see a full blown crash. This is generally defined as a drop of 20% in a short period of time. And these only tend to come around every five to 10 years.

According to Capital Group, on average they occur about every six years. It’s usually when something unexpected happens (eg Donald Trump slapping huge tariffs on the whole world).

Given that we had one in April, I’d be very surprised to see another in 2025. Two crashes in one year would be unusual.

Given that we had one in April, I’d be very surprised to see another in 2025. Two crashes in one year would be unusual.

We could see a pullback in 2025

I do think there’s a good chance we’ll see some volatility in the second half of 2025 though. It might be a 5% pullback, or it may be a 10% move lower (defined as a ‘market correction’).

I don’t know when it will occur. It could come soon or it could come later in the year. And I don’t know exactly what will cause it. It could be related to tariffs or it could be related to corporate earnings or something else.

One thing I do know however, conditions are ripe for a pullback. Right now, there’s a lot of froth in the market.

I’ll buy the dip

I’m not afraid of market volatility though. In fact, I’d welcome it. The reason I’d embrace it is that it would give me the opportunity to buy stocks at lower prices. That’s what I want to be doing as a long-term investor.

A decent market pullback could present me with some compelling opportunities. Whether it’s the opportunity to add to an existing holding at a great price, or buy a new stock at a low price, I’d be able to put some of my cash pile to work.

I’ll point out that there are lots of stocks I’d love to buy more of at lower prices. One example is international payments firm Wise (LSE: WISE). I’ve been buying this stock in recent months. And if it was to come down 10%, I’d snap up more to build my position.

You do not need to take big risks to grow your Snowball.

The chart includes earned dividends but re-invested in another high yielding share. It’s high risk to buy the share now but as always it’s about timing and then time in. You would have achieved the holy grail of investing in that you could withdraw your capital, invest it an another high yielding share and receive income at a cost of zero, zilch, nothing.

Highlights

· Share price total return comfortably outperformed the FTSE Actuaries All-Share Index by over 5% with a total return of 14.2% for H1 2025.

· Net asset value (NAV) total return, with debt and Independent Professional Services (“IPS”) business at fair value, for H1 2025 delivered a performance of 15.0% (15.0% with debt at par).

· Another robust performance from IPS, with net revenue increasing by 7.7%, profit before interest and tax up by 7.5% (compared to H1 2024) and valuation up 4.8% to £203.8 million (compared to 31 December 2024).

· The Company issued 1.3 million new Ordinary Shares at a premium to NAV during H1 with net proceeds of £11.6 million.

Strong Longer-TermRecord

· Consistent share price and NAV (with IPS and debt at FV) outperformance of the benchmark over one, three, five and ten years.

· Share price total return over 10 years of 187.5% (FTSE All-Share: 92.7%), which compares favourably with UK Equity Income peers.

Dividend Highlights

· Declared a first interim dividend of 8.375 pence per ordinary share, paid in July 2025, representing an increase of 4.7% over the prior year’s first interim dividend.

· It is the Board’s intention for each of the first three interim dividends for 2025 to be equivalent to a quarter of Law Debenture’s total 2024 dividend of 33.5 pence per ordinary share.

· Continued strong performance of the Portfolio and growth of the IPS business supports the Board’s intention to maintain or increase the total dividend in 2025, enabling the Company to build on its’ 46 years of increasing or maintaining dividends to shareholders.

· Dividend yield of 3.4% based on our closing share price of 995 pence on 24 July 2025.

· Total dividend income from the portfolio of £22.5 million (H1 2024: £19.9 million).

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Using money to try and make money is basically how I would sum up passive income plans that are based on investing in dividend shares. With a long-term mindset, such an approach can be lucrative. For example, a spare £5,000 today could be invested in such a way that hopefully it ends up generating that much every year as a second income.

That is not based on some pie-in-the-sky “side hustle”, but instead is based on the dividend prospects of large blue-chip firms with proven business models.

Why the long-term approach matters

However, it is crucial to appreciate that this really does depend on taking a long-term approach to investing.

For £5k to generate £5k in dividends next year would require a 100% dividend yield. I see that as totally unrealistic even from very high-risk shares. For context, the current FTSE 100 dividend yield averages 3.3%.

