One in particular, the Royal London Short Term Money Market fund has been one of the most-bought funds for every month this year. So what are money market funds? Well, they’re effectively a cash savings account that you can own in an investment wrapper. So your General Investment Account, your ISA, or your SIP, and you’re paying a normally very low fee, can be 0.1% a year for a professional fund manager to deliver a cash like return for you.

Bull points

Returns around the current bank rate.

Tax free if held inside a tax free account.

Income either paid Monthly or an Accumulation unit available.

Bear points

Being a Unit Trust it only trades at noon, so a small wait for funds to be credited to your account.

When interest rates fall so will the money market returns, so one option if you think rates are going to fall is to lock in the rate with a Gilt purchase.

If held outside a tax free wrapper, easiest if the monthly income option is bought as there is a rather convoluted tax calculation for the accumulation unit.

Key trends and top-performing funds so far in 2025

Our latest episode runs through key trends and reveals the best-performing funds and sectors so far in 2025.

2nd July 2025

by the interactive investor team from interactive investor

We’re halfway through the year and for investors it has been very eventful. This week’s episode takes a look back at key trends that have played out so far. Joining Kyle to help unpick it all is interactive investor’s Sam Benstead. The duo give their take on the investment lessons from the US tariffs causing stock markets to slump in the first quarter, talk through trends within the funds industry, and crunch the numbers to reveal the best-performing funds and sectors year-to-date.

Kyle Caldwell, funds and investment education editor at interactive investor: Hello, and welcome to the latest episode of On the Money, a weekly bite sized show that aims to help you get the most out of your savings and investments. We’re now at the halfway point of the year, so this week’s episode is taking a look back at the key trends that have played out so far in 2025. We’re going to be looking at the investment lessons that were learned from the tariff turmoil that caused stock markets to sell off earlier this year, and we’ve also crunched numbers to look at the top performing funds and sectors year to date. And all that data is to the time of this recording, which is on the 27th June.

Joining me to unpick all of this is interactive investor’s Sam Benstead. Alongside myself, Sam regularly interviews fund managers and writes lots of news analysis articles related to funds, investment trusts and ETFs. So, Sam, let’s start off with tariffs, which have dominated the headlines. They caused stock markets to become more volatile, particularly in the first quarter this year. Let’s take a step back. Could you give an overview of why US President Donald Trump’s tariff policies caused the US stock market and by extension the global stock market to suffer sharp falls from around mid-February to 8th April? And could you also detail the extent to which both US and global markets fell over that period?

Sam Benstead, fixed income lead at interactive investor: So the real key period was between 19th February and 8th April. And what started out as lots of optimism when Donald Trump was elected for the second time, quite quickly turned into pessimism when investors realised that his pre-election promises of tariffs were actually probably going to come true and could be way worse than investors were anticipating. So we had this big build up to what he called Liberation Day on the 2nd April, and people were expecting relatively modest modest tariffs. But what they got was a big presentation with lots of graphics on high tariffs on almost every country in the world.

And if actually Donald Trump went through with these, it would have caused a really deep global recession and would have been a massive shock to stock and bond markets around the world. So during that key period from the 19th February to the 8th April, the S&P 500 dropped -19%, the Nasdaq composite dropped -24%. UK shares fell about -10% over that period, so they were relatively well protected versus the US. And we had this capitulation on that key week on Wednesday, Thursday, Friday when the Liberation Day tariffs were announced. That caused a really key moment in bond markets when actually investors went from buying bonds causing yields to fall to suddenly dumping US bonds and causing US bond yields to rise, which of course increases the cost of the government deficit in The United States. And at the same time, we had an unusual environment where, actually, the US dollar was falling at the same time that bond yields were rising, which is actually pretty typical of an emerging market confidence crisis where everybody just wants to get their money out of that market.

But things, turned quite quickly when the bond market was collapsing. I think it was the influence of the Treasury Secretary Scott Bessent that actually, you know, made him whisper in Trump’s ear saying, this is a bit too much. Things are getting very panicky. This is not good news at all. And Trump actually announced a ninety day pause in tariffs, which sparked a huge reversal in the stock market losses.

And, actually, if you now look back at the year-to-date, you hardly know anything happened during those critical few months in in February, March and April. The S&P 500 in dollar terms is up 5% this year. The FTSE All Share, excluding dividends, is up 6%. But, actually, your portfolio might not look quite so rosy because the dollar is down -9% against the UK pound. So that means if that that if you own US assets via an index fund tracking the S&P 500 or a global stock market fund, which is 70% invested in the US, you are still not back to even quite yet.

Kyle Caldwell: And as you mentioned, Sam, what sparked that market recovery was Donald Trump announcing a ninety-day delay on implementing tariffs for most countries. And then following on from that, we had The US and China announced the reduction in the tariffs that they were imposing on each other. And, of course, we also had the US/UK trade deal. A key lesson for me, Sam, during that tariff turmoil was the power of diversification. Over that period, if you owned a mixture of different investment types, both shares and bonds, your portfolio was typically well protected against the stock market volatility.

So if you look at the performance of multi-asset funds year-to-date, so funds that sit in the 0% to 35% Shares sector, which is the safest of the multi-asset sectors. The average fund is up 2.4% year-to-date. And if you are willing to take a bit more risk, the average fund in the Mixed Investments 20% to 60% Shares sector is up 2.9%. So this shows to me that bonds worked very well as a defensive ballast during that turmoil. And if you were patient and held on, then year-to-date, you are in positive territory if you had a mixed investment approach.

