There is a stock market saying Penny expensive, pound cheap as lots of investors would not buy a penny share because of the risk but would consider buying if the price rose.

Similarly with Renewables lots of investors will not take the risk of buying because of the high yields but IF/WHEN the price rises and the yield falls they may be enticed back into buying.

Capitulation is the moment in which investors/traders lose hope in their long position and liquidate at a loss.

When investors/traders capitulate, they sell for fear of a continual decline in the stock price.

The end of a capitulation can present a buying opportunity due to the opinion that everyone who wanted to sell has already done so.

If you read any BB’s, you would have seen lots of investors posting they have sold out, capitulation.

The rules for the SNOWBALL for any new readers, there are only 3.

RULE 1

RULE 2

RULE 3

Here’s the plan.

The 2026 fcast is 10k. The SNOWBALL is ahead of fcast so it’s possible it could earn income for year 7/8 subject to Mr. Market but it’s too early in the year to change the fcast.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

To me, there are few more appealing ideas than earning a large second income without lifting a finger. This is known as passive income, and while it may sound too good to be true, history shows us that it really isn’t.

But how can an investor turn this from a pipe dream into reality? Here’s a step-by-step plan of how you could turn a £300 monthly investment in shares into an extra income of more than £38,000 a year.

Building the pot

Our strategy involves a little legwork at the beginning. You need to set up a tax-efficient investing account, preferably a Stocks and Shares ISA and/or a Self-Invested Personal Pension (SIPP). Then comes the task of finding the best shares, trusts, and funds to fill it with, based on your investing goals and tolerance and risk.

However, once it’s up and running, you should be able to sit back and watch your wealth steadily grow over time. History isn’t always a reliable guide to future returns. But the long-term performance of the stock market is unmatched, which gives me enormous confidence as an investor.

Since the mid-20th century, share investing has delivered an average annual return of 8% to 10%.

Passive income plans

The cornerstone of our strategy is to use our ISA or SIPP to buy shares that pay dividends. That passive income could be used for retirement spending later on. But in the meantime, it is reinvested to amplify compound gains and grow the size of the pension pot.

We should look for stocks that could pay healthy dividends not just now but in the future. Companies with market-leading positions and diverse revenue streams can deliver reliable and growing dividends over time. Firms with strong balance sheets and cash generation should also be a priority.

A top dividend stock

Coca-Cola HBC (LSE:CCH) is a great FTSE 100 dividend share that enjoys all of these qualities. In fact, it’s a dividend powerhouse I hold in my own personal SIPP.

Dividends here have risen every year since 2012. That’s when the Coca-Cola bottler first listed on the London stock market. And over the past five years they’ve grown at a breakneck compound annual rate of 13.4%.

The question is, can the company keep delivering impressive dividends? I’m confident it can, even though it faces competitive pressures and the problem of rising costs. The exceptional brand power of its drinks mean they remain in high demand across the economic cycle. They also allow the company to hike prices to grow earnings and cash flows, the perfect conditions for sustained dividend growth.

