Put money into a Stocks and Shares ISA, buy a range of high-quality dividend shares, monitor the portfolio from time to time.

Can earning sizeable passive income streams really be as simple as that? Yes it can!

Setting the right approach

I ought to explain immediately that this is no overnight scheme. Rather, it is an example of how a long-term approach to investing can hopefully pay rewards in future.

If the £20k is compounded at 8% annually, after 32 years the Stocks and Shares ISA should be worth over £234k. An 8% dividend yield on that would amount to over £18k a year in passive income – without touching the capital.

With more than £20k, the timeline could be reduced — or the goal could be targeted with less than £20k, but taking more years to reach it. Another variable is the compound annual growth rate and later, dividend yield achieved. The higher that is, the quicker the goal could be hit — but it is important to stay realistic. Too much risk could mean what seems like a quicker approach ends up being a slower one after all.

That helps explain why I think the savvy investor will take time to construct a carefully selected, diversified portfolio of high-quality shares.

Another element that could eat into the compound annual growth is fees, charges, commissions, taxes and the like. So choosing the most suitable Stocks and Shares ISA is also wise in my view.

Making a start

I think an 8% target is realistic in today’s market. The current FTSE 100 average dividend yield is 3.3%. Some individual shares offer much higher yields – and the compound annual growth rate takes share price movement into account too.

Here’s how to aim to make your kids millionaires with a Stocks & Shares ISA

Many of us aim to be ISA millionaires. It’s certainly possible, but it’s potentially even easier to put your children on the path to that millionaire status.

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

Opening a Stocks and Shares ISA for a child at birth or a very young age could be one of the most powerful financial gifts a parent or guardian can give.

With time, consistency, and the power of compounding, even modest monthly contributions have the potential to grow into a substantial sum. This could possibly even making that child a mid-life millionaire.

In the example below, just £300 a month — totalling £3,600 a year — is invested from birth. Assuming a 10% annualised return, the ISA portfolio grows steadily year after year. By age 18, the ISA has already passed £180,000.

And this is where the real compounding starts. By 30, it’s nearing £680,000. Continue holding it — and making contributions — and by age 35 the pot has passed £1.1m. By age 40, it exceeds £1.8m.

The power of compounding

This remarkable growth isn’t down to luck or market timing, but rather the mathematical power of compounding returns over time. The earlier the investing journey starts, the more time capital has to snowball.

This snowballing can happen even from a relatively small base. And because a Stocks and Shares ISA allows tax-free growth and withdrawals, it offers a uniquely efficient vehicle for long-term wealth-building.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

It’s important to remember however, that the stock market carries risk. Returns aren’t guaranteed, and investments can fall as well as rise. The 10% annualised return used here is for illustrative purposes only, based on long-term historical averages like the performance of the S&P 500.

Still, the underlying message is really compelling. Early action coupled with regular contributions and patience can build a seven-figure portfolio for a child. Whether it’s for their first home, education or retirement, giving children a financial head start could be one of the most valuable legacies a parent can offer.

Where to invest?

There are several intelligent ways to start. And unless you’re a seasoned investor, the common theme is diversification. An investor may plan to focus on individual stocks and buy, say, two stocks a month, balancing diversification with highconviction investment opportunities.

Or, they may wish to start by investing in a trust or fund. I’d add that I’ve employed both strategies for my daughter’s ISA and Self-Invested Personal Pension (SIPP). The ISA is composed of 20-30 stocks with strong quantitive scores and the SIPP is more trust- and fund- focused.

