As a replacement share the Snowball is going to buy GCP Infrastructure.

GCP Infrastructure Investments Ltd (GCP) currently trades at a deep discount to NAV and offers a high yield, making it attractive for income-focused investors—but its elevated P/E ratio and sector headwinds suggest caution. Here’s a detailed breakdown to help you assess whether GCP fits your strategy.

📊 Valuation & Performance Snapshot

GCP Infra is a FTSE 250-listed, closed-ended investment company focused on UK infrastructure projects with long-term, public-sector-backed revenues.

It targets sustained, regular dividends, and its portfolio includes renewable energy, social housing, and PFI assets.

Recent buybacks suggest management sees value at current levels.

⚠️ Risks & Considerations

High P/E ratio implies stretched valuation relative to earnings.

Sector headwinds: Infrastructure and renewables have faced pressure from interest rate volatility and policy uncertainty.

Discount to NAV is wide, but may persist if sentiment remains cautious.

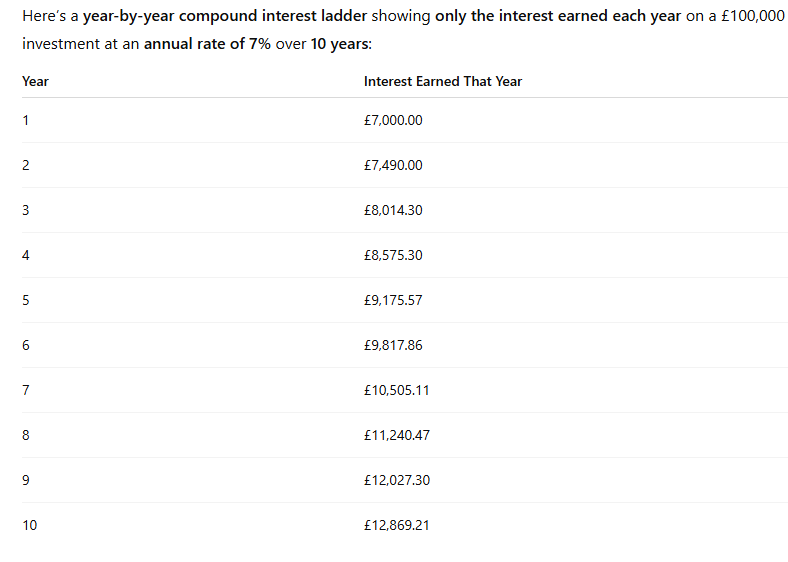

Fcast for 2025 income £11,500, which includes a special dividend from VPC.

It should mean the Snowball will achieve the year five figure in the above table which equates to year three of the plan, which hopefully means it will achieve the year ten figure several years early.

The 2026 fcast is £9,817.86, although next year as a working example I may include in the Snowball a pair trade, which might mean the income may miss the target in the near term.

In November there should be enough accrued dividends to complete the position in ORIT, then further earned dividends could be applied to a term trade.

Sale of stake in Simply Blue’s offshore wind platform

Octopus Renewables Infrastructure Trust plc, the diversified renewables infrastructure company, today announces that investee company, Simply Blue Holdings (“Simply Blue”), has signed a Share Subscription Agreement with Kansai Electric Power Company, Incorporated, to acquire an 80% stake in Simply Blue Energy OSW Ltd (“SBE OSW”), Simply Blue Group’s offshore wind development arm.

The transaction follows the recent carve-out of Simply Blue’s sustainable fuels business into a newly formed entity, Nova Scotia Fuels, and represents the next step in realising value from ORIT’s investment in Simply Blue Group’s platform business.

The transaction consideration is in line with ORIT’s latest holding value of Simply Blue. Proceeds from the transaction will be used in part to repay the shareholder loan facility held by ORIT, with the residual value retained through ORIT’s ongoing minority interest in Simply Blue.

Chris Gaydon, co-fund manager of Octopus Renewables Infrastructure Trust plc, commented: “This is a solid outcome in what remains a challenging market for offshore wind developers. It reinforces our confidence in the Simply Blue team and reflects the strength of the partnership with Kansai who are ideally placed to move this platform forward.”

Are we in a stock market bubble or not? Let’s tackle that question head-on, because it’s all we seem to be hearing about these days.