Sam Benstead: Yeah. And I think these these difficult market periods, any 20% drop, in theory, you might think you can withstand that psychologically. But, if you have all of your all of your wealth and your pension and your your ISA and you see a big 20% drawdown it may be much more painful than you think. So having a spread of of of different assets and outsourcing that to a fund manager is a very sensible decision. And if you’re investing in a fund run by someone else, you actually should have confidence they are going to protect you be invested sensibly rather than picking everything yourself where you can own all that all those decisions and you see your decisions actually leading to a stock market drop, that can be quite a difficult thing to go through.

Another key takeaway for me was that money market funds actually were a very sensible place to be invested, and we’ve seen money market funds really rise in popularity this year. One in particular, the Royal London Short Term Money Market fund has been one of the most-bought funds for every month this year. So what are money market funds? Well, they’re effectively a cash savings account that you can own in an investment wrapper. So your General Investment Account, your ISA, or your SIP, and you’re paying a normally very low fee, can be 0.1% a year for a professional fund manager to deliver a cash like return for you.

And to do this, they invest in ultra safe short-term bonds maturing in just a couple of months. They also put money away with banks and overnight deposit tools and generally have access to lots of ultra safe money market instruments to generate a return on your behalf. And returns are typically in line with the Bank of England base rates. So because of that, about halfway through the year, money market funds are up just over 2%, which makes sense given that the Bank of England interest interest rate has been 4.5% this year until a couple of months ago. If you look at that in the context of inflation, inflation has been about 3% this year, so you are getting a positive real return.

I interviewed fund managers managing money market funds during all the tariff tension and when stock market is in bond markets were falling. And they said there’s been no impact on money market instruments. It’s been business as usual, no volatility, and they’re just delivering that safe return for you. So holding cash in account has been a very good tool against stock and bond markets falling as you would expect, and yields have been ahead of the inflation rate this year.

Kyle Caldwell: And as well as money market funds, other defensive investment types performed well during the tad of turmoil. Well, I say they perform well, they performed as one would expect and hope that they would. We often talk about the trio of wealth preservation investment trusts, which are Capital Gearing Ord

and Ruffer Investment Company RICA0.00%. All three of them did fulfil their mandate of protecting capital during that period that we just spoke about from mid-February to 8th April.

However, star of the show has been gold, which we will come onto later on in the podcast, as spoiler alert it has been gold funds that have dominated the top-performing funds in the first half of this year. But before we get to that, we will turn our attention to a couple of trends and themes we’ve spotted in the first half of this year. The first one is the defence sector. So we’ve seen investors up exposure to defence as a geopolitical hedge.

And another factor at play is that some investors have been viewing the increases in European defence spending as a potential opportunity. It’s a sector that’s been running hot. So, for example, Germany’s biggest weapons maker, Rheinmetall, has seen its share price soar by nearly 200% since the start of the year. We’ve seen among customers of interactive investor, Sam, two defence-focused ETFs climb up the popularity rankings. Could you talk through them?

Sam Benstead: Yeah, of course. So, actually, I identified four ETFs tracking the defence sector with a couple launching more than a year ago and two launching this year. So the ones for the full 2025 record are HANetf’s Future of Defence ETF Acc

and both are up more than 20% since launch. So amazing returns from the sector. And as always, an ETF is a very efficient way of getting access to a theme without having to do your own stock market research. And I’m normally sceptical of ETFs when they launch, particularly thematic ETFs because there’s generally a hype cycle. The big fund managers get on board with this. They see demand for a product, and then they launch it. And, actually, by the time they they’ve launched a product, often it’s too late and you see a bit of a drop in the ETF before before the theme comes back around again. But this time around, think the defence theme has much further to go. We had a NATO summit this week, and all the NATO members announced big increases in in spending on defence. And there’s only a limited number of defence companies out there, so naturally all this capital go goes into those companies.

And before this boom over the past couple of years, they were super, super cheap as well. No one wanted to own these shares. So even though we’ve seen this big run up, fund managers have been telling me that actually these companies still look good value. And if all this spending actually comes to fruition, it should be extremely good for these companies still. One of those was Alec Cutler at Orbis, who’s a very savvy value investor, and he started buying defence shares a few years ago. And he told me recently that actually he still likes the sector and it still has further to run.

Kyle Caldwell: So that’s certainly been a trend within the ETF space. Now let’s switch to investment trust trends. So it has been a very eventful six months for the investment trust industry. US activist investor, Saba Capital, attempted to oust the boards of seven investment trusts early this year. Now while it wasn’t successful in its campaign, it has had success elsewhere as Middlefield Canadian Income Ord

has proposed converting into an ETF or offering shareholders an exit close to the value of its investments, which is the net asset value, NAV.

Now the reason why Saba has circled the investment trust industry is due to the fact that investment trust discounts are at historically wide levels, and they’ve been at those wide levels for a couple of years now ever since interest rates rose and peaked at 5.25%. This has lowered demand for investment trusts. And as a result, lots of investment trusts are trading on discounts, and the average investment trust discount is over 10%, and it has been like that for a couple of years as I’ve just mentioned. Now while Saba wasn’t successful in its campaign, four of the seven trusts that it did target made changes. So some of them have merged with open-ended funds, some have announced tender offers, which give shareholders the opportunity to exit at close to NAV, which in effect removes the discounts that the investment trust are trading on for those investors. So it could be argued that, actually, Saba has been successful in its campaign because boards have introduced those measures, given shareholders an opportunity to exit at a better price rather than seeing their investments languish on a stubbornly wide discount.

Sam Benstead: It’s been such an interesting thing to watch play out this year. You’ve been you’ve seen this big American activist hedge fund go on the attack against relatively sleepy, archaic part of the investment world where a lot of these boards can potentially be accused of being a bit lazy and not doing enough to close discounts. And I think the impact overall for shareholders has has been brilliant. It’s shaken it up.

