I’ve been doing a bit of research on the habits of successful passive income investors, and I came across a bit of a surprise

Yes, real estate has been profitable for a number of people. But I had a very shaky venture into it. And it has a fair few drawbacks for individual investors.

Not really passive

One is that many of us won’t have the capital to go for, say, rental properties. It’s not the kind of thing we can get started with just a few hundred pounds, like we can with a Stocks and Shares ISA.

It’s not entirely passive either. Finding tenants, collecting rent consistently, and maintenance all take time and effort. And the latter can sometimes prove very costly if you’re unlucky.

But there’s a way we can get into real estate without facing those major hurdles. And that’s to consider buying real estate investment trusts (REITs). They’re investment companies that put their money into various kinds of properties, and they do all the management. All we have to do is buy shares in them, just as we do with shares in general

Healthy property

I like Primary Health Properties (LSE: PHP), which invests in GP surgeries, pharmacies, dental clinics. Importantly, they’re mostly rented to the NHS on long-term leases.

Having the UK government as its main customer provides some stability and predictability. But it hasn’t made the trust immune to weak property values in recent times. Over the past five years, the PHP share price has fallen 35%.

Higher interest rates are a burden, especially with debt on the books. At the end of the first half this year, net debt reached £1,367m, up from £1,323m in December 2024. There doesn’t seem to be any liquidity problem, but it could keep the shares down for longer.

Big dividends

On the bright side, a lower share price means a bigger dividend yield. Right now, we’re looking at a forecast 7.3%. And analysts are forecasting rises between now and 2027. We could have long-term capital appreciation too — especially when interest rates fall.

There are plenty of other REITs to choose from, addressing different sectors of the property market.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

Millionaire style

Quite a few millionaire investors also invest for deferred income. That is, they aim for total returns — capital and dividends — and plan to convert it to income later.

Whilst all days are good days for a dividend investment plan, some days are better than others.

Dividends can be more reliable than share prices as they’re driven by the companies performance itself and not by the whim of investors.

As part of a total return / reinvestment strategy, this income could be reinvested into income assets or back into the equity market depending on the relative valuations.

The emotional benefits of dividend re-investment. In fact, with this investment strategy you can actually welcome falling share prices.

TMPL is in the Snowball as a pair trade, where a low yield Trust is paired with a high yield Trust to maintain a blended yield of 7%.

TMPL could be sold if it prints a profit and re-invested in a higher yielding Trust or if not more shares could be bought using the Snowball’s dividend stream.

I will buy another 1k today, bringing the total to 3k as it’s xd this week.

THIRD INTERIM DIVIDEND

The Board of the Company has today declared its third interim dividend for the year ending 31 December 2025 of 3.75p per ordinary share (2024: 3.00p per ordinary share).

As described in the Company’s Annual Report for the year ended 31 December 2024, this dividend includes a 0.75p per ordinary share enhancement reflecting the Board’s decision to distribute an element of the returns earned from share buybacks within the Company’s portfolio.

It is the Board’s current intention, in the absence of unforeseen circumstances, to pay one more dividend of at least 3.75p per ordinary share in respect of the current financial year. This has raised the prospective dividend yield on the Company’s shares to 4.1%.

The third interim dividend will be paid on 30 December 2025 to those shareholders registered at the close of business on 21 November 2025.

The ordinary shares will trade ex-dividend from 20 November 2025.

Current price £3.67, most probably cheaper later today, a yield of 4%.

3i Infrastructure PLC ex-dividend date Aberdeen Asia Focus PLC ex-dividend date BlackRock Greater Europe Investment Trust PLC ex-dividend date Empiric Student Property PLC ex-dividend date Greencoat Renewables PLC ex-dividend date Gresham House Energy Storage Fund PLC ex-dividend date JPMorgan UK Small Cap Growth & Income PLC ex-dividend date Premier Miton Global Renewables Trust PLC ex-dividend date Schroder Oriental Income Fund Ltd ex-dividend date Scottish Mortgage Investment Trust PLC ex-dividend date Temple Bar Investment Trust PLC ex-dividend date

I’ve sold TRIG for a profit of £1,185.00 including the earned dividend but not yet received. There might be, in time, more profit from the Trust but the Snowball is and always will be about earning and re-investing dividends.

Because the Trust was a recent addition to the Snowball the ARR is 9,183.75%, which is only chewing gum for the eyes as it’s not repeatable.

Cash to invest £11,367.00. I might put the profit into TMPL and buy LAND as it’s xd this week.

