has returned to our ISA bestseller list as geopolitical tensions spur the gold price to a series of fresh highs.

With President Donald Trump agitating further to take over Greenland and threatening a fresh round of tariffs in the process, the gold price exceeded $4,690 an ounce this morning, a new record. Gold, silver and copper had already hit fresh highs in the last week.

Investors have duly piled into the BlackRock trust, which had sat in 14th place the week before and has almost 40% of its portfolio in the shares of mining companies focused on gold. The fund also has a 19% exposure to copper but a minimal allocation to the silver sector. Jupiter Gold & Silver I GBP Acc sits just outside this week’s table in 11th place.

whose holdings are benefiting from a rise in defence spending and whose shares traded on a premium of around 22% to net asset value on the back of strong demand, dropped down slightly to fourth place.

How to turn £120K Traitors’ prize money into £2.1m

If you walked away with the maximum jackpot from the hit TV show, would you spend, save or invest it? We uncloak some flabbergasting figures and a valuable shield.

20th January 2026

by Nina Kelly from interactive investor

Imagine being driven away victorious from the Traitors’ castle in the Scottish Highlands with the £120,000 prize pot in your hands. No more Missions or dark glamour from the fantastically fringed Claudia Winkleman, and an end to lying and treachery (maybe).

Bar any pressing short-term needs, the winner might splash out on holidays, or perhaps exercise some restraint and save it. How many prizewinners would prove to be a 100% Investing Faithfuls though and put it all into the stock market?

Hard data demonstrates that this is the shrewdest move, as despite the inevitable bad years for shares, history tells us that investing over the long term outstrips inflation and returns on cash savings, meaning greater wealth. Despite the evidence, there are still plenty of Britons holding long-term savings in cash. In the words of Winkleman, “what are they not seeing” about the value of investing?

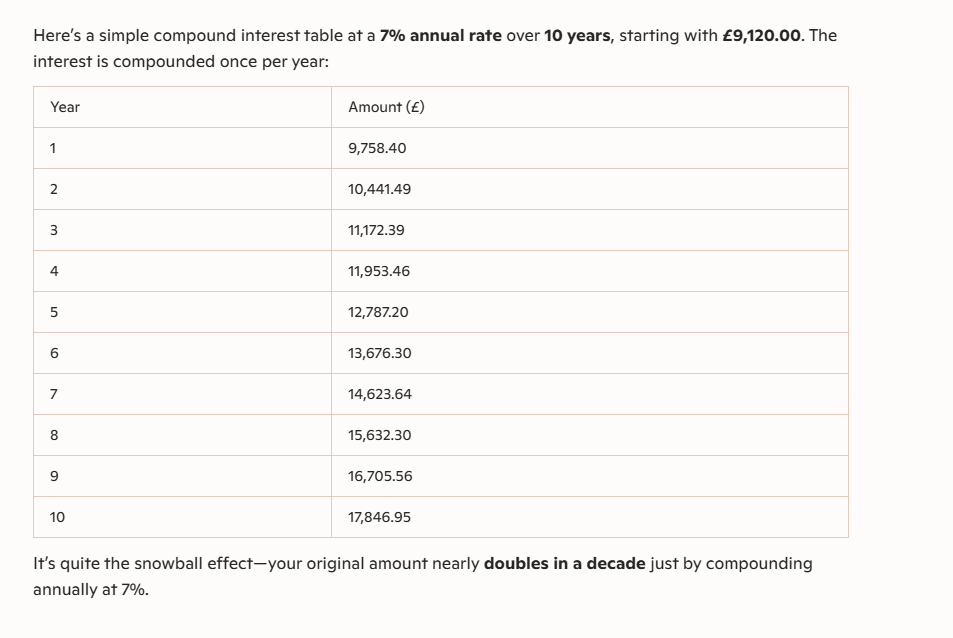

So, while no one can predict what future returns from the stock market will be, our calculations reveal how investing the Traitors’ prize pot of £120,000 over 10 years could see it more than quadruple in size, leaving the winner with more than £500,000.

Let’s gather at the investing round table for some number crunching…

According to consultancy firm McKinsey, the S&P 500 has delivered annualised total returns of a still impressive 9% over 25 years (1996 to 2022), but we’re using BlackRock’s figures to generate potential returns for all assets over the next 10 years. However, it’s worth reminding readers that these are historic returns, and markets may not replicate this boom period for stock markets and many other assets over the next decade.

Why 10 years? Well, investing is very much a long-term game since the stock market is vulnerable to periods of volatility, and leaving your money to compound (where investment returns generate their own returns) for 10 years, means there’s plenty of time for it to grow.

So, according to our calculations, if you invested the £120,000 prize pot in US equities for 10 years, it could potentially grow to more than four times the original sum, hitting £507,147. That’s quite a nest egg for a little delayed gratification.

In comparison, £120,000 kept in cash for the next 10 years would see it grow by only £29,499, reaching a total of £149,499.

Compounding in plain sight

Asset class

Annualised return over 10 years from 2016-2025

Projected potential sum after investing £120,000 for 10 years

US equities

14.50%

£507,147

FTSE 100

8.83%*

£289,240

European equities

8.50%

£279,917

Commodities

7.40%

£250,941

High-yield bonds

5.70%

£211,905

Cash

2.20%

£149,499

Source: BlackRock Asset Return Map. Annual index total returns (income or dividends reinvested) in US dollars. *Total returns data from Morningstar and in GBP. Calculations assume annualised returns remain consistent for the next 10 years. Past performance is not a guide to future performance. Costs have not been taken into consideration.

Keep more of the Traitors’ money with this tax shield

If you opt to keep your £120,000 Traitors’ prize in savings accounts, you’d pay income tax on your interest. If you are a basic-rate taxpayer (paying 20% income tax), you have a personal savings allowance of £1,000, meaning you can earn £1,000 of interest before paying any tax on it. For higher-rate taxpayers (40% income tax), the sum falls to £500. So, if your Traitors’ winnings are in savings accounts, you’re going to lose a big chunk to the taxman. Ouch.

ISAs, whether cash or the stocks & shares version, would keep the taxman’s hands off your windfall, but each adult only has a £20,000 annual allowance, meaning you’d still need an alternative home for a big chunk of your winnings.

However, providing you can manage without the money until your late 50s, you could invest it in a self-invested personal pension (SIPP). Current rules allow you to access a SIPP at 55, rising to 57 in 2028. Investments in a SIPP are sheltered from tax as they grow, just like an ISA. With a SIPP, you have the freedom to choose your own investments, and you can open one alongside a workplace pension.

You can pay the lower of £60,000 or 100% of earnings a year into a pension, but then there’s carry forward rules to potentially take advantage of too. These allow you to utilise any unused pension allowance from the previous three tax years. So, depending on your level of pension contributions over the past few years, you could potentially shovel the remaining £60,000 into your SIPP too. In addition, pension contributions attract upfront tax relief at the individual’s marginal rate, so your winnings would get an additional boost.

If you did put the money into a pension, depending on your age, it’s possible that the money would be invested for much longer than 10 years.

Here’s the projected returns across different assets classes over 20 years:

Asset class

Annualised return over 10 years from 2016-2025

Projected potential sum after investing £120,000 for 20 years

US equities

14.50%

£2,143,318

FTSE 100

8.83%*

£697,168

European equities

8.50%

£652,949

Commodities

7.40%

£524,763

High-yield bonds

5.70%

£374,200

Cash

2.20%

£186,249

Source: BlackRock Asset Return Map. Annual index total returns (income or dividends reinvested) in US dollars. *Total returns data from Morningstar and in GBP. Calculations assume annualised returns remain consistent for the next 20 years. Past performance is not a guide to future performance. Costs have not been taken into consideration.

Banish the cash account?

The point of all this Traitors’ fantasizing has been to illustrate the value of investing over keeping your money in cash savings. However, it’s not about completely banishing cash. Sometimes, keeping money in cash makes sense, for instance as an emergency fund – typically three to six months’ salary – to cover problems such as broken white goods.

While the sum in this piece happens to be £120,000, you don’t need such a large amount – or anything like it – to start investing.

If you’re new to investing or perhaps haven’t started yet, you may fear losing hard-won savings, so-called loss aversion. But there are sources of information to help you:

But, even when global markets fell to their lowest point during the Covid pandemic in March 2020, I didn’t lose all my money (possibly the ultimate fear for those still in cash), and by November, my investment (in a diversified low-cost fund) had recovered.

This year, it’ll be seven years since I started investing. I’m now a dyed-in-the-wool Investing Faithful.

The emotional benefits of dividend re-investment. In fact, with this investment strategy you can actually welcome falling share prices.

There seems to be some perverse human characteristic that likes to make easy things difficult. WB

Warren Buffett just collected another $204 million from Coca-Cola — a reminder that some of the most powerful returns on Wall Street come from patience, dividends, and owning the right business for decades.

Here’s how that payout breaks down, why Coca-Cola keeps funding Berkshire’s war chest, and what this kind of compounding looks like in real dollars.

Coca-Cola has been one of Warren Buffett’s signature bets since the late 1980s, and it’s still paying like clockwork.

Berkshire Hathaway owns 400 million shares, and Coca-Cola’s $0.51 quarterly dividend just delivered a $204 million payout. Sometimes the biggest wins aren’t dramatic. They’re automatic.

Coca-Cola dividends now bring Berkshire over $800 million a year, far beyond the original $1.3 billion cost. Coca-Cola may have its “secret” headlines, but Buffett only cares about one secret: the dividend arriving every quarter.

Why Coca-Cola Still Matters Coca-Cola isn’t just a dividend machine, it’s still a modern profit engine.

With a market cap around $289 billion and gross margins above 61%, the company keeps doing what it does best: defend pricing power, stay everywhere, and find small ways to sell more. Mini cans. Convenience-store pushes. Product tweaks that look boring up close, but scale fast when you’re global.

