Investment Trust Dividends

In January 2026, there are 73 stocks in the FTSE 250 that pay a dividend yield of 4% or more. Zaven Boyrazian investigates one that pays 7.4%!

Posted by Zaven Boyrazian, CFA

Published 18 January

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Typically, UK shares across the FTSE have offered dividend yields that sit close to 4%. However, after a stellar 2025, higher stock prices have dragged down the yields of the UK’s flagship indexes. The FTSE 100 now only offers a payout of around 2.9%, while the FTSE 250 is closer to 3.3%.

The good news for stock pickers is that there are still plenty of higher-yielding opportunities to explore.

So, with that in mind, let’s break down how investors with £5,000 to invest today can aim to unlock a 7.4% yield in 2026.

Right now, there are over 70 stocks in the FTSE 250 with a yield larger than 4%. And among these stands Supermarket Income REIT (LSE:SUPR) with its 7.35% — almost exactly in line with our target of 7.4%.

So, should investors just snap up £5,000 worth of Supermarket shares and call it a day? Sadly, it’s not that simple.

Experienced investors already know that higher payouts almost always come with higher risks. Don’t forget, unlike the interest paid on bonds, dividends are completely optional for a company. Yet, there are always some exceptions. And sometimes the risk ends up being worth taking.

So, is that the case with Supermarket Income REIT?

As a quick introduction, this company owns and manages a real estate portfolio of supermarket properties across the UK and France.

Given that supermarkets tend to see continuous footfall even during economic downturns and leases on supermarkets often span decades, the company has established a pretty reliable source of cash flow. What’s more, with around 77% of its rent inflation-linked, rent organically grows over time without needing to wait for leases to expire before prices are adjusted.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

This continuous and predictable stream of income is actually how management has been able to raise shareholder payouts for seven years in a row so far, boosting the yield in the process.

But this is where things get a bit tricky. While interest rates have started falling, they’re nonetheless still significantly higher compared to a few years ago. Consequently, looking at its latest results, earnings actually fell short of dividends. In other words, the company paid out more to shareholders than it brought in.

The issue isn’t a result of a lack of occupancy or tenants not paying their rent on time. In fact, impressively, the company has maintained 100% occupancy and 100% rent collection since its IPO in 2017. Instead, the problem is debt.

Expanding a real estate portfolio isn’t cheap. And just recently, the group has borrowed yet another £250m through a bond offering at a 5.125% interest rate.

This move provides some welcome near-term capital flexibility. But it further ramps up the pressure on earnings, and in turn dividends – this is the risk income investors face.

With interest rate cuts taking their time and leverage on the rise, the sustainability of Supermarket Income REIT’s dividend is looking a bit wobbly. But as interest rates continue to fall, the group’s debt burden could prove far less troublesome over time, allowing dividends to keep growing.

Personally, the risk profile is a bit too high for my tastes. But luckily, there are still plenty of other high-yield dividend stocks to choose from when hunting for a 7.4% payout.

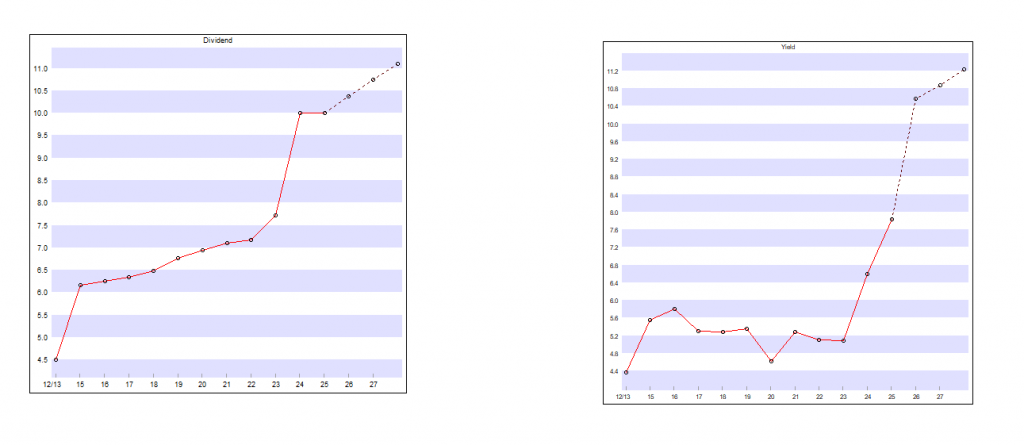

Current Dividend 6.18p

Fcast EPS 6.05p

While its recent rally has made the FTSE 100’s yield less appealing, it is still possible to obtain a highly attractive income from a basket of UK large-cap shares, argues analyst Robert Stephens. Here’s how.