We’ve seen lots of discounts narrow. And, you know, if you were if you were sitting in one of these investment trusts, you’ve now got the option to get out at at NAV. I think that’s been a very good option. And, of course, you don’t have to take up that right, and you can hold on to the shares. But, generally, I think it’s been a good thing, and I don’t think it’s over yet as well. I think we’ll see Saba come out with some more high profile attacks on investment trusts.

One of the other trends we’ve seen this year in the investment trust world is scale becoming more and more important for boards. There were a couple of recent mergers announced in the European investment trust sector with the proposed combination of Henderson European Trust Ord

So as you mentioned, Kyle, the fact that investment trust discounts have been stubbornly wide for a couple of years now is prompting boards to become more and more proactive to try and increase demands. Ultimately, the bigger the investment trust, the greater the chance of higher demand due to the likelihood of it being on the radar of both retail investors and wealth managers. And for wealth managers, this is particularly important as the minimum size they tend to look at is £300 million for an investment trust due to the amount of money that they run on behalf of clients. Basically, if they are large investors, they cannot commit a large sum of money to investment trusts with a smaller amount of assets for liquidity reasons as it can prove problematic to sell a large sum when investment trust is less popular and not seeing much demand.

Kyle Caldwell: I can only see these trends accelerating over the next couple of years. I think scale will become more even more important for boards. At the moment, for wealth managers the minimum size they tend to look for investment trust is around £300 million. Over time, that will likely increase, in turn putting pressure on the more potentially subscale investment trusts. For a retail investor, that doesn’t mean that you can’t consider investment trusts that got £100 million or £200 million of assets. And in some cases, some may be potentially hidden gems. However, one thing that I’d look out for is the bid offer spread when it comes to size because for smaller investment trusts the bid offer spread can be, on occasion, quite wide. So that’s something retail investors should bear in mind and take a look at when they’re doing their wider research.

Let’s now turn to the best-performing funds and fund sectors since the start of the year. Let’s focus on sectors first. So, Sam, I I ran the numbers. And at the time of this recording, As I mentioned earlier 27th June, the top five overall sectors and their performances are Latin America, the average fund is up 15.8%, followed by European Smaller Companies, the average fund is up 13.2%. Then it is Europe excluding the UK, up 11.6%, then Europe including the UK, with the average fund up 9.6%. And then in fifth is UK Equity Income in which the average fund is up 8.2%.

Sam, are you surprised to see Latin American funds in top position? It’s, of course, a very specialist fund sector. It’s very high risk. I don’t think many investors will have much exposure to it. And if they do have exposure to it, it should ideally be a small amount of exposure as part of a well diversified portfolio. Can you put your finger on the reasons as to why it has performed so well?

Sam Benstead:Yes, I was also surprised to see Latin America there. It’s not a sector I’ve read much about this year, and it’s also a bit of a yo-yo sector. It can have really good years followed by really poor years. Like you say, only really worth a small allocation unless you have a really strong view on the investment sector.

But I did some digging, and there are a few factors that stood out. So the first one, and I think this is the most important one, is that a weaker US dollar has been good for a lot of the mining and oil and gas companies that operate in Latin America. And these types of companies generally make up the lion’s share of the investment market. So a weaker dollar means that because these commodities are priced in dollars, it means they can sell more of these assets to overseas buyers. So it’s generally been good news for profits at a lot of the mining and oil and gas companies in Latin America.

And the other reason, and it’s a bit like the UK, is that there’s just been a rotation out of the US market into better value markets, and Latin America is definitely better value after a poor 2024 and a poor 2023. So, generally, this move to cheaper assets, better value shares has been good news for Latin America in the same way that it’s been good news for UK.

Kyle Caldwell: However, I wasn’t surprised to see European funds among the top-performing sectors in the first half of 2025. Europe has been performing well for the past 18 to to 36 months. While investors may find some of the sectors less exciting, for example Europe offers less technology exposure. However, these defensive areas, the likes of healthcare, financial services, defence, they’ve they’ve been performing well in a periods in which economic growth has been sluggish because they offer stable performance due to the consistent demand for their products and services. So on a three-year view, the average European fund is up 40.3%. This compares to the average return of 28.2% for the average UK equity fund.

Sam, let’s continue with the UK. While the average UK fund has underperformed the average European fund over three years, we have seen an upturn in performance of late for the UK. The UK Equity Income sector was the fifth best-performing sector in the first half of 2025. Sam, what have been the key performance drivers for UK funds?

Sam Benstead: So for me, the biggest driver of returns has been that value shares are back in fashion. So investors are taking money out of the pricey US market and looking at better value opportunities, particularly in Europe and in the UK. As the UK market has been cheap, there’s lots of great value opportunities there, and that has been boosting share prices. But while shares have been cheap and that’s been attracting assets, the market is still very underpriced versus the US. I think there’s going to be continued demand for UK shares for that reason. You’ve also got a pretty punchy dividend yield on The UK FTSE All Share at about 3.5%.

So in a world of really high geopolitical uncertainty and volatility, getting that dividend yield has also been appealing to investors. I think another thing that stands out about the UK market is that we’re quite insulated from trade wars with the US. So we have this UK/US trade deal. Generally, relations are quite strong. And also The UK market isn’t full of complex multinational manufacturing companies similar to Apple in the US or car companies across Europe.

So, actually, if we do see a big turndown in global trade, the UK market could look quite competitive in that environment. Will this continue? I recently wrote a story for our website on ‘three reasons the UK outperformance can continue’ and brought in a few views from leading UK value investment managers. Their view is that, yes, the UK market is still cheap. As well as, this installation from trade wars is a good thing for the market. And the final thing they said is that actually global investors are seeing this opportunity and flows coming back into The UK will be good news for share prices.

Kyle Caldwell: And in terms of the worst-performing fund sectors, the bottom three are North American Smaller Companies, the average fund is down -11.7%. Then Health care, the average fund is down -10%. And then the India/Indian subcontinent sector in which the average fund is down -7.2%.

