If you are still not sure that a dividend re-investment plan is suitable for your portfolio or part of you portfolio. Maybe Warren Buffet will convince you.

Warren Buffett just collected another $204 million from Coca-Cola — a reminder that some of the most powerful returns on Wall Street come from patience, dividends, and owning the right business for decades.

Here’s how that payout breaks down, why Coca-Cola keeps funding Berkshire’s war chest, and what this kind of compounding looks like in real dollars.

Coca-Cola has been one of Warren Buffett’s signature bets since the late 1980s, and it’s still paying like clockwork.

Berkshire Hathaway owns 400 million shares, and Coca-Cola’s $0.51 quarterly dividend just delivered a $204 million payout. Sometimes the biggest wins aren’t dramatic. They’re automatic.

Coca-Cola dividends now bring Berkshire over $800 million a year, far beyond the original $1.3 billion cost. Coca-Cola may have its “secret” headlines, but Buffett only cares about one secret: the dividend arriving every quarter.

Why Coca-Cola Still Matters Coca-Cola isn’t just a dividend machine, it’s still a modern profit engine.

With a market cap around $289 billion and gross margins above 61%, the company keeps doing what it does best: defend pricing power, stay everywhere, and find small ways to sell more. Mini cans. Convenience-store pushes. Product tweaks that look boring up close, but scale fast when you’re global.

That durability is why some Wall Street analysts still see upside, with price targets reaching $80. This implies that Coca-Cola is still being priced as a cash machine with staying power. And for Berkshire, that’s the whole point. No hype. No chasing trends. Just owning a durable cash machine, year after year, and letting dividends and compounding do the heavy lifting.

This is where most investors get caught. They chase the hot stock, the pop, the quick win, and end up trading emotions instead of building wealth.

Buffett plays a different game. He doesn’t need to react to every headline. He owns businesses that pay him, then lets time and dividends do the work.

The difference isn’t access to information. It’s behavior, and the traders who last tend to rely on rules, not emotion, like stop-loss and take-profit orders

Why This Dividend Story Matters That $204 million payout is more than a headline number. It’s what long-term investing looks like when the business is durable and the cash flow is real.

While plenty of investors chase the next spike, Buffett’s Coca-Cola stake shows the quieter path: own a high-quality company, let the dividend stack up, and give compounding time to do its job. You don’t need to love soda to take the point, you just need to respect what consistent payouts can build over decades.

Compound interest takes time to make a difference to your portfolio but when markets sell off you will be getting more shares for your money and a better long term retirement. All eyes on the prize.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

I’m a big fan of UK stocks – I think they offer a unique combination of strong businesses and low valuation multiples. But which ones can do well in 2026?

It’s impossible to say with certainty what the stock market will do in the next 12 months. But investors have some pretty clear signs they can pay attention to for clues.

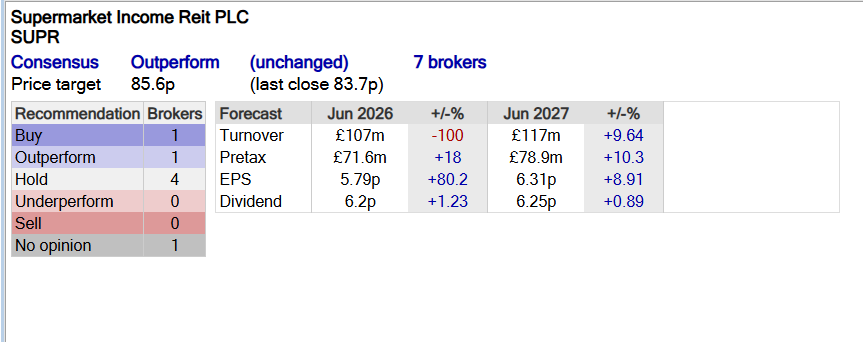

Should you buy Supermarket Income REIT plc shares today?

Economic outlook

Different businesses are suited to different economic environments. So a lot of the question of which stocks will do well in 2026 comes down to what the economy will be like.

The early signs aren’t particularly positive – growth’s expected to be slow and unemployment’s set to rise. The good news though, is that inflation is forecast to fall as oil prices drop.

A lot can happen in the next 12 months. But the early indications suggest that businesses that can generate steady cash flows in a relatively tough environment should be attractive.

