How the 2026 line-up has changed

As mentioned in the introduction, for an investor building an income portfolio today, it is more challenging than a year ago as fund yields across the board are lower.

To address this and reduce the amount required for the £10,000 income challenge, I’ve added in two specialist funds that aim to deliver an extra chunk of income at the expense of capital growth.

Overall, the 2026 portfolio yields 4.67%. Generating £10,000 of income would require a portfolio size of £215,000. This is the lowest starting value in the period I’ve been running the portfolio and is an attempt to give the portfolio a greater bias towards income generation.

All yield figures were sourced in late January, but bear in mind that yield figures are not static. In each case the income share class has been chosen, as this share class returns the income back to investors rather than reinvesting the income (which is what the accumulation share class does).

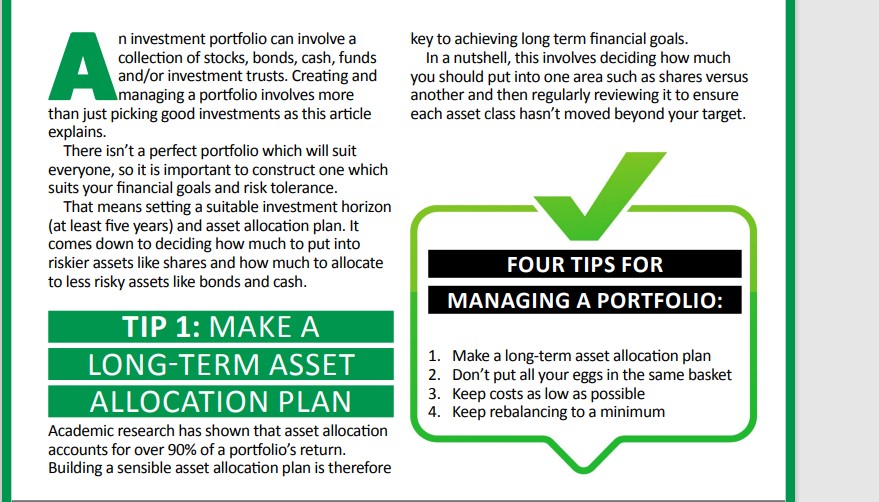

Specialist income funds explained

The specialist income funds are not for everyone and the way they invest is not as straightforward as most other funds. However, they are a way of boosting the overall yield of a portfolio, particularly when only funds can be chosen.

Schroder Income Maximiser and Fidelity Global Enhanced Income have been handed weightings of 10% and 12.5% respectively.

Both funds artificially boost their dividend yields through a special technique that involves selling derivatives to other investors.

Under this strategy, the fund manager agrees to share any future capital gains with a third party. A fee is paid for the agreement, which creates immediate, up-front income. This can be distributed to fund investors as a stream of income.

The downside is that when a fund’s holdings rise in value some of that gain goes to whoever bought the derivative. Therefore, such funds lag the pack in rising markets.

Schroder Income Maximiser’s top 10 holdings are all FTSE 100 income heavyweights. Its top 10 weightings are small in percentage terms, with top holding GSK

accounting for 3.3% of the fund and

the 10th-largest position, a 2.7% position.

Fidelity Global Enhanced Income has a very low weighting to the US (just 7.4% of the fund) and an overweight position to the UK of 20.4%. There’s one UK name in the top 10 holdings, Reckitt Benckiser (LSE:RKT), the consumer staples giant.

The fund’s top three holdings are

Taiwan Semiconductor Manufacturing Co Ltd ADR TSM 2.98%

healthcare giant Roche Holding AG ROG 2.30%

and Spanish clothing firm Industria De Diseno Textil SA Share From Split ITX3.36%, widely known as Inditex.

My thinking is that given that risk has been spread across various funds with different mandates, this gives the portfolio plenty of diversification in rising markets (even with the two enhanced income funds) and the bond exposure can protect capital if a stock market downturn occurs.

Two funds taken out

Exiting the portfolio are Fidelity Global Dividend and Vanguard FTSE All World High Dividend Yield ETF. This is solely down to both fund yields being low, which makes it challenging to have a sufficiently high enough overall portfolio yield.

