I think that everything said was very logical. But, what about this? what if you were to create a killer headline? I mean, I don’t wish to tell you how to run your website, but what if you added a post title that makes people want more? I mean IF – Passive Income is a little vanilla. You might look at Yahoo’s home page and watch how they create post titles to grab viewers to open the links. You might try adding a video or a pic or two to grab readers excited about everything got to say. Just my opinion, it could make your posts a little bit more interesting. https://6t4q8.mssg.me/

Investing one’s hard earned to make your retirement comfortable is serious and not to be approached lightly. The headlines are provided as way for readers of the Snowball to carry out their own research.

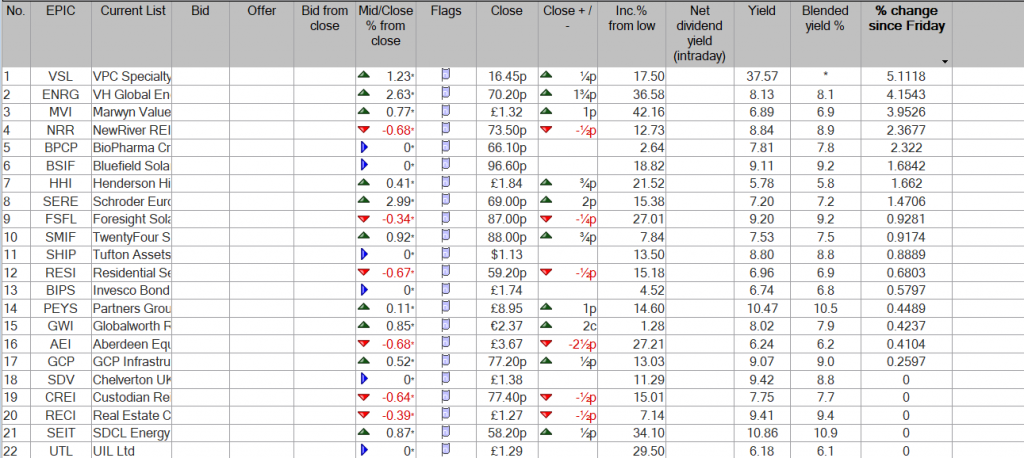

All the profit is currently from the earned dividends. SEIT is currently overweight in the Snowball and would be reduced if the price continues in an upward direction. Current yield 10.9% and the £1,228 has been re-invested in the Snowball and earning dividends both amounts to be re-invested in the Snowball to earn more dividends.

Only one year into the holy grail of investing, so a lot of water to flow under a lot of bridges before that is achieved, if ever.

My name is Brett Owens and I’m an unabashed dividend investor.

Monthly Dividend Superstars: 8% Annual Yields With 10%+ Price Upside, Too Most investors with $600,000 in their portfolios think they don’t have enough money to retire on.

They do – they just need to do two things with their “buy and hope” portfolios to turn them into $4,000+ monthly income streams:

Sell everything – including the 2%, 3% and even 4% payers that simply don’t yield enough to matter. And,

Buy my favorite monthly dividend payers.

The result? More than $4,000 in monthly income (from an average annual yield just over 8%, paid about every 30 days). With upside on your initial $600,000 to boot!

And this strategy isn’t capped at $600,000. If you’ve saved a million (or even two), you can just buy more of these elite monthly payers and boost your passive income to $6,660 or even $13,320 per month.

Though if you’re a billionaire, sorry, you are out of luck. These Goldilocks payers won’t be able to absorb all of your cash. With total market caps around $1 billion or $2 billion, these vehicles are too small for institutional money.

Which is perfect for humble contrarians like you and me. This ceiling has created inefficiencies that we can take advantage of. After all, in a completely efficient market, we’d have to make a choice between dividends and upside. Here, though, we get both.

Inefficient Markets Help Us Bank $100,000 Annually (per Million) Fortunately for you and me, the financial markets aren’t 100% efficient. And some corners are even less mature and less combed through than others.

These corners provide us contrarians with stable income opportunities that are both safe and lucrative.

