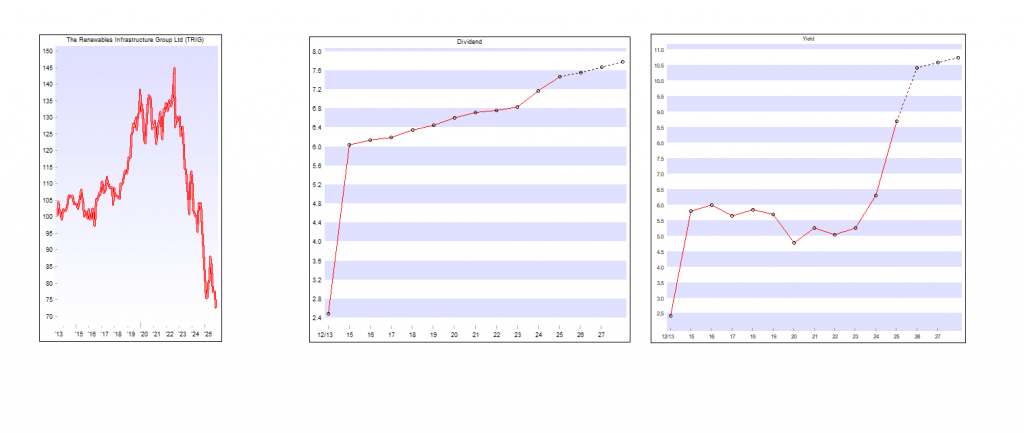

I’ve bought for the Snowball 13651 shares in TRIG.

They go xd Wednesday for 1.89p. By buying just before the xd date it may be possible to receive 5 dividends in just over a year, which would equate to a yield of around 12%. There would be a trading decision to take then but

Disclosure – Non-Independent Marketing Communication

This is a non-independent marketing communication commissioned by The Renewables Infrastructure Group (TRIG). The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

TRIG’s managers position for growth.

Overview

The Renewables Infrastructure Group (TRIG) is one of the leading trusts in the renewable energy infrastructure sector, having a large portfolio of institutional quality assets of significant size and scale, which is diversified geographically and by technology. The renewables sector, of which TRIG is a large constituent, has been facing a challenging backdrop for sentiment, with the significant rise in interest rates around the world the main culprit. Despite progress on sales of assets since 2022, with c. 10% of the portfolio sold at prices above or in line with NAV, TRIG has not yet been able to reduce its short-term borrowings as much as planned. Further transaction activity would also serve to usefully validate TRIG’s NAV.

As we discuss in the Gearing section, TRIG has announced that for the first time it is in the process of arranging longer-term corporate-level debt, which will mean it can pay back the majority of the short-term debt, as well as give it more flexibility to deploy capital in the future—either re-investing in the existing portfolio to boost returns, investing in the development pipeline, or further share buybacks. The board is carefully monitoring the respective attractions of each, focussed on making the trust’s capital work hard and generate value for shareholders.

As we discuss in the Portfolio section, drawing down this debt will also enable the team to bring forward investment to accelerate growth in capital and income. TRIG has a significant development pipeline that could take the proportion invested in battery assets up to c. 10% – 15% if fully built out. Battery assets complement wind and solar assets in that their revenues benefit from the price volatility of intermittent generation, and so as the portfolio mix changes, the portfolio can potentially receive higher returns on invested capital.

Analyst’s View

With scale and a strong balance sheet, TRIG is in a good position to continue to provide a resilient income stream. The company recently held a capital markets event, which demonstrated that the combined expertise of InfraRed and RES working together on the trust is a clear advantage, with the breadth and depth of resources working to maximise returns for shareholders clearly evident.

Drawing down structural company-level debt is a new step for TRIG. As well as enabling the repayment of some of the short-term borrowing facility, it will also enable the team to bring forward investment to accelerate growth in capital and income. This should result in higher revenues and higher NAV over the long term than would otherwise be the case. Buybacks clearly help address the discount and are accretive over the short term, but on their own, do not help the long-term trajectory of the company.

There are other benefits too. TRIG has a real opportunity to enhance diversification and earnings by building out a bigger portfolio of battery projects through its in-house developer, Fig Power. The first of TRIG’s battery development projects is due to energise this year. If further assets are successfully developed, they will increasingly complement the cashflows from TRIG’s wind and solar assets, meaning an enhanced revenue stream from the portfolio as a whole. These factors, and others that we discuss in the Portfolio section, mean that TRIG remains amongst the highest quality offerings in its sector, offering an attractive and resilient dividend yield of 8.5%, currently trading on a significant discount to NAV.

Bull

A high yield of 8.5% from a cash-covered dividend, with the potential for NAV growth

High-quality diversified portfolio, bolstered by proprietary development pipeline and RES’ operational enhancements

Discount may provide an accelerant to NAV returns, if appetites return to the sector

Bear

Discount to NAV may persist for some time

Dividend cover not as high as that of funds that are not amortising, i.e. paying down debt

Macro and political factors outside the managers’ control have at times provided a headwind to the NAV

Net Asset Value update – Q2 2025

TRIG announces an estimated unaudited Net Asset Value as at 30 June 2025 of 108.2 pence per share, a decrease of 4.5 pence per share in the quarter principally due to a reduction in revenue forecasts (-4.4p).

Dividend cover for H1 2025 was 2.2x gross or 1.0x net after the repayment of £105m portfolio-level debt across the Group. A further c. £85m portfolio-level debt is scheduled to be repaid in H2 2025.

The Board reaffirms the dividend target for 2025 of 7.55p per share for FY 20251. Low generation as a result of particularly poor wind speeds in H1 can be expected to impact H2 cash flows meaning that covering the FY 2025 dividend may be tight.

LTAFs promise virgin territory for investors seeking exposure to private markets, but isn’t there something there already?

Pascal Dowling

Updated 21 Sep 2025

Disclaimer

This is not substantive investment research or a research recommendation, as it does not constitute substantive research or analysis. This material should be considered as general market commentary.

To the people of the lush Northeastern Woodlands the news that America, in all its abundance and beauty, had been discovered by a group of bedraggled, hungry God-botherers – too weird even for Britain in 1620, when the head of state spent much of his time writing a detailed manual on how to deal with the witches he believed had delayed his wedding – must have been quite confusing.

Likewise for those of us with any experience of investment trusts, the news that we will soon be able to invest in illiquid assets via a fund structure which allows the manager to invest for the long-term, without worrying about the need to meet redemptions, and with a low minimum investment, seems somewhat like a non-story.

For the benefit of those at the back of the wigwam, Long Term Asset Funds (LTAFs) are a new form of open-ended fund, designed to provide access to illiquid, long-term assets like private equity, venture capital, infrastructure, and property – collectively termed as private markets – and equipped with structural mechanisms specifically designed to protect them from redemption pressures faced by OEICs and unit trusts.

In effect their defining feature is that they are semi-closed-ended funds. Withdrawals are limited to specific times and frequencies; you cannot simply sell up when it suits you. When you can sell, limits on the amount of money that can be redeemed, charges for redemption and even refusals are all at the discretion of the manager, who will make these decisions with the long-term success of the portfolio as their priority.

