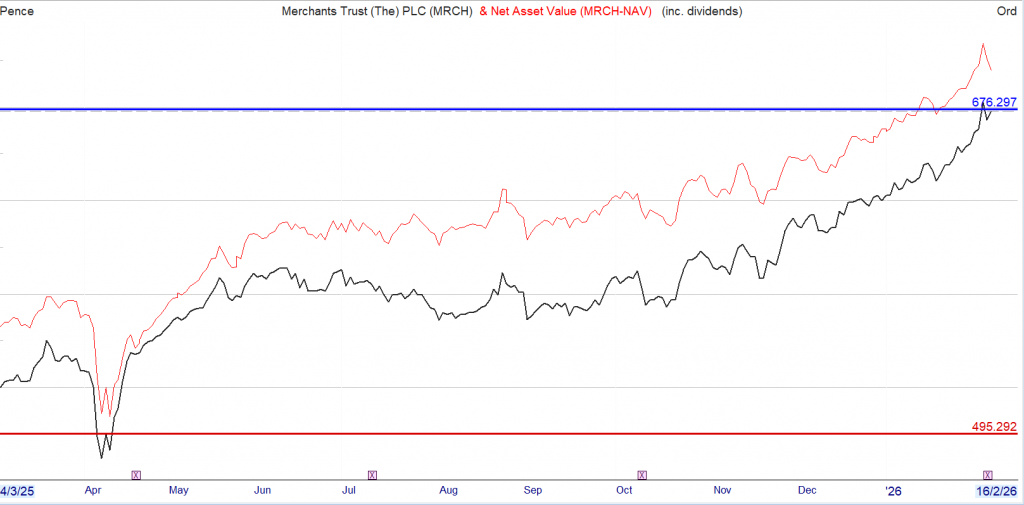

You decided to trade the breakout, the yield at 500p was around 6%. If the breakout failed you would still collect the dividend. Your analysis worked and you would currently be up 30% in less than a year. You would be watching the market to be ready to take part profits, maybe reducing the share holding back to your initial stake.

Performance and portfolio

Merchants delivered a NAV total return of 5.4% over the six-month period, compared with 7.5% for the FTSE All-Share Index. Absolute returns were positive, though relative performance lagged the benchmark and some peers. This was largely due to the narrowness of market leadership: as in the US, certain groups of companies drove the market higher.

Some of these leading stocks did not align with our Manager’s long-term value approach. Instead, greater emphasis has been placed on attractively valued domestic cyclicals, which have underperformed in the recent low-growth environment. While this positioning has weighed on short-term results, we remain convinced that it provides the best foundation for long-term returns. The Board has reviewed the Manager’s strategy in detail and continues to support this disciplined, value-focused approach.

Portfolio activity reflected evolving opportunities, with an unusually high number of new investments compared with a typical half-year. Selective purchases were made where valuations and income prospects were attractive, while holdings with more limited capital growth potential were reduced.

The share price return of 1.5% reflected a widening discount to NAV, in line with a broader trend across UK investment trusts as international investors reduced exposure to UK equities. The Board, together with advisers and the Manager, monitors this closely and retains the option of share buybacks if appropriate. Meanwhile, we remain active in shareholder engagement and marketing to improve awareness and demand.

Earnings and dividends

Total income from the portfolio was £28.8m, 2.5% higher than the £28.1m generated in the first half of last year. Earnings per share rose by 3.5% to 17.7p (2024: 17.1p). This strong income performance provides confidence both in the sustainability of the dividend and in rebuilding revenue reserves.

With the final dividend for the 2025 financial year now approved, Merchants has increased its dividend for 43 consecutive years – earning the Company “Dividend Hero” status from the AIC. The Board has declared a second interim dividend of 7.3p per share, payable on 20 November 2025 to shareholders on the register at 10 October 2025. This brings the total dividend for the first half of the current financial year to 14.6p, compared with 14.5p last year – a year-on-year increase of 0.7%.

One to consider for your Snowball, when Mr. Market gives you the opportunity.

Or how to get rich without taking big risks with your hard earned.