There are anomalies in high yield. In an efficient market, you wouldn’t expect funds that pay big dividends today to also put up solid price gains, too.

We’re taught that it’s an either/or relationship between yield and upside – we can either collect dividends today or enjoy upside tomorrow, but not both.

But that’s simply not true in real life. Otherwise, why would these monthly payers put up serious annualized returns in the last 10 years while boasting outsized dividend yields?

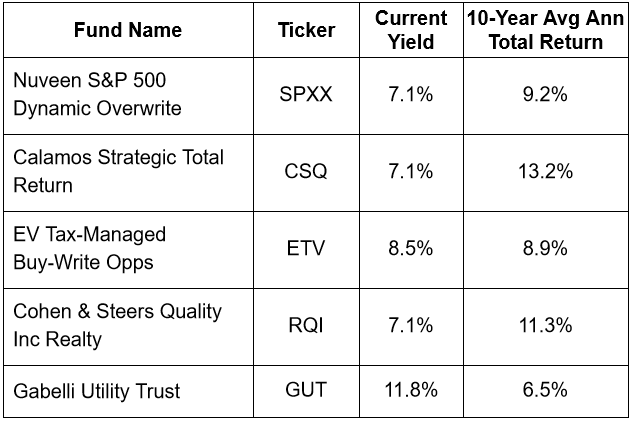

For example, take a look at these 5 incredible funds that pay monthly and soar:

This is the key to a true “8% Monthly Payer Portfolio” – banking enough yields to live on while steadily growing your capital. It’s literally the difference between dying broke and never running out of money!

But I’m not suggesting you run out and buy these funds.

Some have been on my watchlist and in our premium portfolios over the years, but I mention them only as examples of the potential ahead.

How to earn a passive $40,000 on a half-million … $80,000 on a million … and $100,000+ annually on anything higher. And get paid every month, too.

Plus, you won’t even have to tap your initial capital or “draw down” any of your valuable principal.

How much do you need in an ISA to aim for £10,000 a month in passive income?

Millions of us invest for passive income. Here, Dr James Fox explains how much money an investor would need in an ISA to make £120k a year.

Posted by Dr. James Fox

Published 10 August

Image source: Getty Images

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

Earning £10,000 a month in passive income is a financial milestone that many UK investors aspire to. Whether it’s to fund an early retirement, achieve financial independence, or simply provide peace of mind, reaching this level of income is possible.

However, it requires careful planning and a well executed strategy. And, of course, it makes sense to do this through a tax-efficient Stocks and Shares ISA.

With its exemption from income and capital gains tax, the ISA’s a powerful tool for UK investors. But generating £120,000 a year in passive income from an ISA alone is a tall order. To reach that level of cash flow without drawing down capital would need a substantial portfolio. What’s more, investors would need an asset allocation designed to yield reliably

So how much?

So how much is “substantial”? The answer depends on several variables. Chief among them is the average yield of the investments held within the ISA.

A portfolio yielding 4% annually would require a value of £3m to produce £120,000 a year in income. At a 6% yield, the required capital falls to £2m. Of course, higher yields often come with greater risks, including income volatility as well as capital erosion.

Now, many readers may have zoned out at £2m or £3m. However, for those starting early enough, reaching these figures is very possible.