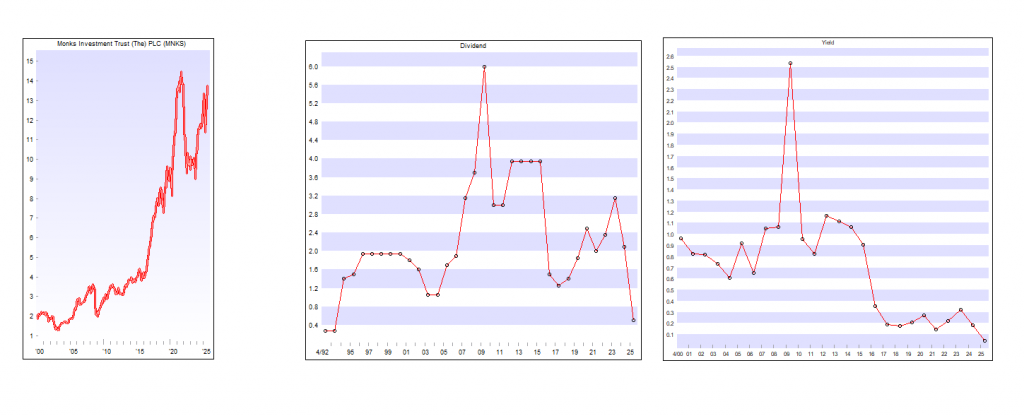

With regard to investment trusts, one present in her SIPP and my pension is The Monks Investment Trust (LSE:MNKS). While it’s lagged its sister portfolio — Scottish Mortgage Investment Trust — over the past decade, it’s actually up 21% over the past year.

Monks’ diversified yet growth-focused approach aims to avoid overexposure to any single theme, while still capturing the appreciation of global innovators. Alongside US tech, it holds stakes in Taiwan Semiconductor, Prosus, and even Ryanair, reflecting a broad geographic and sector mix.

Its inclusion of The Schiehallion Fund — an illiquid vehicle focused on private growth companies — adds another unique angle, though it introduces valuation risk in less transparent markets.

While Monks isn’t as volatile as Scottish Mortgage, it still carries the usual risks associated with equity investing. It also practices gearing — borrowing to invest — which can amplify losses when the market reverses.

There is a very wide spread with MNKS, so be very careful in case the market turns.

Will Stocks Drop Again? Here’s My Take (and an 8.5% Dividend to Profit)

by Michael Foster, Investment Strategist

Volatility is back! And we contrarians know what to do: Get ready to buy. And we don’t have to try to time the depths of the next selloff, either, because the three 7%+ paying, “volatility-loving” dividends we’re going to talk about are perfect for this market. They’re all closed-end funds (CEFs) that see their cash streams grow when markets get skittish. Their secret? They sell covered-call options on their portfolios. This is a smart, low-risk way they can generate extra income – and send it our way as 7%+ dividends. That’s because these funds charge investors a “premium” for the “option” to buy their holdings at a fixed time and date in the future.

They keep that cash no matter what happens with the trade itself. And their dividends (and our income) directly benefit.

If you’ve been reading my column for a while, you’ll recognize these three covered-call CEFs: the 8.5%-paying Nuveen Dow 30 Dynamic Overwrite Fund (DIAX), the 7.6%-yielding Nuveen S&P 500 Dynamic Overwrite Fund (SPXX) and the 8.5%-paying Nuveen NASDAQ 100 Dynamic Overwrite Fund (QQQX).

Investors Go From Greed to Uncertainty. What’s Next?

I also bring these funds up now because, despite the media’s howling, the current market is simply following an age-old course.

It goes like this: As stocks rise, a major news story sparks worries that their gains can’t last. Stocks then sell off on rising investor fear, until the “smart money” comes in to buy the dip. Then the rest of the crowd takes notice and stocks begin to recover.