A £38k+ second income

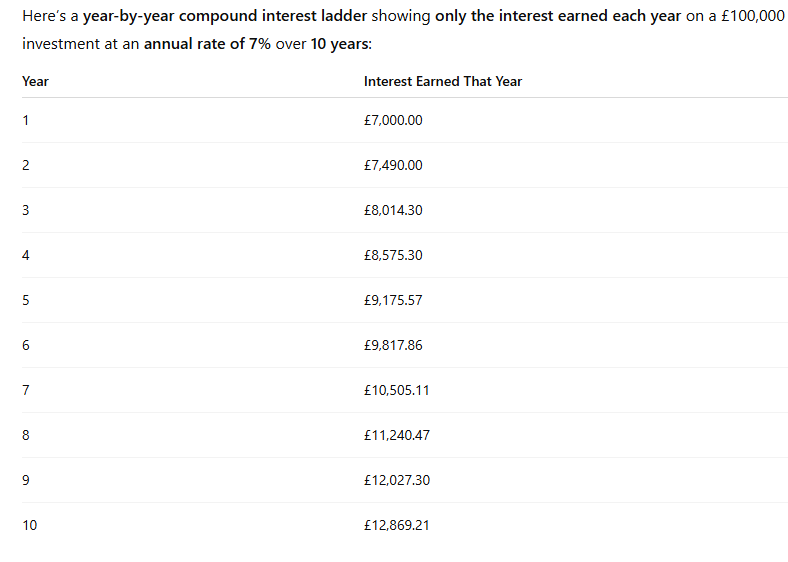

With a diversified portfolio of shares like Coca-Cola HBC, I think an average annual return of 9% is quite possible. Based on this, a £300 monthly investment would, after 30 years, create an ISA or SIPP worth £549,223.

If this was invested in 7%-yielding dividend shares, it could generate an annual second income of £38,446. Combined with the State Pension, this could provide a very comfortable retirement.

A lesson Buffett has learned first hand with his investment in Coca-Cola (NYSE:KO). The soft drinks giant has used its consistent and steady cash flows to increase dividends every year for 63 years in a row. And consequently, Buffett’s now earning more than a 60% yield on his original investment in the late 1980s.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

For income investors who simply want to be passive in nature, buying a FTSE 250 index tracker that distributes dividends is one option. However, I know many who prefer to actively select FTSE 250 stocks. One benefit is the ability to boost the average dividend yield. So is it possible to buy several stocks with a yield double that of the 3.25% index? Absolutely.

Filtering carefully

There are currently 27 stocks that fit the initial filter of having a yield of 6.5% or higher. However, I don’t believe all 27 are worth buying. Some in that mix have a high yield right now because their share prices have tumbled 30% or more over the past year. This has artificially boosted the yield, but I think business troubles could lead to a dividend cut in the near future. Therefore, an investor would likely want to avoid those companies.

Within the sustainable-yield group, the next thought is which sectors do I like? A company might have a good track record for income payments, but if I think the sector is going to underperform in the coming years, it might not be a great pick. In my view, finance, telecoms, and renewable energy are three areas that could do well in the coming years.

After adding in that sector filter, I can now clearly see companies with a generous yield that operate in a space I think will do well. This is the sweet spot. In terms of individual names included in this bucket, Ashmore Group (6.88% yield), Telecom Plus (6.95%) and Greencoat UK Wind (10.98%) could all be considered.

Ideally, an investor could look to include these as part of a larger diversified portfolio. The benefit is that if one company cuts its dividend in the future, the overall negative impact on the portfolio is manageable.

Digging deeper

Another example that could be considered is the TwentyFour Income Fund (LSE:TFIF). The stock is basically flat over the past year, but it boasts a high yield of 9.85%. The fund managers focus on buying asset-backed securities, such as loans for cars, mortgages, and other forms of consumer debt.

These securities pay a high coupon, given the risk of these loans is often higher than that of more traditional debt. However, the fact that the loans are collateralised by assets such as cars and houses means that even if someone defaults, it can help recover some of the loss. It holds 173 investments as of the latest company update, indicating a well-diversified portfolio.

As for dividends, the company pays out almost all of the profit it generates each year to shareholders. That means dividends are largely funded by real cash interest, not capital. That’s a key element in keeping it sustainable going forward. Further, the company has met or exceeded dividend targets every year since its launch in 2013! So, although past performance doesn’t guarantee future returns, the track record does speak for itself.

In terms of risks, the debt and bonds bought depend on consumer and corporate health. So if we get an economic downturn with higher unemployment or housing stress, it could quickly result in higher loan losses.

Even with that concern, I think it’s still a dividend stock with a high yield for investors to consider.