14th January 2026

by Robert Stephens from interactive investor

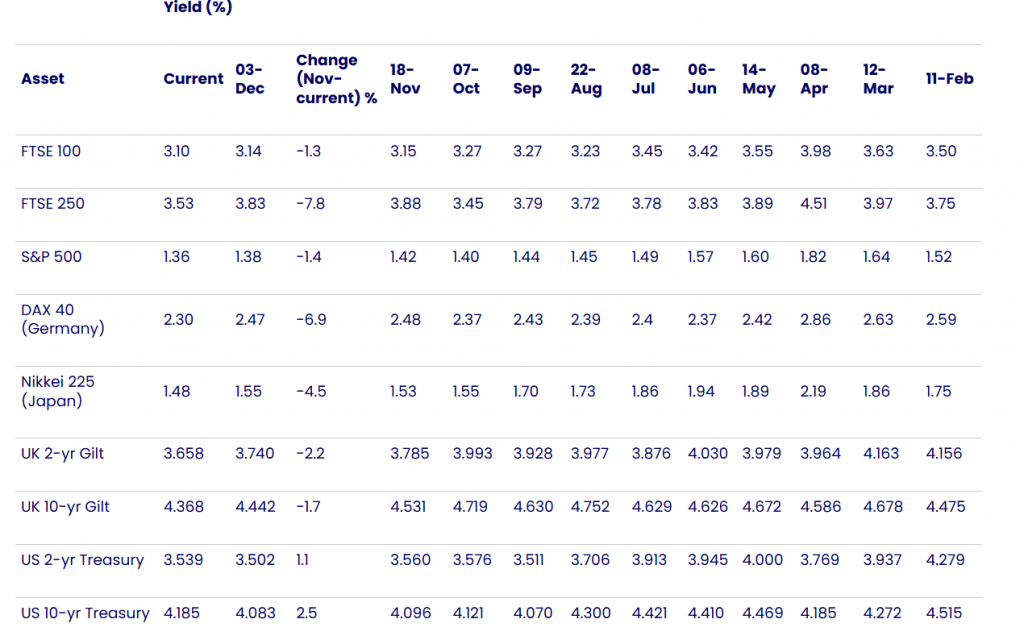

The FTSE 100’s recent surge to 10,000 points has inevitably squeezed its dividend yield. The index’s income return now stands at a rather humdrum 3.1%, which is unlikely to hold significant appeal for income investors seeking to deploy their hard-earned capital.

Indeed, it is possible to obtain a substantially higher return from bonds and easy-access savings accounts. The 10-year gilt yield currently stands at just under 4.4%, for example, while cash balances offer an income return in excess of 4% at present.

In the coming months, it would be wholly unsurprising if the FTSE 100’s dividend yield comes under further pressure as a result of continued capital gains. After all, interest rate cuts enacted across the US, eurozone and the UK over recent months are set to have a positive impact on the world economy’s growth rate.

With further monetary policy easing likely to be implemented in the US and the UK as sticky inflation gradually eases, the operating environment for FTSE 100 stocks, which typically have a heavy international bias, should improve. This could lead to rising profits and stronger investor sentiment that prompts further capital gains and a lower dividend yield for the UK’s large-cap index.

Of course, the FTSE 100’s relatively lacklustre dividend yield does not mean that investors should necessarily look to other asset classes for a worthwhile income. Crucially, an upbeat global economic outlook that leads to higher profitability among FTSE 100 members should allow them to raise dividends at a brisk pace. When combined with an anticipated fall in inflation over the coming months, investors in UK large-cap dividend stocks could experience a generous increase in their spending power.

This contrasts with the outlook for other major asset classes. Easy-access savings accounts, for example, are set to offer a falling income return amid declining interest rates. When combined with the effects of inflation, this could lead to a substantial worsening in spending power. And with bonds offering a fixed income, their presently higher income return vis-à-vis the FTSE 100 is set to be eroded as the effects of dividend growth are gradually felt.