However, by spreading the £5k across a handful of carefully chosen diversified shares, I think an investor could realistically aim for a 7% compound annual growth rate. After 33 years compounding at that rate, the portfolio ought to be worth over £74,000.

Not bad at all for a £5k investment today ! Then, at that point, if the portfolio is invested in 7%-yielding dividend shares, it ought to generate an annual second income of over £5,000 without any of the capital being withdrawn.

A higher or lower compound annual growth rate and yield could mean a shorter or longer timeframe than 33 years. But I think it is important to be realistic about possible returns and risks.

Finding the right shares matters too !

That compound annual growth could come from dividends, share price growth, or both. But dividends are never guaranteed and if share prices fall, that could hurt the portfolio’s growth rate. Clearly, it is important to take care when looking at possible shares to buy for a second income.

One share I think investors should consider at the moment is FTSE 100 insurer Phoenix Group (LSE: PHNX).

The company’s 8.3% dividend yield is certainly impressive – and the company aims to grow the payout per share annually. But as dividends are never guaranteed, it is important for investors to look at the source of a company’s payouts.

Phoenix may not be a household name but it is a big business. In fact, it is huge, with around 12m customers.

Its long-term savings and retirement business helps provide some resilience and predictability of likely future revenues. Brands such as Standard Life help it maintain a competitive position in the marketplace.

Its huge book of assets brings risks. For example, if the property market falls steeply, Phoenix may need to book losses on its mortgage book should the pricing assumptions it is built on no longer apply.

On balance, though, I see Phoenix as a firm with a proven business model that I think could be a low-key but resilient performer over the long term.

A home for the income

To start buying shares, an investor needs somewhere to put their available funds for buying shares and then accumulate any dividends.

So a useful first step would be setting up a share-dealing account, Stocks and Shares ISA, or share-dealing app.

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

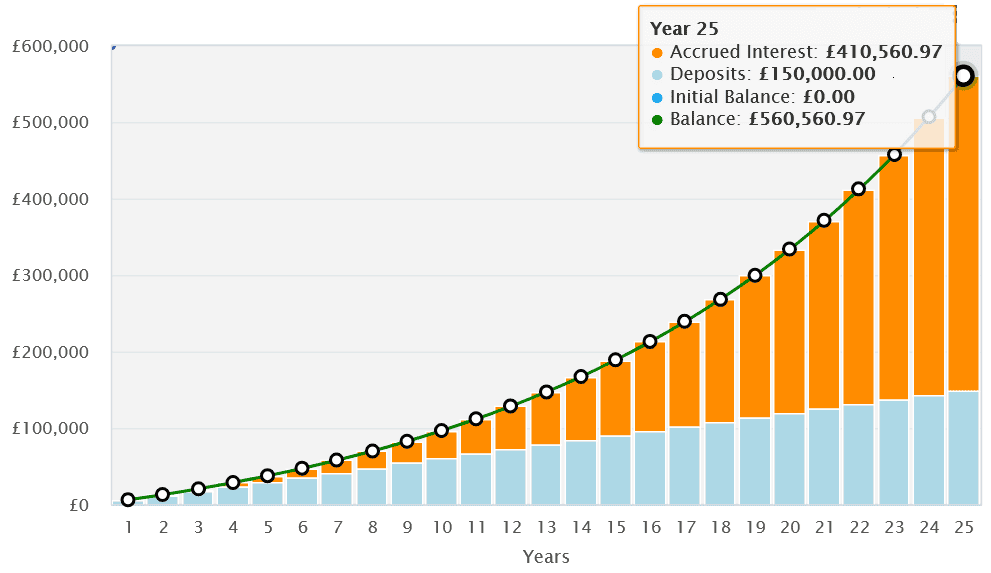

Thanks to the power of compounding, investing in dividend shares can be the fast-track to building significant wealth in a Stocks and Shares ISA.

Compounding involves reinvesting all the dividends one receives to buy more shares. More shares mean more dividends, and over time this snowball effect can supercharge long-term portfolio growth.

Let’s say an investor puts £500 monthly into a Stocks and Shares ISA, reinvesting dividends along the way. Thanks to the compounding effect, they’d have a portfolio worth £560,561 after 25 years, comprising deposits of £150,000 and three times as much as this — £410,561 — in investment returns. That’s based on an average annual return of 9%.