Headline:Renew Infra Grp Ld – Announcement of 2025 Annual ResultsDate/Time:27/02/2026 07:00:50 ▼

27 February 2026

The Renewables Infrastructure Group Limited

The Renewables Infrastructure Group (“TRIG” or “the Company”) is a London-listed renewable energy investment company. TRIG creates shareholder value through a resilient dividend and long-term capital growth, underpinned by a diversified portfolio of renewable energy infrastructure, and managed jointly by specialist investment and operations managers.

Announcement of 2025 Annual Results

TRIG announces its Annual Results for the Company for the year ended 31 December 2025. The Annual Report and Accounts are available on the Company’s website: www.trig-ltd.com.

Highlights

For the year ended 31 December 2025

Resilient cash generation and reduction in Net Asset Value in a challenging macro environment:

·

Operational cash flows of £375 million, covering the dividend 2.1x on a gross basis (2024: 2.1x) and 1.0x (2024: 1.0x) on a net basis after the repayment of £192m project level debt.

·

Net Asset Value (“NAV”) per share2 of 104.0p (31 December 2024: 115.9p), a reduction of 11.9p over the year, driven primarily by external factors including lower power price forecasts, low wind resource and higher discount rates.

·

The weighted average Portfolio Valuation3 discount rate as at 31 December 2025 has increased to 9.0% (31 December 2024: 8.6%), primarily reflecting discount rate increases for European assets and UK offshore wind assets and regulatory changes.

Disciplined capital allocation and conservative balance sheet management:

·

£200 million private placement debt raised post year‑end in February 2026, with a repayment profile that maintains the Company’s low interest rate risk and low refinancing risk. Approximately 90% of project-level debt is fixed rate and fully amortising.

·

Long-term gearing represents 41% of look-through enterprise value with disposals being actively progressed to further reduce short term borrowings.

·

Strong revenue visibility with 75% of portfolio revenues fixed per MWh over the next five years.

·

£80m of the Company’s £150m share buyback programme has been completed, consistent with the proceeds from the €100m partial sell-down of the Gode offshore windfarm. With the private placement raised, the Board is accelerating the share buyback programme alongside these results.

Clear strategy to support long‑term returns:

·

Active portfolio management delivered £32 million of value‑enhancing commercial and operational initiatives during the year.

·

Progress across TRIG’s 900MW development pipeline, with over 200MW of projects in construction, including the 78MW Ryton battery storage project and repowering of Cuxac onshore wind farm.

·

Target dividend for 2026 maintained at 7.55p per share3, reflecting the Board’s focus on balancing an attractive income yield with the restoration of net dividend cover to support future growth.

Richard Morse, Chairman of TRIG, said:

“2025 was a challenging year impacted by policy uncertainty, low wind resource and lower power price forecasts, all of which weighed on the Company’s valuation.

Despite these challenges, TRIG’s portfolio and business model has again demonstrated its resilience by generating £375 million of operational cash which funded a fully covered dividend and enabled significant debt reduction to strengthen the Company’s balance sheet.

Our priority is to restore dividend cover to historical levels and to deliver on the targets we set last year. The Board remains confident in TRIG’s standalone strategy to provide our investors with a sustainable dividend and the opportunity for capital growth.”

Footnotes:

The Company

The Renewables Infrastructure Group (“TRIG” or the “Company”) is a leading London-listed renewable energy infrastructure investment company. The Company seeks to provide shareholders with an attractive long-term, income-based return with a positive correlation to inflation by focusing on strong cash generation across a diversified portfolio of predominantly operating projects.

TRIG is invested in a portfolio of wind, solar and battery storage projects across six markets in Europe with a net operational capacity of 2.3GW. In 2025, the portfolio generated enough renewable electricity to power the equivalent of 1.6 million homes and to avoid 1.8 million tonnes of carbon emissions per annum.

Further details can be found on TRIG’s website at www.trig-ltd.com.