HICL Infrastructure – Combination of HICL and TRIGDate/Time:17/11/2025 07:00:38 ▼

NOT FOR RELEASE, PUBLICATION OR DISTRIBUTION IN WHOLE OR IN PART, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES, CANADA, AUSTRALIA, JAPAN OR SOUTH AFRICA, OR ANY OTHER JURISDICTION WHERE TO DO SO WOULD CONSTITUTE A VIOLATION OF THE RELEVANT LAWS OR REGULATIONS OF THAT JURISDICTION.

The information contained in this announcement is deemed inside information under Article 7 of the UK Market Abuse Regulation. Upon publication, this inside information is in the public domain.

17 November 2025

For immediate release

Combination of

HICL Infrastructure PLC (“HICL”)

and

The Renewables Infrastructure Group Limited (“TRIG”)

· HICL and TRIG to combine to create the UK’s largest listed infrastructure investment company with net assets in excess of £5.3 billion

· Reinvigorated investment strategy enabling investment across the full spectrum of infrastructure, including core and renewables sectors, opening access to new growth assets and subsectors aligned with key infrastructure megatrends

· Diversified and resilient cash flows supporting an initial dividend target of 9.0 pence per share and compelling target NAV total return of over 10 per cent. per annum over the medium term

· Continuity of leading specialist investment management and renewables operational management teams, ensuring consistent stewardship and expertise in delivering the enhanced investment strategy

· Combination to be implemented through the reconstruction and voluntary winding up of TRIG, with TRIG’s assets transferred to HICL in exchange for the issue of new HICL shares and cash

· £350 million liquidity package, comprising a partial cash option of up to £250 million for TRIG shareholders and a further £100 million commitment from Sun Life, which has agreed terms to provide liquidity and secondary market support for the Combined Company through the purchase of ordinary shares following completion of the Combination

· Targeting completion date in Q1 2026, subject to shareholder, regulatory and other approvals

Summary

The Boards of HICL and TRIG are pleased to announce that, following extensive engagement between the two companies and a positive market sounding with large shareholders of both companies, they have signed detailed heads of terms in relation to a combination of the two companies (the “Combination“) to create the UK’s largest listed infrastructure investment company (the “Combined Company“).

The Combined Company will have an enhanced investment mandate covering the full spectrum of infrastructure opportunities, reflecting the convergence of traditional core infrastructure and energy transition assets. An initial annual dividend target of 9.0 pence per share will underpin a target NAV total return of over 10 per cent. per annum over the medium term, alongside a progressive dividend.

The Boards believe that the Combination offers strong strategic, operational and financial benefits for all shareholders, strengthening the already attractive investment cases of both companies and creating a more compelling proposition in the form of the Combined Company. Together, the Boards see an opportunity to create the premier UK listed infrastructure investment company, with greater scale, liquidity and relevance to a broader investor base.

The Combination will be implemented by way of the reconstruction and voluntary winding up of TRIG under Guernsey law, pursuant to which the assets of TRIG will transfer to HICL in exchange for the issue of new HICL shares (“HICL Shares“) and cash, enabling holders of TRIG shares (“TRIG Shares“) to elect for a partial cash exit (the “Scheme“).

Key terms of the Combination include:

– Issue of new HICL Shares: HICL will issue new HICL Shares to TRIG shareholders on a formula asset value-for-formula asset value (FAV-for-FAV) basis, with the exchange ratio determined by reference to the respective 30 September 2025 NAVs of HICL and TRIG. By way of illustration, applying the latest published NAVs for each company results in an illustrative exchange ratio of approximately 0.714173 of a HICL Share for each TRIG Share¹.

– Cash option: TRIG shareholders will have the option to elect for a partial cash exit of up to £250 million in aggregate, representing approximately 11 per cent. of TRIG’s issued share capital, priced at a 10 per cent. discount to the 30 September 2025 TRIG NAV per share, adjusted for any share buybacks undertaken and dividends declared after that date².

– Sun Life secondary market investment: Sun Life, the parent company of InfraRed Capital Partners (“InfraRed“), has agreed terms on which it will provide liquidity and secondary market support for the Combined Company by purchasing £100 million of ordinary shares following completion of the Combination.

Applying the illustrative exchange ratio above, and assuming full take-up of the £250 million partial cash option, HICL shareholders are expected to hold approximately 56 per cent. and TRIG shareholders approximately 44 per cent. of the Combined Company’s issued share capital on completion of the Combination.