North American Smaller Companies being the worst-performing sector is not much of a surprise. If you invest in smaller companies, they can, of course, offer greater rewards compared with larger firms, but they do carry greater risk. When there’s a downturn, smaller company shares do tend to fall further, and so it proved in the first half of this year when there was a pickup in stock market volatility. There was also quite a lot of expectations that US domestic stocks would perform well with Donald Trump returning to the White House. The expectation was that Trump’s American first policy would boost the demand for domestic stocks and The US economy. However, this has not played out so far, and I think that also has played into the fact that North American Smaller Company funds have had a tough time in the first six months of 2025.

Let’s now turn to the best-performing funds in the first half of the year. Sam, I did mention earlier, I gave it away, gold funds have stood out as the best performers. Could you run through some of the fund names and explain why gold continues to shine?

Sam Benstead: So definitely, let let’s start with the gold price. So it started the year at $2,625 per ounce. It’s now at nearly $3,300 an ounce. So that’s a 25% increase in US dollar terms this year. And and why is gold rising?I think there’s two main reasons. The first one is what you would expect. So we’ve had a lot of worry in markets this year, trade tensions, war The Middle East. As gold is a proven hedge against uncertainty, it often rises when investors are afraid.

But that’s just one part of the story. I think the most important part actually is this idea that government deficits are rising. Inflation is still quite high. There’s lots of spending being announced by governments, lots of borrowing, and all this just means that there’s an increased money supply, an increased supply of dollars, an increased supply of pounds swirling around the economy. And, actually, that’s just a reason for inflation to be longer for higher. And in a time of inflation, what you really want is a fixed asset where the supply isn’t going to increase, and gold is the thing that investors turn to during those times. So because they’re worried about the money supply rising, gold being fixed in supply is rising versus fiat currencies. So that, I think, has been behind the rise in the gold price this year.

But if you dig into the data, gold price up about 25%, but gold miners has to have done even better. So it’s funds that have been investing in gold miners that have done incredibly well this year. So what are the risks and opportunities with gold miners? Well, for me, they can just be viewed as a levered bet on gold. So a rising or falling gold price leads to big swings in the profits or losses at these gold miners. There’s also a few other things to be aware of when when investing in gold miners. So there’s the risk that managements do something very positive or very negative at a specific company. Companies can find new reserves, which can be a boon for profits, but also gold mines can get caught up in local issues around mines, particularly in the emerging world. So this also increases the risk and opportunity of gold miners over gold.

And in terms of funds that invest in gold miners that have done really well this year, so I’ll just name three of them, the top three in terms of returns year-to-date. And at number one is the SVS Baker Steel Gold & Precious Metals fund, which is up 52% this year. Then Hanetf AuAg Gold Mining, an ETF with stock market ticker ESGP, is up 49% this year, while the Jupiter Gold & Silver fund is up 47%.

Among the other top performers, there are a few other thematic funds. I think this is typical really. So when funds track a niche theme, it’s often boom or bust because they’re very concentrated bets on a specific type of the stock market. So alongside all these gold names, we’ve seen funds investing in banks, defence, Polish shares, and Korean stocks do well this year.

Kyle Caldwell: And for investors that have not had exposure to gold and now have FOMO and are thinking about having some exposure now, there’s, of course, always the danger of buying in potentially at the peak after a strong run. What are your thoughts, Sam? Is it now too late to join the gold party?

Sam Benstead: I don’t think so, but there’s a risk of trying to make a short-term bets on the price of a metal. But if you think, actually, I like the story of gold. I like this idea that it holds its value when normal currencies do not, and you want to to add a long term allocation portfolio, say three or 4%, I I don’t think now is a bad time to try and make that decision as long as you’re investing for the long term and not looking to make a short term profit. So how would you do that? There’s the gold mining funds, which as I explained, are a bit riskier, but actually, I think the most I think the purest way of adding to gold to a portfolio is to do it with an ETF that is backed by physical gold. So one of those features on our Super 60 list, and that’s the iShares Physical Gold ETC, stock market ticker SGLN. That I would say is the best way of doing it. Try and keep the allocation fixed. So actually, if you see gold go up a lot, you might want to trim to try and keep that allocation at 3% or 4%. If gold is falling a lot, then actually you might want to buy more to try and get that allocation at your desired amount.

Reinvesting dividends: why it could leave you thousands better off

Dividend paying companies in your portfolio can provide a reliable income but potentially millions of investors are missing out on thousands of pounds by not reinvesting dividends,

Dividend paying companies in your portfolio can provide a reliable income but potentially millions of investors are missing out on thousands of pounds by not reinvesting dividends

(Image credit: Cristina Gaidau)

By Laura Miller

Reinvesting dividends offers a sure-fire way to boost your returns and increase your chances of outsized gains from your investments over the longer term. But many investors are missing out when picking top stocks and funds to invest in.

Dividends are payments made by a company to its shareholders, representing a portion of the company’s profits. They are a way for companies to share their success with investors and can be paid out in cash or additional shares of stock.

Investors keen not to disturb their capital and to keep it growing, often draw down just the dividends, creaming those extra payments off the top of their fund for an income, especially in retirement as part of a pension. Some investment funds are designed for investors to take dividend income this way.

Get 6 issues for £1 + a free notebook

Stay ahead of the curve with MoneyWeek magazine and enjoy the latest financial news and expert analysis.

But while dividend-bearing investments are particularly important for income seekers, long-term academic studies on the returns from UK equities have proven that they overwhelmingly account for most of the real return (after inflation) of the UK stock market.

Jason Hollands, managing director at wealth manager Evelyn Partners, said: “Where dividends are reinvested, rather than taken, this creates a very powerful compounding effect.