Investment Manager

InfraRed is a leading international mid-market infrastructure asset manager. Over the past 25 years, InfraRed has established itself as a highly successful developer, particularly in early-stage projects, and an active steward of essential infrastructure.

InfraRed manages US$13bn of equity capital1 for investors around the globe in listed and private funds across both core and value-add strategies.

InfraRed combines a global reach, operating worldwide from offices in London, Frankfurt, Madrid, New York, Miami, Sydney and Seoul, with deep sector expertise from a team of more than 160 people.

InfraRed is part of SLC Management, the institutional alternatives and traditional asset management business of Sun Life, and benefits from its scale and global platform.

Operations Manager

TRIG’s Operations Manager is RES (“Renewable Energy Systems”). RES is the world’s largest independent renewable energy company, working across 24 countries and active in wind, solar, energy storage, biomass, hydro, green hydrogen, transmission, and distribution. An industry innovator for over 40 years, RES has delivered more than 29GW of renewable energy projects across the globe.

As a service provider, RES has the skills and experience in asset management, operations and maintenance (O&M), and spare parts – supporting 45GW of renewable assets worldwide. RES brings to the market a range of purposeful, practical technology-based products and digital solutions designed to maximise investment and deployment of renewable energy. RES is the power behind a clean energy future where everyone has access to affordable zero carbon energy bringing together global experience, passion, and the innovation of its 4,500 people to transform the way energy is generated, stored and supplied.

2025 was, in many ways, a frustrating year for The Renewables Infrastructure Group and I would like to extend my thanks to our shareholders for their support throughout. A combination of external factors including macroeconomic and public policy uncertainty (particularly in the United Kingdom); exceptionally low wind speeds; and reductions in power price forecasts all resulted in a lower Net Asset Value (“NAV”) of the Company and a tightening of the dividend cover.

The withdrawal of HICL from the proposed combination with TRIG late in the year was disappointing. While the combination process has delayed the implementation of TRIG’s standalone strategy that was set out at the Capital Markets Seminar in May 2025, including targeted asset sales and debt financing, the Board remains convinced that TRIG is well positioned as an independent business. Our confidence is underpinned by a clear strategy, a high-quality portfolio and shareholder support.

Our 2025 results reinforce the resilience and robustness of TRIG’s business model, reflected in £375m of operational cash generated¹, which funded a fully covered dividend in line with expectations and the repayment of £192m of project-level debt. We are pleased to have completed the £200m private placement debt issuance, which was announced on 12 February 2026. Disposal activity remains a key priority.

The Board remains committed to delivering capital and income growth to shareholders. Central to this is our policy of increasing the dividend to the extent it is prudent to do so, while retaining the flexibility to invest for attractive capital growth and desire to build cash dividend cover². The Board has decided to maintain the target dividend for 2026 at 7.55p per share. Having discussed the rate of dividend progression with shareholders over recent months, the Board has concluded that there is recognition that the current dividend level is already at a highly attractive level, which represents 7% of NAV and a c.11% dividend yield³. The Board considers it important to prioritise restoring net dividend cover to the range 1.1x-1.2x to generate sufficient cash to fund investments that will drive future growth of the NAV. The Board will continue its open dialogue with shareholders on the Company’s strategy in 2026.

Facilitating long-term growth through active portfolio management is core to TRIG’s strategy. This strategy is underpinned by debt capacity and active portfolio rotation, accretive reinvestment and additional commercial and operational levers. It is anchored by a robust approach to capital allocation and a resilient dividend. Feedback from shareholders has been supportive of this strategy.

Key highlights of strategic progress made by the two Managers in 2025:

In 2025, our 2.3GW portfolio generated 5.4TWh of clean electricity, the equivalent of 2% of the UK’s total electricity generation⁴. TRIG’s high-quality portfolio located across the UK and Europe is the Company’s bedrock. Over 65% of the portfolio’s revenues are fixed per MWh generated over the next ten years, and c.90% of debt is fixed rate and fully amortising in line with the profile of fixed-price revenues. This deliberately considered approach to revenue and balance sheet management is unique among listed renewables investment companies and gives the Board maximum flexibility when evolving the strategy and appraising the options for the Company in order to maximise long-term returns for shareholders.