Prior to completion of the Scheme, both TRIG and HICL will continue to maintain their existing quarterly dividend schedules, with dividends for the quarter ended 30 September 2025 to be paid in the ordinary course, including the third interim dividend of 1.8875 pence per share declared by TRIG on 6 November 2025. Following completion, quarterly dividends are intended to commence at the new higher annual rate of 9.0 pence per share. Dividends to be declared for the quarters ending 31 December 2025 and 31 March 2026 (subject to the timing of completion) and for the full financial year ending 31 March 2027, are expected to reflect this increased level.

InfraRed, which acts as Investment Manager to both HICL and TRIG, will continue in that role for the Combined Company, ensuring consistent stewardship of the combined portfolio and the expertise required for the delivery of the reinvigorated investment strategy. Renewable Energy Systems (“RES“) will continue to provide operational services for renewables assets within the portfolio, as it has done for TRIG since its launch in 2013.

Completion of the Combination remains subject to agreement of the final form documentation, approval by the Financial Conduct Authority (the “FCA“) of HICL’s prospectus and proposed new investment policy, shareholder approval at the general meetings of both companies, foreign direct investment clearances and other regulatory approvals, certain third party project level consents, lender consents and admission of the new HICL Shares to the FCA’s Official List and to trading on the London Stock Exchange’s Main Market for listed securities.

It is anticipated that documentation in connection with the Combination will be posted to shareholders later this week and general meetings are expected to be held in December 2025. Completion of the Scheme (the “Effective Date“) is expected to occur in Q1 2026.

The Directors of both HICL and TRIG have provided irrevocable undertakings to vote in favour of the Combination at the respective shareholder meetings in respect of their holdings of HICL and TRIG Shares. In addition, the Directors of TRIG have confirmed that they will not elect for the Cash Option (as defined below).

Mike Bane, Chair of HICL, commented:

“The combination of HICL and TRIG represents a unique opportunity to capture the key megatrends shaping the infrastructure market today, which increasingly straddle both core infrastructure and the energy transition. By combining two complementary portfolios and teams, the combined company will have the profile, expertise and access to capital to seek enhanced returns from a reinvigorated investment strategy.”

Richard Morse, Chair of TRIG, commented:

“This is a combination that we believe offers a transformational opportunity to drive growth and deliver a resilient, forward-looking investment proposition. Together, HICL and TRIG will form the UK’s largest listed infrastructure and renewables investment company, with the scale, liquidity, and balance sheet strength to better access a broader range of global opportunities and deliver sustainable long-term value for shareholders.”

If you want a chance to score big dividends, and price gains, as interest rates stay “higher for longer”…

And sail through the (inevitable) recession ahead…

These 5 stocks—and the dividend strategy I’ll show you below—could be crucial.

Dear Reader,

You’re about to unlock a dead-simple, 3-step strategy that has uncovered, time and time again, dividend stocks whose payouts are set to surge higher.

And when they do, they take their share prices right along for the (very profitable!) ride.

Even better, this proven system works no matter what the economy (or the Fed!) are doing. Because the key indicators it’s based on help sustain a stock’s price in a market storm, too.

One group of investors has been following the recommendations this stealth strategy has uncovered since 2015.

And the gains they’ve posted have been very impressive indeed.

For example, my indicators flashed BUY on a stock that went on to soar double digits during the 2022 dumpster fire … while just about every other S&P 500 stock crashed!

This strategy has built solid long-term wealth again and again. Like when another recommendation delivered a steady 148% return through ALL market weather.

And right now we’re aiming straight at 5 overlooked dividend stocks poised to DOUBLE in 5 years or less, while their dividend payouts TRIPLE.

Read on and I’ll show you exactly how.

Enter the “Dividend Magnet”

My Dividend Magnet strategy consists of 3 “pillars.”

If a stock shows all three of these telltale signs, it’s time to BUY … then ride along as the company’s dividend grows, pulling its share price higher as it does.

And today I’m going to show you, step by step, exactly how the Dividend Magnet delivered that stout 148% return I mentioned a second ago.

Then we’ll discuss those 5 stocks my research indicates are set to soar far ahead of the market in the coming years.

Personally, I think triple-digit gains are squarely on the table with these 5 hidden gems.

But conservative sort that I am, I’m forecasting steady 15%+ annualized returns for the long haul.

That’s enough to double our investment every five years and triple our income stream, too. We’ll happily take that deal! Especially with the low volatility these 5 stocks offer.

Before we go further, though, I should take a moment to tell you a bit more about myself.

But my real passion is dividend investing. You may have seen me on CNBC, Yahoo Finance or NASDAQ, where I’ve been called on to share my methodology for collecting consistent, predictable and reliable retirement income.