Last week Hargreaves Lansdown published an article outlining the benefits of the new LTAF structure to private investors, among whom are SIPP investors on the HL platform, who can now buy two LTAFs managed by Schroders Capital. Next year ISA investors will also be able to but LTAFs in a tax efficient manner.

Diversification (that old chestnut), the fact that they can be held in a tax efficient SIPP or (as of next year) ISA wrapper, and a ‘low minimum investment threshold’ were among the benefits described in the article.

The headliner, though, for those considering these new vehicles was ‘the chance to invest in private investments that were previously only available to large institutions. These could be sectors shaping our future, like renewables, fintech, biotech, and artificial intelligence’.

We’ve been here for ages, savvy?

The new opportunities outlined here may seem like familiar ground for investors inGreencoat UK Wind (UKW)(among whom I am counted) andThe Renewables Infrastructure Group (TRIG), both of which hold a Kepler Alternative Income Rating thanks to their success in delivering a steady or growing dividend without running down the NAV and both of which are invested in illiquid private assets in the renewables space.

Shareholders in International Biotechnology Trust (IBT), too, might be tempted to argue that they were here already. The trust has shifted its focus to smaller companies in the sector this year in anticipation of an M&A boom – and has the ability to invest up to 15% into unquoted assets via a tie up with SV Health Advisers, where COVID tsar Kate Bingham calls the shots.

IBT has delivered solid returns since inception in 1994, and significantly outperformed the biotech sector under the stewardship of Ailsa Craig and Marek Poszepczynski since they took the reins in 2021.

NB Private Equity Partners (NBPE) is explicitly and solely focused on private markets, offering exposure to a portfolio of 76 private companies, across a wide variety of sectors, via co-investments alongside 48 private equity sponsors, and even retail giant Scottish Mortgage (SMT) has shifted heavily toward unquoted stock in recent years. The Baillie Gifford flagship counts more than fifty private companies among its holdings including SpaceX – the single largest holding in the portfolio.

It’s a big country, surely there’s room for us all?

Via investment trusts ordinary investors have for a long time had access to a structure which allows them to invest in private markets which were ‘previously available only to large institutions’ – since 1868 in fact, when Foreign & Colonial was established “to give the investor of moderate means the same advantages as the large capitalists”.

What’s more, liquidity is better for investment trusts – I can sell my shares in NBPE instantly – and charges are, by and large, lower or at par than they are likely to be via an LTAF. I can also buy private markets assets at a discount, because investment trust shares may trade at a discount to NAV.

So why all the fuss?

There has, over the years, been much talk of the inevitable ‘death’ of investment trusts as an industry – outgunned by and unable to keep up with the more retail-friendly, modern competition.

With Saba still prowling the alleys around Threadneedle Street, the arrival of LTAFs has been added to the ledger as another potential existential threat for an investment trust industry ‘under seige ’. Newspapers like this kind of headline.

And, truly, there is scope for LTAFs to flourish. Kepler’s own Tom Trotter – a partner at the firm – is an expert on the new structure, having orchestrated a study of the sector this year. He says: “Momentum seems to be building with now 150+ELTIFs and 26 LTAFs approved and investable. More broadly, unregulated evergreen structures have been gaining real momentum, and there are now reportedly over 500 funds available, offering access to some of the largest and best-known private markets managers globally.

“Estimates suggest there is approximately $700bn now invested in these evergreen strategies. While a big number, it only represents about 5% of invested capital in private markets, highlighting the potential for this part of the market to grow.”

But perhaps the real growth opportunity for LTAFs is not in edging out retail investors from investment trust share registers, and the threat for investment trusts does not lie in losing ground there. Instead, it is a matter of horses for courses.

A key issue which has faced the investment trust sector in recent years is the problem of liquidity that they present for very large institutional owners. An individual wealth manager twenty years ago might run a portfolio for his rich client with twenty idiosyncratic stocks in it, each chosen by hand (I like to imagine before a boozy lunch at Sweetings then the early train home to West Sussex – but I digress). Today, it is far more likely that the wealth manager will be choosing from the same list of stocks as everybody else in his or her company, approved by a central research function, and then probably doing some mindfulness and a two hour ayurvedic spin class before crying themselves to sleep in a flatshare in Romford.

This means far more money is moving in the same direction at the same time. In that scenario there simply isn’t enough daily liquidity in the shares of many investment trusts for them to be practical targets for investors of this scale and so, for this type of investor, LTAFs may well be of more interest.

So, while the writing may not be on the wall for investment trusts, which remain a far more flexible, affordable and straightforward means to gain exposure to private markets for ordinary investors on small budgets, there is certainly scope for LTAFs to add value for some larger investors – and we will be watching developments closely.

UKW shares hit by ROC consultation, but fundamentals remain undimmed.

William Heathcoat Amory

Updated 07 Nov 2025

Disclaimer

Disclosure – Non-Independent Marketing Communication

This is a non-independent marketing communication commissioned by Greencoat UK Wind (UKW). The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

The Department for Energy Security and Net Zero has launched a consultation on proposed changes to the inflation indexation used in the Renewable Obligation (RO) and Feed-in Tariff (FiT) schemes. Some trusts have provided guidance on the potential impact on NAVs, but this has hit share prices across the renewables sector. Discounts to NAV have widened.

In summary the consultation suggests two options:

Option 1: from March 2026, move ROC indexation from RPI to CPI (this is in effect an immediate move since the next indexation date is March 2026), or

Option 2: freeze the current ROC level and create a “shadow” ROC price assuming ROCs had always been inflated by CPI since 2002. No further inflation-linked increase would take place until this “shadow” CPI price catches up with today’s level (assumed to happen around 2034/35, so effectively the current price is frozen until then). Thereafter, CPI would apply.

It is important to realise that this is only a consultation, and not necessarily an inevitable change. This is not the first time that a consultation on this has been initiated, with a previous consultation in 2023 focusing on a potential migration of ROCs to a fixed price certificate, which included consultation on ROC indexation. The net result of this previous consultation was that no amendments were made to indexation (or anything else).

It is fair to say that the UKW and the wider industry will be engaging in the consultation, and the UK government will be very aware of the potential impact of any changes on future investment in renewable energy development. With the results of the AR7 auction round due to be announced over the next months, we imagine the government will not want to dent the enthusiasm of developers, given this is a key step towards the UK’s net zero transition.

Kepler View

Whilst this recent news has added to the already challenging backdrop for Greencoat UK Wind (UKW), the share price move seems extreme, such that the worst outcomes would appear to be more than accounted for by the current share price discount to NAV. In fact, UKW’s shares now trade below the original IPO price more than twelve years ago, despite the experienced management proving the quality of the asset class and demonstrating how their conservative approach has delivered strong NAV total returns since inception. Backing up this conservative approach is the robust dividend cover, which has allowed UKW to continue to increase the level of the dividend in-line with, or ahead of, UK RPI every year since IPO.

