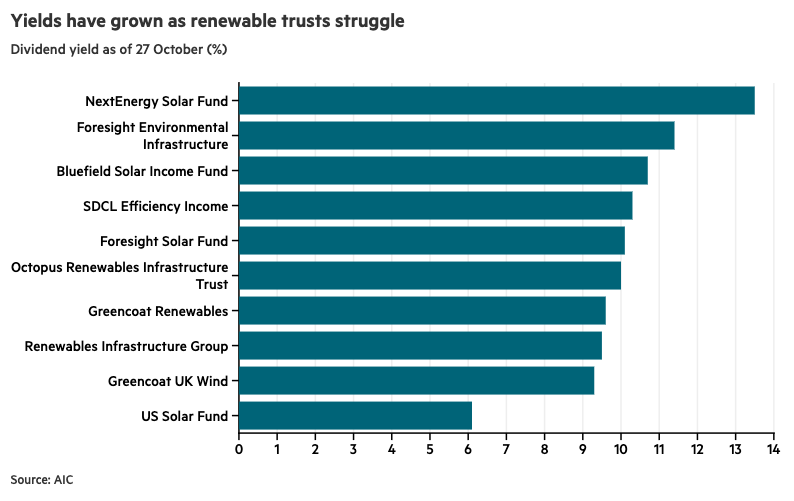

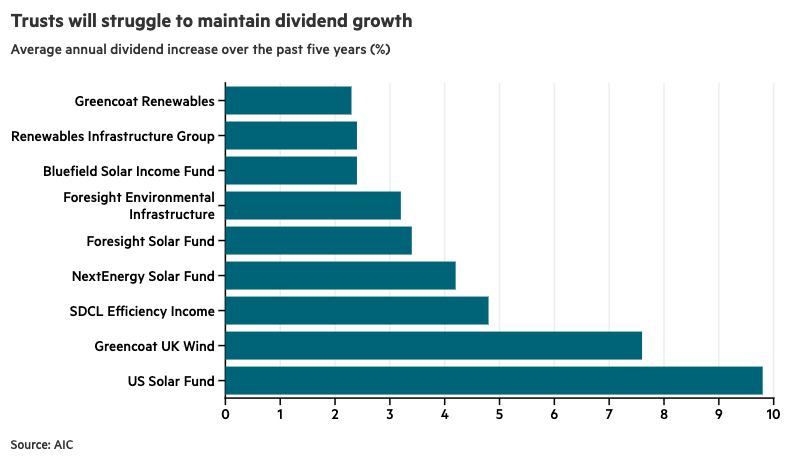

| Everything has a limit, however, and now there is a growing sense of unease about whether these payouts can continue. Wind generation has been lower than average this year, which is impacting dividend cover, defined as how many times a trust can pay its dividend from its revenue. Anything close to or under one means alarm bells. Some trusts are faring better than others, depending on their revenue mix and individual features. But Stifel analysts estimate that at Greencoat Renewables (GRP), dividend cover for the second half of 2025 will be around 0.9 times. And the Renewables Infrastructure Group (TRIG) said in August that covering the dividend for 2025 “may be tight”. Overall, Stifel analysts believe it’s “likely” that wind asset trusts’ revenues in the second half of the year will not cover expected dividends. Wind is not the only issue. For example, Stifel also expressed concerns around dividend cover at energy efficiency play SDCL Efficiency Income Trust (SEIT), where it is currently 1 times, which leaves “little room for budgets to be missed”. What’s that ringing noise ? Falling dividend cover does not automatically imply dividend cuts; trusts can use reserves to meet their obligations, and indeed have done so in the past. “Over the next couple of years, and absent a strategic change in direction, dividend cover will decline as historic power price hedges roll off – but I don’t expect to see dividend cuts,” says Charles Murphy, senior research analyst at Singer Capital Markets. James Carthew, head of investment companies at QuotedData, sounds slightly less confident, noting that it’s just very hard to tell. He points to power price forecasts that keep getting cut, despite growing demand for electricity (for example, because of data centres). Both point out that there is also a long-term question which will come to a head in the next decade or so. Renewable energy trusts need to refresh their assets, or NAVs will continue to decline, but while trading at a discount, they don’t have the capital to do so. “Longer term, I believe that dividend cuts are inevitable,” says Murphy. “Historically, the thinking was that nominal power prices would have risen sufficiently to cover the shortfall from the loss of subsidy and government support. However, the power price forecasts (in real terms) continue to decline, undermining this.” One trust where a cut is a real possibility is Bluefield Solar Income (BSIF). After trying and failing to sell its portfolio, the trust is now proposing an “integrated business model”, which would incorporate the trust’s assets with its investment manager, Bluefield. There isn’t a lot of information on how this will work yet, but it would likely involve a trade-off: more scope for future growth in exchange for a lower dividend in the short term. Carthew notes that over the next few years, it might make more sense for trusts to consider a more radical solution, as Bluefield Solar has done, rather than simply trim payouts. But whether trusts and shareholders agree remains to be seen, and there are questions over whether Bluefield Solar’s plan is feasible. So while the renewables sector remains cheap and somewhat interesting, income investors should be aware that regular payouts are not as watertight as history suggests. At the very least, the real value might decline. In recent years, not all trusts have managed to increase their dividends in line with inflation, and Greencoat UK Wind (UKW) is the only one that explicitly aims to do so. Even if inflation falls back, it might become harder to keep up. |

Leave a Reply