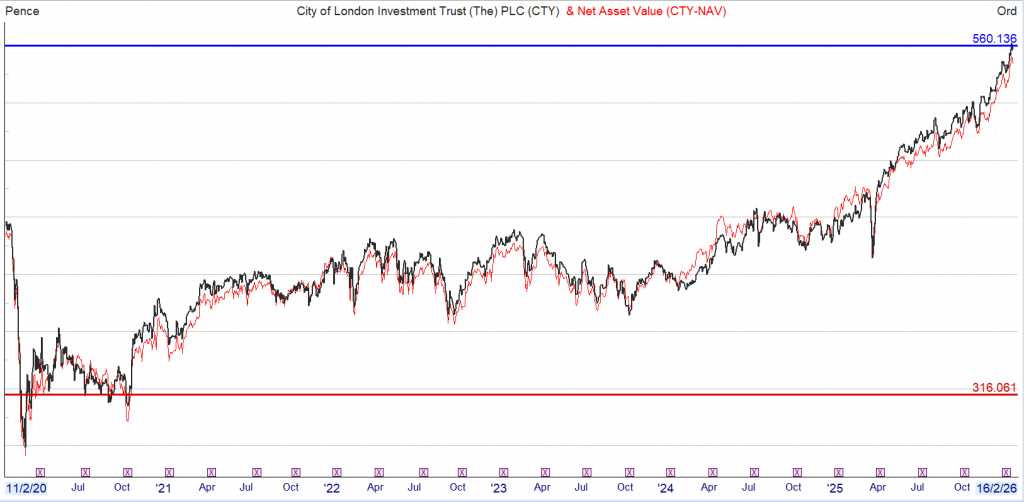

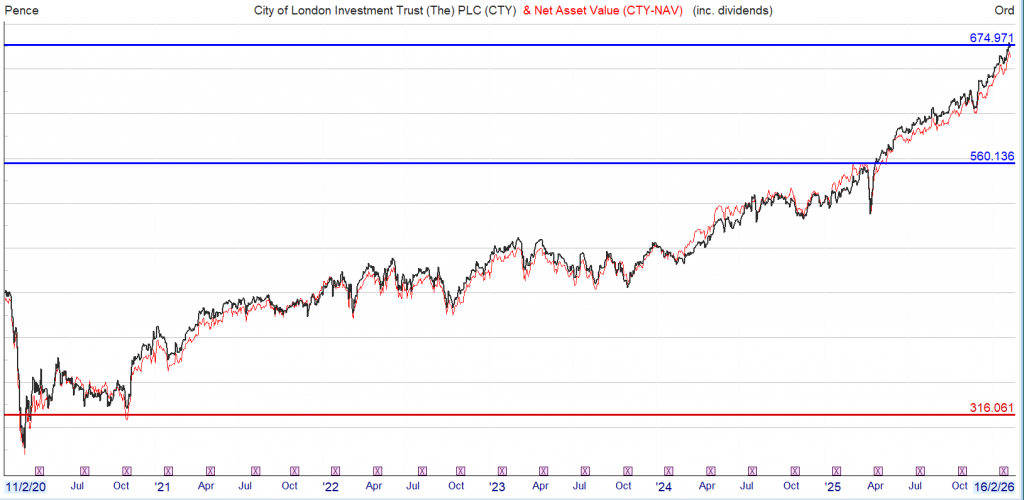

You knew that CTY had paid an increasing dividend for over 40 years. The share was sold off during the covid crisis as some shares cut their dividend forecasts but you knew that CTY had reserves to pay their dividend in crisis times and you knew that CTY had only had to use their reserves to pay their dividend, in 40 years plus, twice.

If you bought at 316p the dividend was 19p yield was 6%, the dividend is now 21.3p, you will receive the 6% plus yield for

One problem would be there were other dividend hero shares that were paying a higher yield as the prices fell but

With dividends included you have achieved the

The current yield is 3.8%, as the price rises the yield falls, you could take out your capital and invest in another higher yielding share and still earn 3.8% on a share that sits in your account at zero, zilch, cost.

Plus you would be earning say 8% on your new share, a yield of 12%.