That durability is why some Wall Street analysts still see upside, with price targets reaching $80. This implies that Coca-Cola is still being priced as a cash machine with staying power. And for Berkshire, that’s the whole point. No hype. No chasing trends. Just owning a durable cash machine, year after year, and letting dividends and compounding do the heavy lifting.

This is where most investors get caught. They chase the hot stock, the pop, the quick win, and end up trading emotions instead of building wealth.

Buffett plays a different game. He doesn’t need to react to every headline. He owns businesses that pay him, then lets time and dividends do the work.

The difference isn’t access to information. It’s behavior, and the traders who last tend to rely on rules, not emotion, like stop-loss and take-profit orders

Why This Dividend Story Matters That $204 million payout is more than a headline number. It’s what long-term investing looks like when the business is durable and the cash flow is real.

While plenty of investors chase the next spike, Buffett’s Coca-Cola stake shows the quieter path: own a high-quality company, let the dividend stack up, and give compounding time to do its job. You don’t need to love soda to take the point, you just need to respect what consistent payouts can build over decades.

The current first quarter income estimate is £3,435.00.

The Snowball gathered some dividends at the end of last year, hoping for a Santa Rally and was lucky not only with the earned dividends but also with some capital gains.

Do not scale to reach a year end figure but it’s a solid foundation for this years target of £10k.

I have been exploring for a bit for any high quality articles or blog posts on this sort of space . Exploring in Yahoo I at last stumbled upon this site. Reading this information So i am happy to convey that I have an incredibly excellent uncanny feeling I found out just what I needed. I so much undoubtedly will make sure to don’t put out of your mind this site and provides it a glance regularly.

For any new readers, below is the plan for The Snowball and the end destination. A plan without an end destination is a very poor plan.

That should provide an ‘annuity’ of around 17% with no additional cash added to the seed capital and guess what you keep all your capital.

Better if you can add to the seed capital but if you can’t remember with compound interest you should make more in the last few years than you do in all the early years.

Antero Midstream, VICI Properties, and Enbridge each yield over 5% and offer a realistic path to 10–12% annual returns.

AM has transformed from a yield trap to a high-quality midstream with robust free cash flow, a 5.1% yield, and significant buyback potential.

VICI’s unique Las Vegas Strip assets, 6.4% yield, and AFFO growth support a safe, double-digit total return, trading below historical valuation multiples.

ENB’s diversified, regulated network, 6% yield, and 5% annual growth target position it as an ETF-like, defensive income compounder for retirees.

Looking for more investing ideas like this one? Get them exclusively at iREIT®+HOYA Capital.

TAKAYUKI UEDA/iStock via Getty Images

Introduction

A big part of why I love my job so much, besides that I don’t have to sit in a corporate office from 9 to 5, is that I get to share my views with tens of thousands of people every day. It’s like I’m running my own mini newspaper.

That’s a problem for those who seek a high yield right now instead of a decade or two from now.

So obviously, I know that the S&P 500 tends to outperform most high-yield ETFs. That’s why I always advise people to start as early as possible. If you do it right and spend decades compounding, maybe you can even cover all expenses with the elevated yield on cost from past S&P 500 investments. That’s the goal, as it means you have both a huge portfolio and elevated income.

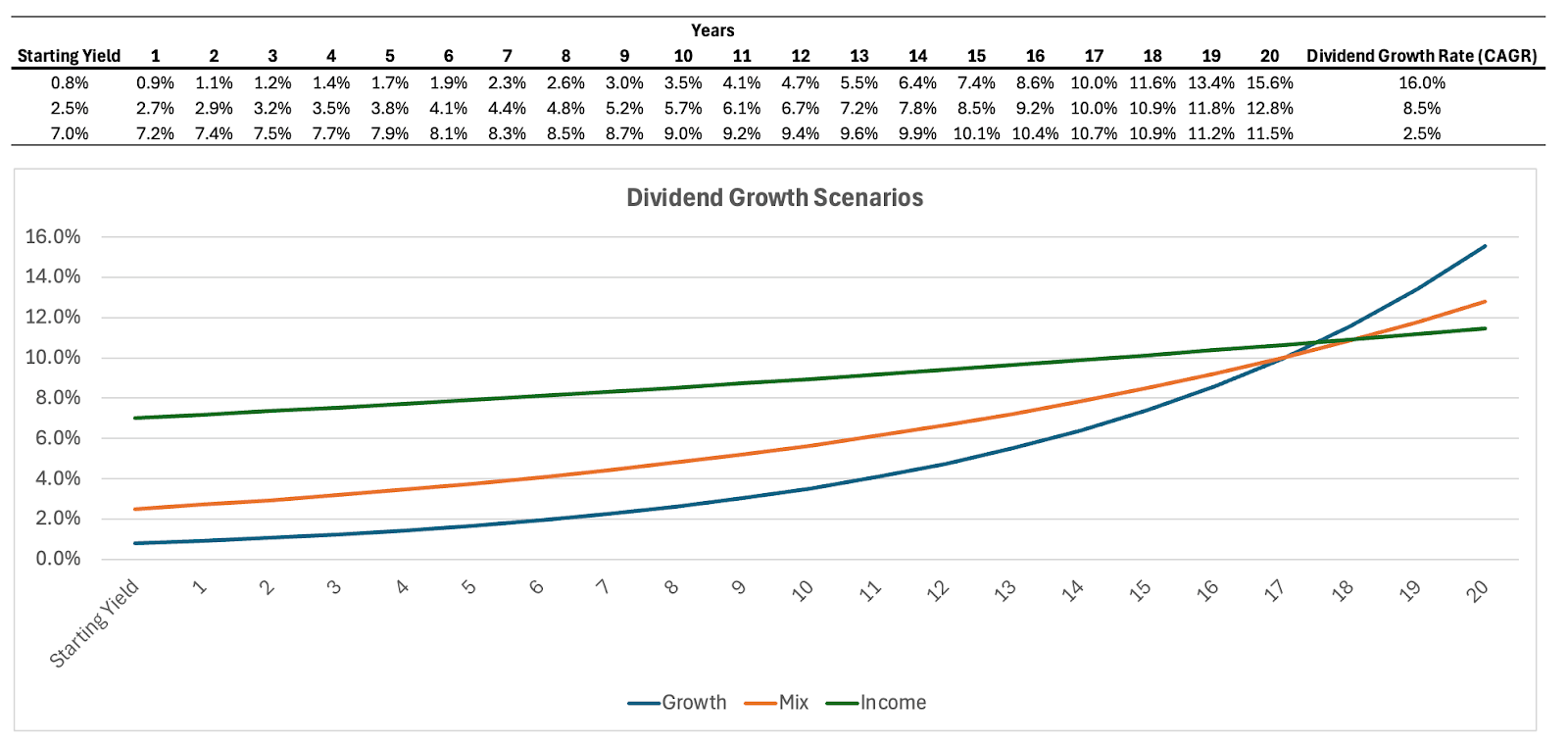

The table below is one of the best examples of that. It shows that a company with a 0.8% yield and 16.0% annual growth ends up providing the same yield on cost as a stock with a 7.0% starting yield and 2.5% annual growth after roughly 16-17 years.

Leo Nelissen

If we assume that a fictional company that grows its dividend by 16.0% per year will also see similar capital gains, that’s the kind of stock that’s perfect for retirement. But then again:

Finding a company that grows by 16% per year is tough.

Some people need to retire earlier.

That’s why I went on the “hunt” for some middle ground.

I spent the past few days going through the many lists of stocks to find companies that deliver both growth and income. These are companies with yields of more than 5.0% and a realistic path to >10.0% annual returns.

These companies have the best of both worlds. While they may not have the growth rates that some tech stocks have, they have enough growth to provide a path to double-digit annual returns. Over time, this can help us build income and a higher net worth much faster.

While I still don’t recommend people my age (30) or anywhere close to that to build a portfolio with an average yield of >5.0%, these kinds of companies are great to buy when already retired or when adding income a decade or two before retirement.

After all, $100,000 compounded at 10.0% for 10 years turns into slightly more than $250,000.

It’s just math, but if I’m right about these companies (I’m sure I am), there’s a lot of value for a wide range of investors. So much so that if I were closer to retirement, I would own all of them.

Now, let’s start with the one I already own.

Antero Midstream (AM) – Why I Bought a Former Yield Trap

Antero Midstream is one of the few high-yield stocks I own. That’s exactly because of the reason I just discussed in the introduction, which is to own an asset I truly never expect to sell because it already has such a favorable income/growth balance.

With that said, Antero Midstream is a C-Corp midstream company. In other words, it doesn’t issue K-1 forms, which some readers hate (some really like these). For me, as a non-American investor, these C-Corps make way more sense, as dealing with Master Limited Partnerships is truly challenging from a tax point of view.

