RGL-room

Review of the FY25 accounts at Regional REIT

Mar 25, 2026

Dear reader,

As previously discussed the overall narrative for Regional REIT ticker RGL’s 2025 is one of strategic repositioning: The company aggressively sold assets to lower debt and is now shifting toward a “Capex-led” growth strategy to upgrade its remaining portfolio.

MEES-ir’s called JaJa Binks

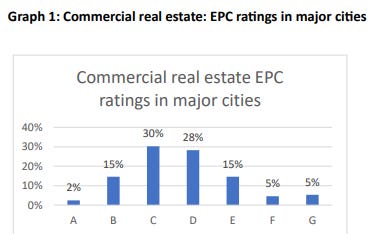

MEES is Minimum Energy Efficiency Standard regulations which forces UK landlords to meet EPC standards.

RGL’s Focus: 84.4% of RGL’s portfolio is now rated EPC C or better, with 60% at EPC B or better. This is a critical metric as net zero environmental regulations tighten for UK commercial landlords.

Is the market giving even £1 of credit to that? Nope.

1. The “EPC E” Floor (Current Law)

Since 2023, it has been unlawful for a landlord to continue letting a commercial property with an EPC rating of F or G. Any business (from a local law firm to a global tech giant) can technically contract an office that is EPC E, D, or C, on the understanding that one day they’ll need to move out or face a building refurb.

2. The “EPC B” Cliff (The Future Risk)

While this is not yet set in stone we all know the current government are determined to drive forward energy reductions so the MEES “target” whilst not legislatively set in stone and besides common sense for buyers too:

- By 2028: All commercial let property must be at least EPC C.

- By 2030: All commercial let property must be at least EPC B.

3. According to the British Property Federation:

- 53% of RGL’s competitors are non-compliant by 2028.

- 83% of RGL’s competitors are non-compliant by 2030.

Yes, a future alternative government might overturn this legislation and Labour might delay on this but a higher EPC equals a lower cost, typically.

So yes, 53% of landlords might stump up the cash in the next 21 months to get to EPC C to avoid becoming non-compliant, but then again they might not. After all they probably face the same difficult market that RGL has faced, don’t you think?

If RGL loses 50%-80% of competition then that places it in a very strong position.

EPC D or below properties probably excludes them from increasing numbers of office renters. Haven’t you spotted how energy bills are going up in 2026? A lot.

RGL tell us that “Demand for quality office space has put an upward pressure on rents, with growth of 4.8% recorded across the Big Nine regional markets in 2025. According to research from Avison Young, average headline rents are now approximately £40.72 per sq. ft.”

Wow! £40.72 is quite a bit higher than RGL’s average of £14.20 per sq. ft. isn’t it?

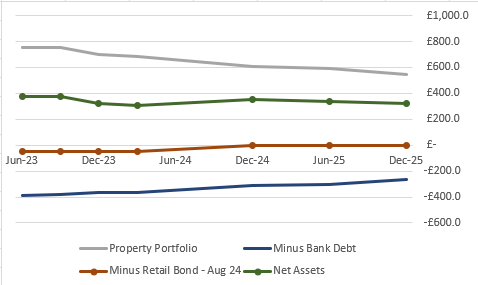

Steady NAV, falling debt

Interesting to see RGL’s NAV (in green) is flat over the past two years but the debt is much reduced (blue and red lines), along with a reduced property portfolio (grey). There’s zero recognition for this achievement in the share price. It is priced based on a cliff edge of debt that isn’t there today.

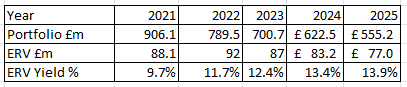

- Portfolio Valuation: £555.2 million (down 5.0% on a like-for-like basis from £622.5m in 2024). This decline was primarily driven by income changes and tenant breaks rather than drops in valuation.

- Dividends: 2026 Target: 8.0p per share. The Board is adopting a more conservative pay-out to retain cash for property upgrades.

- Loan-to-Value (LTV): Reduced to 40.4% (and further to 39.9% post-period end), down from 41.8% in 2024.

- Rent Collection: Remained exceptionally high at 99.1% with bad debt almost non existent.