If either proposal in the consultation were implemented, it would clearly reduce the NAV total returns that Greencoat UK Wind (UKW) would earn in the future, and would likely translate into a one-off hit to NAV. However, whilst UKW is clearly 100% exposed to the UK government subsidy regime (rather than other geographies), it has a mix of revenues streams across ROCs, other subsidy schemes (such as CfDs) and market power prices. It is only the indexation mechanism on the RO and not the value of the certificate itself that is up for debate within the consultation. The potential negative effects will also be mitigated by the relatively short remaining life of the ROCs in the portfolio (average remaining duration c. 7yrs). UKW also derives a significantly lower proportion of its revenues from the Renewables Obligation than solar peers, and so we would expect UKW to be significantly less affected than many in the listed peer group.

Fundamentally, UKW appears resilient. Certainly, if either of these proposed options is implemented, this does not help the headwinds the UKW currently faces. UKW’s gearing is slightly above the company’s preferred range. A lower NAV will mechanically increase gearing, and the uncertainty of these proposed changes will likely make further asset sales at NAV (the proceeds of which could be used to repay borrowings) harder to achieve in the short term.

However, UKW’s structurally high dividend cover means that it still has options to deploy surplus cashflows towards new investments, buybacks or reducing debt. We note that UKW continues to buy shares back, illustrating the confidence the board has in strength of the balance sheet. Currently, UKW offers an attractive dividend yield of 10%, given the shares trade on a discount to NAV of c. 30%. In our view, the sell-off on the announcement of the proposed changes to ROC tariffs are arguably overdone. This is not the first time ROCs have been consulted on, and the pullback is pricing in an overly negative scenario for a decision that is far from certain, and still subject to input from key stakeholders. Even then, UKW’s conservative approach means there are considerable levers to pull in order to mitigate a sizeable amount of their potential impact.

As investors look to year-end and into 2026, the appeal of dividends lies not only in income but also in stability through uncertainty.

When evaluating dividend stocks, I strive to look beyond headline yields and look for quality, as defined by dividend safety and supportive Factor Grades.

This basket of five stocks has an average dividend yield of 3.96%, well above the 1.15% for the S&P 500 and 1.65% for the Vanguard Dividend Appreciation Index ETF (VIG).

All five stocks have Strong Buy Quant Ratings, emphasizing diversification, durability, and quality for investors seeking steady income through market cycles.

I am Steven Cress, Head of Quantitative Strategies at Seeking Alpha. I manage the quant ratings and factor grades on stocks and ETFs in Seeking Alpha Premium. I also lead Alpha Picks, which selects the two most attractive stocks to buy each month, and also determines when to sell them.

mustafaU/iStock via Getty Images

Just released is an update about my Top 10 Quant Stocks of 2025 Up 45%. It’s a great opportunity to recap some of my annual top stock picks as we approach the coming new year and Top 10 Stocks for 2026. In the meantime, now is a good time for investors to explore or revisit the best dividend stocks, as economic and market uncertainty is on the rise. The U.S. government shutdown just earned the distinction of being the longest on record, while Wednesday’s ADP report showed modest employment growth.

Meanwhile, the Fed’s interest rate path is increasingly questionable as Fed Funds Futures now give roughly a 63% probability of a 25 bps cut in December, down from 86% a month ago. Fanning the flames of uncertainty, Trump’s tariff powers are also about to be tested in the Supreme Court. In a go-anywhere type of macro backdrop, the right mix of dividend stocks can provide a good balance of low volatility and yield to support a retirement portfolio or a long-term income and growth strategy.

5 Best Dividend Stocks: Diversification, Quality, Yield

SA Quant has explored its universe of top dividend stocks and selected five options for investors based on their exceptional Quant factor and dividend grades. When evaluating dividend stocks, I strive to look beyond headline yields and look for quality, as defined by dividend safety and supportive Factor Grades in key areas like valuation, growth, and profitability.

This basket of five stocks has an average dividend yield of 3.90%, well above the 1.15% for the S&P 500 and 1.64% for the Vanguard Dividend Appreciation Index ETF (VIG).

Quant Sector Ranking (as of 11/06/2025): 12 out of 174.

Quant Industry Ranking (as of 11/06/2025): 2 out of 11.

Sector: Real Estate.

Industry: Other Specialized REITs.

FWD Yield: 5.97%.