Source: thecalculatorsite.com

There are thousands of dividend-paying shares, funds, and trusts to choose from in the UK alone.

If you are nervous about the stock market, one way of starting on your journey is to buy a tracker that tracks the major indices. If you can choose when to sell you will not lose any money, as major markets in the long run go up, partly to inflation. There will be plenty of thick and thin, so when the markets are falling it may be best to have a modest yield to add to your Snowball.

With markets near to all time highs it’s a very dangerous time to buy a tracker.

Here, you would have doubled your money and the variable dividend re-invested into a higher yielder would have added to your Snowball. What appeared at the time to be a high risk purchase, in fact turned out to be a low risk purchase.

Do you ever feel “the curse” of investing at exactly the wrong point? Like your investing is too late, at the wrong time, or maybe that you’re just unlucky?

Well meet Bob – the World’s Worst Market Timer. Bob began his working career in 1970 at age 22 and was a diligent saver and planner.

His plan was to save $2,000 a year during the 1970’s, then increase his savings by $2,000 each decade. In other words $2,000/year in the 70’s, $4,000/yr in the 80’s, $6,000/year in the 90’s… you get the picture.

Bob started in 1970 with $2,000, added $2,000 in ’71 and ’72, then decided to take the plunge and invest in the S&P 500 at the end of 1972. (Time out: there were no index funds in 1972, but come along with me for illustration purposes).

Now in 1973 – 74, the S&P dropped by nearly 50%. Bob had invested his life savings at the peak, just before it fell in half ! Bob was bummed, but Bob had a plan and he was sticking to it. You see Bob never sold his shares. He didn’t want to be wrong twice by investing at the peak and then selling when prices were low. Smart move Bob !

So Bob kept saving $2k/year in the 70’s and then $4k/yr in the 80’s. But he was feeling the sting of his last investment and did not feel comfortable adding to his fund until he had seen the markets rise a fair amount. In August of 1987 Bob decided to put 15 years of his savings to work. Seriously Bob?

This time the market fell more than 30% right after Bob invested. Bob, amazed at his investing prowess, did not sell.

After the 1987 crash, Bob was really planning to wait it out. In the late 1990s everything was on fire. The internet was unbelievable new technology and stocks were flying high. By 1999 Bob had accumulated $68,000 from saving each year. A firm believer that the Y2K bug was boloney, Bob invested his cash in December 1999 just before a 50% decline that lasted until 2002.

The next buy decision in October 2007 would be one more big investment before he would retire. He had saved up $64,000 since 2000, deciding to invest this right before the financial crisis that saw Bob experience another 50% decline. Monkey’s throwing darts were probably better at investing than Bob.

Distraught and disheartened, Bob continued to save each year and accumulated another $40k. He kept his investments in the market until he retired at the end of 2013.

So let’s recap: Bob is definitely has “bad timing”, only investing at market peaks just before severe market declines. Here are the purchase dates, subsequent declines and the amounts Bob invested:

Fortunately Bob was a good saver, and actually a good investor. You see once he made his investment he considered it to be a long-term commitment and never sold his shares. Even the Bear Market of the 70’s, Black Monday in 1987, the Tech Bubble or the Financial Crisis did not cause him to sell or “get out” of the market.

He never sold a single share. So how did he do?

Bob almost fell out of his chair when his advisor told him he was a millionaire! Even though Bob made every single investment at the peak, he still ended up with $1.1M! How you might ask? Bob actually had what we would call “Good Investor Behavior”.

First, Bob was a diligent and consistent saver. He never waivered from his savings plan (recall $2k/year in the 70’s, $4k in the 80’s, $6k in the 90’s, $8k in the 2000’s, $10k in the 2010’s until his retirement in 2013 at age 65).

Second, Bob allowed his investments to compound through the decades, never selling out of the market over his +40 years of investing – his working career.

During that time Bob endured tremendous psychological toil from seeing huge losses accumulate right after he made each investment. But Bob had a long-term perspective and was willing to stick with his savings and investment plan – even if his timing was “a bit off”. He saved and kept his head down.