- The contracted rents for the coming two years account for 55%-60% of 2025’s rent roll. Good to see. That also implies quite a few lease renewals are going through in 2026 doesn’t it?

- Based on the current performance of 17% above ERV and 12.8% of income renewals in 2026 that implies an additional £11.6m of rents. If the voids reduce then we get closer to the 2025 rental number of £60.4m, or otherwise that’s why we’re seeing a 90% of rental earnings policy instead of a fixed pence per share policy – as previously. But that’s a short term bump to income that actually translates to higher long-term rates as higher rentals come on board to 12% per year of the portfolio.

Does that mean lower rentals in 2026? Possible but not necessarily.

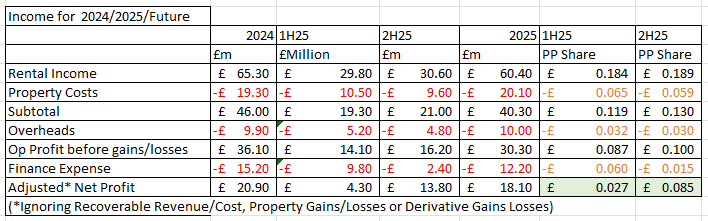

Interesting to see rental income accelerated in 2H25: Operating profit equated to 8.7p in 1H25 and 10p in 2H25, thanks to higher rental income, lower property costs and overheads.