I’ll put my cards on the table: We’re not in a bubble. I’m going to show you why I’m still bullish on stocks at these levels. Then we’re going to play overwrought bubble fears with a “cornerstone” fund that’s beaten stocks over just about every timeline but is still cheap (and yields a rich 8%, too).

When it comes to stocks, the truth is, there’s a good reason why they keep rising: We’re in a booming economy.

Of course, you might not feel that way – many communities across America are suffering. Income inequality, crime, corruption – it’s a mess out there. Those are all serious problems, to be sure. But just as the stock market is not the economy, the stock market is not society, either, and those problems can co-exist with a rising market.

Where Earnings Go, Stocks Follow

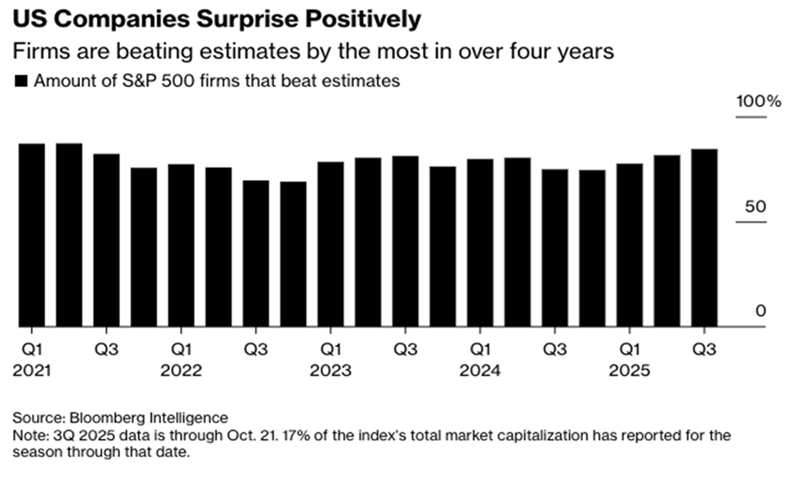

Stocks are rising because their moves are tied to one thing: earnings. And earnings are soaring.

Bloomberg recently reported on something we’ve been talking about for a while here at Contrarian Outlook and in my CEF Insider service: Earnings are growing as companies improve their profits through efficiency gains, some of which are driven by AI.

In fact, the earnings beats we’re seeing come from across the economy, from companies as diverse as General Motors (GM), Coca-Cola (KO), Morgan Stanley (MS) and, of course, tech names like Broadcom (AVGO) and Lam Research (LRCX).

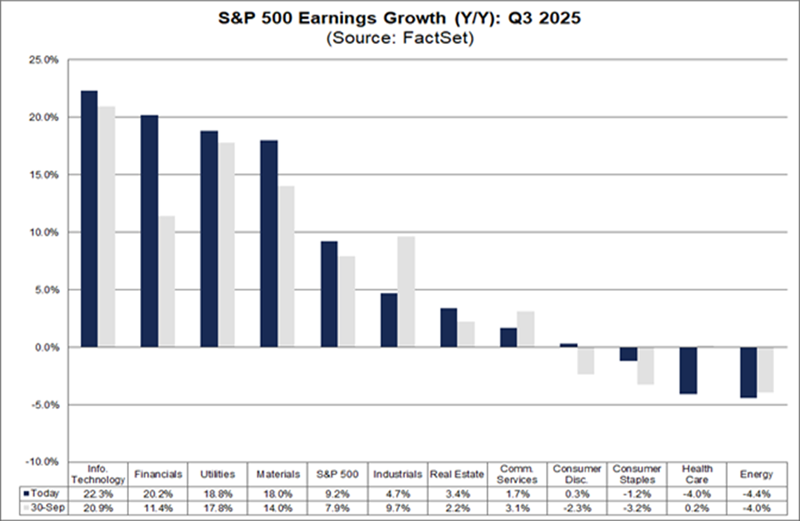

While tech continues to be the top-performing sector, there’s good reason to expect that more and more gains will come from outside of tech, as new innovations spread from that sector into other parts of the economy.

This doesn’t mean we should simply avoid tech and buy the rest of the market. After all, tech’s earnings gains are the strongest out there and will likely remain so, although financials are a close second.