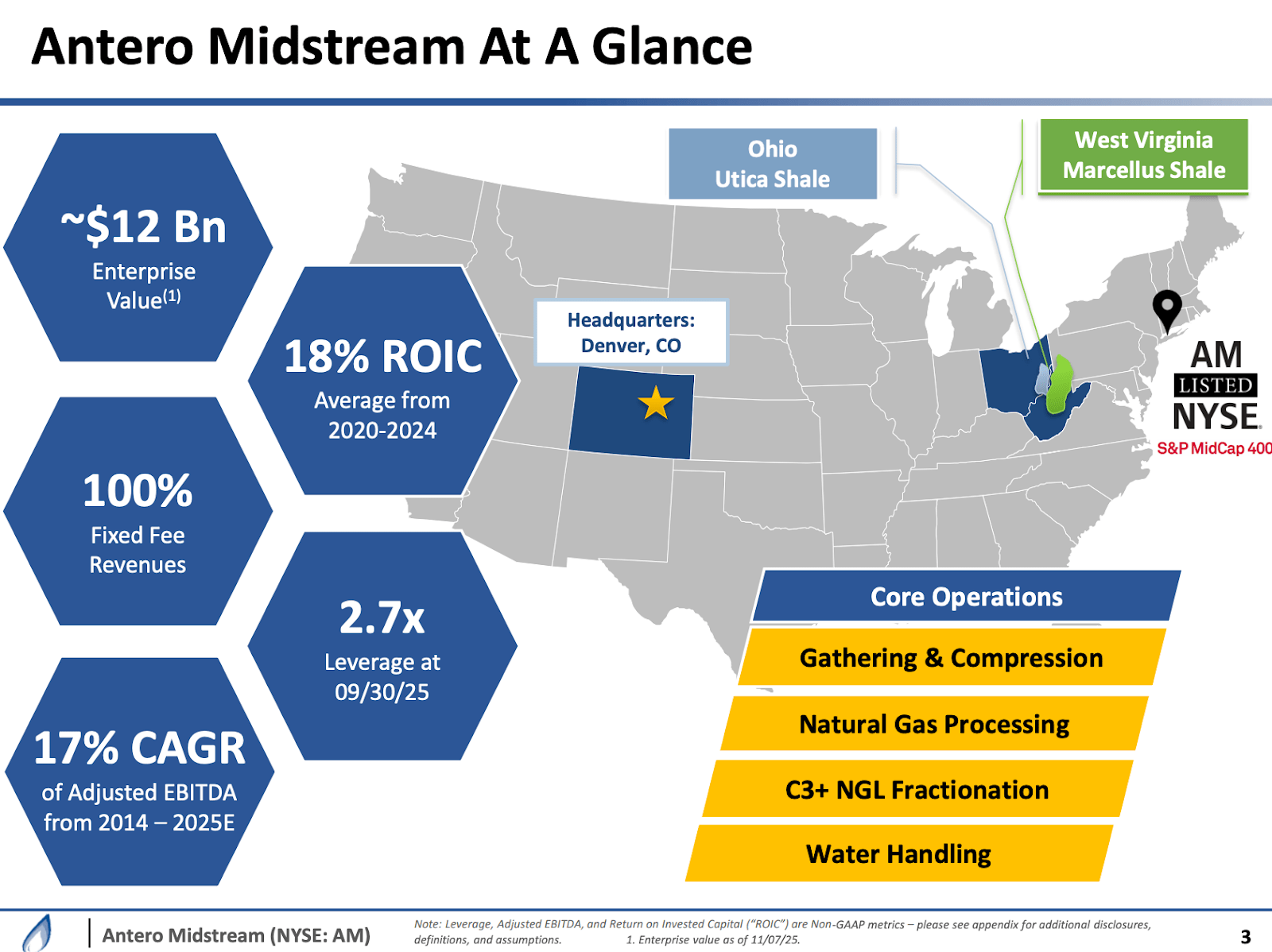

Anyway, Antero Midstream is a midstream company, which puts it in the same industry as ONEOK (OKE) and Kinder Morgan (KMI), with the major difference being size. Antero Midstream has a market cap of $8.5 billion. These other two have market caps bigger than $45 billion. They also have networks that span big parts of the U.S. and multiple oil and gas basins. Antero Midstream doesn’t have any of that.

Antero Midstream was spun off from Antero Resources (AR), which is one of my favorite natural gas producers. Basically, Antero Midstream owns the gathering and processing assets of Antero Resources. It also owns water assets and some pipelines.

Antero Midstream

All of these assets are in Appalachia, which is home to the Ohio Utica Shale and the Marcellus Shale. These are two of the best places to produce natural gas due to very abundant reserves and often low breakeven prices. Another benefit is that these are close to areas with dense populations, including the Northeast, the Midwest, and the strategic LNG corridor to the Gulf Coast. That last area may not be densely populated, but it comes with high natural gas demand due to data center construction and LNG exports.

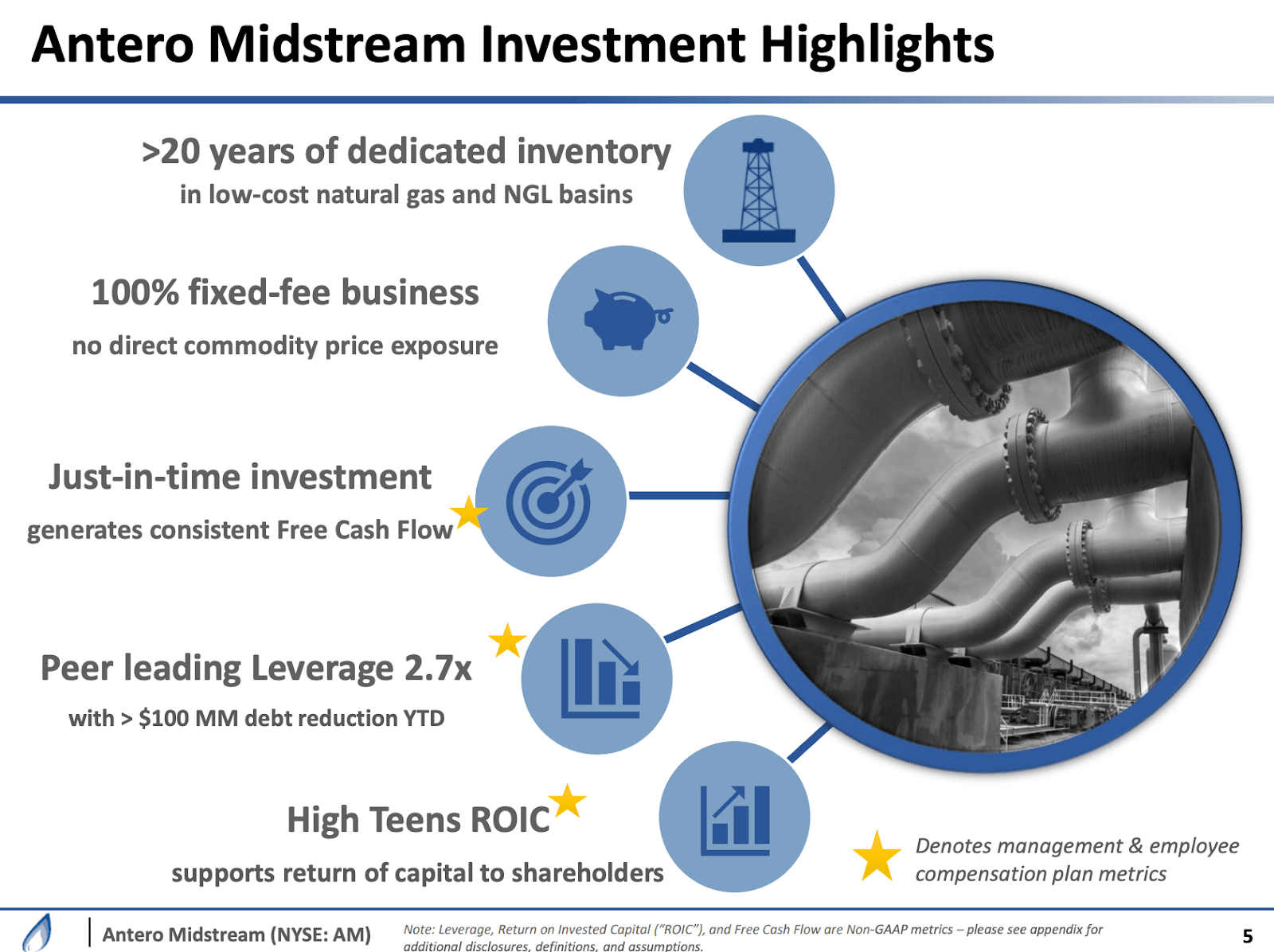

Because of its relationship with Antero Resources, the company enjoys deep reserves, has a 100% fixed-fee business with a player that is extremely predictable (it helps when midstream and upstream are related through business ties), and a “high-teens” return on invested capital. That last fact is also caused by its relationship with AR, as AM can plan ahead and knows exactly when new assets are needed. It does not have to worry about future utilization rates of its growth projects.

Antero Midstream

Moreover, in 2021, AM cut its dividend. Since then, that dividend has not been hiked. That’s the bad news and a reason why many avoid Antero Midstream. To some extent, I get that. However, when diving deeper, we see that there’s a good reason to like it. That reason is free cash flow generation.