Seeking Alpha

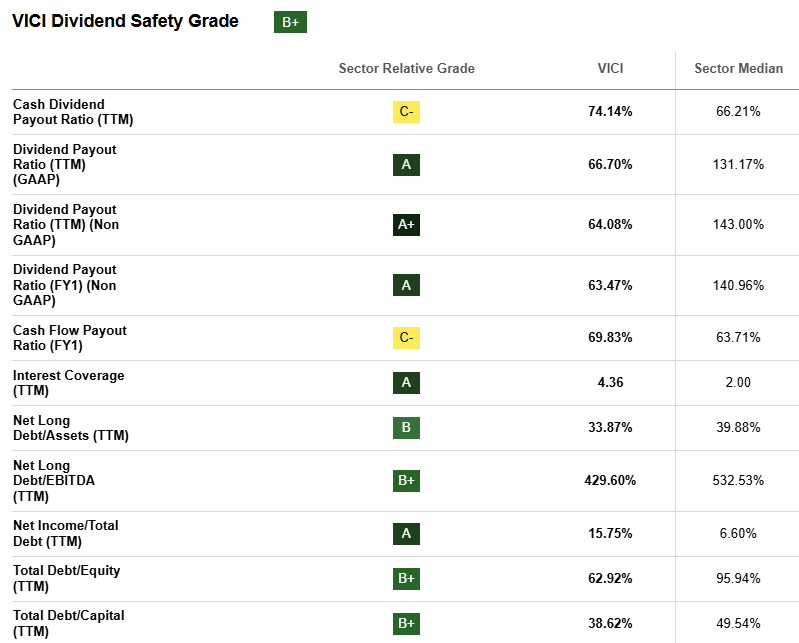

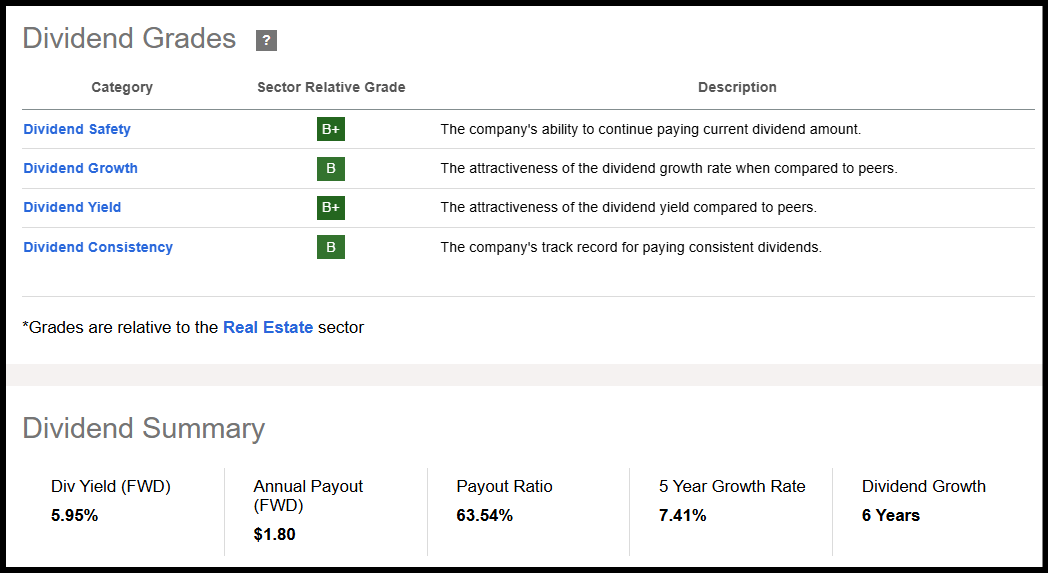

One of my 3 High-Yielding Dividend Stocks For 2025 featured in January, VICI Properties is a real estate investment trust that owns some of the most iconic entertainment and hotel properties in the U.S., including Caesars Palace and MGM Grand. Its portfolio is built on long-term triple-net leases, meaning tenants are responsible for taxes, insurance, and maintenance. This gives VICI predictable, inflation-linked income. VICI’s dividend safety is supported by its outstanding dividend payout ratio of 63.54% and a strong dividend scorecard.

Seeking Alpha

In last week’s Q3 earnings call, CEO Edward Pitoniak opened by emphasizing “Q3 2025 earnings growth rate,” highlighting AFFO per share growth of 5.3% vs. Q3 2024 and underlining the company’s resilience: “The VICI team continues to demonstrate its resourcefulness and resilience in growing relationships that grow our revenues and profits without… significantly growing our capital base.” VICI’s earnings growth supports its multi-year dividend growth history.

Seeking Alpha

VICI also comes at an attractive valuation. The stock trades at a deep discount with a forward P/FFO ratio of 10.90, which is 17.42% below the sector median.

Some investors may be concerned about declines in Las Vegas tourism, but VICI remains resilient as its earnings growth tells a story of strength. With a dividend yield near 6% and recurring cash flows, the company fits neatly into a “steady income through uncertainty” framework. For similar reasons, we include another REIT in our mix of five best dividend stocks for economic uncertainty.

Quant Sector Ranking (as of 11/06/2025): 8 out of 174.

Quant Industry Ranking (as of 11/06/2025): 1 out of 14.

Sector: Real Estate.

Industry: Hotels and Resorts.

FWD Yield: 5.88%.

Seeking Alpha

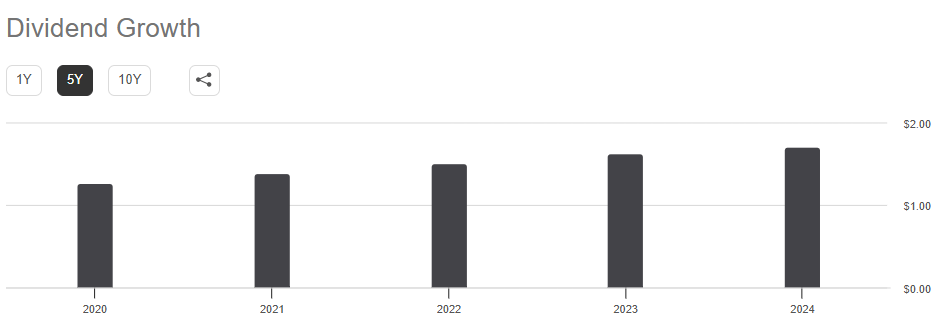

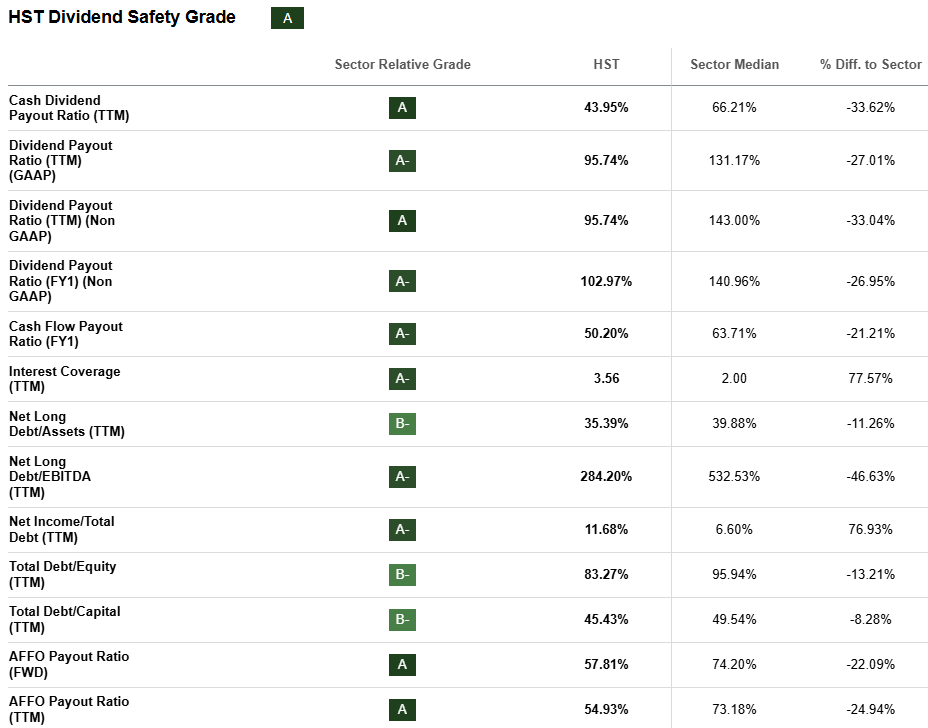

Among the 3 Quality REITs Yielding 5%+ I shared in July, Host Hotels & Resorts is one of the largest lodging REITs in the U.S., owning a premier portfolio of luxury and upper-scale hotels in key markets. While hospitality is more cyclical, HST has strengthened its balance sheet and focused on premium properties that maintain pricing power. At 5.88%, its yield provides strong income potential, and the company benefits if leisure and business travel remain resilient despite moderate economic growth. Although HST has paid a consistent dividend for a mere two years, HST’s ‘A’ dividend safety grade is supported by a lot of green, including its 43.95% cash dividend ratio and forward AFFO payout ratio of 57.81%, which are 33.62% and 22.09% below the sector median, respectively.