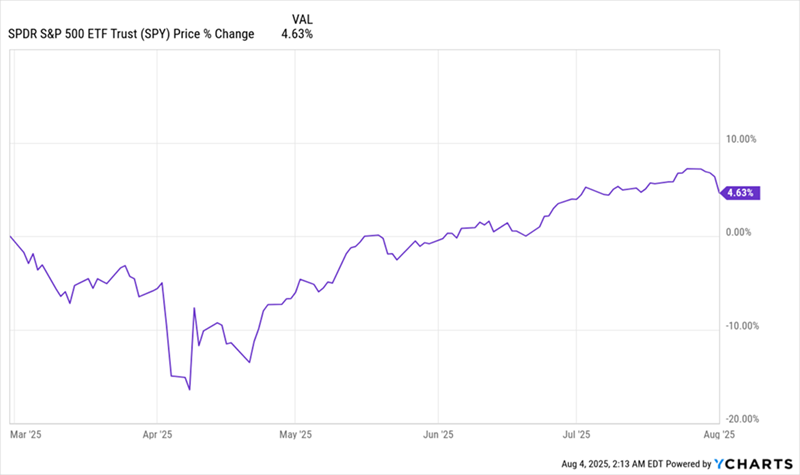

Usually, this cycle happens over a short period – a few weeks, maybe a month or two. A good example is the sharp selloff, and speedy recovery, after President Trump announced large tariffs in April.

However, a negative mood can hang on and prolong a selloff. That’s what happened in 2022, when worries of an economic crisis emerged after 2021’s huge run. But that turned out to be wrong, and the economy didn’t start contracting that year, or in 2023, or even in 2024.

As a result, stocks recovered, but it took a long time as pundit after pundit wrongly insisted a recession was on its way.

Okay, so why am I giving a history lesson here? Because we may very well be on the precipice of a new selloff, with volatility rising again. The trigger was that disappointing jobs report from the Bureau of Labor Statistics last Friday, which included large downward revisions to the previous two months’ readings.

It’s worth noting, however, that the economy is still adding jobs, and, if we look at the last five years of data, we’re still far from the calamities of the pandemic.

In other words, we’re in the fearmongering stage of the cycle, with the media running story after story about the so-called “big drop” in the labor market.

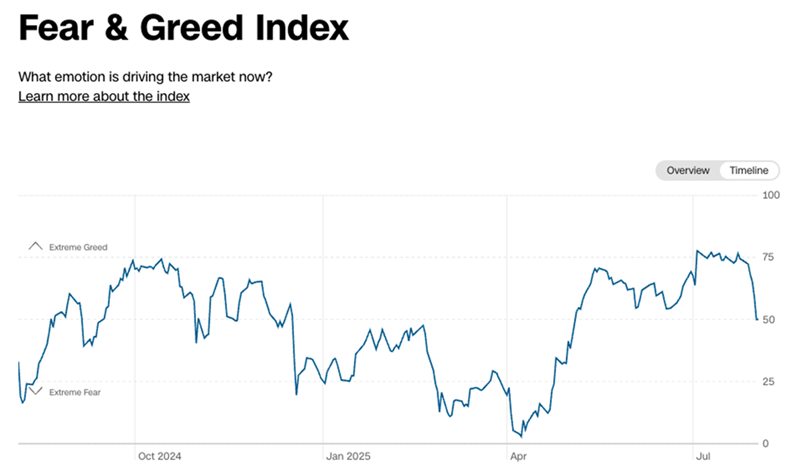

A quick look at the CNN Fear and Greed index, as of this writing, shows us that the extreme-greed mood of the last couple months has flipped to neutral, where it was in March and again at the end of April, after the huge crash earlier that month. However, it’s worth noting that stocks are up both from the end of April and from March.

Neutral Sentiment = Stock Profits So, if sentiment is cooling, we may see stocks sell off in the short term, then recover strongly a bit later. That’s the scenario I find most likely at this time.