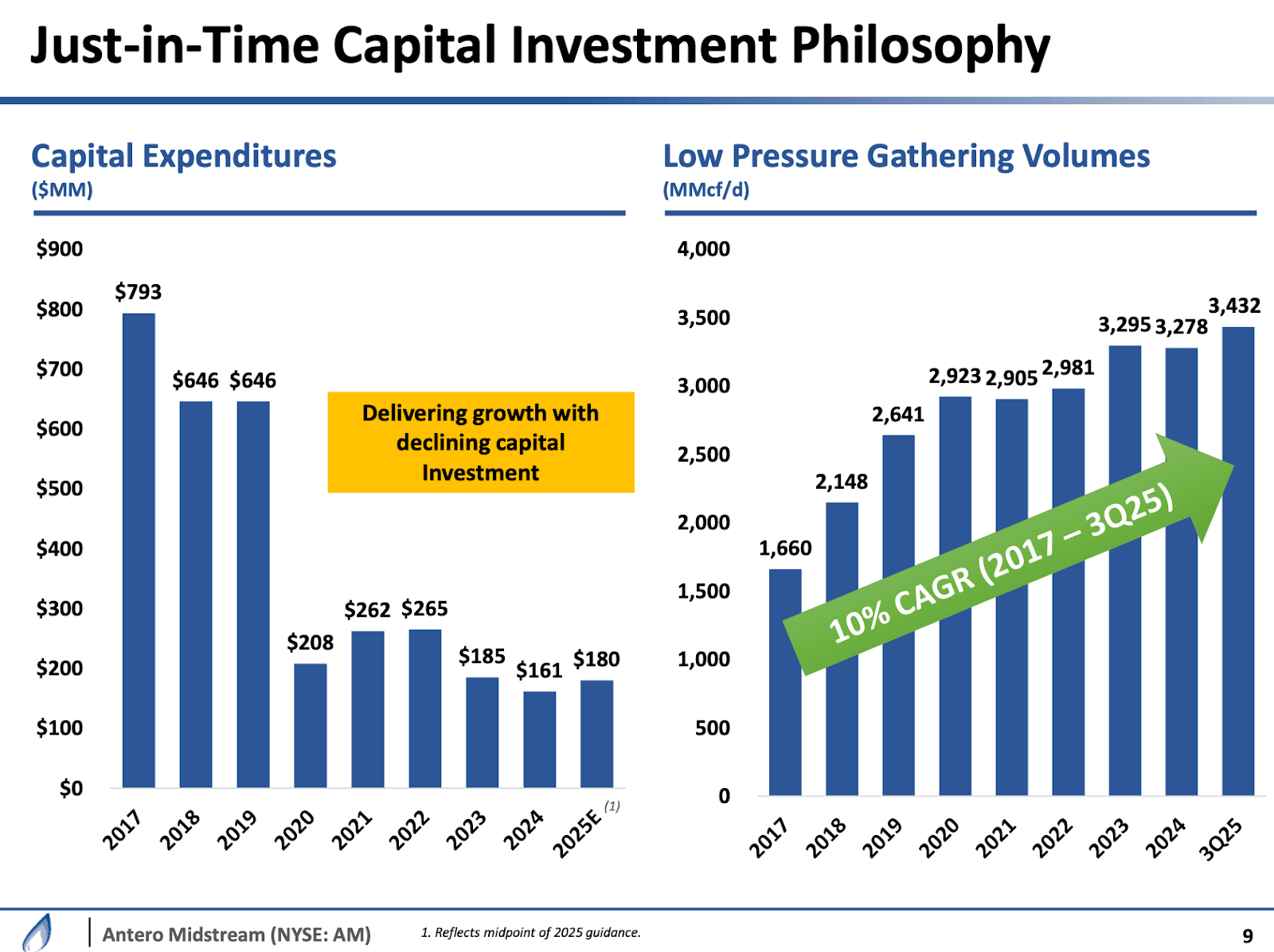

After a few years of aggressive asset investments, the company is now running much lower CapEx programs, as we can see below. In 2025, total CapEx is expected to be just $180 million. That’s way less than the $646 million needed in 2018 and 2019. Even better, because of these assets, the company was able to grow volumes by 10% per year between 2017 and 3Q25.

Antero Midstream

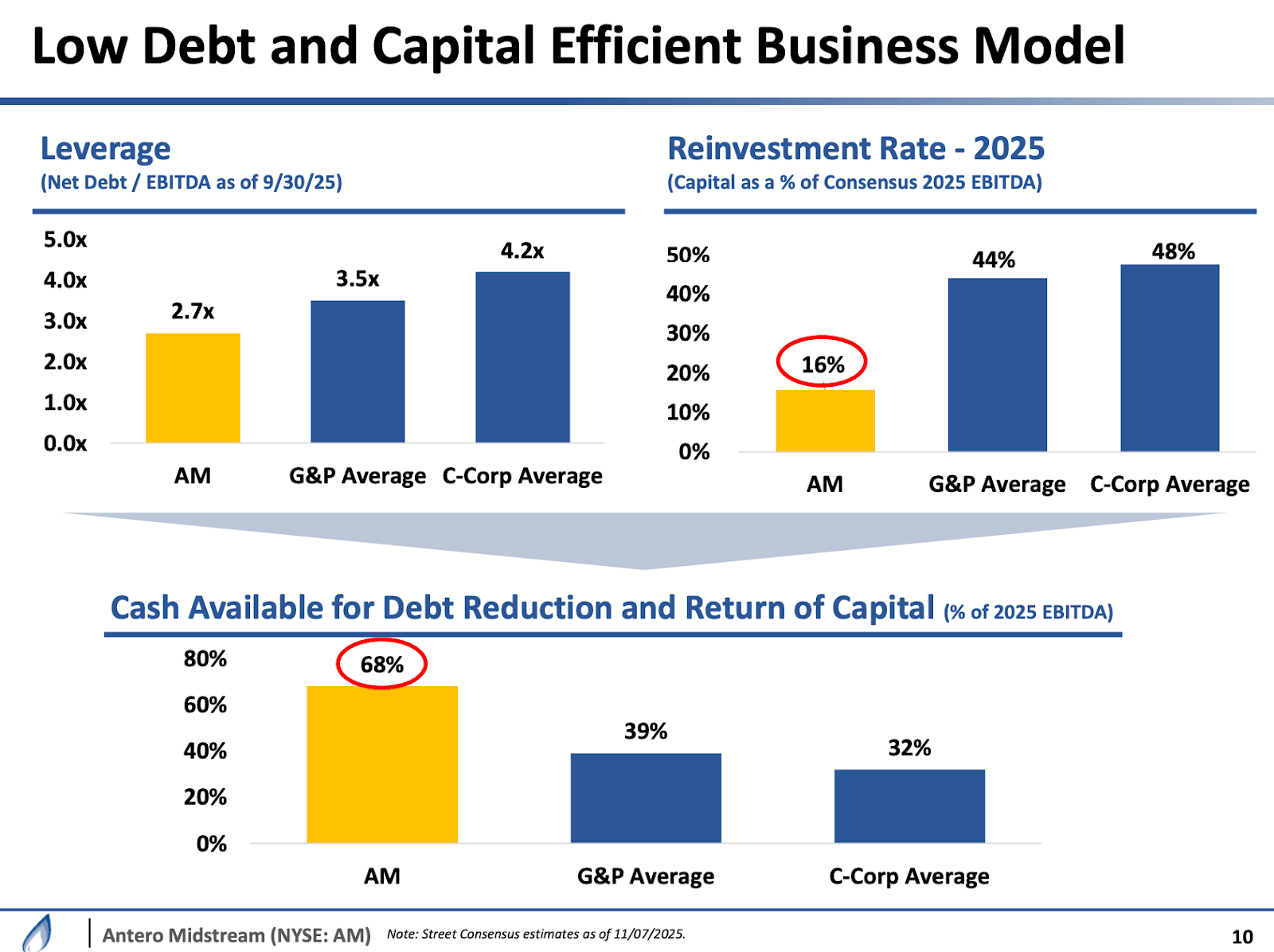

Because of this, the company is a leader when it comes to balance sheet health (it reduced debt quite aggressively in recent years), reinvestment rates, and cash availability for debt reduction, dividends, and buybacks.

Antero Midstream

This mix is very bullish for the company.

To give you an idea of what we’re dealing with here, analysts expect more than $870 million in free cash flow by 2027. That’s more than 10.0% of its current market cap. This is a big deal as AM yields 5.1%. It implies a payout ratio of just 50%, one of the best numbers in the entire industry.

Essentially, at this rate, the company can buy back 5% of its shares on top of paying a 5% dividend. Technically speaking, this alone implies a 10% annual return from 5% income and 5% that improves per-share earnings without any revenue growth.

Over time, these benefits get stronger for dividend investors, as share buybacks reduce the number of shares that are entitled to dividends. That way, the company is paving the way for higher future dividend growth by buying back stock instead of hiking its dividend right now.

I like that a lot.