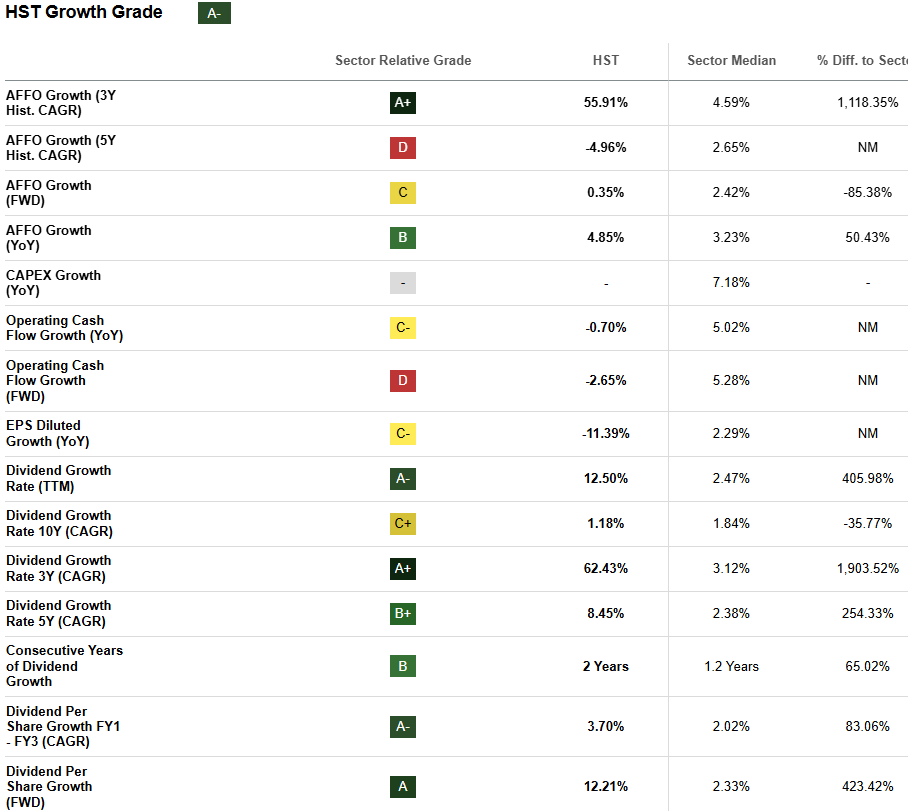

If inflation remains sticky, HST’s growth trends can be a counterbalance. The REIT’s AFFO growth is likely to remain attractive, judging by its three-year CAGR of 55.91%, which crushes the sector median of 4.59%. During the recent earnings call, the consensus FFO estimate is $0.33, and the consensus revenue estimate is $1.31B.

Seeking Alpha

HST suits investors seeking higher income with a calculated level of risk in a diversified dividend mix. As I’ve mentioned before about HST, by owning rather than operating the hotels, HST can focus on driving property value growth while reducing its exposure to daily operational risks and complexity. The company can continue its strong results, driven by higher rates and a strong recovery in select markets like Maui.

Moving from REITs to healthcare, biotech stocks with momentum can provide a solid diversification tool in a dividend stock portfolio.

Quant Sector Ranking (as of 11/06/2025): 30 out of 974.

Quant Industry Ranking (as of 11/06/2025): 19 out of 472.

Sector: Healthcare.

Industry: Biotechnology.

FWD Yield: 2.57%.

Seeking Alpha

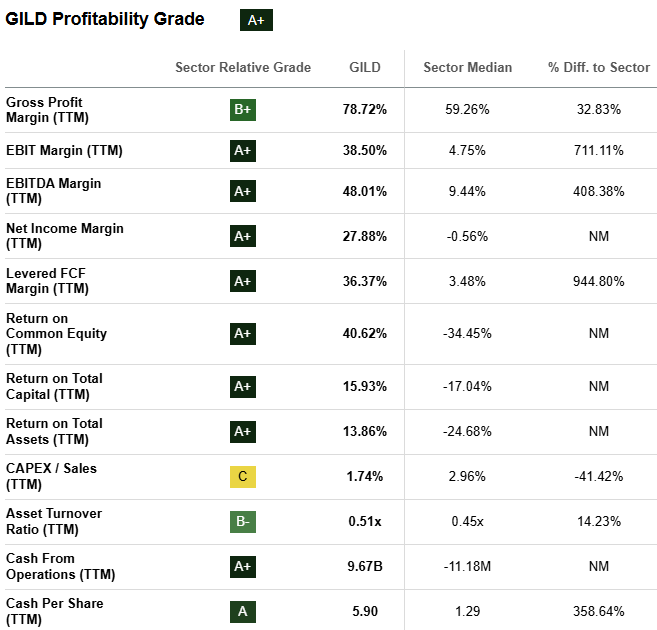

Gilead Sciences is a leading biotechnology firm best known for its antiviral treatments for HIV and hepatitis. Unlike cyclical industries, Gilead’s earnings stem from essential, recurring demand, providing a layer of defense against economic slowdowns or trade-related disruptions. Its solid dividend yield of 2.57% is supported well by free cash flow, and the company maintains one of the more conservative payout ratios among large-cap biopharma names. GILD has continued its strong momentum, returning more than 25% from approximately $97 to $122 per share, since I selected it for Stay In May: Top 5 Dividend Stocks. The company’s yield is supported by strong profitability and dividend safety.

Seeking Alpha

GILD’s A+ profitability grade comes as no surprise as the company’s EBITDA margin of 48% is roughly five times higher than the sector median of 9.44%. With close to $9.7B in cash from operations, GILD offers investors a strong indication that the company’s in a strong position to maintain paying and possibly grow its dividend. In the earnings call last week, Gilead raised its 2025 revenue growth outlook 5%. CEO Daniel O’Day stated that “our third quarter earnings underscore the growing momentum you’re seeing from Gilead today, which is driven by our strong portfolio and the impressive execution of our teams.” He highlighted commercial outperformance across HIV therapies and Livdelzi, with Biktarvy growing 6% year-over-year, Descovy up 20%, and Livdelzi posting 35% sequential growth.

With a steady pipeline and prudent capital allocation, Gilead fits a “slow-growth, sticky inflation” environment by offering income stability that’s less sensitive to interest rate uncertainty.

GILD complements cyclical sectors by adding healthcare’s defensive balance. Meanwhile, a high-quality insurer that performs well across economic cycles can add an element of stability and dividend safety in an uncertain environment.

Quant Sector Ranking (as of 11/05/2025): 10 out of 684.

Quant Industry Ranking (as of 11/05/2025): 3 out of 53.

Sector: Financials.

Industry: Property & Casualty Insurance.

FWD Yield: 2.05%.