Short-Term Volatility: How to Respond

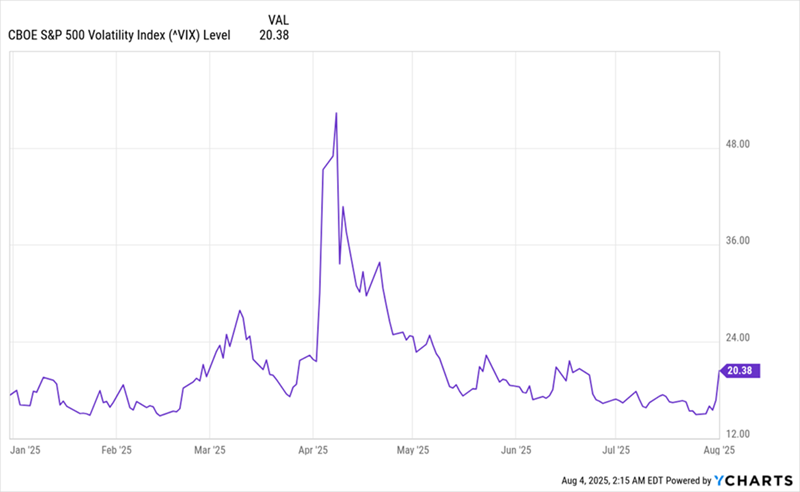

One interesting thing about the current market is that, while volatility has jumped a little, it’s nowhere near the spikes associated with big, steep selloffs. This tells us that a near-term selloff isn’t guaranteed, and one will likely only emerge if the current level of the VIX – the market’s so-called “fear gauge” – rises.

VIX Rising, but Still Muted As you can see above, the VIX recently spiked from an unusually low level, meaning the market is waking up from weeks of complacency. Obviously, in such a market, you can’t just sell everything: If things stay flattish, you might be able to buy back in, but you’ll miss out on dividends.

And if stocks see a short-term decline, who’s to say how low it will go and how long it will last? This doesn’t feel like a 2022-style drop, partly because Americans are less fearful than they were shortly after the pandemic. So a short-term market dip is the likeliest outcome, with a flat market a close second.

In such a market, the best move is to monetize rising volatility. That’s where our (still-) available opportunity on those three covered-call CEFs comes in.

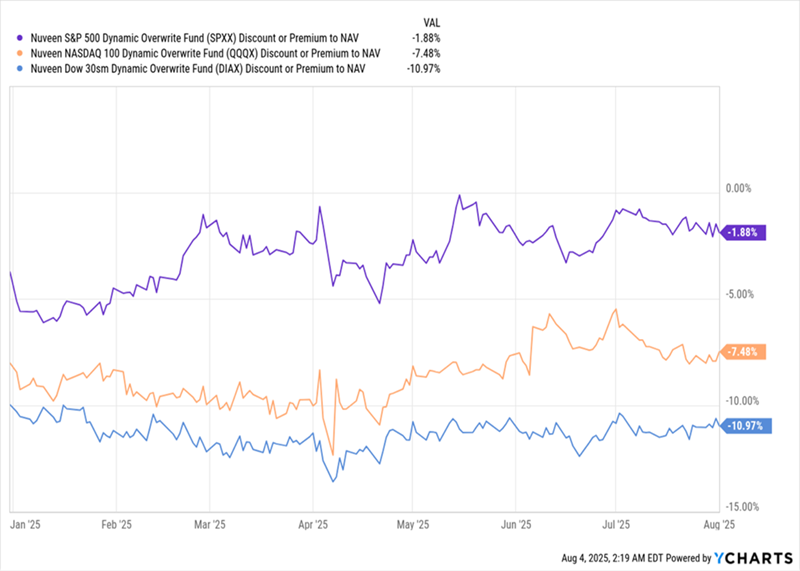

We’re interested in these three because their call options essentially turn rising fear into cash. Plus there’s a big difference in their discounts to net asset value (NAV, or the value of their underlying portfolios) we can take advantage of.

DIAX Is Unusually Cheap Now Note that DIAX (in blue above) trades at a near-11% discount to NAV as of this writing, even though its 8.5% yield matches that of QQQX, which has a much narrower 7.5% discount. And SPXX, with its smaller 7.6% yield, trades at just a 1.9% discount!

This is odd, since CEF investors love high yields and tend to price up higher-yielding funds. And as of now, SPXX pays the least and has the smallest discount. That’s the one part of this that makes sense, and the reason is fairly straightforward: The S&P 500 is the best-known index, so many investors blindly pile into SPXX for that reason.

But consider the fact that DIAX has a higher yield (8.5%, you’ll recall), a bigger discount (nearly 11%, as shown in the chart above) and holds solid blue chips like 3M (MMM), American Express (AXP), Boeing (BA), Coca-Cola (KO) and Procter & Gamble (PG).