That points towards companies that don’t target discretionary spending. So promising sectors include consumer defensives, healthcare, real estate, and utilities.

Real estate

One stock that seems to fit the bill is Supermarket Income REIT (LSE:SUPR). The company is a FTSE 250real estate investment trust (REIT) that leases a portfolio of retail properties.

Supermarkets as an industry should be relatively resilient, even in a challenging economy. People might change where and how often they shop, but they’re unlikely to stop entirely.

With tenants including Aldi and Lidl, as well as Tesco and Sainsbury’s, this should be fine for Supermarket Income REIT. All that matters is that its tenants are able to pay their rent.

For investors, that means a 7.5% annual dividend. And that might be attractive – especially in a tough environment – so I think there’s a decent chance the stock could do well in 2026.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice

Long-term investing

I think anyone looking for a UK stock that has a good chance to do well in 2026 should take a look at Supermarket Income REIT. But I’m less convinced when I look further ahead.

Almost two-thirds of the company’s leases have more than 10 years left. That’s good in terms of stability, but it means the chances of meaningful growth over the next decade are minimal.

Furthermore, 71% of the firm’s rent comes from Tesco and Sainsbury’s. This limits the risk of defaults, but it also means it isn’t in a strong position when it comes to negotiating extensions.

Both of these might be positives in an environment where economic growth across the board’s likely to be limited. But in a stronger economy, they’re likely to be obstacles.

Stocks for 2026

Different investors will – rightly – have different ambitions. And I think that means Supermarket Income REIT’s worth considering seriously for some and not others.

I expect the stock to do well in 2026 and provide steady income going forward. But for investors looking for long-term returns, I think there may be better opportunities available.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

The hunt for good income shares in 2026 is already on. Yet, when trying to make a good second income, it’s not just about which stock has the highest dividend yield. That yield also needs to be sustainable and have a good track record. With a lot of factors at play, I turned to ChatGPT to see if it could offer any wisdom in this regard.

Revealing the pick

Interestingly, the AI chatbot decided to make a pick from across the pond in the US. It chose Johnson & Johnson (NYSE:JNJ) as the most reliable dividend stock right now. On the face of it, I can see why it made the choice. The company has a whopping 63 consecutive years of dividend increases. It has averaged an annual dividend growth rate of 5% for the past decade, with the share price up 44% in the last year.

In terms of reliability, it has a strong and diversified business model. This ranges from pharmaceuticals to everyday health products, with stable demand. As a result, the wide product spread reduces risk and makes earnings more predictable.

All of this sounds great, but ChatGPT missed one key point, namely the dividend yield. At the moment, the company’s yield is 2.51%. For comparison, the average yield of the FTSE 100 right now is 2.99%. If an investor could buy an FTSE 100 tracker that paid out the income from all the stocks in the index, why would they want to buy just one stock instead and get a 0.48% less annual yield in the process?

Of course, I’m not saying just go for super high-yielding stocks. But to pick a company with a low dividend yield just because it has been paying it for decades doesn’t seem like the best move.

The best of both worlds

Instead, I’d prefer to own a company with a strong track record and an above-average yield. For example, the Supermarket Income REIT (LSE:SUPR). It boasts seven years of consecutive dividend growth, with a current yield of 7.56%.

A plummeting share price isn’t causing the high yield. Instead, the stock has risen by 18% in the past year. The elevated yield is thanks to continued dividend-per-share increases, which is a good sign.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

The latest full-year results presentation showed a 7.3% annual increase in the net rental income, showing demand is strong. Only last month, it announced a £98m acquisition of three UK supermarkets. This move should act to boost income almost straight away, with an anticipated initial yield of 5.5%.

Such details, along with the consistent performance of everyday operations, make it an appealing and reliable income stock. Of course, there are risks, such as the debt exposure it takes on to fund new projects. If interest rates stay higher for longer this year, servicing its debt might become more expensive. Yet even with this, I think it’s a better stock for investors to consider than the pick from ChatGPT!

The FTSE 100 hits 10k ! Here’s why the odds of a stock market crash have risen.