Latest Videos From Moneyweek

“This means investors benefit not just from the returns on the original cash invested, but also the returns on the gains made on the dividends which are ploughed back into further share purchases.”

Reinvesting FTSE 100 dividends

Over the last forty years, the FTSE 100 has made a capital return of 391%. This is equal to 205% in real terms – meaning after inflation – as the UK consumer price index inflation rose 186% over this period, by Evelyn Partners’ calculations.

But with UK dividends reinvested the total return is a far more impressive 1,926%.

Hollands said: “While it can be nice to see ad hoc dividend income appear in your bank account, if you don’t need the income now, it is far better to opt for a dividend reinvestment scheme.

“Or, if you are a fund investor, to choose ‘accumulation’ shares classes where any income from the fund portfolio is automatically rolled up rather than distributed.”

Tom Stevenson, investment director at Fidelity International, said a myth has built up that the FTSE 100 has been a serial underperformer: “And when you look only at the headline index level, it’s not hard to see why.”

The UK’s blue-chip index peaked at 6,930 right at the end of the last century, literally on New Year’s Eve 1999. It didn’t get back to that level until February 2015 and then took another nine years to finally make it to 8,000. It’s been a long hard slog.

“But when you factor in the relatively high dividend yield on UK shares, often above 4%, the total return from UK shares starts to look a great deal more interesting,” he pointed out.

Reinvesting dividends meant that the FTSE 100 got back to its 1999 high much more quickly – by February 2006 rather than February 2015. Today the total return index stands more than three times higher than at the peak of the dot.com bubble, said Stevenson.

Missing out on dividend reinvesting

Millions of investors could be missing out on thousands of pounds each, however, by failing to reinvest their dividends, according to Aberdeen Asset Management dividend research.

According to Aberdeen’s findings, 42% of UK investors either said ‘no’ or ‘don’t know’ when asked if they are reinvesting their dividends – equal to 7.5 million investors in the UK.

Analysis by Aberdeen looked at nine major markets over a ten-year period to the end of February 2025 and the impact of reinvesting dividends on returns if an investor had started with a £10,000 lump sum investment.

The biggest difference between total return (reinvesting dividends) versus capital return (not reinvesting dividends) was seen in the Dow Jones Index. It delivered £37,016 on a total return basis over 10 years. This compares to £29,651 on a capital return basis – a difference of £7,365 over 10 years.

Some may be surprised to see the Dow Jones Index lead here given the US is not typically associated with dividends. But that just shows the power of the compounding effect and its impact on the higher total return on the index’s performance.

Because while the S&P 500 delivered the largest total return on £10,00 invested over 10 years – at £41,485 versus £34,699 on a capital return basis – the difference between capital and total return was smaller at £6,786.

The FTSE World Index came third, at £32,002 returns on a total return basis compared to £25,439 on a capital return basis; a difference of £6,563.

The difference was most stark when looking at the AIM market. AIM only delivered positive returns after 10 years, and that was only on a total return basis i.e. when dividends were reinvested, returning £11,335 versus £9,851 when dividends weren’t reinvested.

Interestingly, the FTSE100, often famed for its dividends, came in at number five in Aberdeen’s analysis. Over 10 years it provided a total return of £18,548 versus £12,682 on a capital return basis; a difference of £ 5,866.

Ben Ritchie, head of developed market equities at Aberdeen, said: “Reinvesting dividends is key to long-term returns. While the impact has been seen over the past three and five years, it’s not until ten years that the true magic of compounding really kicks in and delivers, assuming that markets are moving in the right direction – upwards.

“Many income investors rely on their regular dividends to meet their outgoings. But it is compound interest that helps get portfolios to sufficient scale so they can reap the income rewards later on.”

Index

10 year capital return

10 year total return (Dividends Reinvested)

£ difference over 10 years (amount made from total return versus capital return)

Dow Jones

29,651

37,016

7,365

S&P 500

34,699

41,485

6,786

FTSE World

25,439

32,002

6,563

MSCI Europe

15,954

22,037

6,083

FTSE 100

12,682

18,548

5,866

MSCI Emerging Markets

13,588

17,948

4,360

FTSE 250 including investment trusts

11,767

15,446

3,679

FTSE 250 excluding investment trusts

11,254

14,806

3,552

AIM

9,851

11,335

1,484

Source: Bloomberg, 28 February 2025

Picking dividend winners

As well as the powerful effect of dividend reinvestment, it is worth looking out for reliable, consistently dividend paying companies for another reason.

“A company that is able to pay a sustainable and growing dividend that is amply covered by its earnings per share can be regarded as shareholder friendly and able to generate healthy cash flows,” said Hollands.

However, some caution is also required, especially where the level of dividend yield appears “too-good-to-be true”.

“When buying shares with high dividend yields, it is important not to get dazzled by the highest headline yields without digging deeper into how well supported those payouts are by the underlying profits,” Hollands said.

Targeting higher yielding stocks can be a bit of a trap, as a very high yield can be an indication that the market does not believe the dividend payout rate is sustainable and the outlook for the business is poor, so a low share price creates the effect of a high yield.

It is much better to find companies that have the potential to grow their dividends over time, because the underlying business is performing well.

“It’s also worth pointing out that recently many companies have now adopted share buybacks alongside dividends, which can help enhance shareholder returns, so these might be considered alongside dividends,” Hollands said

Supermarket Income REIT plc (LSE: SUPR), the real estate investment trust with secure, inflation-linked, long-dated income from grocery property, has today declared an interim dividend in respect of the period from 1 April 2025 to 30 June 2025 of 1.53 pence per ordinary share (the “Fourth Quarterly Dividend”).

The Fourth Quarterly Dividend will be paid on or around 22 August 2025 as a Property Income Distribution (“PID”) in respect of the Company’s tax-exempt property rental business to shareholders on the register as at 25 July 2025. The ex-dividend date will be 24 July 2025.