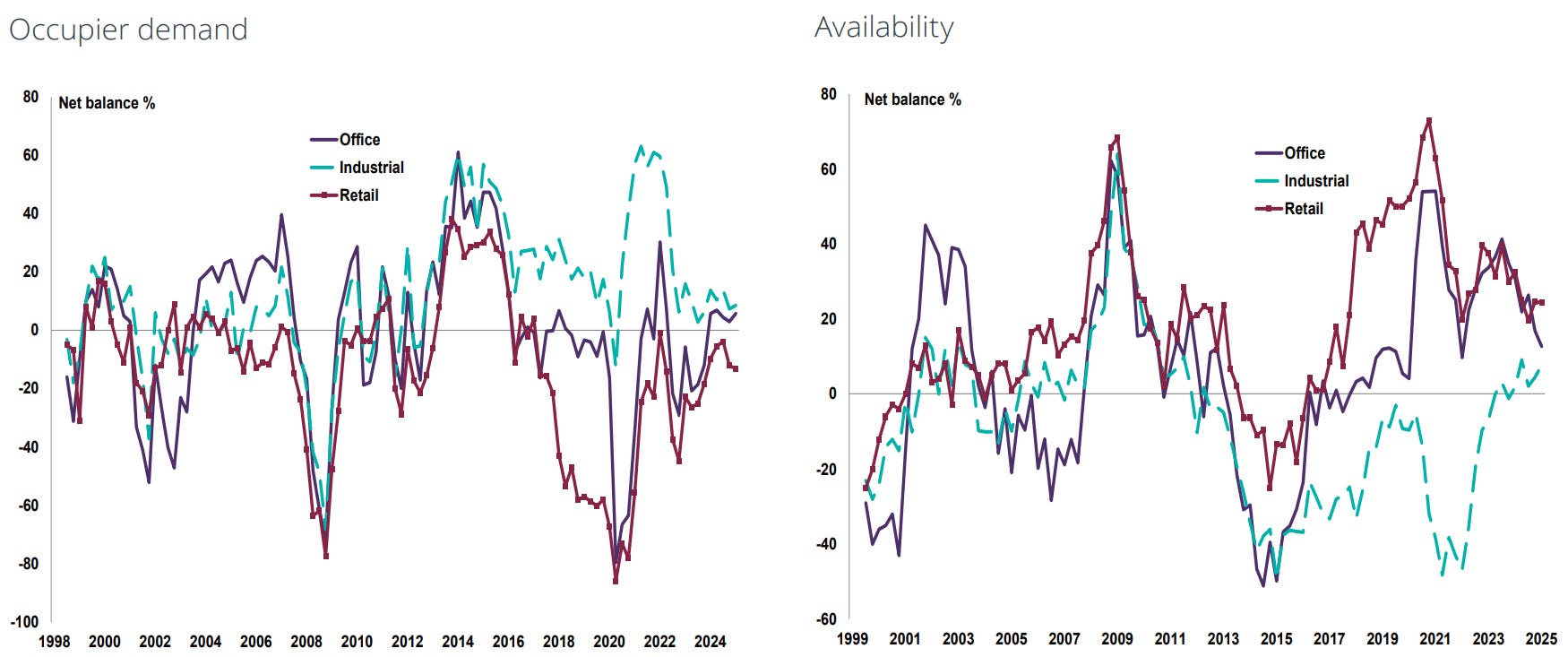

This 1Q26 RICS survey shows offices in blue where demand is rising and availability is falling.

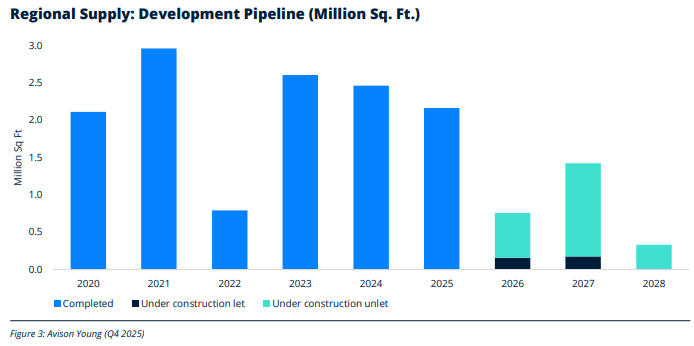

The RICS finding is mirrored when you considered the forward pipeline of new office builds is pitiful. The Building Safety Act and various onerous planning costs as well as still-high interest rates and finance costs make new builds deeply unattractive.

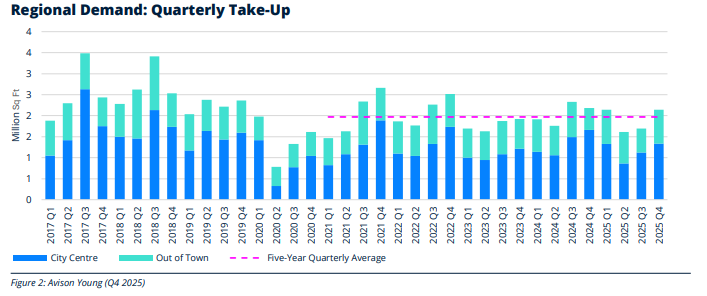

This constrained supply is smashing into a fairly steady 2m Sq.Ft of demand. Moreover the Business Rates revaluation is likely to drive more businesses outside the M25 – and into the waiting arms of RGL.

Build costs are simply too high to justify adding supply at current prices.

In fact what clearer evidence is there than post period lettings are averaging 17% above ERV (estimated rental value). Does that not make you slightly say Wow? Extrapolating that percentage to the £77m ERV gets you to a £90m per annum ERV. Compared with a £148m market cap?

The ERV as I’ve previously reported has been increasing and hit 13.9% in 2025. The 17% above i.e. £90m would take this to a 16.2% yield.

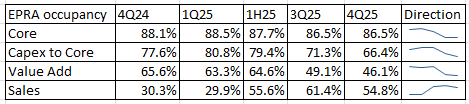

RGL isn’t yet achieving £77m ERV, let alone £90m, but its trajectory is inching towards there. 62.9% of the portfolio were core in 4Q25 up from 58.4% in 1H25, so while the EPRA occupancy is “static” the proportion that fall under the 86.5% occupancy is increasing.

Post Period:

Think this in addition to the new rentals on average 17% above ERV tells you what you need to know post period: Disposals continue ABOVE book value.

There are £12.3m disposals post period, reducing debt by £7.8m so “another £50m” reduction is on target pro rata.

Conclusion

I didn’t really expect the annual report to throw up lots of further insights beyond those already shared in the trading update. The presentation should add further insights but even just the annual report shows RGL is well positioned in the market and probably at a low point so despite a weak share price YTD this is – in my opinion – an owner of interesting and increasingly valuable assets.

Regards

The Oak Bloke

Disclaimers:

This is not advice – you make your own investment decisions.

Micro cap and Nano cap holdings including REITs might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip”.

Leave a Reply