Jon Smith explains why a rising UK stock market might not marry up with the underlying situation in the UK, and talks about stock market crash scenarios.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

On 2 January, the elite UK stock market index broke above 10,000 points for the first time. It’s a big milestone and cements the strong rally it’s been on since the tariff-induced falls back in April last year. Yet despite all the cheers, I think the odds of another stock market crash have risen. Here’s why.

Complacency creeps in

The pop over the past couple of weeks has come more from positive global risk sentiment. Even though this is good, I think the UK stock market is being carried by this, rather than by strong UK-specific factors. In fact, given the state of the economy, I believe some investors are becoming complacent.

The latest GDP figure for Q3 showed anaemic growth of 0.1%. In more recent data, the unemployment rate has risen to 5.1%, the highest level since 2021. There’s also growing chatter about a rise in struggling firms. This fuels worries about underlying economic weakness that could hit corporate earnings.

Yet for the moment, the stock market is being carried higher. This is fuelled in part by rising valuations for AI and tech companies in the US. If we see a correction in this area, it could pull the FTSE 100 lower. At that point, people might start to behave more as if the UK economy isn’t in the best shape, compounding the problems.

Given that the UK data has been deteriorating in recent months, along with the increase in US tech valuations, I think the odds of a crash have risen.

How to handle it

I don’t want to be seen as someone who’s completely doom and gloom. Despite my view that the odds of a big move lower are increasing, I still don’t believe we’re going to see a sharp fall immediately. However, I think it’s worth considering some defensive stocks at the moment to help protect a diversified portfolio.

For example, Associated British Foods (LSE:ABF) is a food company that owns famous brands, including Kingsmill bread and Ovaltine, as well as operating at the beginning of the supply chain via manufacturing and selling raw ingredients.

Over the past year, the share price is up 5%, with a dividend yield of 2.93%. This doesn’t make it a high-growth stock, but it has several qualities that make it a good defensive idea. For example, it generates revenue from multiple divisions, some of which are entirely unrelated to others. Furthermore, it owns brands that sell everyday groceries and staples. People buy these regardless of the economic cycle.

It’s a global company too. So even if the UK underperforms, it can offset any negative impact here from sales around the world.

And of course, we can’t ignore its Primark unit. It’s one of the biggest names in fast fashion and is continuing to expand in the UK, Europe and US.

As a risk, it’s exposed to commodity prices (such as wheat and sugar), which can be very volatile. This can mean that costs of production could increase without much warning. And Primark, while huge, has been rather sluggish of late. Despite this, I think it’s a good stock to consider if someone is worried about the chance of a crash.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Dividend stocks are a popular way for some investors to generate passive income. Owning the stock gives them the right to receive a cut of the company’s declared dividend. And this money can be reinvested back into the stock market, compounding the benefits. Here’s how the strategy could play out over time.

Putting the money to work

With £10k in savings, it provides a good initial pot of cash to put to work. To begin with, I’d look at what yield the investor is trying to target. After all, the £10k is likely only earning 2%-3% annual interest in a regular savings account. Therefore, the added risk of buying stocks (where the capital can fluctuate in value every day) must be offset by a higher reward.

The average dividend yield of the FTSE 100 is 2.99% so I don’t think it makes sense to invest in a tracker. Instead, an investor could actively pick a selection of stocks in the 6%-8% range. The potential income is high enough to warrant withdrawing funds from savings and investing them in the market.

The next factor is assessing how long it could take to reach the goal of £455 a month in dividends. If only the initial £10k were used and no further money were injected, it could take 30 years, with an average yield of 7%. That’s a long time! However, if an investor could supplement the lump sum with £250 each month, it could take just under 12 years.

Of course, there’s no guarantee on these timeframes. The hot income stock of today could struggle years down the line, cutting the dividend. That’s why it’s good to have a diversified portfolio, so at least if this does happen, the impact can be manageable.

Boosting dividend payments

Actively picking good dividend shares in the 6%-8% yield range needs some research. One example to consider that I’ve researched is Chesnara (LSE:CSN). It has a current dividend yield of 7.2%, with the share price up 30% in the last year.

The FTSE 250 company isn’t the most traditional insurance and pensions firm, as it focuses on buying and managing existing life insurance and pension policies. It earns fees from administering these policies and profits from managing the investments backing them.