The active versus passive debate has been raging for the past two decades. The biggest issue with active funds is fees. No investor should pay higher fees for sub-par performance. Still, if managers can outperform – earning their fees and then some extra – it is a good deal for investors.

However, it is difficult to dispute that passive funds beat active ones on average over the long run. The S&P Indices Versus Active (Spiva) reports from S&P Dow Jones consistently show that active funds have lagged behind relevant benchmark indices over long periods. Among US-based large-cap US equity funds, 64% have underperformed the S&P 500 over the past 24 years. In Europe, 93% of funds underperformed the S&P Europe 350 over ten years, while 82% of UK funds have lagged behind the S&P United Kingdom BMI.

The Morningstar active/passive barometer uses a slightly different approach of comparing active funds with passive funds in the same category, since this takes account of the reality that passive funds are not a perfect, cost-less replication of an benchmark index. Still, the results are very similar. Just 14.2% of active funds based in Europe beat passive strategies over the past ten years. Again, for large-cap equities, active fund performance has been particularly poor, making it “increasingly difficult to justify their higher fees”.

So the key is to find the areas where active managers still have the edge. For example, Morningstar notes that small-and mid-cap equities all saw active managers perform better: for example, 33% of managers investing in US small caps and 36% of investors in eurozone small caps beat passive peers.

This is still not a majority of funds. However, at least it suggests that investors are less likely to be wasting their time looking for an active manager who can add value here. So there is a stronger case for using active funds tactically in particular markets or sectors.

One of the latest features is the active/passive fund comparison: a daily-updated page that tracks how active funds are performing relative to their passive counterparts.

The data only currently stretches back five years, but there’s a ten-year screener in the works.

The results suggest that there is no point in investors trying to seek outperformance with an active manager in well-covered markets. For example, in the global large-cap sector, the platform has 258 active funds with a track record of five years, compared with 65 passive funds. On average, the median net total annualised return for the active funds is 8.6%, compared with 11.5% for passives.

More surprisingly, be careful in emerging markets – an area where many investors believe that active managers can readily succeed because markets are less efficient. The platform has 40 passive funds and 201 actives in the emerging markets equity category. Yet the actives have still underperformed passives by 0.17% annualised (on a median basis) over the past five years.

In the least-efficient markets, the odds may start to improve. The six active funds focusing on Africa and the Middle East have outperformed the one passive fund by 3.95% annualised over five years, on average. Active funds focusing on India have outperformed by 2% annualised, while those in frontier markets (ten active funds and two passives) have outperformed by 4.3% annualised. Similar trends can be seen in other categories that involve more small caps and in specialist markets such as biotech and alternative energy.

This article was first published in MoneyWeek’s magazine

You’ve no doubt heard pundit after pundit say that you need at least a million dollars to retire well.

Heck, we’ve all heard it so often, I bet it’s the first number most people think of when someone says “retirement savings”!

Let me explain why this endlessly repeated fallacy is dead wrong. You’ll actually need a lot less than that.

I’m talking about just $600,000. And in some parts of the country you could easily do it on less: a fully paid-for retirement for just $500,000.

Got more? Great. I’ll show you how you can retire filthy rich on your current stake.

I know that sounds ridiculous in these inflationary times, but stick with me for a few moments and I’ll walk you straight through it.

The key is my “8% Monthly Payer Portfolio,” which lets you live on dividends alone—without selling a single stock to generate extra cash.

And you’ll get paid the same big dividends every month of the year – so that your income and expenses will once again be lined up!

This approach is a must if you want to quickly and safely grow your wealth and safeguard your nest egg through the next market correction, too!

This isn’t just a dividend play, either: this proven strategy also positions you to benefit from 10%+ yearly price upside potential, in addition to your monthly dividends.

That’s the Power of Monthly Dividends

We’ll talk more about that price upside shortly. First, let’s set up a smooth income stream that rolls in every month, not every quarter like the dividends you get from most blue-chip stocks.

You probably know that it’s a pain to deal with payouts that roll in quarterly when our bills roll in monthly.

But convenience is far from the only benefit you get with monthly dividends. They also give you your cash faster—so you can reinvest it faster if you don’t need income from your portfolio right away.

More on that a little further on. First I want to show you…

How Not to Build a Solid Monthly Income Stream

When it comes to dividend investing, many “first-level” investors take themselves out of the game right off the hop. That’s because they head straight to the list of Dividend Aristocrats—the S&P 500 companies that have hiked their payouts for 25 years or more.

That kind of dividend growth is impressive. But here’s the problem: these folks are forgetting that companies don’t need a high dividend yield to join this club—and without a high, safe payout, you can forget about generating a livable income stream on any reasonably sized nest egg.

Worse, you could be forced to sell stocks in retirement—maybe even into the kind of plunges we saw in March 2020 or throughout 2022—just to make ends meet.

That’s a nightmare for any retiree, and leaning too hard on the so-called Aristocrats can easily make it a reality: the ProShares S&P 500 Dividend Aristocrats ETF (NOBL), which holds all 69 Aristocrats, still yields just 2% as I write this.

Inefficient Markets Help Us

Bank $100,000 Annually (per Million)

Fortunately for you and me, the financial markets aren’t 100% efficient. And some corners are even less mature and less combed through than others.

These corners provide us contrarians with stable income opportunities that are both safe and lucrative.

There are anomalies in high yield. In an efficient market, you wouldn’t expect funds that pay big dividends today to also put up solid price gains, too.

We’re taught that it’s an either/or relationship between yield and upside – we can either collect dividends today or enjoy upside tomorrow, but not both.

But that’s simply not true in real life. Otherwise, why would these monthly payers put up serious annualized returns in the last 10 years while boasting outsized dividend yields?