Seeking Alpha

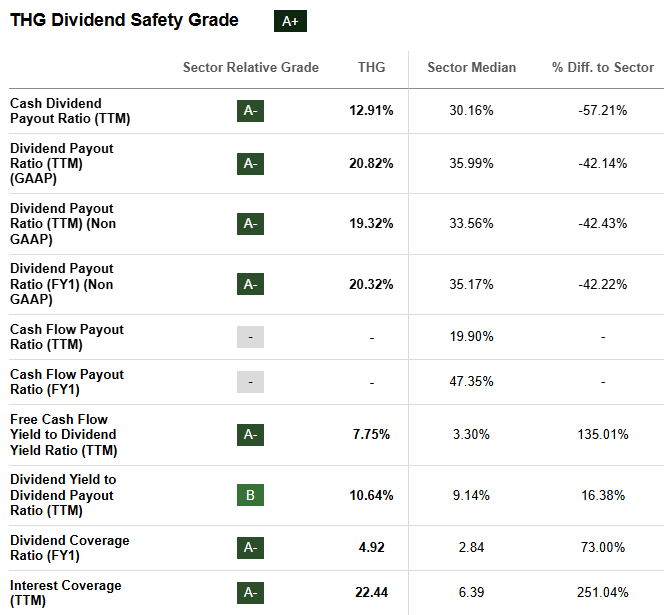

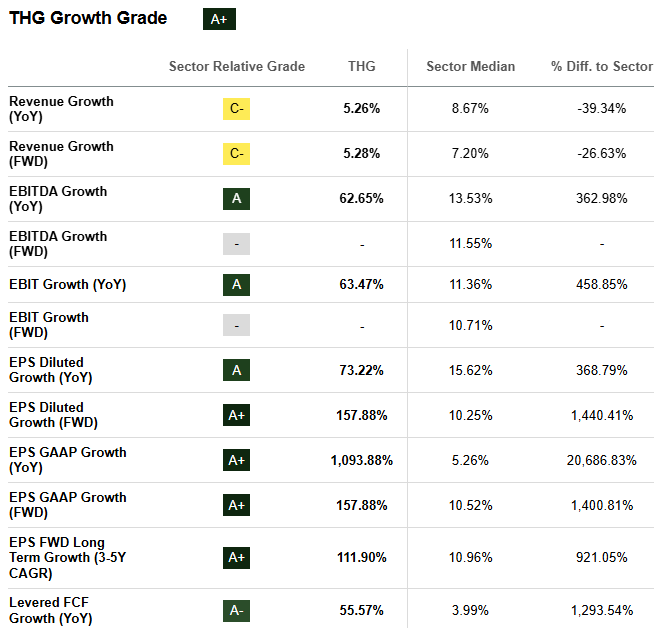

The Hanover Insurance Group is a property insurer providing coverage for business, homes, and specialty lines across the U.S. Its disciplined underwriting and diversified portfolio make it a high-quality insurer that performs well across economic cycles. In an environment of moderate growth and persistent inflation, insurers like THG can have pricing power to maintain margins, offering a built-in inflation buffer. While its yield of 2.05% is lower than some high-yielding REITs in the mix, the payout is well supported by strong EBITDA growth.

Seeking Alpha

At its earnings call last week, Hanover signaled growth acceleration into 2026 with a record Q3 ROE and AI-driven specialty expansion. CEO John “Jack” C. Roche described the third quarter as delivering “exceptional results” due to “robust net investment income, a very strong ex-CAT performance and a quiet catastrophe quarter.” He pointed out Personal Lines’ improved profitability and Core Commercial’s flexibility to adapt amid shifting market dynamics. In Specialty, Roche described new AI-powered underwriting tools in E&S as streamlining submission processing, improving efficiency, and creating scalability: “This scalable approach we’re taking ensures that innovation developed in one segment can be adapted and deployed across our enterprise.”

The company’s focus on commercial and specialty segments adds another layer of defense against an uncertain economic environment with stable pricing power. THG’s long record of dividend growth reflects a management philosophy emphasizing shareholder return and prudent risk management rather than aggressive expansion.

For investors prioritizing quality, reliability, and modest growth over higher yields, THG provides an appealing anchor amid an uncertain economic climate.

Quant Sector Ranking (as of 11/06/2025): 30 out of 277.

Quant Industry Ranking (as of 11/06/2025): 4 out of 5.

Sector: Materials.

Industry: Aluminum.

FWD Yield: 3.33%.

Seeking Alpha

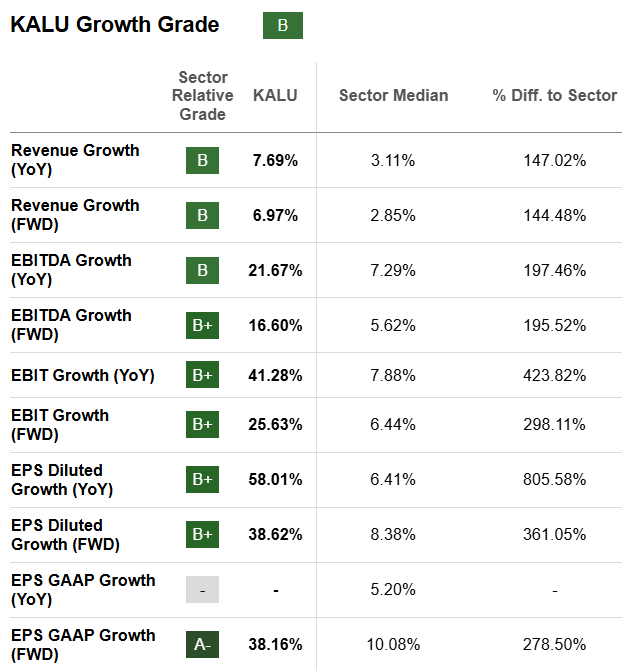

Kaiser Aluminum is a leading producer of specialty-fabricated aluminum products serving aerospace, automotive, packaging, and industrial markets. The company operates across the value chain, from rolling mills to finished components, giving it flexibility and pricing leverage. With a dividend yield of 3.33%, KALU offers a solid income stream supported by steady cash flow and prudent balance sheet management. Also supported by solid growth, Kaiser’s consistent dividend payments and disciplined capital spending make it one of the more stable industrial names in the cyclical materials sector

Seeking Alpha

Adding to its growth story at its Q3 earnings call, Kaiser’s CEO Keith Harvey noted “another strong quarter, marking our fourth consecutive period of performance ahead of our expectations.” He highlighted $20 million in start-up costs tied to strategic investments for aerospace and packaging, while a favorable metal pricing environment continued to support results. The CEO then added, “As a result, we’re once again raising our full-year EBITDA outlook.”

In an environment of sticky inflation and tariff uncertainty, aluminum producers stand to benefit from domestic reshoring trends and supply chain diversification, both of which support demand for U.S.-made materials. For investors seeking a blend of moderate yield and real asset exposure, KALU adds an industrial dimension to the other pieces of our best dividend stocks mix in real estate, healthcare, and insurance.

Conclusion: 5 Best Dividend Stocks to Diversify Amid Uncertainty

As investors look to the end of the year and into 2026, the appeal of dividends lies not just in income but also in stability through uncertainty. The five stocks on our list, VICI Properties, Host Hotels & Resorts, Gilead Sciences, The Hanover Group, and Kaiser Aluminum, reflect different paths to achieving that goal. VICI and HST offer high yields and real estate that can maintain strength in sticky inflation, while GILD brings consistency from healthcare’s defensive stability. THG adds the insurance piece, providing dependable cash flow well suited to a slow-to-moderate growth economic environment. Kaiser Aluminum adds industrial strength to the group, offering inflation-sensitive exposure to U.S. manufacturing while maintaining decent yields. Together, these names illustrate how investors can balance yield and quality, providing stability amid the uncertainties of a market that may be headed for slower growth, sticky inflation, and tariff uncertainty. Common threads across all five are diversification and durability, which are qualities investors seek through cycles, not just in booms.

Stir-up Sunday started back in Victorian times, and was a tradition where families would come together to get their fruit puddings stirred up, steamed and stored ahead of Christmas. Each member of the family would take a turn to give all the ingredients a good mix, whilst making a wish and help tick off the first task of the festive season.