Its CEO said in the interim results in August that it saw “cash generation up 26%, an increase in our solvency ratio and a further 3% increase in the interim dividend”. Further, in December, it got regulatory approval for the takeover of HSBC’s UK life insurance division. This has boosted investor sentiment already, but could help even further as more details about the extra £4bn of assets under administration and 454,000 policies come through.

Against this backdrop, the dividend per share has been rising for several consecutive years. I can see this continuing based on the momentum from last year. However, one risk is that the stock market underperforms this year, leading to volatility in the assets Chesnara manages. This could not only hurt earnings but also cause reputational damage for clients who have their money with the firm.

Overall though, I think it’s a good stock for investors to consider as part of an overall strategy.

When/if SUPR continues up to the broker’s target, as it’s just below resistance those that trade TR may take some or all of their profit.

When/if SUPR continues up to the broker’s target, as it’s just below resistance those that trade dividend re-investment may take some of their profit but continue to hold for the dividends.

Those that hold for the dividend to pay their bills may just continue to hold until the yield falls and they switch positions.

Dunedin Income Growth: positioning for resilient returns across market cycles

Ben Ritchie and Rebecca Maclean outline recent portfolio changes, mid-cap opportunities and how Dunedin Income Growth balances income, quality and sustainability.

Kepler Trust Intelligence

Updated 07 Jan 2026

Disclaimer

This is a non-independent marketing communication commissioned by Aberdeen. The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

Video

Ben Ritchie and Rebecca Maclean, co-managers of Dunedin Income Growth Investment Trust (DIG), discuss recent portfolio changes, including additions such as Tesco, Softcat and Experian, alongside exits where fundamentals have weakened. They explore why UK mid-cap valuations look compelling, the impact of interest rates, geopolitics and investor flows, and how a focus on cash generation, dividend growth and a differentiated sustainable investment approach underpins the Trust’s long-term income and return objectives.

Transcript

Hi, my name is Ben Ritchie. I’m the co-manager of Dunedin Income Growth Investment Trust. We’ve made quite a lot of changes to the portfolio in the last six months. And I think that reflects two things. One, the ongoing compelling valuations that we’re able to find in the UK and European equity market. And secondly, the strength of the idea generation that we have within our wider team of UK equity specialists. We’ve added a number of really interesting companies to the portfolio that have a combination of enduring long-term growth potential and very attractive implied returns combined with strong cash generation and the ability to pay high and growing dividends back to investors.

Just to give you a flavor of some of those, we’ve added Tesco into the portfolio, the UK supermarket, a business with a tremendously strong market position that we think is going to get only stronger from here, will be increasing its returns, growing its margins, accelerating its top line development and ultimately returning that back to investors in the shape of dividends and buybacks.

We’ve also initiated some smaller positions in Experian and Compass Group. Experian is the credit rating agency and data provider, very significant businesses in the United States, but also strong positions in the UK and Latin America. That’s a business that we think is going to grow very nicely, particularly on the back of enabling AI and its products. We see strong, consistent revenue growth, again, resulting in cash generation and good, consistent dividends back to investors.

Compass is another business we like, the global specialist in contract catering, a very difficult business to compete in. They are by far the global number one, dominant positions in a wide range of markets. And a company that we think can grow at high single digits, expand its margins, make acquisitions, buy back stock, and ultimately grow earnings at a good double digit clip on a relatively consistent basis.

The thing that pulls these companies together is that they are relatively acyclical. Yes, economics matters. But ultimately, we expect these businesses to be able to grow regardless of the economic cycle. And we think that’s a really important point. Having had a pretty extended period of relatively ok markets, when things get tougher, we think these companies are in a good position to be able to continue to perform very well.

On the other side of that, we’ve been tending to some of the businesses that have found life a little bit more difficult. And while we’re long-term investors and we want to back businesses for the long term, ultimately, sometimes it does just get a little bit too difficult. So, we’ve exited out of chemical distributor Xalys, which has found significant end market declines as consumption of chemicals across the world has been put under pressure, partly by Chinese production, but also by the relatively subdued economic environment and that’s put pressure on their business model.