Certainly you realize Bob is an illustration. We would never advise only investing in a single strategy, let alone a single investment like an index fund. If Bob had invested systematically, the same amount each month, increasing his savings like he did he would have ended up with even more money, (over $2.3M) – but that would not have been Bob, the Worlds Worst Market Timer.

So what are the lessons?

If you are going to invest, invest with an optimistic outlook. Long-Term thinking often rewards the optimist. Unless you think the world is coming to an end, optimists are typically rewarded.

Temporary, short-term losses are part of the deal when you invest. How you react to those losses will be one of the biggest determinants of your investment performance.

The biggest factor in investment success is savings. How much you save, and how methodically you save has a much bigger impact than investment return. Get these three things right along with a disciplined investment strategy and you should do well. Even Bob did well. Nice work Bob.

As part of your Snowball, add a tracker, add funds from your dividends when markets crash.

In this dividend champions list, we will take a look at some of the best stocks to invest in.

Dividend Aristocrats are firms within the S&P 500 Index that have consistently raised their dividend payments for a minimum of 25 straight years. On the other hand, Dividend Champions are companies that have also maintained at least 25 years of dividend increases but may not be part of the S&P 500.

Despite the difference in classifications, stocks with a history of growing dividends have long remained a favorite among investors. After facing nearly two years of sluggish performance, these stocks are regaining popularity in 2025. Global funds focused on dividend-paying equities are now seeing renewed investor interest, as many look for reliable income sources amid ongoing economic and geopolitical uncertainty. According to LSEG’s Lipper data, dividend-focused exchange-traded funds worldwide attracted $23.7 billion in inflows during the first half of 2025 — marking their strongest showing in three years.

Steve Watson, an equity portfolio manager at Capital Group, made the following comment:

“Consistent dividend growth signals a company’s managers are disciplined at capital allocation and confident about future business prospects. With tariff negotiations likely to linger for months, dividend growers could provide portfolios with a measure of stability when markets become volatile.”

Given this, we will take a look at some of the best stocks in our dividend champions list.

Our Methodology

For this article, we scanned the list of Dividend Champions, companies that have raised their dividends for 25 years or more, and picked companies that are comparatively lesser known to investors but are reliable investment options. Next, the hedge fund sentiment was measured using data from 1,000 hedge funds tracked by Insider Monkey in Q1 2025. The list is ranked in ascending order of the number of hedge funds having stakes in the companies.

Why are we interested in the stocks that hedge funds pile into? The reason is simple: our research has shown that we can outperform the market by imitating the top stock picks of the best hedge funds. Our quarterly newsletter’s strategy selects 14 small-cap and large-cap stocks every quarter and has returned 373.4% since May 2014, beating its benchmark by 218 percentage points.

Norwood Financial Corp. (NASDAQ:NWFL) is among the best stocks on our dividend champions list. In July, the company, along with PB Bankshares, announced that their boards have approved a merger agreement under which PB Bankshares will be merged into Norwood. The merger will create a combined institution with around $3.0 billion in assets, positioning it as a leading community bank serving Northeastern, Central, and Southeastern Pennsylvania.

This move significantly broadens Norwood Financial Corp. (NASDAQ:NWFL)’s presence, extending its reach into faster-growing markets across Central and Southeastern Pennsylvania. The company recently announced earnings for its Q2 2025 and reported strong results. Its return on assets improved by 31 basis points to reach 1.06% compared to Q2 2024. Net interest margin rose 13 basis points from the previous quarter and 63 basis points year-over-year. Loan growth was strong, with annualized increases of 4.4% for the quarter and 8.2% year-to-date. Meanwhile, deposits expanded at a 15% annualized pace year-to-date, while the cost of deposits declined by 20 basis points since Q4 2024.

Norwood Financial Corp. (NASDAQ:NWFL) ended the quarter with over $53 million available in cash and cash equivalents. On June 18, the company declared a quarterly dividend of $0.31 per share, which was in line with its previous dividend. Overall, it raised its payouts for 33 years in a row. The stock has a dividend yield of 5.05%, as of July 23.

California Water Service Group (NYSE:CWT) is a California-based public utility company that offers drinking water and wastewater services. The company remains committed to securing a timely and positive outcome in its 2024 California General Rate Case, recognizing its importance in supporting infrastructure investment and maintaining long-term service reliability. On a broader economic level, management believes that the company’s steady performance, reliable results driven by rate base growth, and solid dividend program present a compelling opportunity to deliver long-term value to shareholders.