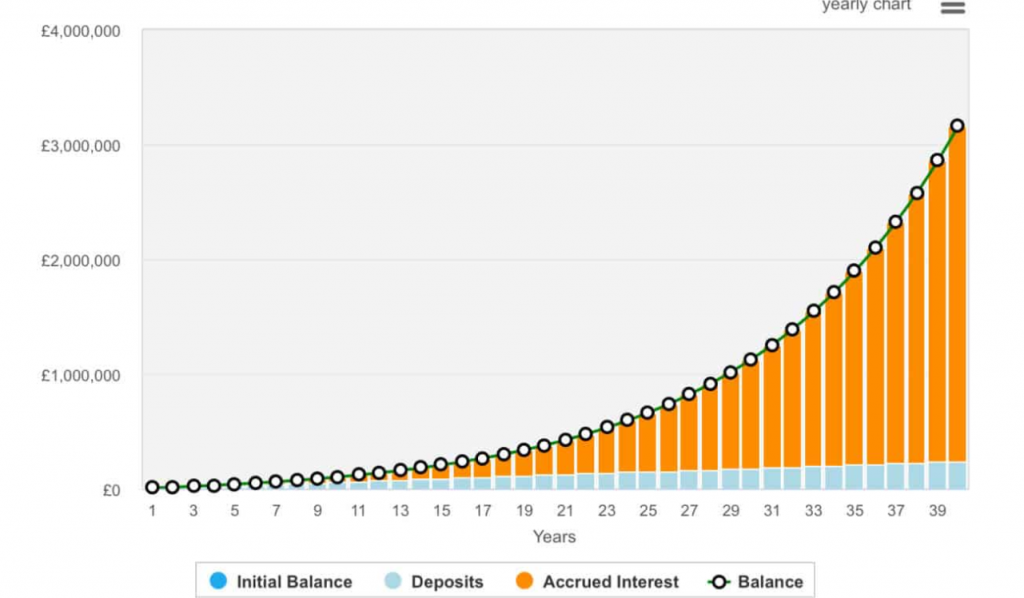

Take the case of investing £500 a month over 40 years with 10% annualised returns. In the first decade, progress can feel modest. After 10 years, the portfolio’s worth just over £100,000.

Source: thecalculatorsite.com

But compounding begins to accelerate. By year 20, the balance grows to around £380,000, and by year 30 it passes £1.1m. In the final 10 years, growth becomes dramatic: the portfolio adds over £2m, ending above £3.1m by year 40.

Despite contributing just £240,000 in total, over £2.9m comes purely from reinvested gains. This is the exponential nature of compounding. It starts slow, then surges.

Of course, it’s not all plain sailing. There are risks involved with investing, and we can lose as well as gain money. What’s more, 10% may prove to be a challenging target for some investors.

An investment for the long run?

Investors typically want to strive for diversification. One way to do that is by investing in 20-30 individual stocks, another is to focus on in a handful of investment trusts or funds.

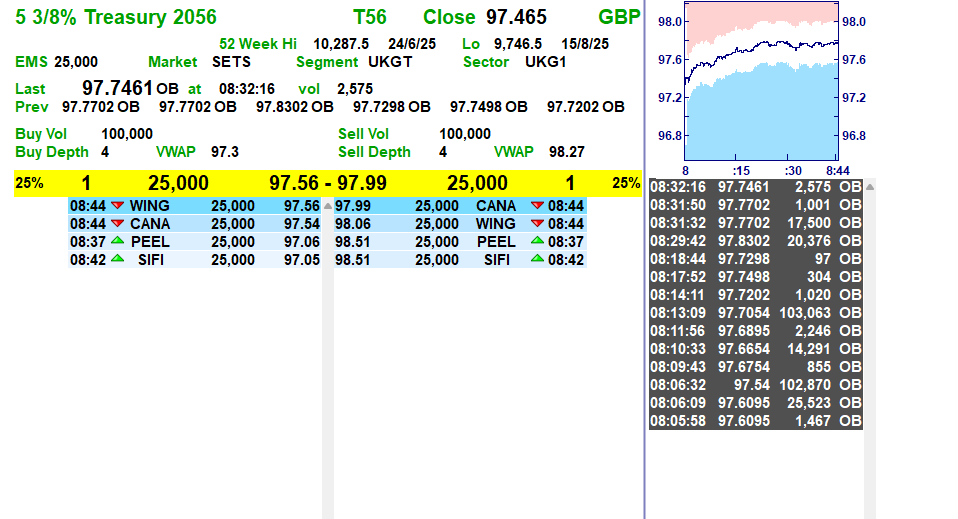

If you used T56 as a core constituent of your Snowball, you would receive two payments a year with a total yield of 5.46%. If held in a tax free account you could buy and forget about the Gilt, it’s likely the capital value may fall a touch but as you intend to buy and hold forever it’s of no concern.