And the other company which we’ve exited during the period would be Novo Nordisk, a well-known firm, a specialist in diabetes provision and also in obesity treatment, but where they seem to have lost the race to dominate the obesity category with Eli Lilly and we took the opportunity to sell out of that in the middle of the year. And that capital which we freed up, we’ve been able to reinvest back into some of those more compelling opportunities that I’ve talked about.

So, a pretty active period for us within the portfolio. We still see plenty of opportunities. The hopper of new ideas has never been fuller. We see compelling opportunities across the market cap spectrum and really we’re pretty excited about what awaits over the next six months as well.

Hello, I’m Rebecca Maclean and I co-manage Dunedin Income Growth Investment Trust. So, one of the aspects of the strategy is that we invest across the market cap spectrum. So, we have currently about 45 % of the portfolio in companies with a market cap below £10 billion and we’re seeing lots of opportunities within the mid-cap space.

And actually, if you look at the valuation of the mid-cap market in the UK, the FTSE 250, it’s showing quite an unusual yield signal. So, the dividend yield on the mid-cap index is now higher than the large-cap index, which is very unusual given historically the level of dividend growth that we have seen out of smaller businesses compared to larger companies, which are typically in more mature markets. So, valuation is certainly signaling interesting opportunities within the MidCap space.

We have a number of holdings within this, so one is Softcat, which is the UK’s leading value-added reseller of technology to SMEs in the UK. It’s benefiting from structural growth in terms of demand for technology. But it’s also gaining market share because it has a broad offering, it’s meeting its customers’ needs in terms of helping them find what technology solutions will be best for them and they’ve got a very strong culture too. So this is a company which has delivered excellent growth historically and we expect strong growth in the future, it’s cash generative and this supports an attractive and growing dividend plus special dividends too given the strength of their balance sheet.

In terms of what are the catalysts to help mid-caps going forward after a period of underperformance compared to their large cap peers, I think there are a couple that I’d highlight. The first would be to look at the macro because the mid-cap area is more domestically focused. And I think if we saw an improvement in economic activity, consumer confidence and business confidence, this will certainly help some of those cyclical sectors, whether it’s house building and real estate, which are currently trading towards the trough of their cycle.

The second catalyst is interest rates. So typically these businesses are more interest rate sensitive. And if we look at the inflation data that’s been printing in the UK, this is supporting our economist view that interest rates will continue to be cut. So our economists are expecting another 25 basis points cut in December and another three basis points, three cuts in 2026. So this will be supportive for the mid-cap part of the market. And finally, the picture has been clouded in the UK by persistent outflows out of UK equities. And this has disproportionately impacted smaller and mid-sized businesses compared to large-cap companies.

So I think if we saw a shift in terms of investors allocation towards the UK and an inflow into UK activities, this would be supportive for that part of the market. We certainly see mid caps as being attractive hunting grounds for looking for quality and resilient businesses, which are now screening to be at an attractive valuation.

Well, geopolitics is always a big driver of companies within the portfolio. And I would say it has been a headwind overall over the past few years. I’d pick out three specific developments. First of all, within the UK, we’ve certainly seen a consistent degree of political tumult. We’ve seen indecision around economic decisions from both the previous government and the current government. And that has been unhelpful, particularly for domestic-facing companies. At the same time, we’ve seen Donald Trump and the global tariff trade war, again, has been unhelpful for businesses looking to export and do business overseas and again that has been a headwind.

And one of the drags that’s been ongoing and continuous both I think affecting companies we don’t own and to some degree affecting companies and the wider market in which we do invest has been the Ukraine conflict. The Ukraine conflict has certainly driven up inflation in Europe and the UK and has also significantly boosted the defence sector, a sector which we can’t access given our sustainability criteria.

So these geopolitical elements have been something of a headwind for the Dunedin portfolio over recent times. But the good news is we think that some of these things are starting to ease. Tariffs will annualise as we move through 2026. We don’t think that’s going to happen again. If anything, they may become looser. And that, we think, will benefit those overseas international companies. And we’ve tended to favour those types of global businesses with wider reach and better growth prospects.

I think again when we think about the Ukraine, perhaps it’s more likely that we’ll see a resolution there. And that could be very helpful in terms of energy and commodity prices, both in the UK and abroad. And both of those elements could also come together in terms of helping to generate a little bit of weakness in sterling as well, which has been very strong and again acted as a bit of a headwind. And in terms of the domestics, we don’t have great expectations for this government. We don’t have great expectations for the economy.