My readers and I don’t go anywhere near profitless techs, penny stocks or other gambles you can’t tell your spouse about.

Safety is my No. 1 priority. Always has been. Always will be.

You see, I take a strategically contrarian approach to the markets.

And for the past several years, I’ve helped thousands of readers fund their retirement thanks to what I call “Hidden Yield stocks.”

Take a look at some of the big returns my premium members have booked:

TD Synnex (SNX): Up 83% in 3 Years

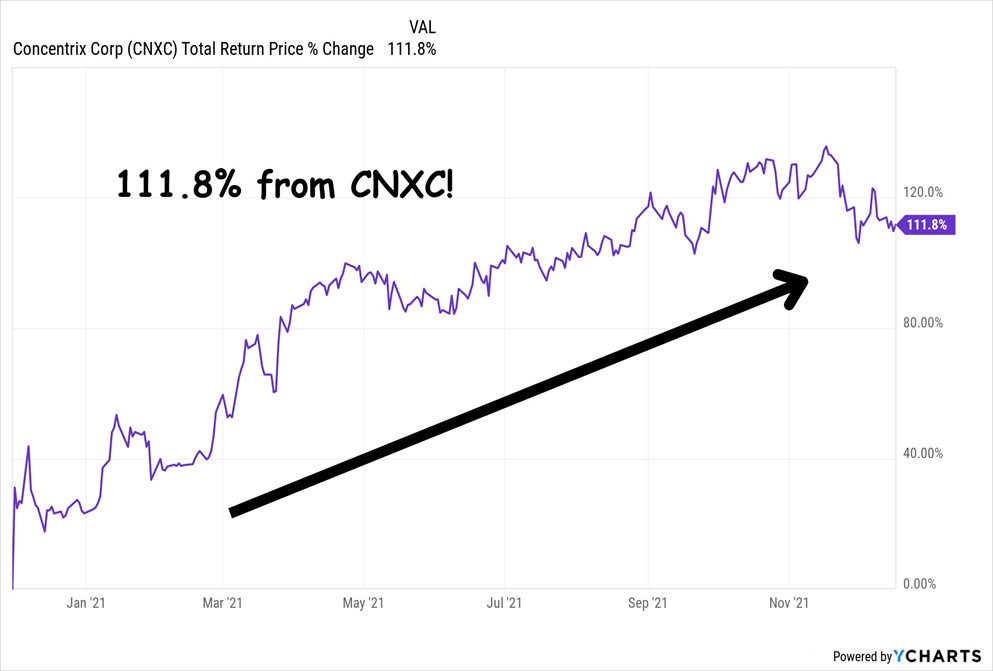

Concentrix (CNXC) Skyrocketed 111.8% in Just 1 Year!

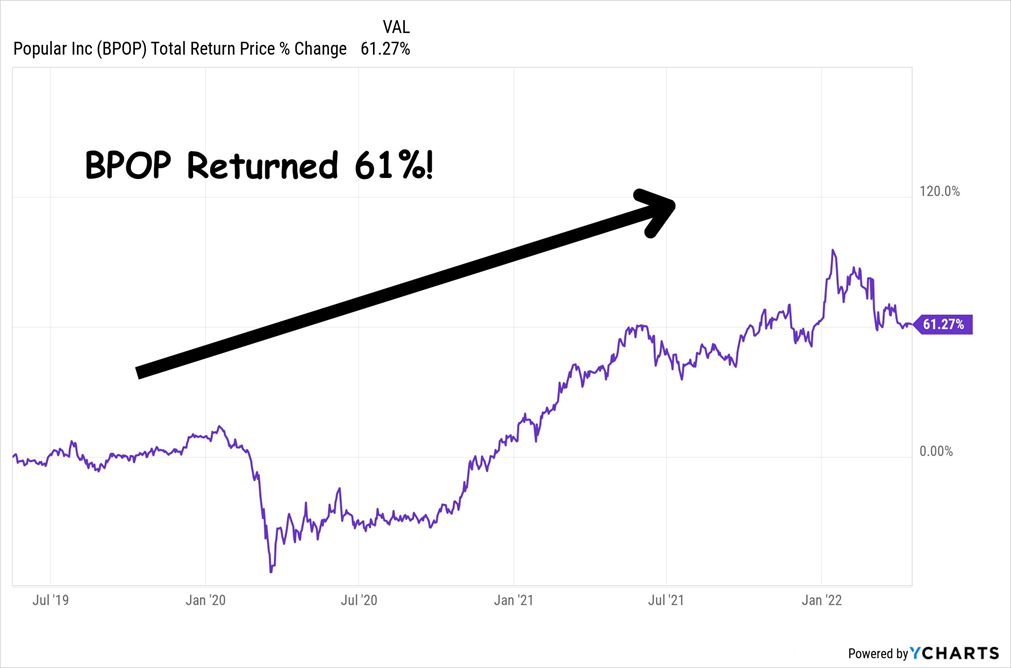

Popular (BPOP) “Popped” 61% in a Little Under 3 Years

Of course we both know investing in the stock market does come with some risk, so while we’d like every stock to go up, some recommendations do decline from time to time.