A minimum blended yield of 7% for your Snowball is recommended, as if this is re-invested at a yield of 7% plus this doubles your income in ten years.

If for comparison purposes only, you pair traded with NESF

The blended yield would be 16.5%, you have reduced the overall risk to your portfolio and achieved a yield of 8%. This could then be re-invested into your portfolio.

Two funds in Vanguard’s LifeStrategy range rose in popularity last week. Costing 0.22%, the version that has 80% invested in equities and 20% in bonds rose one place to fourth, while the 100% equities version rose three places to sixth. They are “funds of funds”, built using Vanguard’s own index funds, providing a useful one-stop shop for investors seeking global stock and bond market exposure.

0.44%, which rose three places to third. It has a dividend yield of 8.5% and owns wind farm assets across the UK.

The final riser was Fidelity Index World, which was a new entry in 10th. This fund was one of three global equity passive funds to make last week’s top collectives list. It tracks the MSCI World index of developed market shares for a 0.12% annual fee.

0.05% dropped in popularity last week but held on to their spots on the most-bought list. Respectively, they are actively managed portfolios of income and shares and growth shares.

UK equity income investment trust City of London dropped off the list.

Cash Will Be King Soon, 4 Out Of 5 Market Top Signs Are Here

Aug. 15, 2025

Summary

I’m selling into market strength, as underlying weakness and red flags suggest we’re near a market top, despite record index highs.

Key sectors like transportation, consumer discretionary, and real estate are showing signs of strain, while jobs data is weakening.

Market breadth is dangerously narrow, margin debt is at record highs, and speculative trading is rampant—classic signals of a topping market.

I’m raising cash now, believing caution is wise; cash will be king when the next market pullback offers better opportunities.

Daniel Grizelj/DigitalVision via Getty Images

The stock market is doing great and it has been making new record highs. The momentum could carry it higher for a while, but I am using this as an opportunity to sell into strength, because not all is well when you dig deeper and beyond the major indexes. I am not a huge bear, and I am keeping my core holdings for the long term, but I am skeptical and I believe cash will be king as soon as this Fall. Let’s take a closer look below at some points of concern and also at 5 of the indicators that often signal a market top.