This means it’s likelier to see higher volatility in the short term (especially since its portfolio only includes 30 stocks – those in the Dow). But that’s a plus, as these option strategies do best in volatile markets. That should raise demand for DIAX, causing its near-11% discount to shrink. And that’s why, right now, DIAX is a compelling hedge for short-term volatility.

“TRIG” or “the Company”, a London-listed renewables investment company advised by InfraRed Capital Partners (“InfraRed”) as Investment Manager and Renewable Energy Systems (“RES”) as Operations Manager.

Announcement of Interim Results for the six months to 30 June 2025

£199m of operational cash generated despite low wind resource in the UK, France and Germany:

· In line with the expectation set out in the Q1 2025 Net Asset Value (“NAV”) update, dividend cover was 1.0x in the period (30 June 2024: 1.1x), or 2.2x before the repayment of £105m of project level debt. TRIG’s dividend guidance of 7.55p/share for FY 2025 is reaffirmed by the Board.

· Generation in the period was 10% below budget driven by poor wind resource.

Should You Buy the 3 Highest-Paying Dividend Stocks in the Dow Jones?

James Brumley, The Motley Fool

Wed, August 6, 2025

Key Points

A handful of the 30 stocks that make up the Dow Jones have lagged, inflating their dividend yields.

This poor performance points to the market’s credible concerns about each company’s foreseeable future.

Merck, Chevron, and Verizon each need to be considered carefully based on their prospects ahead.

The premise makes enough sense on the surface. Not only does a higher dividend yield mean more income per invested dollar, it may also mean the stock in question is undervalued and ripe for a rebound.

That’s particularly true when you’re talking about the blue chip stocks found within the Dow Jones Industrial Average. There’s even a stock-picking strategy called the “Dogs of the Dow” based on this very idea.

But before plowing into the Dow’s three highest-yielding stocks just because their yields are big, remember that every one of your stock picks should first and foremost be based on the quality of the company in question.

With that as the backdrop, here’s a closer look at the Dow Jones’ three highest-yielding tickers right now. You may end up liking all three of them enough to add them to your portfolio. Or, maybe not.

Why so high?

The highest-paying dividend stocks in the Dow Jones Industrial Average right now are Verizon Communications (NYSE: VZ), Chevron (NYSE: CVX), and Merck (NYSE: MRK), sporting trailing yields of 6.4%, 4.5%, and 4% (respectively). But even if your primary goal is income, these big yields don’t inherently make the stocks worth owning.

Take Verizon as an example. Investors would struggle to find a higher-yielding ticker of this caliber. But the market’s allowed this stock to remain at relatively low levels mostly because investors know there’s little to no growth in store because the mobile phone market is so saturated.

Numbers from Pew Research indicate that 98% of all adults living in the U.S. already own and use a mobile phone. Any growth that’s going to be achieved by Verizon will mostly be driven by U.S. population growth, which has been and remains rather tepid.

Energy giant Chevron’s situation is different although not necessarily better. The world still needs oil and gas, but doesn’t need more and more of it. Goldman Sachs says “peak oil” — the point at which average daily usage starts to decline — is coming in 2035, but it’s only going to grow at a pace of less than 1% per year every year between now and then. Again, investors will want at least a little something more to build on.

As for Merck, a year ago you wouldn’t have been able to plug in at a yield anywhere near its current trailing yield of 4%. Shares have fallen more than 30% since then, starting with weakening sales of its HPV (human papillomavirus) vaccine in China, but more recently due to uncertainty linked to tariffs and the possibility that it will soon be forced to offer better drug prices to Medicare.

These sellers, however, have arguably overshot their target. For perspective, Merck stock’s trailing price-to-earnings ratio is now only a rock-bottom 12 versus the industry’s large-cap average of 22.6 (according to data from StockAnalysis), underscoring the extreme degree of concern that investors have priced in.

To buy, or not to buy?

But the question remains: Are these high-yielding Dow stocks a buy? As a group? No. Individually? It depends.