Now, as we move toward 2026, there are still plenty of oversold dividends on the board for us, despite the strong run the market’s been on. In fact, I expect our next round of picks to do even better than the ones I just showed you.

My Dividend Magnet system continues to be our North Star. I want you to join us.

Whatever your investing goal, this strategy — and the 5 dividend growers I’ll tell you about in a moment — MUST be at the heart of your investment plan.

As you might guess by this point, the humble dividend is the key to our Dividend Magnet approach—but not in the way most folks think.

How Dividends Drove a 63,894% Gain

Dividends really are the “Rodney Dangerfields” of the investing world—they get no respect!

But they should, because growing dividends are the key to thriving through any market.

And if you roll your dividends back into your portfolio, the power of compounding takes over and delivers the sort of growth that tech fanboys (and girls) can only dream of.

Here’s the proof, from our friends at Hartford Funds.

Hartford looked at the years between 1960 and the end of 2024, which included everything: the inflation of the ’70s, economic crashes in 2001 and 2008 and, of course, the pandemic.

Here’s what they found: if you’d put $10,000 in the S&P 500 in 1960, you would have had $982,072 at the end of the period, based solely on price gains.

That’s not bad: a 9,721% increase.

It shows you why most folks only think about share prices when they invest. After all, with a gain like that, it’s tough to get excited about a dividend that dribbles a few cents your way every quarter.

But here’s the thing: when you reinvest your dividends, the magic of compounding kicks in. The difference is shocking: your $10,000 would have grown to $6,399,429, or more than $5.4 million more than you’d have booked on price gains alone!

That’s a 63,894% profit.

It’s a crystal clear example of how critical dividends are. And you can grab stronger profits if you buy stocks whose dividends aren’t just growing but accelerating.

Which is exactly what we’re going to do in the first step of my 3-part Dividend Magnet strategy …

Step 1: Buy an “Accelerating Dividend”

(for Growth, Income and High Yields)

One thing we can say about today’s market is that, as employment growth slows (due in part to AI replacing expensive humans), interest rates are likely to move lower.

That setup reminds me a little bit of 2018, when rates were elevated but Jay Powell was edging toward rate cuts.

Lower rates, of course, are great for utility stocks—”bond proxies” that tend to rise as rates fall. So in November of that year, we picked up cell-tower landlord American Tower (AMT), a REIT whose “tenants” include AT&T (T) and Verizon (VZ).

We liked AMT because it’s a classic “tollbooth” play.

The company charges its clients for using its tower network, then hands that cash to investors as a steadily rising dividend. Buying AMT is a much better move than trying to pick winners among the big telcos.

You can see that in AMT’s performance as rates fell during our holding period: It crushed Verizon, America’s biggest telecom provider. (Verizon’s market leadership was no help to its shareholders in this period—they actually lost money, even with the company’s storied dividend included):

Even better, unlike pretty much any other stock, AMT had been raising its payout every quarter, to the tune of 65% during our holding period!

That rising payout acted like a “Dividend Magnet,” pulling up the share price in lockstep and delivering the 57% total return you see above. AMT also kept the hikes rolling through the pandemic, “magnetizing” the shares as it did!

That’s the “Dividend Magnet” in action—I’ve seen it work its magic on share prices time and time again. Like with our next stock, a chipmaker founded way back in 1930.

TXN’s “Accelerating” Dividend Powered

Us to a 148% Return

Texas Instruments (TXN) isn’t the stodgy calculator peddler it was 30 years ago. Today its analog chips power everything from appliances to industrial sensors.

Management is known for making shareholders’ interests a priority, and it doles out that cash to them on the regular. Those payouts, in turn, have powered the stock’s Dividend Magnet.

TXN’s dividend soared 120% over the 5 years we held it, helping us bag that 148% total return I mentioned earlier.