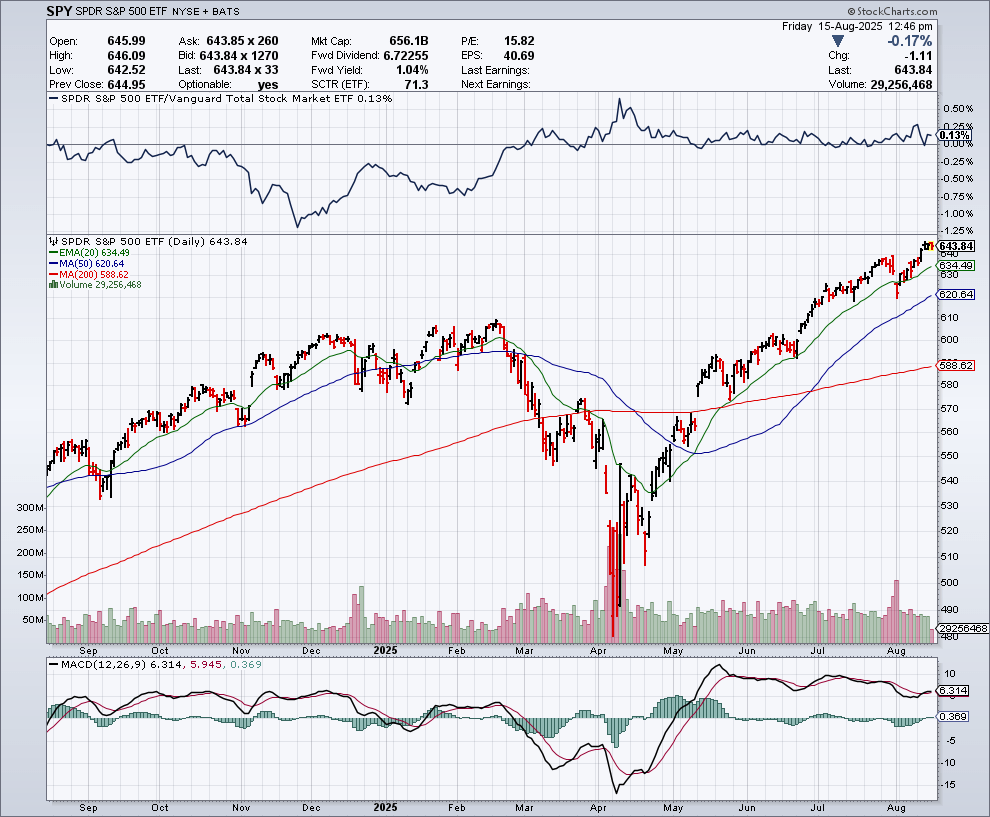

The Chart

When I look at the chart of the S&P 500 Index (NYSEARCA:SPY) below, it looks like we are potentially at or near the blow-off top stage of this bull market. I certainly do not look at this chart and say that this is when I want to be adding more money and risk to my portfolio.

StockCharts.com

Why Things Are Not So Great Under The Surface

The market strength in terms of the indexes looks great but there is underlying weakness in some important segments of the market such as the transportation stocks and consumer discretionary. For example, UPS (UPS) is trading near 52-week lows. FedEx (FDX) is way below the 52-week high. A major European container shipping company recently warned that high global tariffs could slow down volumes in the coming months. When things aren’t being shipped, it means they aren’t being sold and this weakness in shipping volumes is a major concern.

The real estate market appears to be in correction mode in many parts of the country. I am seeing price cuts where I live in California that I have not seen in years. I am also seeing homes sit on the market for months in many cases. Companies like Whirlpool (WHR) recently reported challenges with tariffs and weaker than expected results. Lower home prices could lead to weaker consumer sentiment as a potential negative wealth effect from real estate takes its toll.

The jobs market seems to be shifting rapidly and this could be the start of a new and very negative trend. On August 1, the Bureau of Labor Statistics released the jobs report which showed July non-farm payroll growth was just 73,000. This was much lower than the expectations for 110,000. But it gets worse, because payrolls for May and June were revised down by a total of 258,000. This means the job market weakness really started earlier this year and we are only starting to recognize the start of this potentially new trend now.

A Tariff 2.0 Growth Scare Could Be Coming

The stock market recovered from a brutal decline in April after President Trump announced the Liberation Day tariffs. The stock market is back at new highs, and consumers have not seemingly been hit with big price increases. So, it now seems like we can have a huge increase in tariffs that brings billions of dollars in new revenues to the U.S. Government and there is really no impact or downside.

However, this could be false hope, and we could be in the “quiet before the storm” period. That’s because there is a major lag time for tariffs to take effect and to hit with full impact. We have to realize that many countries were able to defer tariffs during the negotiation period and many companies stockpiled raw materials and other items. Many businesses have also held back on raising prices because there has been uncertainty as to whether or not tariffs would remain high or be negotiated away. A recent CNBC article says that higher prices might be coming in September, according to some analysts and this is based on seasonal inventory patterns and products that are working their way through the supply chain system. I believe it is way too early to suggest that we are in the clear when it comes to tariffs and the potential inflationary impact.

A Number Of Indicators Of Market Tops Are At Red Flag Levels Now

They often say that no one rings a bell at the market top, but there are multiple indicators that seem to be ringing a bell, for anyone who is willing to listen:

1) Narrowing Market Breadth: A healthy bull market has broad participation, but this bull market has been very dependent on mega-cap tech stocks which could be a warning sign of trouble ahead. A recent Goldman Sachs (GS) article points out that market breadth has been too narrow and it states:

“Although the S&P 500 has reached record highs, the median stock within the index is more than 10% below its 52-week high. This has lowered market breadth—a measure of how widely a market’s performance is reflected by its constituents—to its lowest level since 2023, according to Goldman Sachs Research’s market breadth indicator.