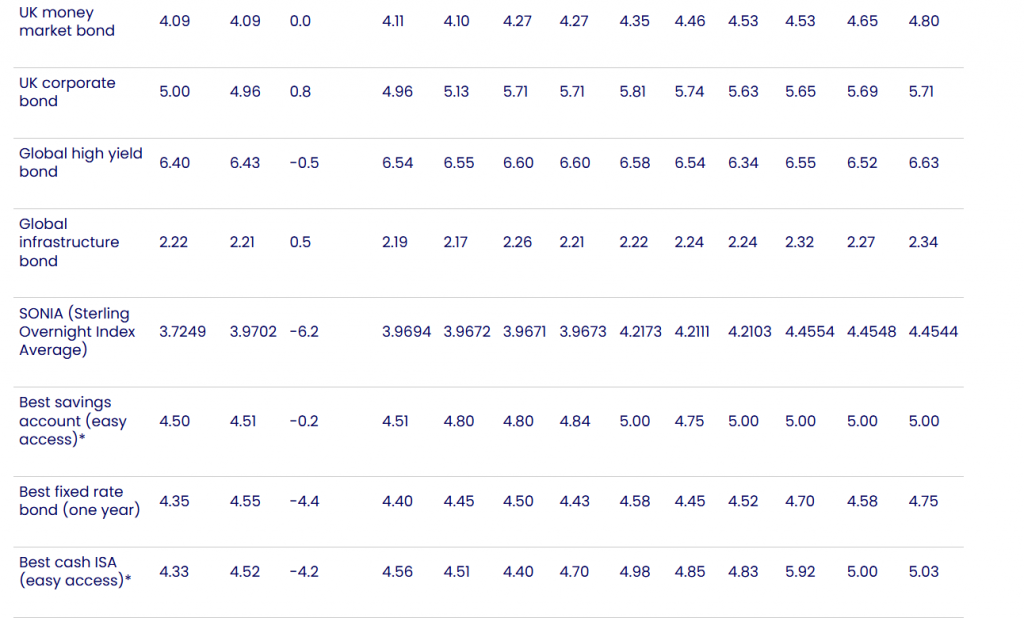

Source: Refinitiv as at 12 January 2026. Bond yields are distribution yields of selected Royal London active bond funds (as at 30 November 2025), except the global infrastructure bond which is 12-month trailing yield for iShares Global Infras ETF USD Dist as at 8 January. SONIA reflects the average of interest rates that banks pay to borrow sterling overnight from each other (8 January). Best accounts by moneyfactscompare.co.uk refer to Annual Equivalent Rate (AER) as at 12 January. *Includes introductory bonus.

While the FTSE 100’s yield is now somewhat unappealing, especially on a relative basis, it is still possible to obtain a highly attractive income return from a basket of UK large-cap shares. Indeed, 41 of the index’s members currently offer a higher income return than the FTSE 100, with 27 of them having a dividend yield in excess of 4%. This suggests it is still possible to build a diverse portfolio of companies that together have a higher income return than that of other major asset classes.

Crucially, though, investors should seek to avoid potential dividend “traps”. This is where a stock has a relatively high yield based on historical dividend payments that ultimately prove to be unsustainable. For example, a company may be experiencing a period of financial difficulty that leads to a dividend cut which has already been priced in by investors via its high yield.

Such companies may, as a result, provide a much lower level of income than their historical yield suggests. They could also produce a relatively weak share price performance as a result of deteriorating investor sentiment and/or lower profitability.

Income seekers can increase their chances of avoiding dividend “traps” simply by focusing on company fundamentals. Considering factors such as dividend cover, which states how many times a firm could afford to make its shareholder payouts; interest cover, which shows how many times a company’s debt servicing costs were covered by operating profits; and focusing on a firm’s future financial prospects could help investors to prioritise stocks that are likely to pay a growing, rather than declining, dividend.

Furthermore, diversifying across a wide range of sectors can help income seekers avoid potential challenges that may be felt more keenly within certain industries. For example, three of the FTSE 100’s current five highest-yielding stocks operate in the Financials industry. Ensuring that a portfolio has exposure to other industries could lessen the impact of unforeseen sector-related difficulties and, ultimately, produce a more reliable and sustainable income stream over the long run.

is among the FTSE 100 index’s highest-yielding stocks at present. The real estate investment trust (REIT), which focuses on London-based offices and out-of-town retail parks, currently yields 5.5%.