It was all thanks to the Dividend Magnet, which you can see pulling up TXN’s share price:

TXN’s Dividend Magnet Fires Up

130% dividend hikes. 120% price gains!

Add those payouts and gains together and you get that stellar 148% total return.

The two “dividends up, share price up” patterns I just showed you were no coincidence.

In fact, this predictable setup can not only tell us when to buy, but when to sell, too …

Consider utility American Electric Power (AEP), which I recommended in February 2024. My readers only held this one for a short time, for the best of reasons: It took off! By the time we sold in October, we were sitting on a sweet 27% total return.

But the reason why we bought AEP in the first place was its powerful Dividend Magnet. In the preceding decade, its payout had shot up 76%, and its share price had tracked it higher point for point.

Though by February 2024, a gap had opened up. That was our “in”!

AEP’s Payout Pulled Its Share Price Higher, Until a “Payout Gap” Gave Us Our Shot

We pounced. And by October, the share price had closed the gap. This was important because when a share price catches up to a dividend, and moves past it, it’s a key sell signal.

Share Price Catches the Payout, and We Take Profits

Once the 10-year gap between the price and dividend “reconnected,” we took our quick 27% gain off the table. And rolled it into the NEXT dividend grower!

This is hands-down the most exhilarating part of investing in Dividend Magnet plays like these: When investors (finally) catch wind of them, the stock can pop virtually overnight!

Do all of our calls work out like these? Of course not. I wouldn’t insult your intelligence and say they do. Investing in the stock market involves some risk, even with top-quality large-cap names like these, and you can lose money.

But I think you can see where I’m going here: we buy accelerating dividends, ride them higher and collect bigger payouts and price gains over time. This gives us a huge built-in advantage over investors who rely on traditional measures like earnings per share (EPS) growth, P/E ratios or whatever.

Now that we’ve seen how the Dividend Magnet can tell us to buy (and sell), let’s boost our payout-powered gains with a (wrongfully!) disrespected share-price driver: share buybacks.

Step 2: Toss in a Buyback “Afterburner”

Buybacks get a bad rap, but they shouldn’t, because when done right (i.e., when a stock is cheap), they can light a fire under share prices.

They work by cutting the number of shares outstanding, which boosts EPS and, in turn, share prices. They also boost our dividends because they reduce the number of shares on which a company has to pay out.

And when you combine a solid buyback program with an accelerating dividend, you get something very special indeed!

To see what I mean, let’s loop back to Texas Instruments. The company backstopped its Dividend Magnet with a steady buyback program during our holding period.

That took nearly 7% of its shares off the market:

TXN’s Buybacks Give Its Stock an Extra Kick

As you can see, the company’s Dividend Magnet is humming along beautifully, pulling the share price up as it goes.

Meantime, the buybacks kicked in an extra boost, pushing the shares ahead of TXN’s dividend growth!

Step 3: Use This Powerful Indicator for

Extra Dividend (and Share Price) Safety

Finally, we’re going to safeguard our gains and dividends by purchasing stocks with low beta ratings.

Beta what?

Don’t get too hung up on the jargon here.

Beta is a measure of volatility that you’ve probably seen on your favorite stock screener. A stock with a beta of 1 moves at roughly the same speed as the market (up or down). Betas below 1 are less volatile; those above 1 are more volatile.

For example, consider pharma giant AbbVie (ABBV), whose sturdy business results in a steady stock price.

ABBV has a 5-year beta of 0.52, which means it’s 48% less volatile than the S&P 500.

In other words, on days when the S&P 500 is down 3%, this stock should be down less than 2%.

That’s the theory.

In reality, it’s even better.

AbbVie is one of a tiny group of equities that actually gained through the 2022 mess, and by no small amount, either:

ABBV Soared in the 2022 Market Mayhem

Plus, this stock has a potent Dividend Magnet!

Check out how the share price (in purple below) has tracked the payout (in orange) over the last decade, during which we’ve seen rate hikes, rate cuts, a global pandemic, surging inflation and, yes, trade wars.

ABBV’s Dividend Magnet Drives Steady GAINS

Despite COVID, Inflation, Trade Wars and More

We’re not recommending ABBV today, because the share price has leapt ahead of dividend growth, as you can see on the right side of the chart above. This shows that ABBV is currently overvalued.

Taken together, this gives us a clear picture of how a rising dividend, buybacks and a low beta rating give this one downside protection, making it a true “recession-proof” dividend.

This is a sector in which you need to be very selective to succeed.

MicroStockHub/iStock via Getty Images

I’m a strong proponent of REIT investing (VNQ). I invest about half of my own portfolio in REITs and regularly write bullish articles on them here on Seeking Alpha. Some of you may even call me a REIT cheerleader.