At a time like this, we want broad-based market exposure. But of course, as my CEF Insider members know, we do not want an index fund. Their paltry 1% yields are just plain unacceptable to us income investors.

The 8% Dividend Opportunity

Instead, we’re going with a closed-end fund (CEF) that invests in a broad range of S&P 500 stocks, but with a key difference: This one pays a rich 8% yield.

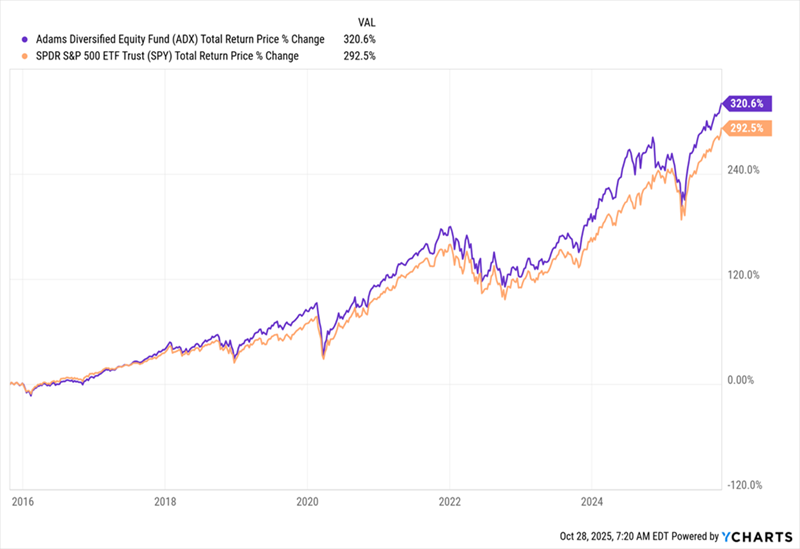

That would be the Adams Diversified Equity Fund (ADX), which holds tech darlings like Broadcom, as well as top performers from other sectors, like JPMorgan Chase & Co. (JPM). Thanks to its well-crafted portfolio, ADX hasn’t just matched the stock market’s returns over the last decade – it’s beaten it.

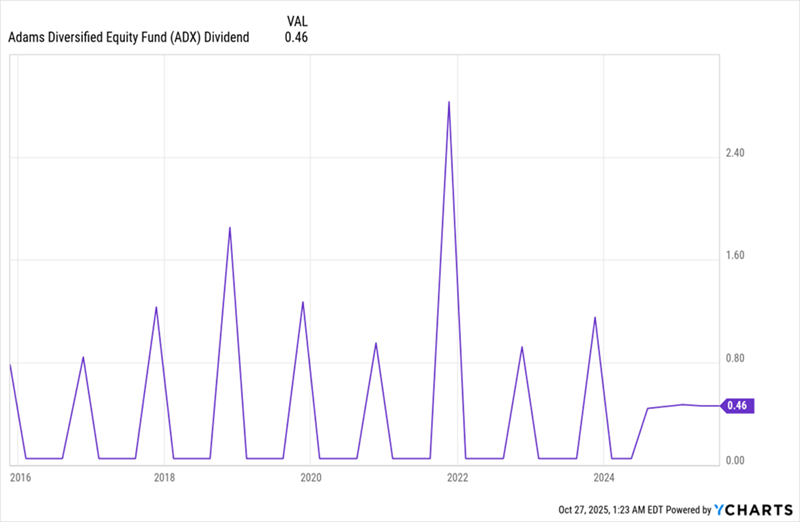

ADX Ahead of the Pack This is why, at CEF Insider, we’ve been holding ADX for almost the entire time shown on this chart (and we would’ve held it for the entire time if CEF Insider had launched in 2015, rather than in 2017). This outperformance is great – but so is the dividend.

Big Payoffs – Now More Stable ADX has yielded around 9.5% over the last decade, thanks to the huge special payouts management issued at year-end. But in 2024, the fund changed its distribution plans, going with a more evenly spread payout tied to the fund’s net asset value (NAV, or the value of its underlying portfolio). Now, ADX’s regular distributions are more consistent and reliable.

The fund pays about 8% now, largely because the stock price is up over 13% in 2025 (as prices rise, yields fall). But its total return including dividends is 21.7% for the year, as of this writing, again far ahead of the S&P 500, at 16.6%.