While this is 260 basis points higher than the wider index’s income return, the company raised dividends per share by less than 1% in the first half of its current financial year. Furthermore, in its latest full year, the firm’s shareholder payouts were unchanged versus the prior year on a per share basis. This means that investors in the business have experienced a reduction in their spending power of late.

This trend could realistically persist in the short run. Although interest rates have been cut by 150 basis points over the past 17 months, their full impact on the economy is unlikely to be felt in the near term due to the existence of time lags. Once they pass, however, lower interest rates that may yet fall further from their current level should have a positive impact on the economy’s growth rate and spur higher demand, and thereby potentially raising rental income for British Land’s office and retail space.

Indeed, the company’s latest half-year results stated that it expects earnings per share to rise by at least 6% in the 2027 financial year and to grow by 3-6% per annum thereafter. This is set to largely be passed on to investors in the form of a higher dividend. And with inflation expected to move closer to the Bank of England’s 2% target in the second quarter of the year, according to the central bank’s own forecasts, investors in the firm are likely to experience a real-terms rise in their income over the coming years.

An improving operating environment could also lead to a higher share price over the long run. Not only could it support higher property prices that boosts the value of British Land’s portfolio, but a stronger financial performance may also bolster investor sentiment towards the stock. Given that the company’s shares currently trade on a price-to-book ratio of just 0.7, even after their 16% rise in the past six months, there is scope for a significant upward rerating that could equate to relatively impressive capital returns.

In the meantime, the company’s financial position suggests it has the means to overcome further economic uncertainty. For example, its loan-to-value (LTV) ratio currently stands at 39.1%, while it has cash and undrawn credit facilities of £1.7 billion. The firm’s latest half-year results, meanwhile, stated that it was able to reduce administrative costs by 12%.

Clearly, British Land’s share price could prove to be relatively volatile in the short run amid continued economic uncertainty. And while it has a far higher yield than the wider FTSE 100 index, the company’s dividend growth rate may prove to be somewhat lacklustre in the short run.

But as the impact of interest rate cuts on demand for commercial property is gradually felt, the company’s financial performance is likely to improve. This should lead to a positive real-terms increase in dividends, as well as scope for capital growth that follows on from its recent strong share price performance.

Robert Stephens is a freelance contributor and not a direct employee of interactive investor.

Flash update from Kepler Trust Intelligence

The Department for Energy Security and Net Zero has launched a consultation on proposed changes to the inflation indexation used in the Renewable Obligation (RO) and Feed-in Tariff (FiT) schemes. This has hit share prices across the renewables sector. It is important to realise that this is only a consultation, and not necessarily an inevitable change. The net result of a previous consultation in 2023, which covered fixed price certificates and included indexation arrangements, was that no amendments were made to indexation (or anything else). Whilst this recent news has added to the already challenging backdrop for the sector, the share price move for UKW seems extreme, such that the worst outcomes would appear to be more than accounted for by the current share price discount to NAV.

10/11/2025

Kepler View

If either proposal in the consultation were implemented, it would likely translate into a one-off hit to NAV. However, whilst UKW is clearly 100% exposed to the UK government subsidy regime (rather than other geographies), it has a mix of revenues streams across Renewable Obligation Certificates (ROCs), other subsidy schemes (such as CfDs) and market power prices. It is only the indexation mechanism on the RO and not value of the certificate itself that is up for debate within the consultation. The potential negative effects will also be mitigated by the relatively short remaining life of the ROCs in the portfolio (average remaining duration c. 7yrs) and we also note the structurally high dividend cover of UKW’s model. UKW also derives a significantly lower proportion of its revenues from the Renewables Obligation than solar peers, and so we would expect UKW to be significantly less affected than many in the listed peer group.

Fundamentally, UKW appears resilient. UKW’s structurally high dividend cover means that it has options to deploy surplus cashflows towards new investments, buybacks or reducing debt. We note that UKW continues to buy shares back, illustrating the confidence the board has in strength of the balance sheet. UKW’s conservative approach means there are likely to be considerable levers to pull in order to mitigate a sizeable amount of any potential impact.