Rules-based investing certainly has its advantages. Chief among them is the removal of often-misleading emotions and assumptions from the decision-making progress. And purchasing the highest-yielding names from a relatively small universe of stocks is most definitely a rules-based approach to stock-picking.

Except, maybe this particular premise isn’t one you want to blindly embrace. While it’s a solid starting point, as was noted, selecting stocks is still done best on a case-by-case basis to meet specific portfolio needs.

Consider Verizon. With a trailing yield of 6.4% based on a quarterly dividend payment that’s not only been paid like clockwork but raised every year for the past 18 years, it’s one heck of an income investment. Investment-grade bonds aren’t paying as much. Just don’t count on any meaningful capital appreciation.

There’s a reason Verizon shares are currently priced where they were over 25 years ago, and it’s not just the company’s high level of debt.

Chevron shares have fared far better, at least until 2022’s peak. They’ve only drifted lower since then, more or less in step with the continued proliferation of alternative energy sources and the outright explosion of electric vehicle sales.

Notably, crude oil prices have also drifted lower during this stretch despite a couple of major supply disruptions stemming from political tensions in the Middle East. This may be the new norm for the industry that’s likely nearing a peak and subsequent pivot point. In this vein, the United States’ Energy Information Administration believes Brent crude prices are set to fall from an average of $81 per barrel last year to $66 this year to $59 per barrel in 2026.

There’s still plenty of money to be made drilling for oil, to be clear, simply because the world will still need it for years to come. Chevron’s also now upped its dividend for an incredible 38 consecutive years. It’s going to become increasingly challenging for the company to maintain this streak indefinitely, though, given that roughly half of its usual — but now pressured — annual earnings are used to fund its dividend payments.

As for Merck, there’s certainly plenty of value here. There’s also plenty of cause for concern. Even if Medicare’s pricing-pushback efforts don’t end up turning into a serious problem for its bottom line this time around, this political undertow isn’t simply going away.

Image source: Getty Images.

Just don’t lose perspective on the matter. Pharmaceutical companies have been facing these sorts of legislative and policy headwinds for decades. The industry has survived them just fine.

Merck is no exception, and it’s not apt to become one anytime soon. Its cancer-fighting Keytruda remains a powerful profit center, for instance, accounting for half of its revenue thanks to last quarter’s 9% year-over-year sales growth. And while Keytruda’s patent protection doesn’t start expiring in earnest until 2028, the drugmaker’s got a robust developmental pipeline set to replace much of the revenue that will be lost once Keytruda’s sales start to wane.

There’s always more to the story

The bigger point is, Merck’s got ways of evolving itself as needed. It always has. This discounted price and beefed-up dividend yield is a great buying opportunity. Just be sure you’re committed for the long haul. It will take a while for the market to remember this about the pharma company and reprice the stock appropriately.

The more philosophical takeaway here, of course, is that a high yield alone isn’t enough of a reason to buy a stock even if that stock is a part of the Dow Jones Industrial Average. The underlying business must also be one worth owning, and you must also actually want and need dividend income. Just keep the bigger picture in mind.

Brett Owens, Chief Investment Strategist Updated: August 6, 2025

Monthly bills are no problem for careful contrarian readers banking 8.8% yields in monthly divvies. Let’s discuss this rare but excellent dividend breed, the company or fund that pays monthly instead of quarterly.

Only 6% of dividend payers dish monthly. The rest are quarterly or annually, which will likely not be in time to cover your upcoming cell phone bill.