Fidelity Global Divided has a yield of 2.5%. If I were to choose it instead of Fidelity Global Enhanced Income and handed it the same 10% portfolio weighting it would bring the portfolio’s yield down from 4.67% to 4.34%.

Fidelity Global Divided does typically have a low yield (it was 2.4% a year ago) as the fund aims to limit downside risks by being defensively positioned. However, while I think the fund is a worthy candidate as a global equity income holding, I could no longer retain it given fund yields have fallen across the board compared to when I made my selections a year ago.

Vanguard FTSE All World High Dividend Yield ETF is now offering a yield of 2.8% compared to 3.2% a year ago. As a result, I’ve opted to remove it as part of my plan to have a higher overall portfolio yield. The exchange-traded fund follows the ups and downs of the FTSE All-World High Yield Index, which comprises more than 2,000 large and mid-cap stocks with higher-than-average dividend yields.

Money market fund removed in favour of higher-yield option

For the bonds, one change has been made to the 2026 line-up. Royal London Short Term Money Market has been removed in favour of L&G Short Dated £ Corporate Bond Index.

Over the past couple of years, money market funds have proved to be a solid allocation for cautious investors, or for those looking to park cash for a short time. In 2025, money market funds returned 4%-plus in sterling terms, with negligible volatility.

However, interest rate cuts mean the amount of income such funds can generate is declining. With UK interest rates standing at 3.75% at the time of publication, and the expectation of one or two cuts in 2026, this will quickly feed through into lower future returns for these funds. A year ago, Royal London Short Term Money Market had a yield of 4.8%, but it is now 3.9%.

In theory, lower rates could lead some investors to take on greater risk elsewhere in pursuit of potentially higher returns.

One route for investors with a slightly higher risk appetite might be short-dated enhanced income funds, which generally offer more attractive yields. However, the trade-off is that a bit more risk needs to be taken versus money market funds that aim to deliver a cash-like return.

One option is the L&G Short Dated £ Corporate Bond Index fund, which invests in investment-grade sterling bonds with less than five years to maturity and tracks the Markit iBoxx GBP Corporates 1-5 Index. The distribution yield is around 4.7% and the yearly fee is 0.14%.

Overall, the bond exposure is around 35%, which is slightly less than last year’s 40% weighting. This is due to handing Artemis Monthly Distribution a 15% weighting rather than a 20% weighting due to a lower fund yield (3.7%) than a year ago (4.3%).

| Fund | Yield (%) | Percentage weighting (%) | Investment (£) | Estimated income | How often the dividend is paid |

| UK equity income | |||||

| Artemis Income | 3.3 | 7.5 | 16,125 | 532.125 | Twice a year |

| Man Income | 4.3 | 7.5 | 16,125 | 693.375 | Monthly |

| Schroder Income Maximiser | 7 | 10 | 21,500 | 1505 | Quarterly |

| Vanguard FTSE UK Equity Income Index* | 4.2 | 7.5 | 16,125 | 677.25 | Twice a year |

| Global/overseas income | |||||

| Fidelity Global Enhanced Income | 5.1 | 12.5 | 26,875 | 1370.625 | Quarterly |

| Guinness Asian Equity Income | 3.5 | 10 | 21,500 | 752.5 | Twice a year |

| Mixed Asset | |||||

| Artemis Monthly Distribution | 3.7 | 15 | 32,250 | 1193.25 | Monthly |

| Bonds | |||||

| Royal London Global Bond Opportunities | 6 | 10 | 21,500 | 1290 | Quarterly |

| Jupiter Strategic Bond** | 4.7 | 10 | 21,500 | 1010.5 | Quarterly |

| L&G Short Dated £ Corporate Bond Index*** | 4.7 | 10 | 21,500 | 1010.5 | Twice a year |

| Total | 4.6675 | 100 | 215,000 | 10,035 (rounded) |

All current yield figures sourced from Trustnet at end of January and additional check made that yields are in line with the fund firm factsheets with additional check with latest fund firm factsheets that show dividend yield figures, apart from the three stated below. Past performance is not a guide to future performance.

