Building a substantial passive income can be hard work. While I dream of retiring and living off my UK shares, it isn’t an easy objective to achieve.

Savings discipline

Before I start building a substantial passive income I need to have some money to invest in the first place. I think the foundation of my investment dream comes from savings discipline.

When I calculate my potential passive income in the future, one of the biggest factors is how much I have to invest on a regular basis. For instance, if I assume a 7% annual return and invested £20 each week, I could have a portfolio worth £105,628 in 30 years’ time.

Let’s change that to £100 per week invested. With that same rate of return and timeline, I could instead be sitting on £528,139 worth of investments in 30 years. That’s a huge difference that’s driven by savings discipline and sticking to my goals for the long run.

Dividend shares

Another big factor in achieving my passive income dreams is the investments themselves. I believe in a Foolish long-term perspective and am always looking for strong UK shares that tick my boxes.

For instance, I’m a big believer in dividend shares. This is especially the case for my passive income goals as I do like the regular payout and ability to reinvest versus uncertainty of future capital growth.

How to Reach Financial Freedom

Of course, there’s uncertainty with dividends. Companies do change dividend policies and that’s almost guaranteed over my long-term time horizon

Take the likes of Legal & General (LSE: LGEN). This is a blue-chip insurer and asset manager in the FTSE 100 with a £13bn market cap and 9.3% dividend yield right now.

The company has strong brand awareness (we all know the coloured umbrella) and the potential to grow its total assets in the lucrative UK retirement policy market. I think it’s certainly one for dividend-hungry investors to consider if it can maintain that yield.

While Legal & General isn’t top of my buy list, it does show there are some serious dividend payers on the market that can help me achieve my dream. Ultimately, investing in a portfolio of dividend shares that can regularly deliver me a passive income stream is the goal for me.

Diversification

Diversification is the final piece of my puzzle. I don’t want to put all of my passive income hopes and dreams in the hands of one stock.

How you could bank tens of thousands of dollars in yearly dividend cash for every $500,000 invested, and …

Dear Reader,

A half-million dollars is a lot of money. Unfortunately, it won’t generate much income today if you limit yourself to popular mainstream investments.

The 10-year Treasury pays around 4.3% as I write this. That’s not bad, historically speaking, but put your $500K in them and you’re only looking at $21,500, right around the poverty level for a two-person household. Yikes.

And dividend-paying stocks don’t yield nearly enough. For example, Vanguard’s popular Dividend Appreciation ETF (VIG) pays around 1.7%. Sad.

When investment income falls short, retirees are often forced to sell their investments to supplement their income.

Of course, the problem here is that when capital is sold, the payout stream takes an immediate hit – so that more capital must be sold next time, and so on.

Avoid the Share Selling “Death Spiral”

Some financial advisors (who are not retired themselves, by the way) say that you can safely withdraw and spend, say, 4% of your retirement portfolio every year. Or whatever percentage they manipulate their spreadsheet to say.

Problem is, in reality, every few years you’re faced with a chart that looks like this.

Apple’s Dividend Was Fine – Its Stock Wasn’t

As you can see, the dividend (orange line above) is fine — growing, even — but you’re selling at a 25% loss!

In other words, you’re forced to sell more shares to supplement your income when they’re depressed.

Remember the benefits of dollar-cost averaging that built your portfolio? You bought regularly, and were able to buy more shares when prices were low?

In this case, you’re forced to sell more shares when prices are low.

When shares rebound, you need an even bigger gain just to get back to your original value.

The Only Reliable Retirement Solution

Instead of ever selling your stocks, you should instead make sure you live on dividends alone so that you never have to touch your capital.

This is easier said than done, and obviously the more money you have, the better off you are. But with yields still pretty low, even rich folks are having a tough time living off of interest today.

And you can actually live better than they can off of a (much) more modest nest egg if you know where to look for lesser-known, meaningful and secure yield.

I’m talking about annual income of 8%, 9% or even 10%+ so that you’re banking $50,000 (and potentially more) each year for every $500,000 you invest.

You and I both know an income stream like that is a very nice head start to a well-funded retirement.

And it’s totally scalable: Got more? Great!

We’ll keep building up your income stream, right along with your additional capital.

And you’ll never have to touch your nest egg capital – which means you won’t have to worry about or running out of money in retirement, or even the day-to-day ups and downs of the stock market.

The only thing you need to concern yourself with is the security of your dividends.

As long as your payouts are safe, who cares if your stock prices swing up or down on a given day?

Most investors know this is the right approach to retirement.