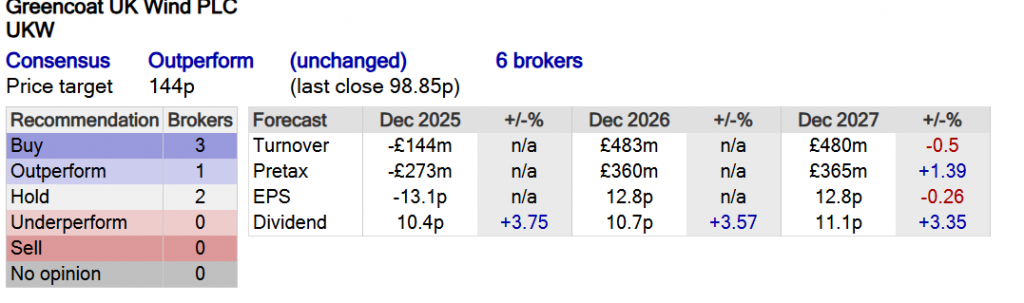

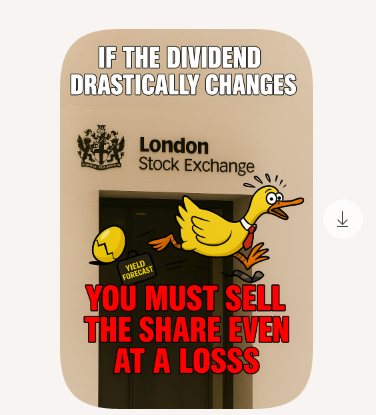

Greencoat UK Wind FY25 total dividend target 10.35p vs 10p YoY

| Company Name | Place change | |

| 1 | Artemis Global Income I Acc | Up 1 |

| 2 | Royal London Short Term Money Mkt Y Acc | Down 1 |

| 3 | Seraphim Space Investment Trust Ord SSIT3.30% | Unchanged |

| 4 | Greencoat UK Wind UKW0.05% | Up 5 |

| 5 | Vanguard LifeStrategy 80% Equity A Acc | Down 1 |

| 6 | Scottish Mortgage Ord SMT0.04% | Down 1 |

| 7 | City of London Ord CTY0.18% | Unchanged |

| 8 | Artemis SmartGARP European Eq I Acc GBP | New |

| 9 | Vanguard FTSE Global All Cp Idx £ Acc | Up 1 |

| 10 | HSBC FTSE All-World Index C Acc | Down 4 |

Royal London Short Term Money Mkt Y Acc has given up its place as the weekly ISA bestseller, ending a six-month spell at the top of the table.

The fund, which offers cash-like returns, has fallen to second place, displaced by the US-light Artemis Global Income I Acc, which returned roughly 45% in 2025.

The reshuffle partly reflects the sheer strength of returns from the Artemis fund, which takes the top spot for the first time. But there’s also a chance that the Royal London fund, and cash funds in general, could lose their shine as interest rates fall.

The Bank of England cut the rate to 3.75% in December and returns from cash funds (and cash accounts) have reduced in turn.

Investors could well now look to seemingly safe assets which pay out higher amounts, such as bonds, or even turn to riskier assets.

We’ve noted that Artemis is enjoying a moment in the sun, and another of its strong performers crops up in the list this week.

Artemis SmartGARP European Equity, which uses a proprietary screening tool to identify stock picks, returned roughly 56% last year and has a big allocation to financials, moves into the table in eighth place. The UK offering from the same franchise, Artemis SmartGARP UK Eq I Acc GBP, sits just outside the table in 15th place.

There’s the usual presence of global equity trackers (and one of Vanguard’s LifeStrategy funds) in the list, plus two very different investor favourites in the form of adventurous global growth fund Scottish Mortgage Ord SMT

and steady UK income play City of London Ord CTY.

Elsewhere, it’s interesting to see two investment trusts with very different runs of performance in the top five.

With geopolitical strife back on the agenda, shares in Seraphim Space Investment Trust Ord SSIT

many of whose holdings have been busy signing defence contracts, have returned almost 9% so far in 2026. That has pushed the shares on to a premium to net asset value (NAV), which at one point reached almost 18% last week but has since moderated to around the 9% mark.

which has been in the wars amid a challenging few years for the renewable energy infrastructure sector, moves up to fourth place. It’s likely that investors still spy a bargain here, given that the shares trade on a roughly 31% discount and come with a dividend yield of more than 10%.

There are plenty of big yields now available in that sector, although this may suggest investors are sceptical about how sustainable they are. NextEnergy Solar Ord NESF

shares now come with a yield just shy of 17%, for example.

Funds and trusts section written by Dave Baxter, senior fund content specialist at ii.

| 96 in com 96.comx normanelsa76 | Howdy! Would you mind if I share your blog with my zynga group ? There’s a lot of folks that I think would really enjoy your content. Please let me know. Thanks |

Of course you can.