In the first quarter of 2025, California Water Service Group (NYSE:CWT) reported revenue of $204 million, down 25% from the same period last year. As of March 31, 2025, the Group held $90.1 million in cash and cash equivalents, including $45.7 million in restricted funds. In addition, the Group had access to $315 million in short-term borrowing through its credit lines, available upon satisfying the borrowing requirements for both the Group and its subsidiary, California Water Service (Cal Water).

California Water Service Group (NYSE:CWT) currently offers a quarterly dividend of $0.30 per share, having raised it by 7.1% in January this year. This was the company’s 58th consecutive year of dividend growth, which makes CWT one of the best dividend stocks on our dividend champions list. The stock has a dividend yield of 2.66%, as of July 23.

Community Financial System, Inc. (NYSE:CBU) is a financial services firm with operations across four key areas: banking, employee benefits, insurance, and wealth management. Its banking arm, Community Bank, N.A., ranks among the top 100 banks in the US by asset size, managing over $16 billion. The bank serves customers through roughly 200 branches located in Upstate New York, Northeastern Pennsylvania, Vermont, and Western Massachusetts.

Community Financial System, Inc. (NYSE:CBU) recently announced earnings for the second quarter of 2025. The company posted revenue of $199.3 million, which saw an 8.4% growth from the same period last year. It reported net interest income of $124.7 million for the second quarter, marking a new quarterly record and reflecting a 14% increase, or $15.3 million, compared to the same period last year. During the quarter, the company also announced an agreement with Santander Bank, N.A. to acquire seven branch locations in the Allentown, Pennsylvania area. The acquisition includes select branch-related loans, deposits, and wealth management relationships, and is expected to advance the company’s previously outlined retail growth strategy.

Community Financial System, Inc. (NYSE:CBU) ended the quarter with $237.2 million available in cash and cash equivalents. On July 16, the company declared a 2.2% hike in its quarterly dividend to $0.47 per share. Through this increase, the company stretched its dividend growth streak to 33 years, which places it on the dividend champions list. The stock has a dividend yield of 2.66%, as of July 23.

Donaldson Company, Inc. (NYSE:DCI) is one of the best dividend stocks on our dividend champions list. The company manufactures filters used in a wide range of applications— from computers and power plants to large industrial machinery— helping protect these systems from damage and enhancing their overall efficiency. The stock has surged by over 6.6% since the start of 2025.

Donaldson Company, Inc. (NYSE:DCI) demonstrated its strength by reporting record sales and record adjusted earnings per share in fiscal Q3 2025. It also increased its full-year adjusted earnings per share guidance and accelerated its share repurchase program, buying back 3.3% of its outstanding shares since the beginning of the year. The company reported revenue of $940.1 million, up 1.3% from the same period last year. The revenue also beat consensus estimates by $6.65 million.

For the first nine months of the year, Donaldson Company, Inc. (NYSE:DCI) generated $251 million in operating cash flow and had $178.5 million available in cash and cash equivalents. The company remained committed to its shareholder obligation, returning $32.3 million to investors through dividends in the third quarter. Currently, it offers a quarterly dividend of $0.30 per share and has a dividend yield of 1.68%, as of July 23. The company has been growing its payouts for 29 years.

Commerce Bancshares, Inc. (NASDAQ:CBSH) is a regional bank holding company that provides a wide range of services, including banking, lending, payment processing, wealth management, and trust solutions. Its success is supported by a solid compliance structure, strong capital position, careful risk management practices, and a strong emphasis on serving its customers. The stock has surged by nearly 3% in the past 12 months.

Commerce Bancshares, Inc. (NASDAQ:CBSH) reported strong earnings in the second quarter of 2025, with revenues of $448.4 million. The revenue saw a 6.7% growth from the same period last year and also beat analysts’ estimates by $12.54 million. Commerce reported solid financial results for the second quarter, driven by its diversified business model and the strength of its team. The performance was supported by an increase in loans, healthy fee income, low credit costs, and ongoing discipline in managing expenses— factors that have consistently contributed to the company’s long-term profit growth.