Problem is, they don’t know how to find 8%, and 10% yields to fund their lives.

And when they do find high yields, they’re not sure if these payouts are safe. Will the company or fund have enough cash flow to pay the dividends into the future?

And how sensitive are these payouts to the latest headline, Fed policy changes or unrest on the other side of the globe?

We’ll talk specific stocks, funds and yields in a moment.

But first, a bit about myself.

I graduated cum laude with an industrial engineering degree — which is actually pretty popular with Wall Street recruiters.

But I couldn’t stand the thought of grinding it out in a cubicle for 80 hours a week. So I moved to San Francisco and got into the tech scene.

A buddy and I started up two software companies that serve more than 26,000 business users.

The result was a nice chunk of change coming in … and I had to decide what to do with my money.

I had seen plenty of young “techies” come into sudden cash and burn through their windfall in a year, ending up right back where they started.

That was NOT going to be me. I already had dreams of living off my wealth one day, decades before I retired.

I got plenty of cold calls from brokers wanting to “help” me. But I knew that nobody would care as much about my money as me.

So I went out on my own and invested my startup profits in dividend-paying stocks.

I’ve been hunting down safe, stable and generous yields ever since, growing my wealth with vehicles paying me 8%, 9%, even 10%+ dividends.

Over the past 10+ years, I’ve been writing about the methods I use to generate these high levels of income.

Today I serve as chief investment strategist for Contrarian Income Report — a publication that uncovers secure, high-yielding investments for thousands of investors.

Since inception, my subscribers have enjoyed dividends 5 times (and much more!) the S&P 500 average, plus big annualized gains!

And that brings me to a crucial piece of advice…

The ONE Thing You Must Remember

If I could leave you with just one nugget of investing wisdom today, it would be to NEVER overlook the incredible wealth-building power of dividends.

Few investors realize how important these unglamorous workhorses actually are.

Here’s a perfect example…

If you put $1,000 in the dividend-paying stocks of the S&P 500 back in 1973, you would have had $87,560 by 2023, or 87x your money.

But the same $1,000 in the non-dividend payers would have grown to just $8,430 — 90% less.

That’s why I’m a dividend fan.

The stock market is a fantastic wealth-building machine, but it doesn’t always go straight up!

There have been plenty of 10-year periods where the only money investors made was in dividends.

And that’s what gives us dividend investors such an edge.

When you lock in an 8%+ yield, you’re booking an income stream that’s bigger than the stock market’s long-term average return right off the bat.

Of course you can’t just buy every ticker symbol out there with a flashy yield, or you’ll get burned pretty fast.

So let’s wipe the false promises of mainstream finance from our minds and start thinking the “No Withdrawal” way…

The above article is for information only and is not an endorsement for Contrarian Income Report /Investor or investing in CEF’s.

Most half-million-dollar stashes are piled into “America’s ticker” SPY.

The SPDR S&P 500 ETF (SPY) is the most popular symbol in the land. For many 401(K)’s, this is all there is.

And that’s sad for two reasons.

First, SPY yields just 1.2%. That’s $6,000 per year on $500K invested… poverty level stuff.

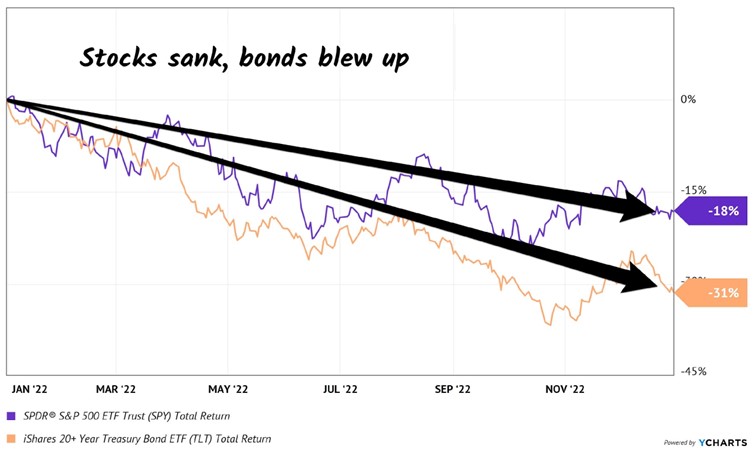

Second, consider 2022 for a moment (and only a moment, I promise!).

SPY was down nearly 20% that year. That is no bueno, because that $500K would have been reduced to $400K.

The last thing we want to do is lose the money we’re getting in dividends (or more) to losses in the share price. Which is why we must protect our capital at all costs.