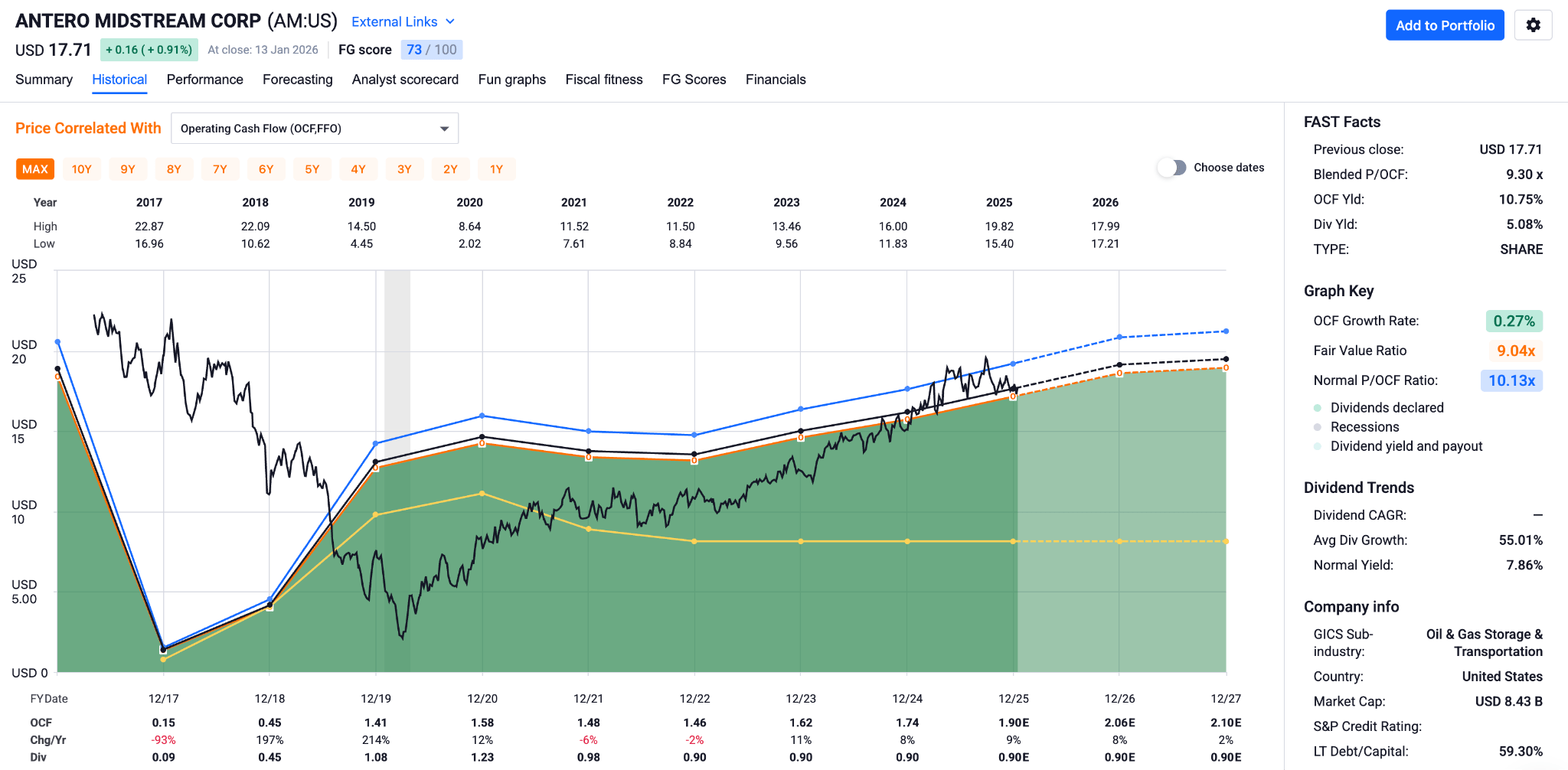

Even better, analysts expect per-share operating cash flow growth of 9% in 2025 to be followed by 8% and 2% growth in 2026 and 2027, respectively.

FAST Graphs

Moreover, as I do not believe that a 9.3x operating cash flow multiple will post a headwind, I think this company is in a good spot to return 12-15% per year, making it one of my favorite high-yield stocks.

I think it has gone from a 2021 yield trap to one of the highest-quality midstream companies on the market with a lot of room to run, thanks to secular growth in natural gas.

VICI Properties (VICI) – Income, Moderate Growth, and a Thick Layer of Safety

I know what you’re thinking right now. And you’re not wrong. VICI is indeed one of these stocks that every analyst seems to like. On Seeking Alpha, the stock has 7 Strong Buy ratings, 8 Buy ratings, 1 Hold rating, and zero Sell ratings. This reflects Wall Street, which also has no Sell ratings.

VICI Properties is one of these companies that has become a bit of a controversial stock. That’s not because management is doing something controversial (it’s not), but because some people believe it’s a yield trap, while others believe it’s an opportunity of the decade, or something along those lines.

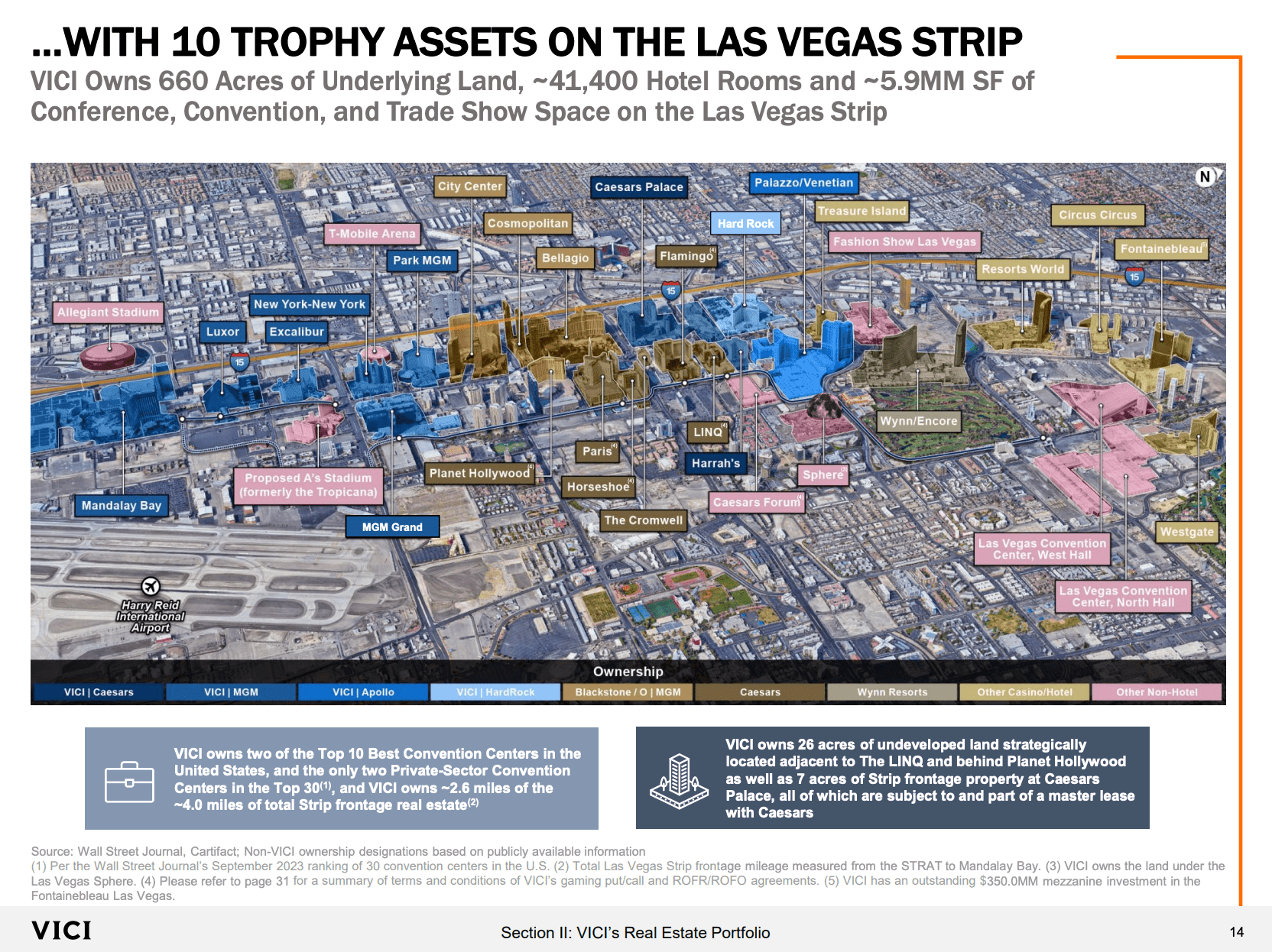

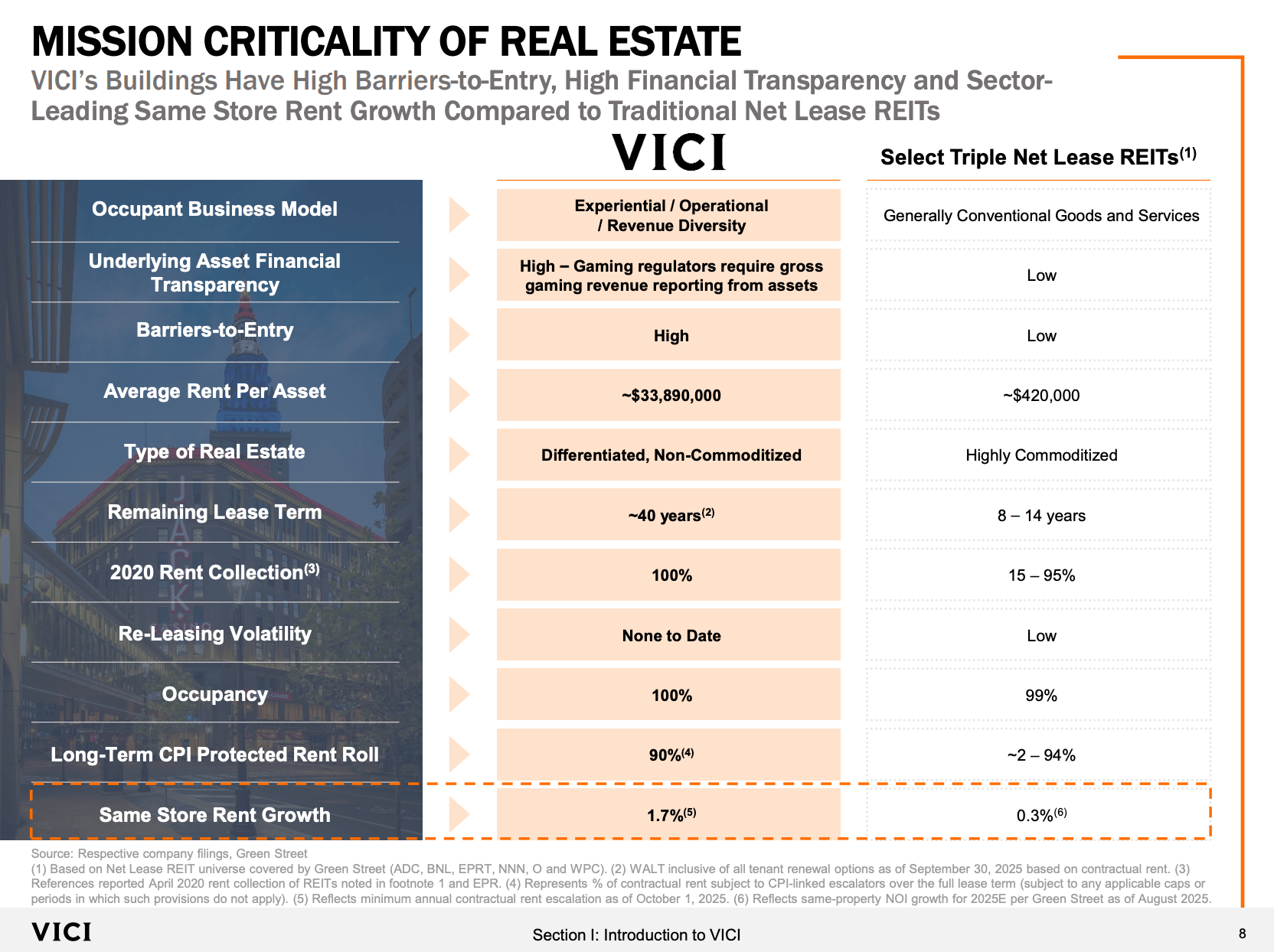

As most of you may know by now, VICI is a net lease REIT like Realty Income (O), as its tenants pay for insurance, maintenance, and taxes. However, that’s where the similarities end, as VICI may be the only REIT (I think it’s the only one) with differentiated assets that cannot simply be replicated. That’s because it generates roughly half of its rent on the Las Vegas Strip, where it owns some of the most iconic casino-focused assets like the MGM Grand, Caesars Palace, Mandalay Bay, Park MGM, and others.