But I don’t think anybody else does either. And the opportunity to create some form of stability that companies can work with and build off is definitely there. By the time you’re listening to this, we will have had the budget. We hope that at the very least, it doesn’t make things more difficult for UK corporates, but we think it’s very much unlikely to have the same negative impact which we saw from the same event 12 months ago. And so if we can see stability on the domestic front, we think there’s a big prize to go for.

From the Bank of England potentially being able to reduce interest rates, which could be a significant tailwind for the UK economy and the Dunedin portfolio. We’re optimistic about 2026 and the impact of tariffs and there could even be some benefits to come through from a resolution to the conflict in the Ukraine. And so the geopolitical environment having been unhelpful over the last two to three years could turn, if not into a tailwind, then certainly into a much more neutral platform for the portfolio.And that could be very good news for us.

So one of the points of differentiation for the need in income growth is that the Trust does have a sustainable investing approach, which is unique in the UK Income Investment Trust market. And as a reminder, there are three-pronged approach. So there are exclusions in place which are in place in order to reduce the portfolio’s exposure to parts of the market which face the highest environmental, social and governance risks.

We also have a positive allocation to companies that we see are leaders in ESG, companies that provide sustainable solutions, but also companies that we believe are going to participate in a transition and improve their sustainability performance over time. And thirdly, we look to engage in our portfolio, so meeting our companies regularly, discussing these issues with them in order to understand their concerns, the risks and the opportunities and support these businesses through their journey.

So, part of the element of the approach is to have exclusions. It’s about 25 % of the FTSE All-Share, which is excluded according to this policy. And if you look at the impact of that on the investable universe, we see no impact on their ability to generate income from looking at that investable universe that’s screened from our sustainability perspective. So, that’s supportive.

From a performance perspective, there have been parts and times when the sustainability screen has been a headwind. So I’d point to the start of 2022 after the Ukraine war where we saw a spike up in commodity prices. This did lead to a headwind in terms of relative performance of that investable universe versus the benchmark. And this year again, when we look at the aerospace and defense sector, which is up over 85 % the year to date, then, and that’s part of the sector of the market that we don’t invest in, that has been a headwind.

But if we look over the longer term, we don’t see it as a material headwind to performance. Sustainability is very much aligned to our approach when we think about the quality of businesses. Indeed, it’s one aspect of quality which we assess when we’re looking to select the highest quality companies for the portfolio. And we’ll continue to do that in line with our investment strategy, which is to focus on total return, quality and resilient businesses that meet the company’s sustainable and responsible investment policy.

If you need any more information about Dunedin Income Growth Investment Trust, please visit our website for more information.

Energy Yields Up to 8.4% While Herd Chases Orinoco Pipe Dream

Brett Owens, Chief Investment Strategist

Wall Street is treating Venezuela like the next “black gold” rush.

Nah—I don’t think so. Let me explain why and share my favorite US-based energy dividends up to 8.4%.

Vanilla investors are piling into the majors like Exxon Mobil (XOM) and Chevron (CVX), betting that regime change is a “buy” signal for anyone with a drill bit near Venezuela’s flush Orinoco Belt. But we careful contrarians know better. Energy infrastructure does not simply bounce back overnight. (Fictional TV “landman” Tommy Norris is not taking a plane south to instantly fix production with a few phone calls, hard lines and Michelob Ultras!)

Venezuela’s oil system has been decaying for decades. It is beyond broken. Rusted shut, really.

Let’s stay home while the Wall Street suits board their private jets to chase their new shiny geopolitical gusher. The real money is here in America with the “toll bridges” that are actively pumping oil and moving gas today.

Traffic is what the US energy system does in 2026. We produce. We refine. We export. Oil is cheap but the pipes are still filling up. Whether prices move higher or lower, we want companies that will get paid.

Diamondback Energy (FANG), my “Permian Prince,” is the most efficient operator in the most prolific oil patch on the planet. This is a cash cow hiding in plain sight.

Diamondback doesn’t “explore” in the traditional sense; they basically manufacture oil. They’ve turned the Permian Basin into a factory floor, using “Simul-Frac” technology to frack multiple wells simultaneously like an assembly line. This relentless focus on efficiency has slashed their corporate breakeven to a rock-bottom $37 per barrel.