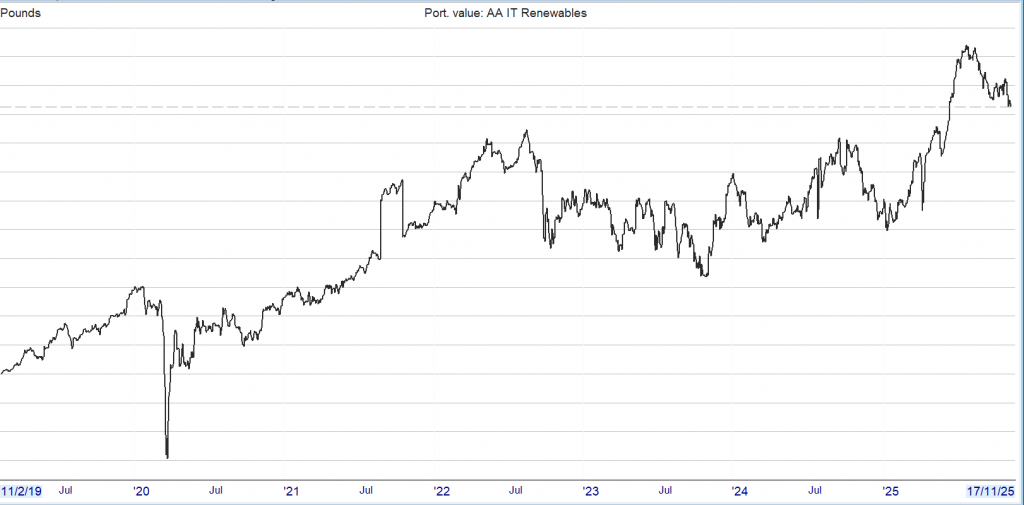

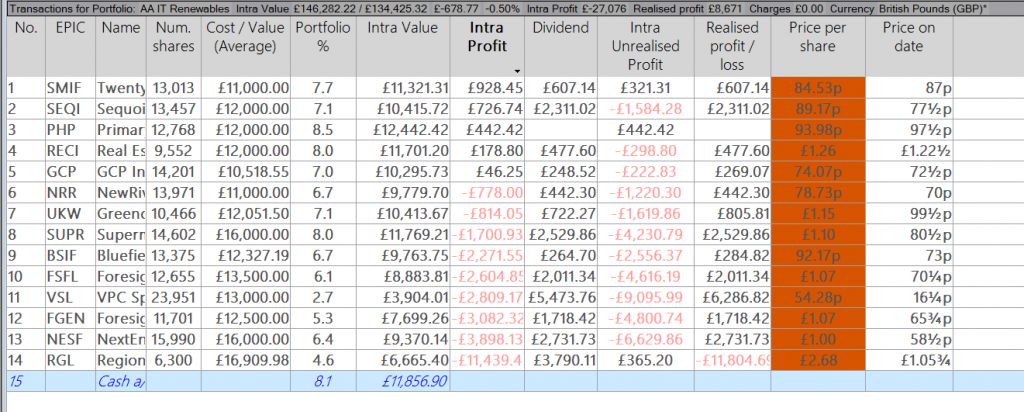

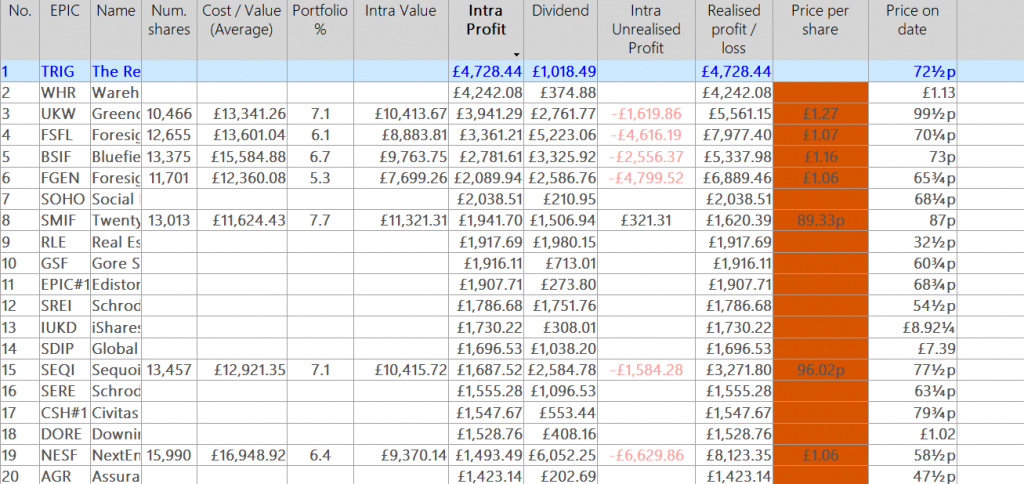

The portfolio was started because my son who is a huge climate warrior wanted to move his pension and I suggested a portfolio of Renewable Trusts.

He decided to move his pension elsewhere but I have maintained the portfolio, updating it once or twice a month. I have copied the performance in the posts below, so you can see how it all plays out, warts and all.

Note the loss during the Covid crash, which turned out to be a plus for the portfolio because as the price falls the yield rises. One traders disaster is another’s opportunity.

Low on chart £85,215.00 and the current price £146,282.00. The portfolio value is of no interest as the plan is to use the dividend stream as an ‘annuity’, unless an unexpected event happens and then you still have access to your cash, which you wouldn’t if you bought an annuity.

The current blended yield is around 10% which would provide an ‘annuity’ next year of around 15% on seed capital of 100k.

The holy grail of investing of having a share in your Snowball that provides income but sits in your portfolio at a zero, zilch, cost.

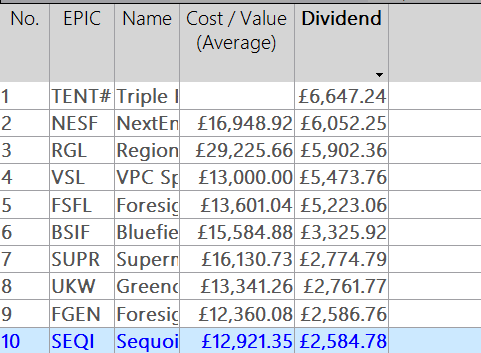

ALL TRANSACTIONS

NESF, FSFL. Year 4 in achieving the Holy Grail of Investing.

Although when I predict the future I’m normally wrong, I expect there will be some Trusts will be absorbed by others.

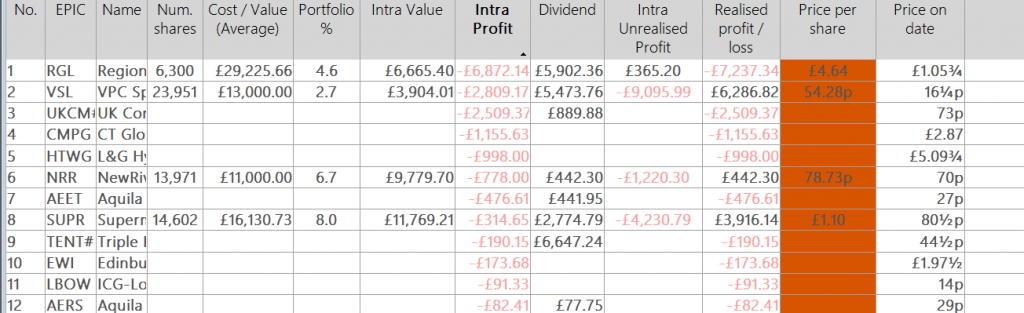

If you look at the figure for RGL in part 3 you will see the amount of loss for the overall position is a lot less but it’s very unlikely the cash lost will ever be completely recovered but you would have also earned some more cash which has been re-invested from their paid dividends.