VICI Properties

Most of these deals have multi-decade durations and are protected by master leases. In other words, tenants cannot just default on one rent. It would mean they lose the right to all buildings. Besides that, because these buildings are so unique and critical to their success, not paying rent will be the last thing on their minds when financial headwinds hit.

VICI Properties

One of the reasons why VICI is unloved by some is the trouble that the City of Las Vegas is dealing with. This includes unfavorable visitor numbers due to affordability issues. From what I have learned in recent years, Las Vegas resorts have increasingly focused on margins. While it initially was a town where food and hotel rooms were affordable to get people to spend money on gambling and entertainment, has become a city where the entire “experience” has become much more expensive.

The good news is that VICI is a landlord. It does not make money from slots. That’s why it even raised its guidance in 3Q25 after growing its adjusted funds from operations (“AFFO”) by 5.3%.

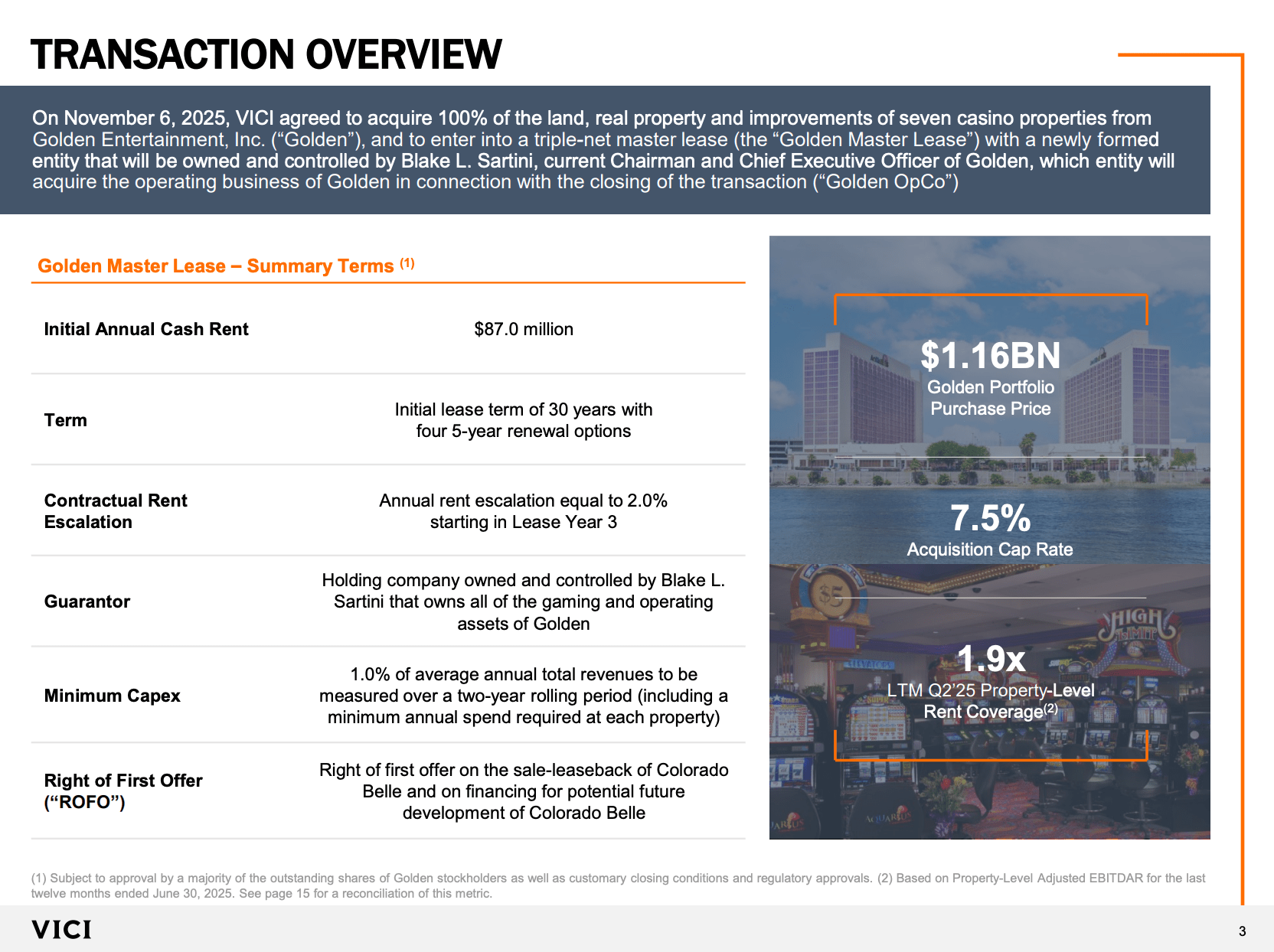

Moreover, the company is diversifying and adding growth through deals like the one with Golden Entertainment. That’s the company that owns the Las Vegas STRAT (the big tower) and a wide range of smaller assets. At the end of last year, VICI bought 100% of the land, real property, and improvements on seven casinos, as we can see below.

VICI Properties

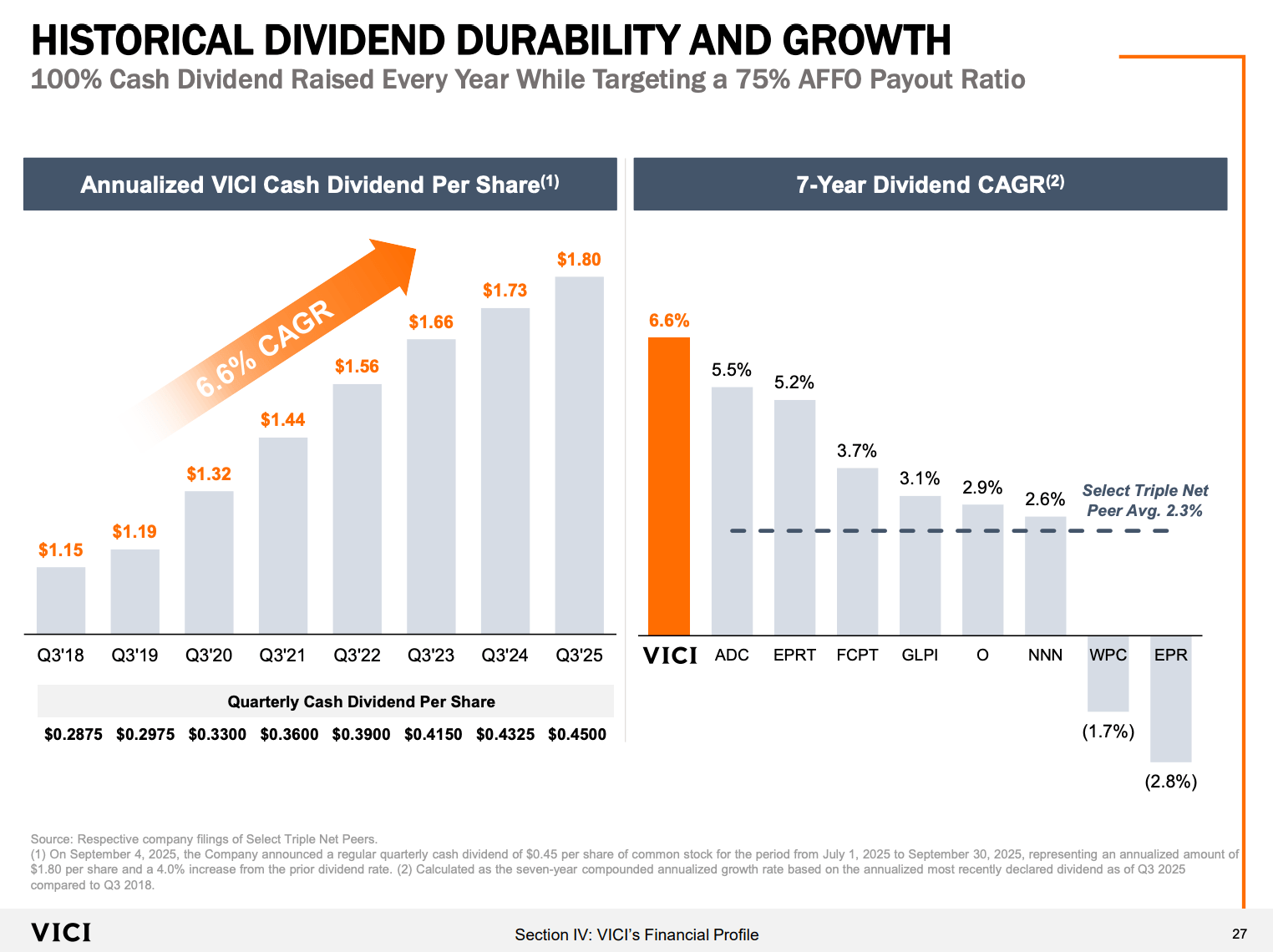

This strategy isn’t a high-growth strategy, but it’s a strategy that works. Currently, VICI yields 6.4%. This dividend comes with a 75% payout ratio and has been hiked by 6.6% per year since 3Q18.