Step 2: Ditch 60/40, Too

The 60/40 portfolio has been exposed as senseless.

Retirees were sold a bill of goods when promised that a 60% slice of stocks and 40% of bonds would somehow be a “safe mix” that would not drop together.

Oops.

Inflation — plus an aggressive Federal Reserve, plus a (thus far) persistently steady economy — drop-kicked equities and fixed income before they went on a serious bull run in 2023 and 2024.

It just goes to show that bonds are not the haven guaranteed by the 60/40 high priests. They could easily plunge just as hard (or harder) than stocks in the next economic crisis.

Just like they did in 2022 (sorry, we’re only going to spend one more second on that disaster of a year). US Treasuries plunged, which resulted in the iShares 20+ Year Treasury Bond ETF (TLT) getting tagged.

Sure, it still paid its dividend. But even including payouts, the fund was down 31% — worse than the S&P 500. Ouch!

When stocks and bonds are dicey, where do we turn? To a better bet.

A strategy to retire on dividends alone that leaves that beautiful pile of cash untouched.

Step 3: Create a “No Withdrawal” Portfolio

My colleague Tom Jacobs and I literally wrote the book on a dividend-powered retirement.

In How to Retire on Dividends: Earn a Safe 8%, Leave Your Principal Intact, we outline our “no withdrawal” approach to retirement:

Save a bunch of money. (“Check.”)

Buy safe dividend stocks with big yields

Enjoy the income while keeping the original principal intact.

To make that nest egg last, and our working life worthwhile, we really need yields in the 7% to 10% range. We typically don’t see these stocks touted on Bloomberg or CNBC, but they are around.

Of course, there are plenty of landmines in the high-yield space. Some of these stocks are cheap for a reason. Which is why we need to be contrarian when looking for income.

We must identify why a yield is incorrectly allowed to be so high. (In other words, we need to figure out why the stock is priced so cheaply!)

As I write, the top 10 payers in my Contrarian Income Report portfolio yield about 10.6% on average.

On every million dollars invested, this dividend collection is spinning off an incredible $106,000 every single year!

And you don’t have to be a millionaire to take advantage of this strategy.

A $750k nest egg will generate $79,500 annually…

$500K could hand you $53,000…

You get the idea.

The important thing is that these yields are safe, which creates stability for the stock (and fund) prices attached to them.

We want our income, with our principal intact.

It’s really the only way to retire comfortably, without having to stare at stock tickers all day, every day.

Now, many blue-chip yields are safe. They just need to hit the gym and bulk up a bit. Here’s how we take perfectly good, yet modest, dividends and make them into braggarts.

Step 4: Supersize Those Yields

Mastercard (MA) is a near-perfect dividend stock. Its payout is always climbing, having nearly doubled over the last five years. (MA shareholders, you can thank every business that accepts Mastercard for your “pennies on every dollar” rake.)

Tap, tap, tap. Remember cash? Me neither. Another 2020 casualty, with Mastercard making a few dimes or dollars on every plastic transaction.

The cashless trend has been in motion for years. But international growth prospects remain huge. Just a few years ago, 80%+ of transactions in Spain, Italy and even tech-savvy Japan were in cash.

We expect more dividend hikes as more cash turns to plastic. Or skips plastic entirely and goes straight to e-transfers. Mastercard and close cousin Visa (V) nab a nice piece of that action, too.

The only chink in MA’s armor? Everyone knows it is a dynamic dividend stock. So it only yields 0.5%. Investors keep bidding it higher, knowing that the next dividend raise is just around the corner.

So, the compounding of those hikes makes MA a great stock for our kids and grandkids. You and I, however, don’t have the time to wait for 0.5% to grow. And $2,500 on a $500K investment simply won’t get it done.

Let’s instead consider top-notch closed-end fund (CEF) Gabelli Dividend & Income Trust (GDV), managed by legendary value investor Mario Gabelli.

Mastercard is one of Gabelli’s largest holdings. But we income investors would prefer GDV because it boasts a healthy dividend right around 6.8%, paid monthly, nearly 14 times what Mastercard pays (and this is low in CEF-land; other funds, like the next one we’ll talk about, pay nearly double that).

And today, thanks to the conservative folks who buy CEFs, we have a rare opportunity to buy Mario’s portfolio for just 87 cents on the dollar.

Yup, GDV trades at a 13% discount to its net asset value, or NAV. It’s a way to boost MA’s payout and snag a discount, too.

Where does this discount come from?