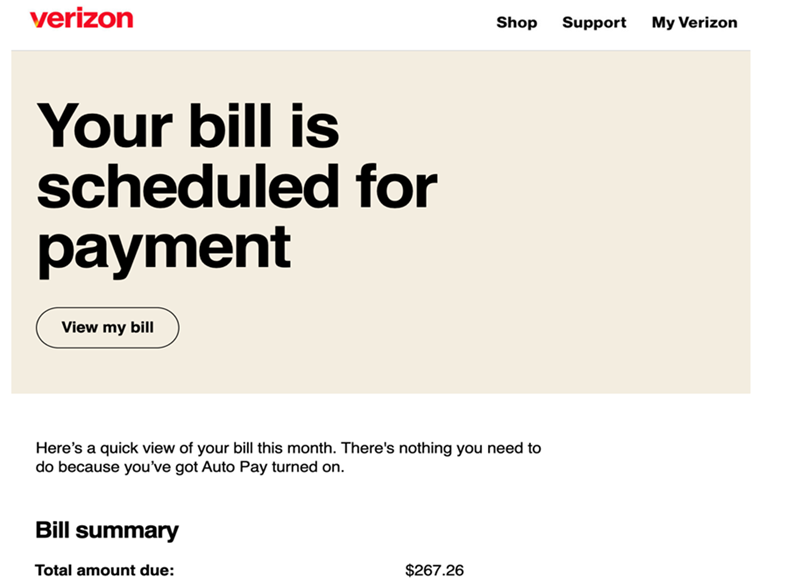

My monthly email from carrier Verizon arrives in a day or two. Another $267.26 will be debited from my account automatically on the 20th of August.

Fortunately, Verizon notes that there is “nothing I need to do” thanks to AutoPay. As if the automatic payment implies it costs any less money!

On the bright side of the phone ledger, we have no landline. The cell bill is it. But don’t fall asleep, bank account. All the other cord cutting exacts its pound of flesh!

For example, we “cut the cable cord” years ago. And replaced it with an equally pricey version, albeit a wireless one!

YouTube TV has a base plan of $82.99. However, my August 29 tab will be $131.95 plus tax.

How’d I manage a 50%+ premium? By demanding sports in 4K (+$9.99/month). And refusing to live a Sunday in the fall without NFL RedZone and its 6+ hours of live look ins across football games (+$10.99/month).

Oh, and the WNBA season ticket that I watch with my daughters during the summer.

Speaking of which, A/C is a must-have here in Sacramento! I paid the power company $187.76 two days ago and that’s a light month for our summers.

But the big one, the mortgage payment, dwarfs all. And oh yes, automatically deducted from our account on the first of August.

“Just” eleven years to go on the mortgage! We shortened to 15-years when we refi’d in 2021. My “basketball dad” car is paid off (2019 Acura MDX) and, while motivated to drive it “into the ground,” the odds are this car won’t be my last.

So the big monthly payment wheel keeps on spinning. I am sure you can relate to a few of these regular drains in your own life.

For which we have a solution: plug these monthly drains with monthly dividends.

But you observe, “Brett! You said only 6% pay monthly. How can I find them?”

Glad you asked! Our Contrarian Income Report has a “virtual monopoly” on the sector. We have 18 monthly payers yielding an average 8.8%. Think about that. A million bucks in the CIR monthly payer lineup generates $7,333.33 per month in passive income.

Plus, the original million invested in these “elite 18” stays intact. Or better yet, grinds higher! Since inception 10 years ago, our entire CIR portfolio has generated 10.7% in annual returns. And that’s mostly paid in cash dividends, with the majority dishing monthly.

Our CIR monthly dividend GOAT (greatest of all time) is DoubleLine Income Solutions Fund (DSL). In April 2016, we added DSL to the CIR portfolio at a price of $16.99 per share.

Since then we have collected 111 monthly dividends that have totaled $15.27. That’s 90% of our initial buy price in payouts. It’s almost house money now!

Imagine investing in a simple fund that trades just like any blue-chip stock—and earning your entire investment back within 10 years via monthly dividends. With the regular payout stream still rolling strong!

And DSL is not a mere annuity. It’s way better. DSL is a bond fund run by the “bond god” himself Jeffrey Gundlach. The modern-day deity of fixed-income investing scours the globe to collect deals that power DSL’s monthly 11-cent divvie.

DSL yields 10.9% today. Investors with $100,000 invested in DSL shares enjoy $10,900 per year in passive dividend income. That’s $908.33 in monthly deposits and—oh!—that’s right: it’s autopay, but to you!

Enough to pay Verizon, YouTube TV and internet while air conditioning the house—with extra cash left over for a nice dinner!