VICI Properties

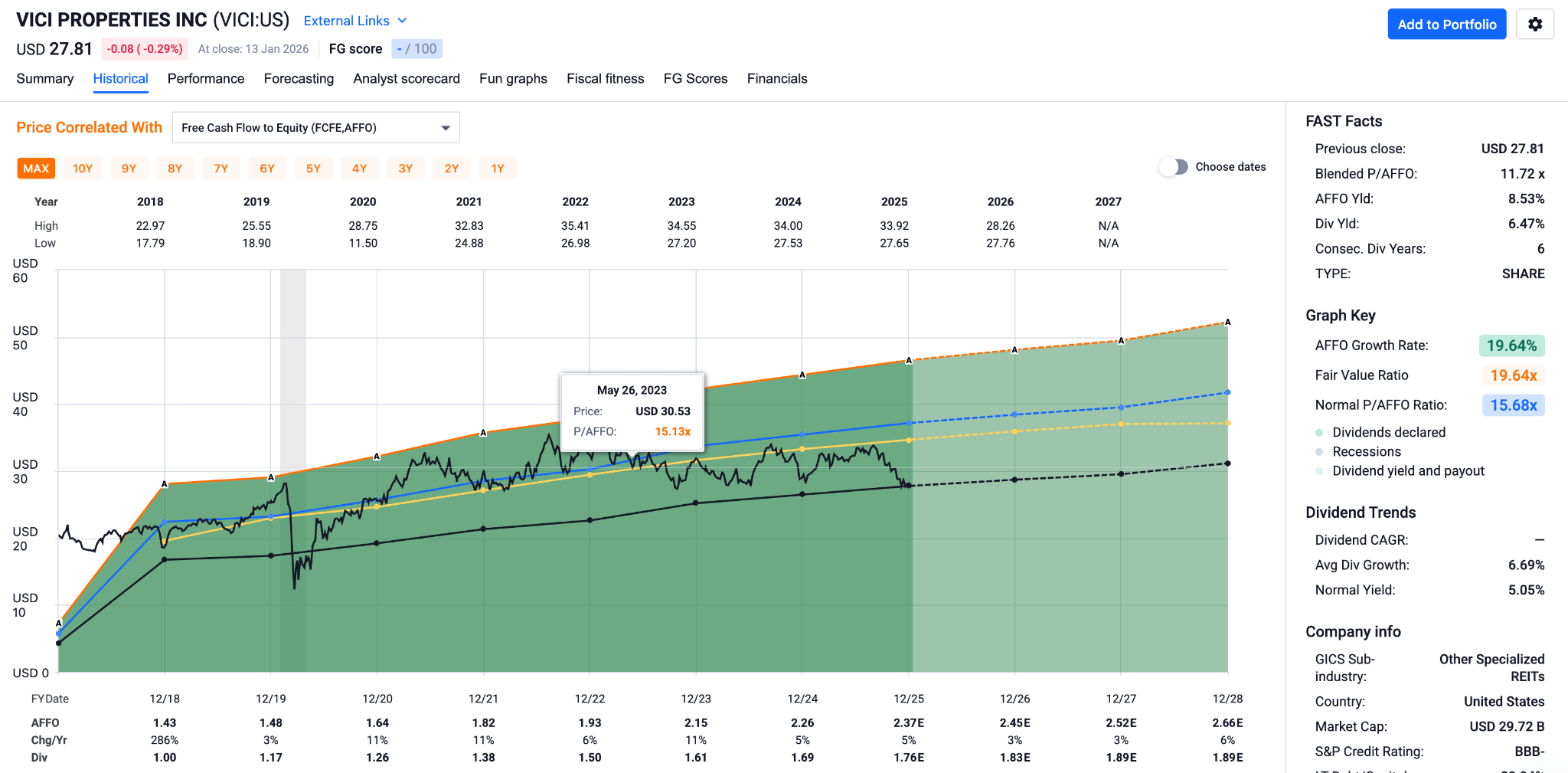

Going forward, that dividend growth rate may come down a bit, as analysts expect 3% per-share AFFO in both 2025 and 2026. In 2027, we could see a rebound to 6%. Generally speaking, it seems to me that the mix of annual rent escalators of 1.7% (including CPI escalators) and deals for external growth provides roughly 3-5% long-term growth.

FAST Graphs

Hence, VICI, which also has an investment-grade credit rating of BBB-, is expected to return 10% to 11% per year based on its dividend and per-share AFFO growth alone. Given VICI’s predictable business model and stable income, that component of the total return is relatively safe, I would say.

The other factor, valuation, is obviously more volatile. However, as VICI trades at just 11.7x AFFO, a mile below its long-term average of 15.7x, I believe this is more of a tailwind than a headwind in the years ahead, meaning the odds of a higher-than-expected total return seem to be better than the odds of seeing a lower total return.

That’s why I like VICI, as the risk/reward of this landlord is so good right now.