During the year, the Board secured a reduction in management fees for TRIG, amounting to c.£8m p.a. (a 28% reduction), which contributes to the cost efficiency of the Company⁵. The total operating expenses ratio for 2025 was 0.94%. Good and efficient governance remains a focus and the breadth of skills of the Directors means that TRIG is able to deliver a diversified, active-management strategy at scale with a lean Board of Directors.

Financial performance

TRIG’s portfolio is highly cash generative with operational cash flows generated in 2025 totalling £375m, representing 2.1 times gross cash cover of the 2025 dividend. After project-level debt repayments of £192m across the Group⁶, net dividend cover was 1.0 times.

As signalled in the Company’s 2025 Interim Results, dividend cover for 2025 was moderated by below budget portfolio generation predominantly due to significantly lower than average wind speeds in H1. Meanwhile, actual power price levels achieved during the year were broadly in line with budgeted levels.

The Company’s Net Asset Value per share as at 31 December 2025 was 104.0p, an 11.9p reduction to the prior year driven principally by macro and external factors. The external factors that weighed on the valuation included lower revenue price forecasts (-6.5p), low wind resource in the year and unscheduled, uncompensated grid outages (-4.2p) and higher discount rates reflecting the increase in European reference rates and the softer market for UK offshore wind investments (-2.4p).

The Managers’ value enhancement activities including improving energy yields through software and hardware upgrades and entering into fixed power price arrangements added 1.3p to NAV. Earnings per share for the year was -5.4p, reflecting the reduction in valuation.

Capital allocation

Given the prevailing weakness in the TRIG share price, which is consistent with the broader sector, the Board recognises the extraordinary value offered through buying back the Company’s shares. £80m of the Company’s £150m share buyback programme has been completed, consistent with the proceeds from the €100m partial sell-down of the Gode offshore windfarm. The Board has varied the pace of the buyback programme throughout the year in response to TRIG’s share price, while being mindful of the Company’s cash resources. New investments entered into exceeded the hurdle rate set by share buybacks.

With the private placement debt now raised, the Board is increasing the pace of the buyback. A further assessment will be made as to the size and pace of the share buyback programme as disposals are executed. The Board remains focused on disciplined capital allocation to drive shareholder returns and will continue to consider carefully the right balance between retaining capital for accretive growth and returning capital to shareholders through dividends and share buybacks.

Outlook

Every asset class is defined by its return relative to the risk taken. It is how opportunities are pursued and risk is managed that defines the success of any investment strategy over the longer term.

Renewables assets are subject to the same principal risks today as in 2013, when the first renewables infrastructure investment companies, including TRIG, were launched. This principally includes exposure to movements in power prices, underlying portfolio performance, and regulatory and public policy risk. The increased risks have weighed on sector NAVs and sentiment over the past 24 months, overlaid with an increase in the cost of capital to levels not seen for almost 20 years.

The TRIG Board believes the companies that will weather these challenges and deliver long-term value to shareholders are those that can operate at scale with a growth investment pipeline, remain diversified across geographies and technologies, provide clear cash flow visibility, resilient portfolio earnings and a robust capital structure. TRIG is the only London-listed renewables investment company fulfilling all of these criteria, managed by its unique dual manager structure.

The Company will have its first Continuation Vote at the Annual General Meeting in June 2026. Ahead of that vote, the Board will present a fulsome update on strategy to shareholders at a Capital Markets Seminar in May 2026, which will seek to give investors the opportunity to support the Company’s long term future with confidence.