CEFs are like their mutual fund cousins, with one exception: they have fixed pools of shares, so they can (and do) trade higher and lower than their NAVs, or “fair” values (the value of their holdings minus any debt).

As contrarians, we can step in when they are temporarily out of favor, like after a pullback, when liquidity is low, and buy them at generous discounts.

GDV holds more blue-chip dividend payers alongside MA, such as American Express (AXP), Microsoft (MSFT) and JPMorgan Chase & Co. (JPM). And with GDV, we have an opportunity to purchase them at a 13% discount.

These high-quality stocks wouldn’t normally qualify for our “retire on $500K” portfolio because everyone in the world knows they are strong long-term investments.

Even though these companies are constantly raising their dividends, constant demand for their shares keeps their prices high (and current yields low). So they never meet our current-yield requirement.

GDV does. The fund pays a monthly dividend that adds up to a nice 6.8% annual yield.

Let me give you one more idea (and this is where that much larger payout comes in): the Eaton Vance Tax-Managed Global Diversified Equity (EXG) is another CEF with a similar blue-chip dividend portfolio.

But EXG generates even more income than GDV by selling covered calls on the shares it owns.

More cash flow means a bigger dividend — and EXG pays an already terrific 9.4%!

So we buy and hold EXG and GDV forever, collecting their monthly dividends merrily along the way? Not quite.

In bull markets, these funds are great. But in bear markets, they’ll chew you up.

Step 5: Protect That Principal!

My CIR readers will fondly recall the 15 months we held GDV and EXG together, collecting monthly dividends plus price gains that added up to 43% total returns.

What was happening in that period, from October 2020 until February 2022? The Federal Reserve was printing money like crazy. Not only did the Fed stoke inflation, but we also enjoyed an asset-price lift.

Starting in 2022, we had the opposite situation. The stock market was topping, and we didn’t want to fight the Fed. We sold high, and by late 2022, both funds were down sharply:

We Sold EXG and GDV Just Before They Plunged

For whatever reason, “market timing” is a taboo phrase among long-term investors. That’s a shame because it is quite important.

By aligning our dividends with the market backdrop, we can protect our principal from bear markets.

Step 6: Start Here to Retire on $500K

So if the “tried and true” money advice — like the 60/40 portfolio and the 4% rule — has been properly exposed as broken…

Where do we go from here?

Well, imagine your portfolio in just a few days or weeks from now spinning off 8%, 9% and even double-digit dividends with the reliability of a Swiss watch… with many of my recommendations paying every single month no less!

No more worrying how much is coming in next month.

Passive income is essentially money that comes in regularly with little active effort once the initial setup is complete. Think of it as an income stream that flows even when you’re not clocking in hours at a traditional job. From dividend-paying stocks and investment trusts to real estate rentals or monetized digital content, the idea is to build an infrastructure—be it financial capital or creative assets—that generates income almost on autopilot.

The term “Passive Income Live” can refer to platforms or resources—like the website Passive Income Live—that offer up-to-date insights on navigating today’s economic challenges while building such income streams. For example, articles featured on that site discuss strategies like leveraging investment trust dividends, diversifying asset allocation, and mitigating the risks that come with market concentration, particularly in highly weighted indices. This kind of analysis is especially useful now, as market fluctuations (from tariff impacts to broader economic shocks) remind investors that even “passive” strategies must be managed intelligently.

For someone in the UK, there’s a growing interest in tailoring passive income strategies to local conditions. Resources such as the article on “6 Best Passive Income Ideas To Make £1,000/Month In The UK” from The Motley Fool outline approaches ranging from dividend stocks to real estate investments and beyond. What stands out is the emphasis on diversification—not putting all your eggs in one basket—to build a resilient financial portfolio that continues working for you over the long haul.

If you’re exploring passive income for yourself, it’s worth reflecting on your own situation: What assets (time, money, skills) can you invest upfront ? How comfortable are you with risk? And importantly, how diversified do you want your income streams to be? Building a few different channels can safeguard you against market shifts and boost overall financial security.

Cash is not king. During a market rout, seek undervalued income

A 43 year track record of increasing payouts stands this trust in good stead

Robert Stephens

Extreme stock market volatility will inevitably prompt some income investors to declare that “cash is king”. After all, cash does not fluctuate in value and currently offers an income return in excess of 4pc.

However, holding cash for the long term is problematic for several reasons. It offers no capital growth potential, which means it has a rather drab long-term track record versus shares, and is likely to produce a diminishing income return as monetary policy easing continues.

By contrast, share prices are extremely likely to rise from their current levels and produce growing dividends as the economic outlook gradually improves.