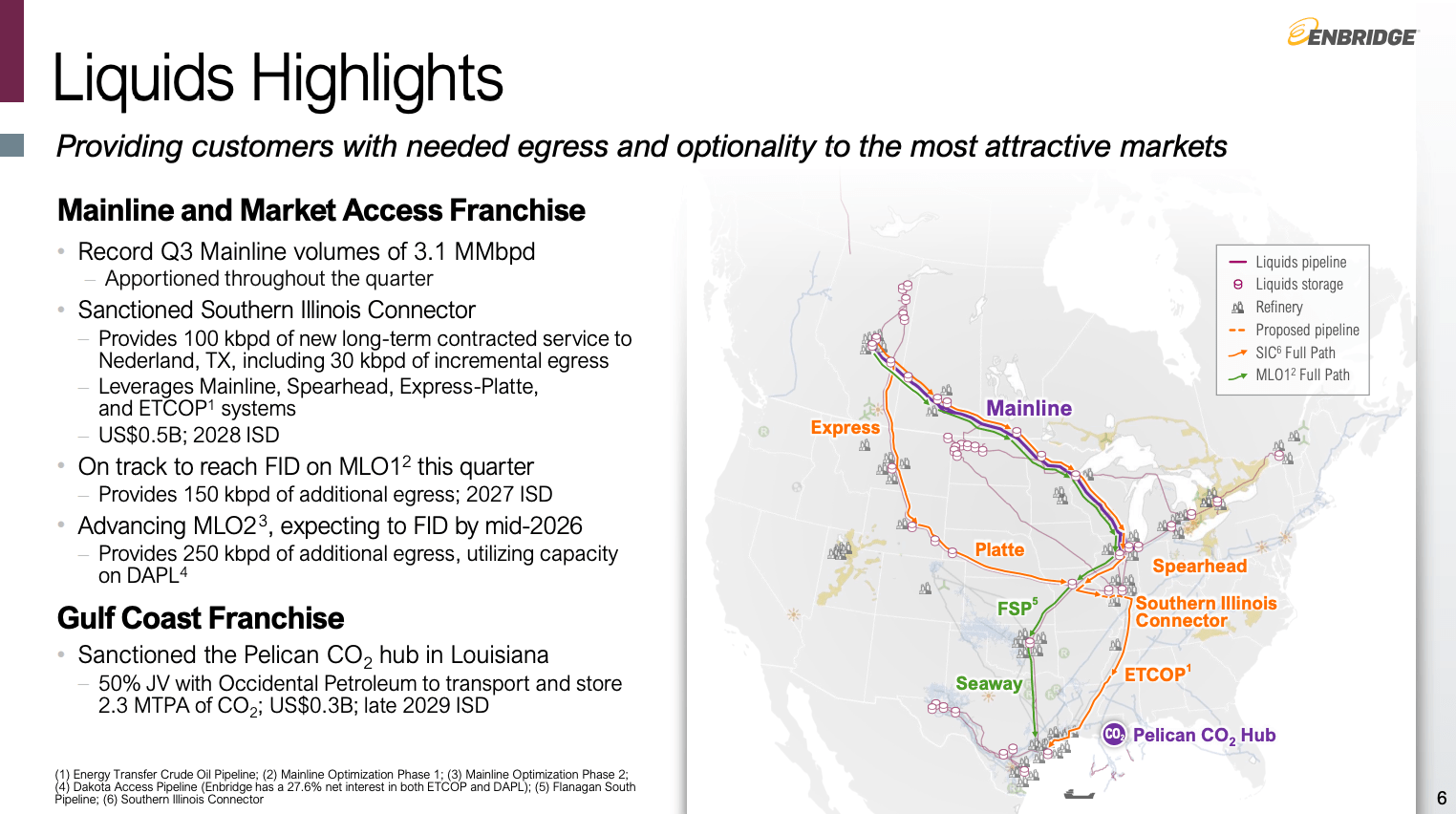

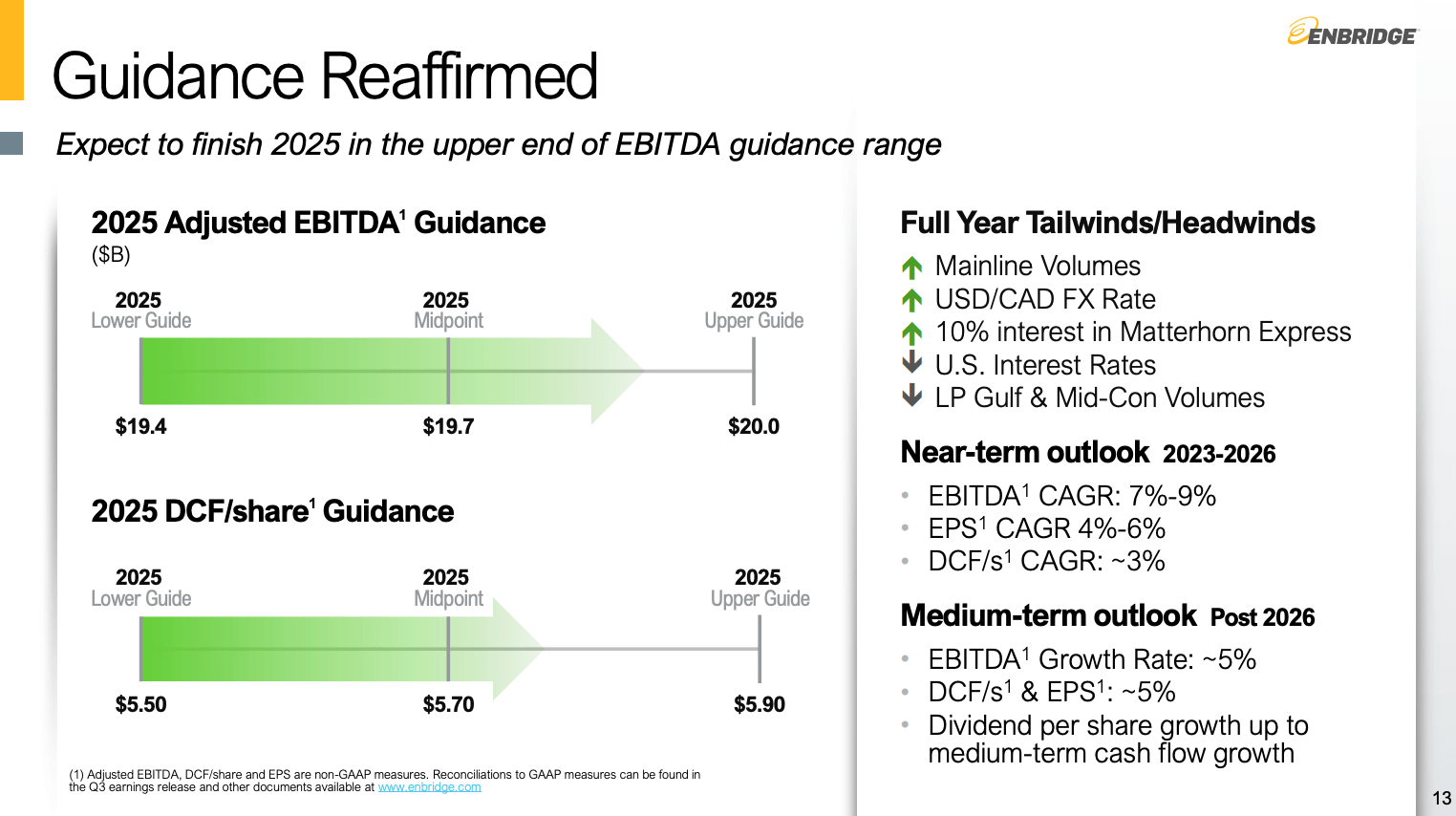

I have to admit that it wasn’t my intention to include two midstream stocks in this article, as hard as that may be to believe for some. However, Enbridge deserves a spot, which is why I kicked out my initial idea for this article.

For starters, Enbridge is also a C-Corp, which means it doesn’t issue K-1 forms. It’s also the largest midstream company in North America with a market cap of $100 billion.

It currently yields 6.0%.

This dividend is protected by a massive infrastructure network, including liquids, gas transmission, storage, and renewable power. Its liquids network, for example, connects major producing areas like the Western Canadian Sedimentary Basin, the Texas Permian, and high-demand areas like the U.S. Gulf Coast.

Enbridge

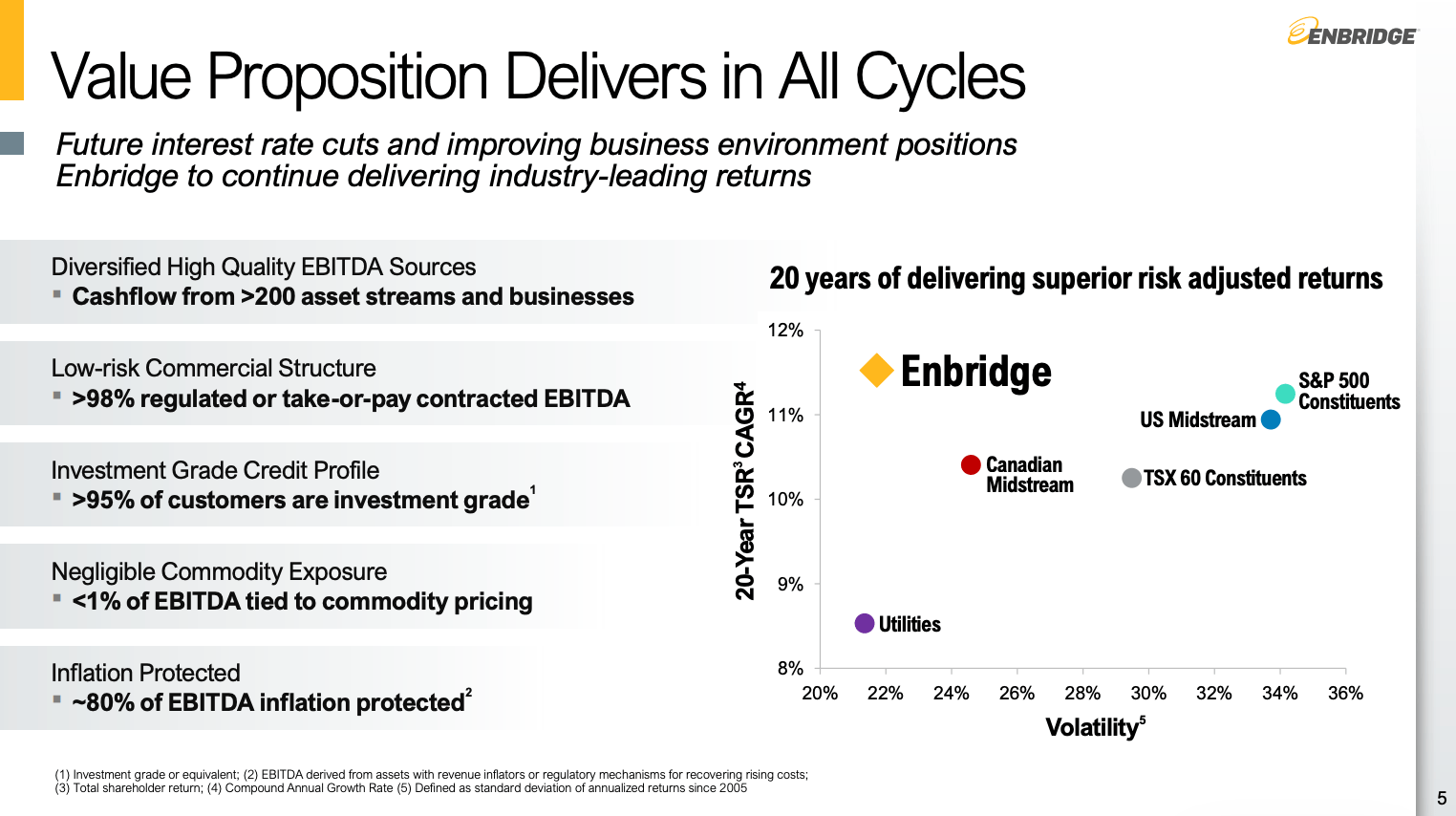

As of 3Q25, it generated roughly 53% of its adjusted EBITDA from liquids. Gas transmission and midstream accounted for 30%. Gas distribution and storage added close to C$600 million in EBITDA (13%). The size and diversification make this company an ETF-like midstream player that enjoys safety from a 98% regulated take-or-pay contract, a customer base that almost entirely consists of companies with investment-grade balance sheets, 80% inflation-protected EBITDA, and less than 1% direct exposure to commodity prices.

Enbridge

On top of safety, Enbridge enjoys strong secular growth from its “essential” operations due to booming data center power demand. These assets are often looking to go behind the meter to get data centers up and running much faster and avoid strains on the local grid. That is bullish for midstream companies.

This is one of the reasons why it sees roughly 5% annual EBITDA growth per year after 2026. It expects the same growth rate for its distributable cash flow, its EPS, and its dividend per share. That’s a good deal, as this company yields 6%.

Enbridge

The 6.0% yield and 5.0% growth target alone pave the way for 11.0% annual returns. This excludes acquisitions, major growth projects, and any valuation tailwinds.

Moreover, from a personal point of view, buying Enbridge would make a lot of sense for me once I’m retired. Assuming I’m still in Albania when I retire, I would pay a tax of just 15% on Canadian dividends. That would make ENB a no-brainer for me, especially given its diversification. While I won’t do it, I wouldn’t lose sleep if I had all of my capital in ENB. That’s how I know it’s a company I trust.

Takeaway

To me, the ultimate retirement combo is a mix of stocks that pay big now and can grow.

In this article, I discussed three of them that all yield more than 5.0% and have a clear path to an annual return of 10% to 12% without having to incorporate any wild growth fantasies.

These companies provide income now and a shot at growing your capital for many years, if not decades, to come.

I’m not retired, and I have no plans to retire anytime soon, but knowing that I could buy these, retire, and grow my wealth over time makes me feel a lot safer about my future.

Risks to My Thesis

There are two main risks here. On top of general operational risks, I believe a steep spike in interest rates could pressure both REITs and midstream companies due to the negative impact this has on their cost of capital. It would also give investors a higher risk-free rate, which means they may be less tempted to invest in dividend stocks.

Moreover, although both AM and ENB have almost zero exposure to direct commodity prices, an environment where commodity prices like oil and gas are so subdued that producers cut output could have a negative impact on growth expectations.