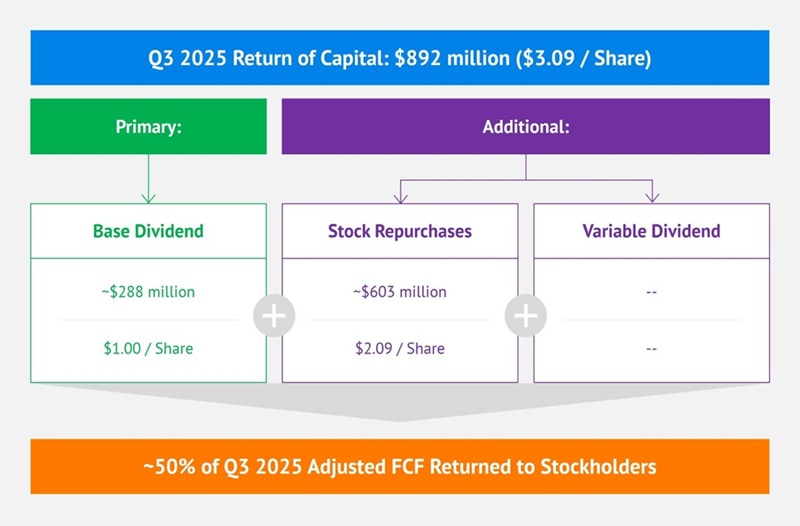

Let me repeat: Diamondback makes money down to $37. Oil can crash from today’s $57, OPEC can argue, the global economy can stumble, but Diamondback still throws off free cash flow. And they’ve committed to piping 50% of that cash back to us through a combination of stock repurchases plus a unique “base + variable” dividend model:

Diamondback’s Shareholder Reward Plan

And Diamondback just acquired Endeavor Energy, quietly making the combined company more efficient and profitable. Endeavor was the largest private explorer in the Permian, with top-tier Midland Basin acreage. By swallowing them, Diamondback “high-graded” its inventory.

Think of it like a puzzle board. Before the merger, Diamondback owned pieces of land next to Endeavor’s pieces. Now, they own the whole board. This allows them to drill longer laterals, extending their horizontal wells from 10,000 feet to 15,000 feet. Longer wells mean more oil for the same surface work.

Management expects $550 million in annual synergies. This cash drops straight to the bottom line—and then into our pockets via dividends and buybacks. Diamondback yields 2.7% but remember, this is only the “base dividend.” When the variable kicks in, this divvie has upside.

And the domestic energy dividends don’t stop at the wellhead. The “toll collector” that moves the gas quietly powering the US economy is Kinder Morgan (KMI). Kinder is a must-have in the AI age, a “pick-and-shovel” play that few investors think of. Every query to a chatbot taps into server racks that draw electricity on the scale of a small city. Which is why AI is evolving from a tech to a power story.

Kinder runs 79,000 miles of pipelines, moving an incredible 40% of the natural gas produced in the US. They get paid whether gas trades for $2 or $10. This energy toll collector threw off $5 billion in distributable cash flow last year, comfortably covering the 4.2% dividend.

And for those yelling: “More yield!” I hear you. Kayne Anderson Energy Infrastructure (KYN) owns the top names in energy logistics, including a large position in Kinder.

The appeal of KYN is that it yields 8.4% and trades at an 11% discount to its net asset value (NAV) It’s a way to buy Kinder & Co. for just 89 cents on the dollar.

Why is this dividend deal available in a supposedly efficient market? KYN is a closed-end fund (CEF), and CEFs trade crazy. Sometimes they fetch premiums to NAV, other times they demand a discount. It depends whether retail investors (the big players in CEFland) are salivating with greed or panicking.

When they freak out, KYN’s price drops, we grab the fund.

And by the way, KYN avoids the K-1 hassle that many of its individual holdings generate come tax time. The fund issues one neat 1099 form, just like a regular stock.

Bottom energy line? Let’s leave the “shiny objects” in Venezuela and instead focus on the cash cows in our own backyard. Go ahead and chase away, Wall Street. We’ll stay home and collect the tolls.

Diamondback and Kinder are current plays in our Hidden Yields portfolio