At a glance: how the other retained funds invest

Artemis Income

This fund aims to provide a steady and growing income along with capital growth. It has a larger company focus, which accounts for 85% of the fund. Banks are well represented, with Lloyds Banking Group LLOY 0.49%

and NatWest Group NWG 0.38%

having weightings of 4.9%, while

Barclays BARC3.66% is also in its top 10 holdings, accounting for 4.1%.

Its longstanding fund manager Adrian Frost has managed the fund since 2002, with signs of robust succession planning in place, with co-manager Nick Shenton joining in January 2013 and co-manager Andy Marsh joining in February 2018.

Man Income

The fund adopts a value-driven approach to provide a yield well in excess of the FTSE-All Share’s. Henry Dixon has managed the fund since inception in November 2013, when he joined Man GLG.

It pays a monthly income, which is rare for a UK equity income fund as most pay out quarterly or twice a year.

Vanguard FTSE UK Equity Income Index

The index this tracker fund follows – the FTSE UK Equity Income index – consists of shares “that are expected to pay dividends that generally are higher than average”. Therefore, its performance and income generation is heavily influenced by the biggest FTSE 100 dividend stocks.

It has comfortably outperformed the UK equity income sector average over one, three, five, and 10 years. As well as performance beating many fund managers, the fund generates a higher yield than the wider market at 4.2% versus around 3% for the FTSE 100 index. However, its yield is notably lower than a year ago, when it stood at 4.9%.

Guinness Asian Equity Income

An equally weighted approach to 36 stocks helps to reduce stock-specific risk. Edmund Harriss, who has managed the fund since inception in 2006, focuses on high-quality companies paying dividends and with sustainable competitive advantages, such as firms with products or services that are better than competitors.

China accounts for its biggest country weighting, at 39.7%, followed by Taiwan, which comprises 19.3%.

Artemis Monthly Distribution

The mixed-asset fund paying a monthly income typically has 60% in shares and 40% in bonds.

It is managed by four experienced specialists. Jacob de Tusch-Lec and James Davidson are responsible for managing the equity part of the portfolio, co-ordinating with Jack Holmes and David Ennett who manage the bond exposure.

The fund focuses on “attractive valuation and income characteristics, diversified beyond the ‘usual suspects’ often held by competitors”.

The strategy has a strong track record, ranking in the top quartile of the IA Mixed Investment 20-60% Shares peer group over one, three, five and 10 years.

Royal London Global Bond Opportunities

Investing in under-researched parts of the market, including unrated bonds, this fund’s been a solid performer across multiple time periods.

It can invest across a broad spectrum of global fixed income, encompassing investment grade (those deemed “high quality”), sub-investment grade and unrated bonds, which helps to mitigate risk while providing considerable opportunities. The combined exposure to high yield and unrated bonds is considerable, sitting at just over 60%.

It is managed by the experienced duo of Rachid Semaoune and Eric Holt.

Jupiter Strategic Bond

This is a “go anywhere” fund, meaning the managers can seek out the best opportunities within the global bond universe while carefully managing downside risk.

Bonds are picked based on the managers’ view of the global economy, with them assessing how much risk it is appropriate to take, deciding which sectors and countries offer the best opportunities, and considering factors such as inflation, interest rates and economic growth.

The fund is managed by the highly experienced Ariel Bezalel since inception in June 2008, alongside Harry Richards, who has been a manager on the fund since 2019 and joined the firm in 2011.

Purpose of the portfolio

The hypothetical portfolio aims to show DIY investors how they can build their own diversified income portfolios alongside wider research.

The funds are chosen on the basis that over the medium to long term they would be expected to grow both capital and income. However, there are no guarantees these aims will be achieved.

Moreover, it’s important to be mindful of the fact that overall total returns (capital and income combined) can decline, especially in the short term.

Bear in mind that funds must distribute all the income generated each year. Therefore, when income dries up, as it did in 2020 when the Covid-19 pandemic emerged, a dividend cut is pretty much inevitable.

Investment trusts, on the other hand, can hold back up to 15% of dividends received each year, which means they can build up a reserve to bolster payouts in leaner years.