Looking forward, the energy transition remains embedded within government policy and central to corporate strategies across Europe. Society continues to demand more secure and cleaner electricity generation. TRIG provides investors with access to the megatrend of global electrification and the UK’s desire for a cleaner, secure and affordable energy system.

In 2025, energy demand in the European Union returned to growth for the first time since 2017 and electricity demand is forecast to increase by around 2% per year through 2030. While Britain recorded a second consecutive year of power demand growth and the fastest annual growth for the first time in over two decades.⁷ Renewables capacity continues to grow, with capacity expansions setting records for 22 years running.⁸ TRIG is actively participating in this transition, reinvesting into new capacity to extend the life of our portfolio, while continuing to offer shareholders an attractive, resilient dividend alongside the potential for capital growth.

Richard Morse

Chair 26 February 2026

Investment Report

Financialhighlights

Financial performance and near-term outlook

For a full table of financial performance metrics for the year, see the table on page 18 of the Annual Report.

The Company expects to sell assets in line with the portfolio rotation strategy, which can be expected to reduce revenue, EBITDA, project and fund-level debt. New higher returning projects can be expected to grow revenue and EBITDA as these come into operation once through construction.

Cash flows and near-term outlook

The Group’s operational cash flow for the year was £375m, which represents 2.1 times gross cover of the £182m cash dividend paid to shareholders. Operational cash flows were used to repay £192m project-level debt. After operating expenses, finance costs and working capital, the Group’s distributable cash flow of £183m (2024: £184m) covered the cash dividend 1.0 times.

Pro-forma portfolio EBITDA for the year was £459m (2024: £493m). The table on the previous page shows TRIG’s share (pro-rated for TRIG investment %) of revenues, portfolio EBITDA and cash received from investments. The reduction from 2024 is predominantly due to a combination of the partial sale of Gode (c.£25m of the reduction) in addition to low wind resource, low power prices in Sweden (resulting in economic curtailment) and higher uncompensated grid downtime during 2025.

The balances on the opposite page are not on a statutory IFRS basis, but are pro-forma portfolio balances, which show the Group’s share of the revenue and EBITDA for each of the projects. These balances have been provided to give shareholders more transparency as to the Group’s underlying portfolio performance, capacity for investments and resilience to service the dividend.

In the absence of any disposals or assets entering operations, and assuming the normalisation of wind resource and recognising that the more significant grid outages experienced in 2025 are being resolved, revenues are expected to improve from 2025 to 2026.

Revenues were lower in 2025 compared to 2024, driven by the same factors as covered above for portfolio EBITDA (Gode disposal, wind resource, economic curtailment and grid downtime). Distributable cash flow reduced less than revenue and portfolio EBITDA from 2024 to 2025, principally as a result of taxes and debt service paid at Gode reducing the impact with the sell down of the investment.

Portfolio EBITDA margin was strong at 71% reflecting the high capital expenditure and low operational gearing of renewables projects. After servicing project finance interest and debt repayments, tax and working capital, cash is distributed from the portfolio to TRIG.

Valuation

The Company’s Net Asset Value as at 31 December 2025 was 104.0p per share (31 December 2024: 115.9p per share) and the Company’s portfolio valuation was £2,875m. Earnings for the year were -5.4p per share (2024: -4.7p), principally due to macro and external factors.

InfraRed and RES continue to actively manage TRIG’s portfolio to reduce the impact of the macro environment and external factors on the portfolio valuation, adding c.£32m in the year to portfolio valuation.

Active management of TRIG’s financial and operational activities includes energy yield enhancements across several assets, profit on disposal for the partial stake in Gode, active revenue management across the portfolio and value addition in relation to a planned adjacent battery project to the existing Valdesolar solar farm in Spain. These resulted in a combined positive impact to NAV per share. In addition, share buybacks added 0.8p per share to NAV.