In the past, sharp declines in market breadth have often signalled below-average returns and larger-than-average drawdowns ahead.”

2) Excessive Euphoria And Margin Debt: We are hearing things that suggest we are in a new “Golden Age” and we are in a new era with AI and humanoid robots coming, all of which can seem limitless in terms of potential. Past market tops also had concepts that were touted as having incredible potential, such as the Internet/dotcom bubble. I believe there is excessive euphoria now and this often leads to investors believing that buying stocks is a no-can-lose proposition over the long run, even to the point where they are borrowing money to buy stocks. According to the latest statistics from FINRA, margin debt levels just went over $1 trillion in June 2025 and this is a new record. Since margin debt levels often hit record levels at or near market tops, I view this as another bell or warning signal that is going off right now.

3) Rising Interest Rates: This is often a problem for the stock market, but we are not seeing rising rates now, so this is the one indicator that is neutral and not ringing a bell. However, there is a case to be made that interest rates have been held up high for too long and that the damage might already be done. I think some of this damage is starting to show up in the jobs data.

4) Declining Economic Indicators: Earlier in this article, the weakening labor market was discussed, and this could be a major indicator of economic weakness, but there are others as well. New factory orders and durable goods orders fell in June and the ISM Manufacturing PMI showed in July that manufacturing is in a state of contraction. The ISM services index also declined in July, which is yet another potential warning sign. Lumber prices have plunged in recent weeks and this could be another sign of looming weakness in the economy.

5) A Surge In Speculative Trading: In the past couple of weeks we have seen a renewed meme stock rally whereby investors are buying into highly speculative stocks, which in some cases have very poor fundamentals. This is yet another potential red flag warning sign as this type of behavior is often seen at or near the market top. The record levels at which many cryptocurrencies trade is another sign of speculation. The stock market and other assets classes have clear signs of froth in certain areas and that will likely need to be flushed out.

In Summary

There are multiple signs that seem to suggest we could be at or near a market top. I definitely think it makes sense to be cautious when others are being greedy, and even using record levels of margin debt to buy stocks. I also believe that new stock market highs are being fuelled by a narrow part of the market and that this is masking some of the underlying weakness that has just started to appear in some of the manufacturing and services data as well as the jobs data. I think this is a great time to raise cash, and that cash will be king again and much smarter to deploy in the next big market pullback.

Just turned 40? Here’s how much you could have by retirement if you invest £500 a month via a SIPP

Worried about having enough money to retire on ? Investing regularly with a SIPP could potentially build a multi-million-pound nest egg!

Posted by

Zaven Boyrazian, CFA

Published 17 August, 7:21 am BST

Image source: Getty Images

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

The Self-Invested Personal Pension (SIPP) is one of the best retirement preparation tools available to British investors. While taxes do eventually re-enter the picture, the elimination of dividend and capital gains tax, along with income tax relief, drastically accelerates the wealth-building process. So much so that even when starting later at the age of 40, it enables investors to accumulate a substantial nest egg. Here’s how.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

Potential retirement wealth

Let’s assume an investor has just turned 40, is planning to retire at 65, and is currently in the Basic income tax bracket, paying a rate of 20%. Depositing £500 into a SIPP entitles them to 20% tax relief, transforming this monthly lump sum into £625. And investing this capital at the average stock market return of 8% a year for 25 years, compounds into a £594,392 pension portfolio.

Looking at the latest data from the Office for National Statistics, that’s just over four times what the average 65-year-old has saved up in 2025. And when following the 4% withdrawal rule, it’s enough to generate a retirement income of £23,775 a year.

Combining with the extra £11,973 from the UK State Pension, this simple investing strategy would put someone on the path to having a £35,748 passive income. And according to the Pensions and Lifetime Savings Association, that’s just over the £31,700 threshold needed to enjoy a moderate retirement in 2025.

Yet, when factoring in inflation, that threshold’s bound to rise over the next 25 years. Therefore, investors may need to aim a bit higher.