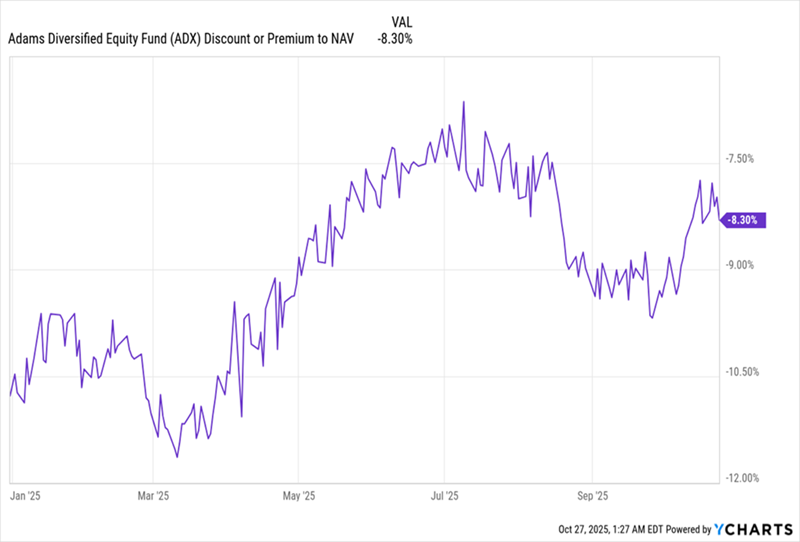

In other words, this fund has outperformed over the short and the long term. Yet it still trades at a discount to NAV.

ADX’s Wide – But Narrowing – Discount ADX’s discount is now 8.3%, but it was over 10% at the start of the year (and was around 12% most of the time before that). With the fund’s high yield, market outperformance and smartly built portfolio, this discount is likely to disappear, especially as more money comes into stocks as bubble fears fade.

If you buy ADX today, you can still lock in this discount, boosting your upside potential while also securing that healthy yield.

4 Cheap 8% Dividends to Buy as Bubble Fears Spread, AI Grows

As we just discussed, all of this bubble talk is a great setup for us to come at this market from the opposite direction as most investors:

Instead of letting bubble fears drive us away from stocks, we’re buying. Specifically, we’re looking beyond Big Tech, at other sectors set to reap big profits as AI revolutionizes their businesses.

These are the companies that are quietly adopting AI, but its value to their businesses is not priced in yet.

We’re going to buy those stocks through – you guessed it – CEFs

I know this if off topic but I’m looking into starting my own weblog and was wondering what all is needed to get set up? I’m assuming having a blog like yours would cost a pretty penny? I’m not very web savvy so I’m not 100 positive. Any suggestions or advice would be greatly appreciated. Thanks

WordPress thru FastHosts . Current cost around £8.00 a month although there is a free introductory offer. No coding skill necessary.

Lately, a lot of investors (myself included) have been looking at some increasingly frothy-looking stock market valuations and wondering if they may suggest that we are headed for a crash.

Lately, a lot of investors (myself included) have been looking at some increasingly frothy-looking stock market valuations and wondering if they may suggest that we are headed for a crash.

There will be a crash sooner or later, of course. There always is. But nobody knows when it will come.

It might start tomorrow or not for decades. (I would be surprised if we have to wait for decades, but it is a possibility

While there is a lot of chatter right now about what happens if there is a stock market crash I think another question is worth asking: what happens if the stock market just keeps going from strength to strength?

Reasons to be optimistic The idea that a crash may be coming is built on several foundations.

One is that many valuations now look stretched by historical standards.

Another is that massive AI valuations look like a bubble. Nvidia (NASDAQ:NVDA), for example, this week hit a landmark $5trn market capitalisation.

It seems like little time since we were marvelling at the first $3trn market capitalisation in history, in 2022. We have since seen a $4trn capitalisation and now $5trn.

But is Nvidia, with its huge valuation, indicative of a stock market bubble? I do not necessarily think so.

The company’s revenue in the latest quarter alone was $47bn. Its net income was $27bn.

In other words, this is a massive and massively profitable company. Surging use of AI and the related demand for chips could help the business keep growing fast.

One way of looking at the recent stock market performance is that prices have been trying to adjust to a rapidly evolving business landscape fuelled by the AI boom.