But even then, I’m objective enough to recognize that not everything is sunshine and rainbows in the REIT sector.

In fact, I would go as far as to say that the REIT sector has a dark side, which represents a large fraction of it, and should be avoided at all costs.

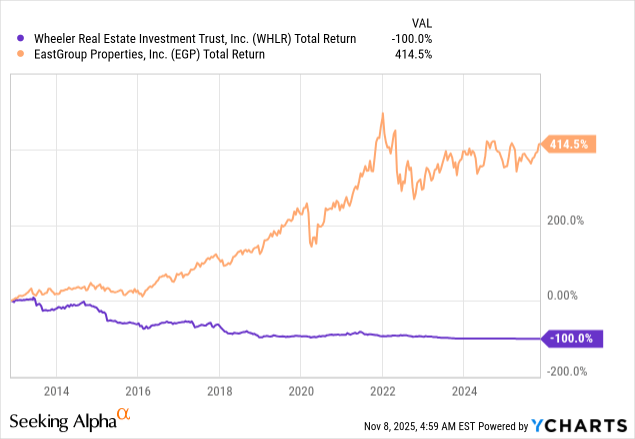

This is a vast and versatile sector, and just because two companies share the REIT acronym does not mean that they have anything in common. To give you a good example, consider the case of Wheeler REIT (WHLR) vs. EastGroup Properties (EGP). Both are REITs. Yet, one would have earned you a little fortune, while the other one would have lost you everything.

Data by YCharts

In today’s article, I’m going to discuss this dark side of the REIT sector and how to avoid losers like Wheeler in the future.

Dividend Traps

The unfortunate reality is that a lot of REITs are paying dividends that are not sustainable.

Just in the past few years, I have correctly predicted nine REIT dividend cuts in my various articles. All of these have cut their dividend by at least 20% since then:

The reason why so many REITs end up overpaying is that their management teams and boards are trying to make their company as compelling as possible to REIT investors, most of whom are income-oriented.

They know that a higher dividend may help them reach a higher valuation, which could then give them access to equity markets to raise more capital and accelerate growth. This can then allow them to further hike the dividend.

But, in doing so, they often end up setting the dividend too high from the start, leaving little room for error in case of future setbacks.

Eventually, setbacks occur, the dividend becomes unsustainable, but management teams and boards will often still resist cutting the dividend for a while, knowing that it would disappoint investors and hurt their market sentiment.

This then forces them to take on more debt to fund their dividend, only putting them in a worse position.

Eventually, after delaying the inevitable for a while, they still have to rip off the Band Aid, which then often leads to sharp sell-offs as frustrated shareholders sell the stock.

Therefore, it’s crucial to assess the dividend sustainability of a REIT before investing in it.

And it’s not as easy as checking the payout ratio. There are lots of REITs with a relatively low dividend payout ratio that still cannot sustain their dividend.

You also need to look at the leverage, the capex requirements, the cash flow growth prospects, and the track record of the REIT.

Overleverage

Many REITs are also overleveraged, and again, this is often the result of conflicts of interest between the manager and shareholders.

REIT managers are generally incentivized to grow their FFO per share, and the easiest way to achieve that is to take on more leverage and buy additional properties. As long as the cap rate is higher than the interest rate, this should grow the FFO per share, granting REIT managers their performance-based bonuses.

But this only works for so long. Eventually, the REIT runs into some setbacks, and the losses are then amplified by the leverage, often forcing the REIT to sell assets, raise equity, and/or cut the dividend, all of which can then permanently impair equity value.

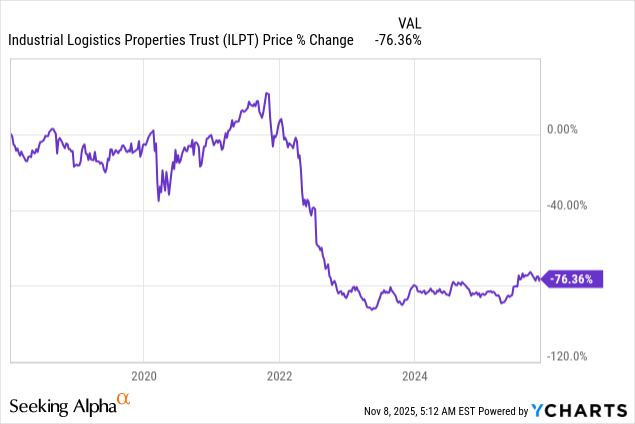

Take the example of Industrial Logistics Properties Trust (ILPT). The REIT owns great assets, but management took on too much leverage in an attempt to grow faster, and here are the results:

Data by YCharts

History has shown that the most rewarding REITs are those that are conservative with their leverage, as this leads to more consistent results across the cycle and allows the REITs to play offense during times of crisis, often acquiring properties for pennies on the dollar from distressed sellers.