For example, take a look at these 5 incredible funds that pay monthly and soar:

This is the key to a true “8% Monthly Payer Portfolio” – banking enough yields to live on while steadily growing your capital. It’s literally the difference between dying broke and never running out of money!

But I’m not suggesting you run out and buy these funds.

Midstream energy infrastructure is especially well-positioned to benefit from rising demand for natural gas, particularly through liquefied natural gas (LNG) exports. North American LNG-export capacity is expected to more than double by 2030. Meanwhile, America’s demand for electricity is climbing for the first time in nearly 20 years (driven by electrification and data centres), boosting natural gas-fired power generation.

The Alerian Midstream Energy Dividend UCITS ETF (LSE: MMLP) is an exchange-traded fund offering exposure to US and Canadian midstream firms. Roughly 65% of MMLP’s index by weighting is focused on natural gas infrastructure.

Profits in the energy infrastructure pipeline

Williams is also pursuing natural gas power projects to support data centres. Scheduled to start up in 2026, its Socrates project in Ohio for a data centre belonging to Meta is backed by a long-term, fixed-price power purchase agreement. Williams has two similar power projects under development. Williams recently raised its forecast for this year’s adjusted EBITDA by $50 million. The company expects adjusted EBITDA growth of 9% in 2025 and raised its dividend by 5.3% earlier this year.

Canada’s TC Energy (Toronto: TRP) handles approximately 30% of the natural gas consumed daily across North America. It spun off its liquids pipeline business last year, and now natural gas pipelines represent 90% of the company’s expected 2025 EBITDA. With robust growth opportunities, TC Energy expects to notch up C$6 billion-C$7 billion annually in capital expenditure. For instance, the company recently announced the Northwoods pipeline project to support power generation in the US Midwest, including for data centres. It is expected to come online in 2029.

TC Energy expects comparable yearly EBITDA growth of 5%-7% from 2024 through 2027. The company expects C$10.8 billion in comparable EBITDA for 2025, which implies 8% growth. TC Energy boasts a 25-year record of dividend increases and anticipates 3%-5% annual dividend growth over the next few years.

Also worth researching is Cheniere Energy (NYSE: LNG). It liquefies natural gas for export. The company is expanding its export capacity at Corpus Christi, a key gas port, and expects to sanction an additional expansion project this year. EBITDA is expected to expand by 9% growth in 2025.

Cheniere has been the clear leader in terms of buyback activity in the midstream sector, repurchasing $5.5 billion of equity since 2022. Cheniere had $3.5 billion remaining on its repurchase authorisation at the end of March. The company has also prioritised dividend growth, committing to raising its payout by about 10% each year through to the end of this decade

This article was first published in MoneyWeek’s magazine.

The Bank of England’s Bank Rate is coming down more slowly than perhaps many anticipated, the economic outlook remains murky and the twin threats of online retail and hybrid working continue to place additional pressure on the business models of some Real Estate Investment Trusts (REITs). But another bid battle for a property play, this time between Tritax BigBox (BBOX) and private equity giant Blackstone (BX:NYSE) for Warehouse REIT (WHR), suggests there is value to be had here.

We have already bagged a bid for CARE REIT and should be a beneficiary of the fight for Assura (AGR)between Primary Health Properties (PHP) and KKR (KKR:NYSE). In this context, the discounts on offer to net asset value per share (NAV) at British Land (BLND), Derwent London (DLN), Shaftesbury Capital (SHC) and Town Centre Securities (TOWN), which range from 24pc to 52pc, still feel like they merit patient support, even if the foursome operate in different areas of the property market compared to Warehouse REIT and Assura.

Lower interest rates and improved economic activity could both help, while a growing number of REITs, including bid target Assura, Safestore, Custodian Property Income, Sirius Real Estate and British Land, are also starting to show signs of stabilisation, or even renewed increase, in net asset value (NAV) per share. The discounts are starting to close in some cases, and any further merger and acquisition activity could accelerate that process.

Questor says: hold Assura (AGR): 50.1p British Land (BLND): 381p Derwent London (DLN): £20.50 Shaftesbury Capital (SHC): 151.8p Town Centre Securities (TOWN): 139.0p