A general note about comments.

All comments are moderated and with the best will in the world no comments can be posted in a foreign language.

Although there is appeal for porn, otherwise there wouldn’t be so many sites, it’s not a suitable topic for this blog.

Ditto sex dolls.

Apologies if any comments slip thru the net.

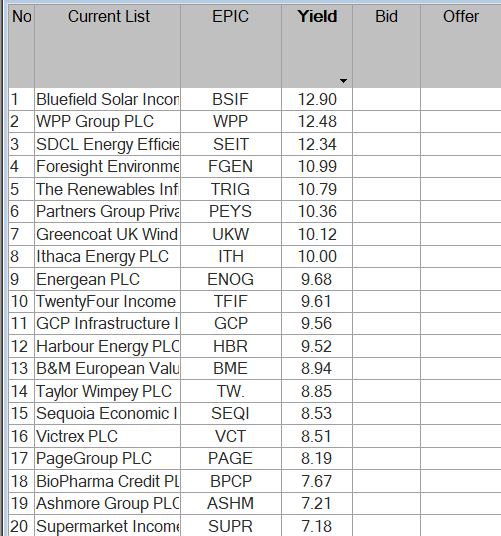

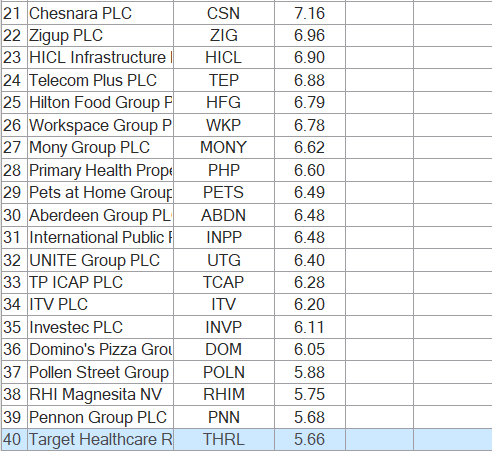

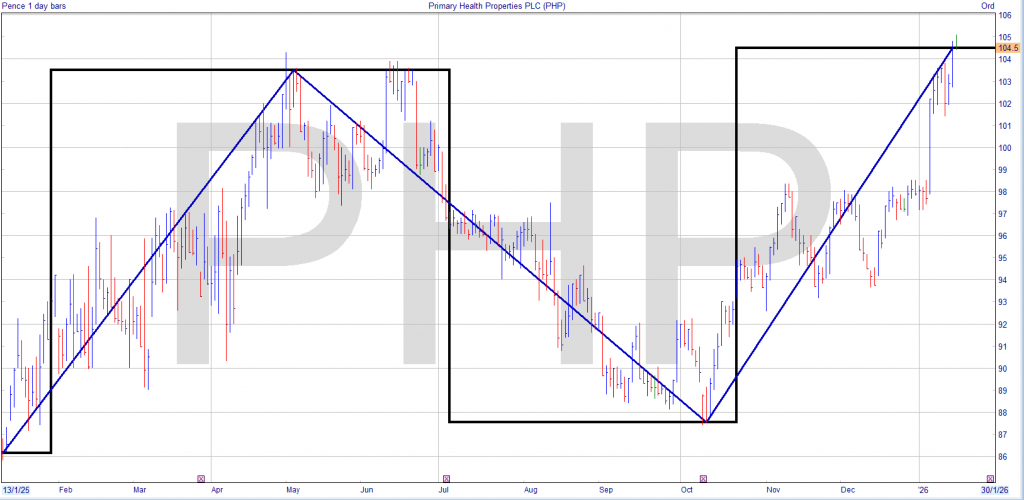

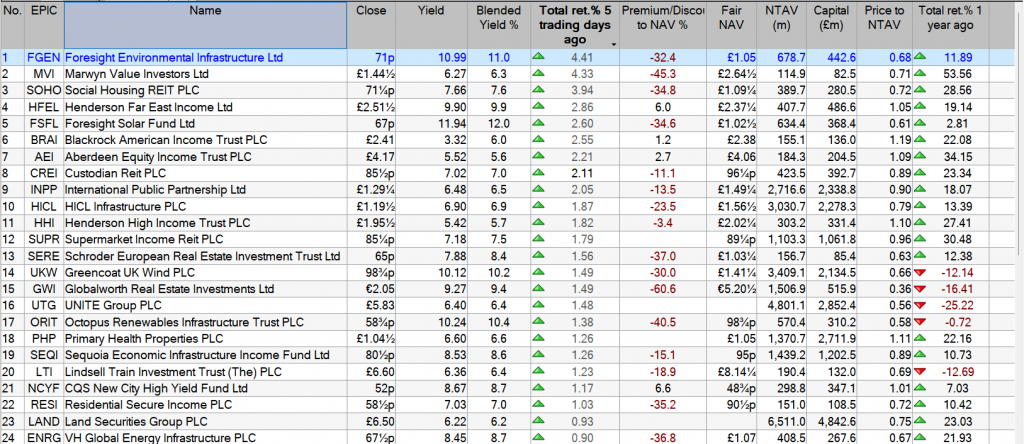

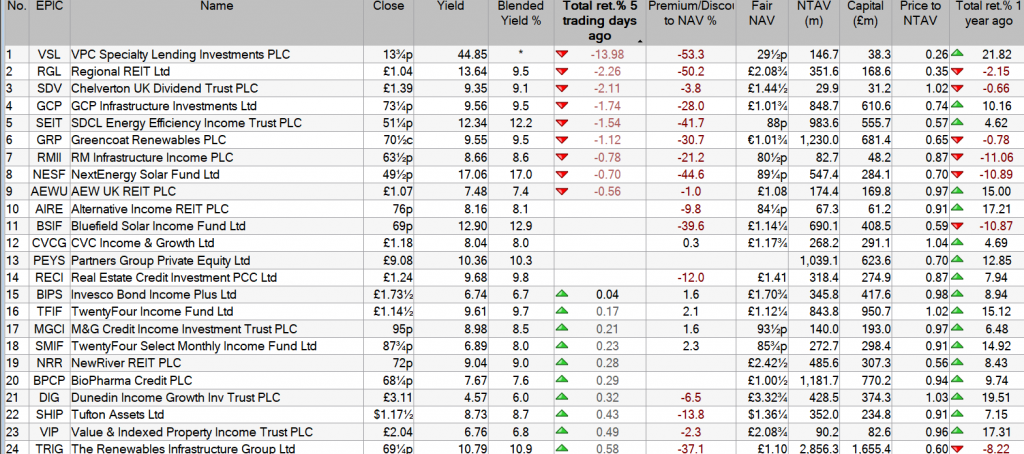

Copied from the Watch List Below.

The yield is a blend of the future fcast yield and the historical yield. Here because of the takeover of Assura the yield may change.

Notice of interim dividend

The Company announces the first quarterly interim dividend in 2026 of 1.825 pence per ordinary share, equivalent to 7.3 pence on an annualised basis, which represents an increase of 2.8% over the dividend per share distributed in 2025 of 7.1 pence and will mark the 30th year of consecutive dividend growth for PHP.

The 1.825 pence dividend will be paid by way of a Property Income Distribution (“PID”) of 1.325 pence and an ordinary dividend of 0.500 pence on 13 March 2026 to shareholders on the register on 30 January 2026.

The Company intends to maintain its strategy of paying a progressive dividend, paid in equal quarterly instalments, that is covered by adjusted earnings in each financial year. Further dividend payments are planned to be made on a quarterly basis in May, August and November 2026 which are expected to comprise a mixture of both PID and normal dividend.

Share price £1.04 dividend 7.3p Yield 7%

You can only base your decisions on the statement from the company and take action if the future dividend changes.

There is no premium/discount to NAV as although the share is a REIT it’s an Investment Company, so you need to look at the Fair Value, which isn’t as reliable as a company’s NAV RNS.

NTAV is the capital minus any outstanding loans.

Trading Tip

Looking at the loans figure you can understand why REIT’s fall in value when interest rates rise and vice versa when they fall.

If you were lucky with your timing or new that REIT’s prices rise when interest rates fall, not all REIT’s so better to be lucky than clever, you would have made a TR return of 22%.

Which you may decide to take some or all of your profit and re-invest in another share, with a higher yield and discount to NAV.

Or maintain the holding and use the ‘secure’ dividend, no dividend is 100% secure

and re-invest the dividends in a higher yielder.

The Watch List will be reviewed at the end of the month and any shares that yield less than 5% will be deleted.

© 2026 Passive Income Live

Theme by Anders Noren — Up ↑