Macroeconomic movements and changes in government policy adversely impacted the Portfolio Valuation, and therefore earnings, by 7.6p per share. These included reductions in revenue forecasts, increases in discount rates across Europe and UK offshore wind, changes in the UK Government’s indexation basis for RO and FIT arrangements, and reductions in capital allowances and increases in business rates announced in the UK Government’s Autumn 2025 Budget. Other factors, principally lower than forecast generation due to low UK wind speeds, reduced the NAV by a further 6.3p per share.

Greater detail on the valuation movements for the year ended 31 December 2025 can be found in the Valuation of the Portfolio section on page 37.

Capital allocation

Responsible balance sheet management and disciplined capital allocation are important factors to help address TRIG’s 38% share price discount to Net Asset Value as at 25 February 2026.

In March 2025, €100m of proceeds were received from partial sale of a stake in the Gode offshore wind farm at a 9% premium to NAV to the valuation of the investment as at 31 December 2023.

In February 2026, TRIG issued a £200m debt private placement. Following strong demand, the issuance was upsized from the £150m target and pricing tightened to a weighted average interest rate of 5.23%. The debt has an amortisation profile aligned with the term of TRIG’s current fixed-revenue arrangements that ensures TRIG continues to have low interest rate and low refinancing risks.

The market for secondary renewables transactions has evolved over the past couple of years with an oversupply of renewables assets, in particular resulting from developers selling positions to strengthen their balance sheet, relative to the capital looking to deploy into renewables investments. An imbalance partly caused by regulatory uncertainty, particularly in the UK. While it was positive that potential plans to overhaul and disrupt the electricity market were abandoned by the UK Government during the summer, this was promptly followed by a consultation to retrospectively change the basis of indexation for RO and FIT arrangements, which has continued to depress sentiment towards the sector going into 2026 despite robust underlying performance of investments.

During 2025, the Board has progressed its capital allocation priorities.

Share buybacks delivered 0.8p of NAV per share accretion in the year to 31 December 2025 from the repurchase of 73 million shares for £57m. Buybacks at a significant discount to NAV are accretive to NAV per share and distributable cash flow per share. The buyback programme was suspended from 17 November 2025 while the proposed combination with HICL was announced, before being recommenced on 12 January 2026.

The vast majority of TRIG’s debt is long-term, fixed-rate, amortising project-level debt. The average interest rate on TRIG’s overall debt is 3.8%. Project-level debt was reduced by £192m in the period and was £1.7bn as at 31 December 2025, representing 37% of enterprise value. Including the £200m private placement signed post-year-end, this structural debt would represent 41% of enterprise value. TRIG’s exposure to floating-rate debt and refinancing risk is limited to the Company’s Revolving Credit Facility. Borrowings under the RCF were £213m on 25 February 2026 following receipt of proceeds from the private placement issuance. The interest rate on the RCF is currently c.5%, drawn in both Sterling and Euros.

£116m of construction spend was incurred during the year, mostly relating to the Ryton and Spennymoor battery storage projects and the repowering of the Cuxac onshore wind farm. Development and construction-stage investments are a strategic priority of the Company to enhance returns, extend the life of the portfolio and progress technology diversification. New investment decisions are benchmarked against alternative uses of capital, particularly share buybacks.

As at 31 December 2025, the Company had outstanding investment commitments of £114m, principally relating to construction activities.

Dividend

The Company’s dividend policy is to increase the dividend when the Board considers it prudent to do so, considering forecast cash flows, expected dividend cover, inflation across TRIG’s key markets, the outlook for electricity prices and the operational performance of the Company’s portfolio. The dividend target for 2026 has been set at 7.55p per share, maintaining the level of the 2025 dividend. The Board has discussed the rate of dividend progression in detail with shareholders during 2025 and there is recognition that this dividend level, which represents 7% of NAV, is at a highly attractive level while prioritising restoring net dividend cover to 1.1x-1.2x. The 2026 dividend target represents a c.11% yield to TRIG’s closing share price on 25 February 2026