Analysts are hopeful the tide is turning on the beleaguered sector

Published on July 1, 2025

by Holly McKechnie

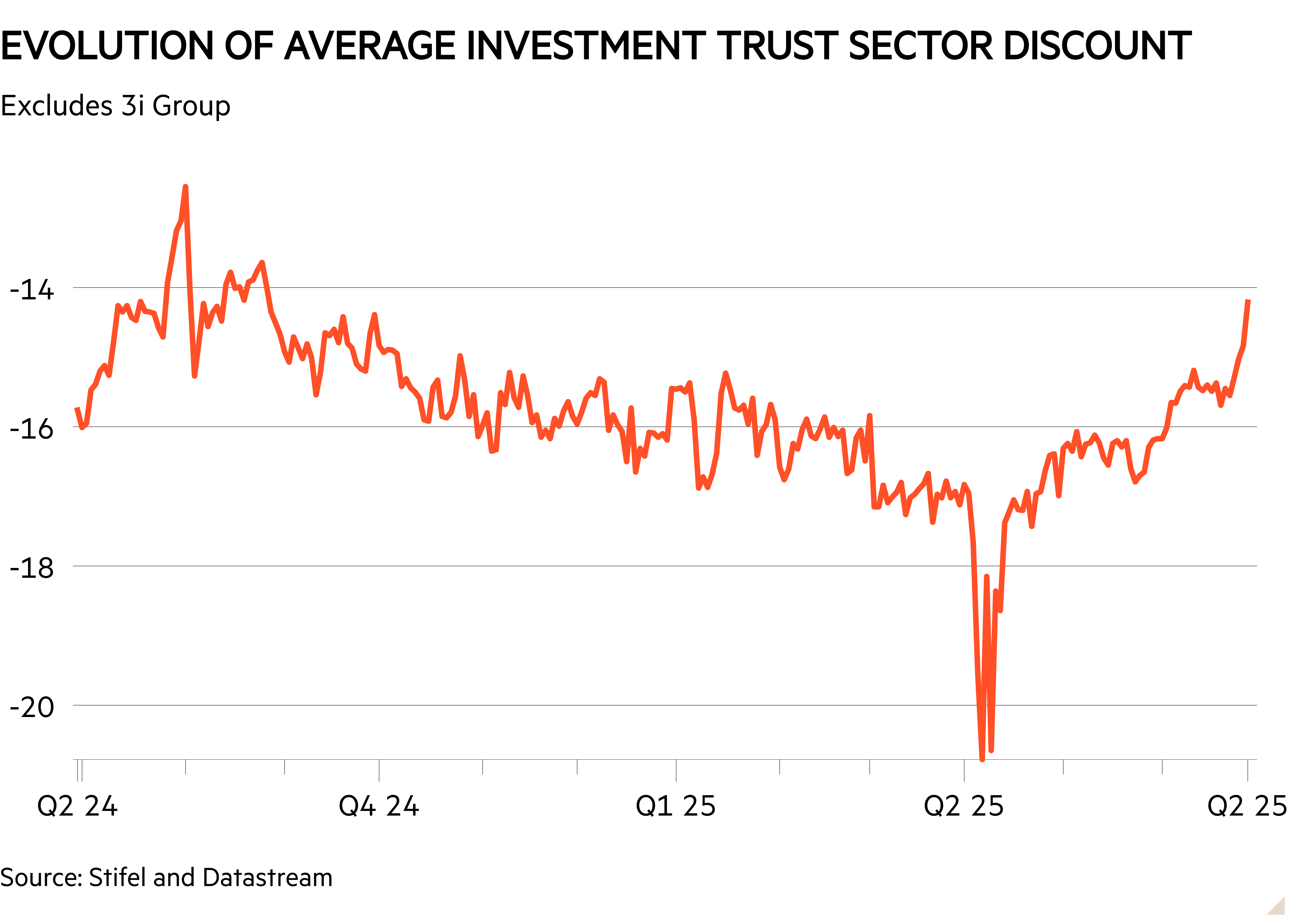

For the first time in a long time, there is some positive news on the investment trust discount front.

Over the past three months, the average investment trust discount has started to narrow, having reached new highs in April following the tariff turmoil. Analysts are hopeful that this trend will continue.

Several factors are behind this shift. In part it has been driven by increased investor confidence, as markets bounce back following April’s dip.

“The market has seen increased buying interest for investment company shares and we think it is fair to say that a market rally ‘floats all boats’,” Stifel analysts Iain Scouller and William Crighton said.

Broadly the discounts narrowing are reflective of the movement of major indices during this period.

However, other factors have also had an impact. Share buyback programmes, prevalent across the sector since interest rates started to go up in 2022 have, up until now, had limited success in addressing the average discount.

In part, this was because the sector average was unduly impacted by the alternative asset trusts as these tend to trade on bigger discounts. But thanks to the slow implementation of share buyback programmes this is beginning to change, analysts said.

“Buying back stock when you’ve got assets that are quite illiquid is hard,” James Carthew, head of investment company research at QuotedData, said. However, alternative asset trust boards have begun to make some progress, which is reflected in the narrowing average discount.

“They have rejigged the way that those funds work so that they have cash available to fund buybacks, which has been a long, slow, painful process, but a lot of them are doing it now,” Carthew added.

Investors’ Chronicle

Increased M&A activity has also helped to narrow the average investment trust discount. In June, for example, Downing Renewables & Infrastructure Trust PLC (DORE) accepted a £175mn bid from Downing Estate Planning, while earlier this year BBGI Global Infrastructure (BBGI) received a £1bn takeover bid from British Columbia Investment Management.

Again, this trend has been most pronounced in the alternative assets subsector, particularly in relation to property trusts, with bidding wars for both Assura (AGR) and Warehouse Reit (WHR) under way.

Kamal Warraich, head of fund research at Canaccord Wealth, argued that the current uptick in M&A is set to accelerate. This could “further reduce discount rates, as investors prefer more liquidity and lower fees, both of which come with greater scale,” he said.

A rise in activist activity across the investment trust sector has also had an effect, with Saba’s interventions earlier in the year being the most high profile example of this.

While shareholders rejected Saba’s proposals for the seven investment trusts it targeted, its actions did prompt the trust’s boards to introduce new measures in response.

For example, Schroder UK Mid Cap (SCP) has introduced an active buyback policy as well as a management fee reduction. Meanwhile, European Smaller Companies (ESCT) has enacted a sizeable tender offer. CQS Natural Resources Growth & Income (CYN) has also put forward a tender offer, as well as proposing the introduction of a higher dividend and decreased management fees.

New activist players have also cropped up during this period, including Achilles Investment Company (AIC), which was launched earlier this year by seasoned activists Chris Mills and Robert Naylor. The trust is primarily targeting funds in the property, renewable and infrastructure sectors.

Meanwhile, more established activist trusts have also stepped up the pressure.

“AVI Global (AGT) has, for ages, been buying stakes in private equity funds. But it’s shifted from just investing in funds with wide discounts, to investing in funds with wide discounts and trying to do something about it. It changes the mindset of it,” Carthew said.

Finally, falling interest rates have also had a positive effect on investment trust discounts. In particular prompting interest in investment trusts “with relatively high yields such as UK equity income, infrastructure and renewables,” Scouller and Crighton observed.