I try to stick to REITs with LTVs below 50%, but ideally, closer to 30%. Some REITs in my portfolio, such as EastGroup Properties and Big Yellow Group (BYG/OTCPK:BYLOF), have LTVs as low as 10%. Naturally, this results in lower yields and higher valuation multiples, which is why many investors aren’t interested in them, but it also results in faster growth, lower risk, and higher total returns over time. The trade-off is well worth it, in my opinion.

Secular Headwinds

REITs invest in more than 20 different property sectors, and some of them are facing severe headwinds.

The office sector is the most obvious example. Vacancy rates are today at an all-time high of more than 20% as a result of the growing trend of remote and hybrid work. Moreover, I expect the AI revolution to only make things worse as it will lead to significant white collar job disruption, reducing the need for office space, and pushing tenants to require more flexible lease terms. This could then make it harder to finance these assets, pushing cap rates to higher levels, and leading to significant value destruction.

BXP

But it’s not just the office. Hotels are another sector with uncertain prospects. The post-COVID rise of Zoom (ZM) has permanently reduced business travel. It has also accelerated the growth of Airbnb (ABNB), which is leading to more supply, price competition, and ultimately lower margins. Finally, booking websites are also ever-growing, more powerful, and taking a greater share of the revenue as hotel flags lose value.

Host Hotel

Most Class A malls are today doing surprisingly well, but as AI supercharges the growth of e-commerce with more powerful and personalized marketing, cheaper shipping, and an explosion in small e-commerce business formation (as it also reduces barriers to entry), I expect more pain for traditional retailers who fail to adapt, which could then lead to more trouble for malls.

Simon Property Group

Mortgage REITs also have a notoriously poor track record due to their businesses being too heavily dependent on macro factors that are out of their control. Even small changes in interest rates and spreads can make or break their businesses, which makes them quite unattractive, in my opinion.

And there are many other examples…

This is a sector in which you need to be highly selective because not all property sectors are well positioned for the long run.

Share Dilution

Finally, some REITs, especially those that are externally managed, will often issue new equity in an effort to buy more properties and grow the size of the portfolio, as this may justify higher management fees for themselves.

This is all fine as long as they are raising the equity at a price that’s high enough to earn a positive spread on new investments. The problem is that many of these REITs will not hesitate to issue equity even when they trade at a discount to NAV, resulting in a negative spread and diluting shareholders.

This can then negate all the potential benefits of the REIT, as constant dilution leads to poor performance.

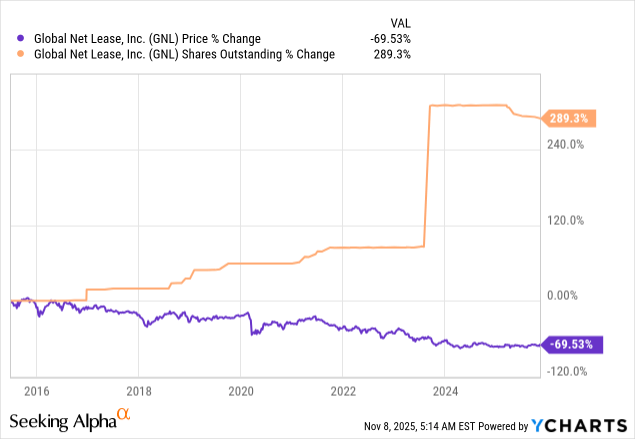

I think that Global Net Lease has been a victim of this in the past. Just look at the clear inverse correlation between its share price and its rising share count:

Data by YCharts

This is why I have previously argued that investors should always start their REIT analysis by taking a hard look at the management team. Nothing else matters if the management is going to dilute you time and time again.

Bottom Line

If you look at my past articles here on Seeking Alpha, you will note that I regularly cover REITs to avoid and others that are likely to cut their dividend.

I make it a point to cover the good and the bad because no sector is ever perfect, and knowing what not to buy is often just as important, if not more, than identifying good investment opportunities.

We, of course, aren’t perfect either. At High Yield Landlord, we have suffered quite a few losses in our portfolio lately. But fortunately, we have had many more winners over the years as well.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.