It remains to be seen whether companies like Nvidia can keep up their strong profit growth rates. If they can, the stock market could conceivably keep moving higher from here.

And that’s the rub.

Arguably it is the same with every bull market. Sit out, expecting a crash, and potentially miss out on years of gains along the way. Or throw normal valuation metrics to the wind and invest. Both have a sort of logic, but both can also be poor decisions.

A good starting point to solving that conundrum is to ask: can I really time the market with certainty ? The answer, always, is no.

So sitting out waiting for a crash does not necessarily seem like an obvious option, given that I cannot time the market.

Instead, I prefer to do what I do whether the stock market looks cheap or expensive: hunt for individual shares that have an attractive price given their business prospects.

Nvidia’s business does appeal to me. It has proprietary designs and a large, deep-pocketed customer base.

But it faces risks too, such as export limits. Taken altogether, the current price-to-earnings ratio of 57 is higher than I feel comfortable paying. I think valuation always matters, even (or perhaps especially) when other investors are getting caught up in the excitement of a surging market.

Whether there is a crash coming, or the stock market simply keeps hitting new highs, I believe my long-term strategy of trying to find great businesses at attractive prices is a good way to try and build wealth.

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

The content of this article is provided for information purposes only and is not intended to be, nor does it constitute, any form of personal advice. Investments in a currency other than sterling are exposed to currency exchange risk. Currency exchange rates are constantly changing, which may affect the value of the investment in sterling terms. You could lose money in sterling even if the stock price rises in the currency of origin. Stocks listed on overseas exchanges may be subject to additional dealing and exchange rate charges, and may have other tax implications, and may not provide the same, or any, regulatory protection as in the UK.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Will the market take a tumble soon? Or will it power on? Lots of people have opinions on this, although in reality none of us actually knows what will happen next in the stock market. But with the S&P 500 riding high, many investors remain bullish about where we may go from here.

It is not just the S&P 500.

The Dow Jones Industrial Average and Nasdaq indexes both closed at record highs yesterday (28 October), alongside the S&P 500. On this side of the pond, the FTSE 100 has repeatedly hit new all-time highs this year – including today (29 October).

Does that sound like the sort of market action that precedes a crash ? Some investors believe so, but others argue that ‘this time it’s different’.

Most stock market bubbles that end up popping involve people claiming that this one is different to all the rest.

But – might they be right this time?

AI is not necessarily another dotcom boom

It is easy to see echoes in today’s market of another soaring market a quarter of a century ago: the dotcom boom. That ended in a crash.

However, when people say that things are different this time, they do have a point.

During the dotcom era, the market had attracted large sums of money into many companies that had little or no revenues. In some cases, they scarcely even had a business plan beyond stuffing the word ‘Internet’ into as many press releases as possible. Hello, pets.com, boo.com and many more.

By contrast, 2025’s soaring S&P 500 has been driven by companies like Nvidia (NASDAQ: NVDA). The chip company is already enormously profitable, established for decades and has a large customer base.

There’s a lot of liquidity

That is not the only difference between the current market and some previous bubbles.

Sometimes, there is a lack of spare cash and nervous investors withdraw funds from the market in part because they need the money. Now we are in essentially the opposite situation. For some years the markets have been awash with liquidity as investors seek somewhere to stash their cash.

The huge amount of available liquidity means that, in my view, the market continues to be propped up by easy money looking for a home. Historically such situations have made investors less picky than when liquidity is tight.

Lots of alarm bells

Still, from the soaring gold price to the increasingly convoluted deal structures we are seeing in everything from car finance to the AI supply chain, there are plenty of indicators flashing that have often been associated with a crash.

The S&P 500 looks highly valued to me. Nvidia is a case in point.

Is it a proven, massively profitable business? Yes. Does AI present it with incredible opportunities? So far, yes – and they may get even better.

Does that justify a price-to-earnings ratio of 59 and a market capitalisation of over $5trn?

Personally, I do not think so.

From a potential slowdown in AI spending after initial installations to geopolitical tensions and export bans, Nvidia faces plenty of risks. Its current price does not reflect them properly in my view.

The fundamentals of good investing remain the same. I have no plans to buy Nvidia stock soon – or any S&P 500 share, come to that.