Five ways to generate a dependable monthly income in retirement

From doling out dividends to maximising interest income – here’s how you can keep the cash coming in.

Esther Shaw

06 November 2025

Credit: Getty Images/Getty Images

While many of us spend much of our working lives looking forward to retirement, working out how to make our finances stretch for the rest of our life – perhaps until 100 – can be stressful.

“For many people, moving from a world of receiving a regular monthly income to one where you are managing a finite retirement pot can feel very unsettling,” said Harry Donoghue, chartered wealth manager at Tideway Wealth.

The good news is, there are ways to maintain a monthly income – beyond any four-weekly state pension payments, which we know don’t go very far. Recreating your own payday can help make regular bills more manageable and reduce the chances of overspending from your pot. Here, Telegraph Money outlines some of your options.

Investing in dividend-paying shares or funds can provide a steady stream of income, often paid quarterly or biannually.

“These payments can help mimic a salary, especially if you build a diversified portfolio across sectors and geographies which pay dividends on different months,” said David Little, chartered financial planner at Evelyn Partners. “It’s important to balance yield with quality. You need to look for companies with strong cashflow and a history of consistent payouts.”

Just remember, dividend payouts can be cut and are never guaranteed – so diversification is key.

You’ll also need to consider tax when drawing income from your investments. Dividend income is tax-free up to £500, and is then taxed at your marginal tax rate – 8.75pc for basic-rate taxpayers, 33.75pc for the higher rate, and 39.35pc if you pay additional-rate tax.

However, if your investments are held in an Isa, you won’t need to pay tax on these returns.

Mr Little added: “Investment Isas offer a tax-free income stream and should be utilised as fully as possible during your working years – helping to build a strong foundation for retirement income.”

These products, which convert a pension fund into a guaranteed income for life, or for a fixed term, can offer both simplicity and peace of mind.

Becky O’Connor, director of public affairs at PensionBee, said: “Annuities are the traditional income option and involve ‘buying’ an income that will last for a set period – or until you die – with some or all of your pension fund. The stability they give is practically unparalleled.”

If this sounds appealing, you’ll be pleased to know that with interest rates rising, annuities are making a comeback.

According to the latest figures from Standard Life, average rates reached 7.65pc in September this year, a year-on-year increase of nearly 10pc.

Pete Cowell, head of annuities at Standard Life, said: “Rates remain strong and continue to offer valuable income certainty for retirees.”

For those worrying about losing the rhythm of a monthly salary when they retire, he added that annuities can offer a really practical solution.

“They provide a guaranteed income stream that can feel just like payday, long after your working life ends,” he said. “This income can be monthly, quarterly, or annually, and once set up, the payments land in your bank account automatically, just like a salary.” While much of this may sound appealing, annuities won’t be right for everyone.

“One big trade-off with opting to purchase an annuity is that you might not get as high an income as might be possible through continuing to leave your pot invested,” said Ms O’Connor.

The key, as with any retirement planning decision, is to research your options carefully. Take the time to seek professional advice where necessary, to help you make an informed choice.

Consider rental income In the past, investing in buy-to-let has been a popular option with retirees, as it can provide reliable monthly income through rental payments. Better still, this often keeps pace with inflation.

If you are fortunate enough to already own a buy-to-let house or flat, this can potentially provide a natural retirement income stream.

The problem is, in recent years, buy-to-let has fallen out of favour somewhat as a result of changes to tax treatment (such as the reduction of mortgage interest relief) as well as a tougher regulatory regime for landlords on housing standards. This will get even tougher when the Renters’ Rights Act comes into force.

“While rental income can be a powerful tool, it may be less passive than it sounds on the face of it, depending on the quality of tenants and maintenance costs. The benefits also depend on whether your rental property is mortgaged and if it is, what happens to interest rates,” said Ms O’Connor.

As a landlord, you need to be prepared to build in a sufficient (and realistic) buffer for ongoing costs from maintenance, void periods, letting agency fees and tax when calculating the likely return.

Given all of this, experts suggest that for some retirees, selling an existing portfolio and using property equity elsewhere might actually be a better route than active letting.

Mr Little said: “From a taxation point of view, buy-to-let offers very little in the way of tax efficiency – it’s arguably one of the most tax-inefficient asset classes to hold.”

Once again, you need to research carefully, and consider speaking to a tax specialist to work out what’s best for you.

Give yourself ‘fixed paydays’ from pension drawdown Rather than ad-hoc withdrawals, you can, as a retiree, set up regular monthly or quarterly payments from your pension drawdown pot. By doing this, you can effectively create a personal, flexible payday.

While arriving at a figure that covers the spending you need can help keep a handle on how quickly your account reduces, this arrangement still offers retirees the flexibility to alter the income amounts when they need to – after all, there will always be the odd “out of budget” item that crops up.

“But to the best of your ability, try to stick to these regular and set withdrawals,” added Ms O’Connor. “This will give you a sense of control and peace that you are on track for a sustainable income.”

It may take a little trial and error to find the right amount for you; our pension drawdown calculator can help you make sure you don’t go in too high.

Organise regular savings interest If you’re searching for a modest but predictable income stream, you might want to seek out one of the savings accounts which offer the option to pay out savings interest – as opposed to compounding it.

NS&I’s Guaranteed Income Bonds are an example of accounts that offer this, with interest paid monthly at 3.97pc on savings between £500-£1m. Based on a savings balance of £100,000, you could expect a regular interest payment of around £330 a month.

However, you’ll need to tread carefully if you rely on this for retirement income. Firstly, you’re relying on savings providers offering an interest rate you can live off.

Mr Little said: “While interest rates have had a resurgence in recent years, they’re still unlikely to meet full income needs – or keep pace with longer-term inflation.”

You’ll also need to factor in the issue that your initial lump sum of savings won’t grow at all while you’re spending the interest, meaning its value will be eroded by inflation over time.

Make sure you have a plan The key to managing your finances successfully during your later years is having a plan.

Mr Donoghue said: “Rather than jumping straight into products or deciding withdrawals on the fly, take a step back and work out what you actually need to spend to enjoy the retirement you want.”

Expenditure does not necessarily have to stay consistent throughout retirement. It is very common for people to spend more in the early years on things like travel and hobbies, before naturally slowing down later on.

Mr Little said: “The key to successful retirement planning lies in blending income sources to match your lifestyle, tax position, and risk tolerance. By combining multiple, small, income sources, retirees can structure a single, tax-efficient, monthly income that closely mirrors the consistency of a salary – without the full punitive impact of income tax.”