Therefore, rather than sitting on piles of cash in perpetuity, Questor believes that drip-feeding excess cash into undervalued shares is a far better idea. With several high-quality income shares now offering lower valuations and higher yields than they did earlier this year, there is a wide range of attractive options for income-seeking investors.

For example, FTSE 250-listed The Merchants Trust has a dividend yield of 5.5pc thanks to its 5pc share price decline since the start of the year. This is 190 basis points higher than the FTSE All-Share index’s yield, and the trust has the added bonus of raising its dividend for the past 43 consecutive years, a record it won’t be keen to lose.

While this does not guarantee further dividend growth in future, when combined with revenue reserves amounting to around 65pc of last year’s shareholder payout, it suggests the trust could prove to be a relatively reliable income option.

In addition, its dividends have risen at an annualised rate of 6.3pc since 1982. This compares favourably with an average annual inflation rate of around 3pc over the same period and, as a result, its shareholders have enjoyed a material increase in their purchasing power.

The company’s recent share price decline also means that it now trades at a 2.3pc discount to net asset value. This compares with an average discount of just 0.2pc over the past five years and suggests the trust offers good value for money.

Separately, the company’s major holdings are dominated by well-known FTSE 100 stocks including British American Tobacco, GSK and Shell. However, it also has significant exposure to mid-cap shares, with 32pc of its assets currently invested in the more domestically-focused FTSE 250 index.

This is significantly higher than the mid-cap index’s representation in the FTSE All-Share, which sits at roughly 15pc of the wide-ranging market, meaning the trust’s performance is more closely aligned with the UK economy’s performance vis-à-vis its benchmark.

In Questor’s view, this adds to Merchants’ overall appeal. The FTSE 250 has, after all, been exceptionally unpopular with investors over recent years. As a result, depressed valuations were widespread even before the stock market’s recent bout of extreme volatility. Over the long run, today’s grossly undervalued stocks could deliver strong total returns as the economy’s performance gradually improves.

Of course, a significant mid-cap focus and a gearing ratio of just over 14pc mean the company’s share price is likely to be relatively volatile. It could even fall further in the short run as the ongoing global trade war may yet worsen before it improves.

We must also note that the company’s shares have lagged the FTSE 100 index by 10 percentage points since our ‘buy’ recommendation in February 2020.

In this column’s view, however, Merchants has a sound long-term outlook. Its relatively appealing valuation, significant exposure to the grossly undervalued FTSE 250 index and substantial gearing mean it is well placed to deliver capital growth as the economy’s outlook improves.

When considered from an income perspective, the company’s generous yield and longstanding track record of inflation-beating dividend growth equate to a worthwhile long-term opportunity.

The company therefore becomes the latest addition to our income portfolio. We will use excess cash generated from previous sales to fund its notional purchase.

Clearly, some investors will naturally be tempted to do the opposite and hold cash during the current period of economic and stock market turbulence. However, this column firmly believes that gradual purchases of high-quality, undervalued dividend stocks represents a far superior means to obtain an attractive income over the coming years.

Questor says: buy Ticker: MRCH Share price at close: £5.32

Dividend yields balloon on renewables and infrastructure investment trusts Published: 16 Apr 2025

Dividend yields on renewable energy infrastructure and infrastructure investment trusts are close to all-time highs, data from the industry data shows.

The average yield of the renewable energy sector spiked to 10.6% this month, an all-time high, the Association of Investment Companies (AIC) said.

For infrastructure investment trusts, the yield is 6.4%, with a record of 6.8% on 7 April.

The recent market sell-off sparked by Donald Trump’s new US tariffs has led to yields in both sectors ballooning to all-time highs.

Shares prices for these trusts are at historically wide discounts to their net asset values, with a 21% discount for infrastructure trusts and 33% for renewable energy infrastructure.

“Performance of both these sectors has suffered in the last three years as rising interest rates and cost disclosure issues have taken their toll,” said AIC director Annabel Brodie-Smith.

“However, analysts believe the pessimistic view of these infrastructure sectors is overdone and there’s reason for optimism,” she said.

“The infrastructure dividend yields are some of the highest on the UK market, offering resilient income in an uncertain world.

“There has been some corporate activity within the sector and there are predictions of more to come. Boards are acting proactively for their shareholders, undertaking more share buybacks and realising assets. The market has priced in interest rate cuts which would benefit these investment trusts.”

She noted that investors should “do their homework” and thoroughly research investment trust options and should speak to a financial adviser if they have any doubts.