And a $50,000 stake in DSL delivers $454.17 in monthly payouts. That’s still meaningful income to cover those every-30-day expenses.

Now, I wouldn’t pile everything into DSL today, when savvy investors can spread risk among 17 more solid monthly payers that deliver a green cash river too. This is diversification without di-worseification (thank you, Peter Lynch!). We want to retire on dividends, and the best way is to bulletproof our payout streams across asset classes, sectors and national borders.

And that’s our elite 18!

We are not hanging on the Federal Reserve’s next word. Nor are we glued to policymaker decisions. We are insulated from this noise by assembling an elite 8.8% paying portfolio of monthly dividend payers.

If this monthly dividend discussion sparked an “ah ha!” moment for you, well, welcome! Wall Street has been feeding you the equivalent of “junk food” financial advice your entire life.

The 4% withdrawal rule? C’mon man.

None of the vanilla maxims generate passive income. Annually, monthly or quarterly!

It’s time to clean up the financial diet. Trim down the “buy and hope” desperation and beef up the dividends.

NextEnergy Solar Fund, a leading specialist investor in solar energy and energy storage, is pleased to announce its first interim dividend of 2.10p per Ordinary Share for the quarter ended 30 June 2025, in line with its previously stated target of paying dividends of 8.43p per Ordinary Share for the year ending 31 March 2026.

The first interim dividend of 2.10p per Ordinary Share will be paid on 30 September 2025 to Ordinary Shareholders on the register as at the close of business on 15 August 2025. The ex-dividend date is 14 August 2025.

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

The higher interest rate environment is putting a lot of pressure on these debt-ridden businesses. But with rates steadily falling, and many continuing to generate stable cash flows, dividends are still being put in investor pockets.

The combination of dividends with lower share prices has steadily pushed yields higher over the last couple of years. As such, some yields are now starting to climb beyond 8% !

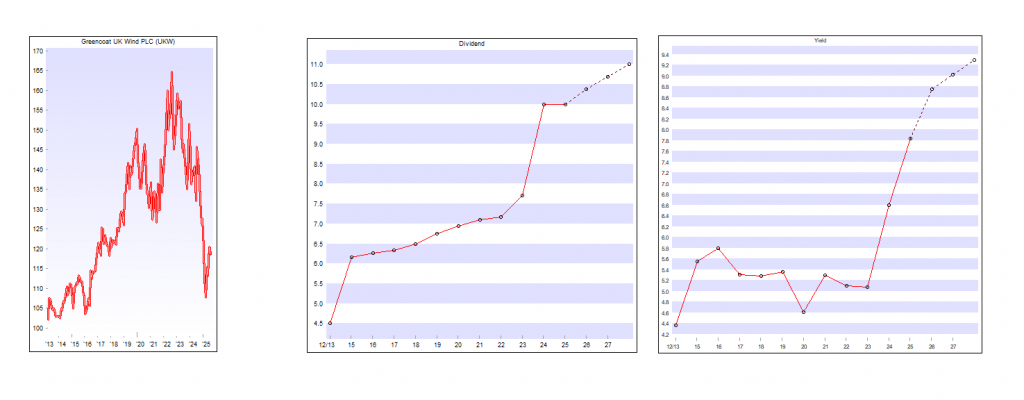

Greencoat UK Wind‘s (LSE:UKW) a prime example of this, with its payout now stretching beyond 8.5%. That’s a little lower than a few months ago, but it’s still the highest level seen in over a decade. And based on current guidance, dividends, even at this massive yield, are set to grow even further in the coming years.

Greencoat manages a portfolio of onshore and offshore wind farms throughout Britain. Instead of collecting rent, it sells clean electricity to the national grid. And since energy’s in constant demand, it enjoys a relatively stable cash flow to fund shareholder payouts.

However, with so much profit being paid out, these businesses are often almost entirely dependent on external financing. As such, they tend to be highly leveraged enterprises. That was fine for most of the last 15 years. But when interest rates started climbing again, high debt burdens proved quite troublesome.