NOTE

I was requested to include more memes for those where English is not their first language, keep everything crossed for another market crash, which becomes more certain as markets continue to rise, when is the known unknown, until then

Jon Smith highlights a REIT he thinks could be set for a long-term comeback as more people return to office working. It also comes with a generous yield.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services. Become a Motley Fool member today to get instant access to our top analyst recommendations, in-depth research, investing resources, and more.

Real estate investment trusts (REITs) are companies that focus on property. By managing and leasing sites, income can be generated, making them attractive options for dividend investors. Ones that have been beaten down recently can be undervalued, with one high-yielding option catching my eye.

Why the stock is down

I’m talking about the Regional REIT (LSE:RGL). It focuses on regional office properties, mainly commercial buildings outside London’s M25. It owns and manages a portfolio of these and aims to generate income and capital growth from rents and asset value increases.

Over the past year, the stock ‘s fallen 12%, which is broadly in line with the portfolio’s net asset value (NAV) decline. In theory, these should correlate well with each other, although I note that the stock trades at a long-term discount to the NAV. This typically indicates weak sentiment towards the company, but in years to come it should reduce to be closer to the NAV.

The drop in the NAV reflects the decline in value in the commercial property market. However, I don’t see this as a big risk going forward. Several of my friends are slowly being forced back to working three or four days a week in the office. In a few years’ time, I think most traditional businesses will be back with staff in the office every day as standard. Based on this reasoning, I think the REIT’s long-term outlook’s positive.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

Juicy income

Historically, Regional REIT’s paid income out quarterly. From looking at the dividend per share over the past year, the rise in dividend yield has come partly from the payout increasing, as well as the stock falling.

Aside from the yield, the main thing I look at is the dividend cover. It’s currently 1, which means earnings per share can completely cover the dividend. This is a good sign, as the business isn’t paying shareholders more than it can actually afford. One risk is that if it falls below par, then it’ll start eating into retained earnings, which isn’t great.

Another factor I check for REIT dividends is rent collection. In the latest quarterly update, this stood at 97.7%. I want this to be as close to 100% as possible, so that the company can maximise the revenue potential.

The outlook from here

Back in November, the company said: “Leasing momentum has been negatively impacted by the uncertainty stemming from the broader economic environment and specifically by the inconsistent messaging from the UK Government regarding the forthcoming budget“.

This has now passed, and I don’t feel it was as bad as many expected. Of course, it’s a risk going forward, but I think the next report should detail more management certainty about the UK economy for 2026, helping the stock. Overall, I think it’s a good income share for investors to consider.

Looking for the best dividend stocks to buy in 2026 ? These top real estate investment trusts (REITs) might merit serious attention, says Royston Wild.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services. Become a Motley Fool member today to get instant access to our top analyst recommendations, in-depth research, investing resources, and more. Learn More.

Real estate investment trusts (REITs) can be an excellent way to target a long and lasting passive income. Dividends aren’t guaranteed, but they have qualities than can make them better income choices than most other UK shares.

Under REIT rules, companies must pay at least 90% of annual rental earnings out in dividends. This still leaves payouts sensitive to profits performance, but it also provides a higher level of income visibility for investors than most other stocks.

Should you buy Alternative Income REIT Plc shares today?

Despite ongoing uncertainties from Trump’s tariffs to global conflicts, Mark Rogers and his team believe many UK shares still trade at substantial discounts, offering savvy investors plenty of potential opportunities to learn about.

So what are the hottest REITs to buy right now. In my opinion, three of the hottest to consider are:

Schroder European Real Estate Investment Trust

Alternative Income REIT

Regional REIT

Each of these property powerhouses offers a forward dividend yield of at least 10%. Want to know what makes them true dividend heroes?

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

Euro giant

Schroder European Real Estate Investment Trust holds a top-class portfolio of properties in continental hotspots. We’re talking about highly desirable cities with strong economies and infrastructure. Think Paris, Berlin, and Hamburg, to name a few of its locations.

It’s a winning strategy that leads to reliable rent collection and strong occupancy (portfolio occupancy was 97%, latest financials show). The trust’s exposure to different sectors like logistics, office, retail, and data centres also gives it strength.

The forward dividend yield here is 8.1%. I think it’s a top trust to consider, even though adverse currency movements could take a bite out of earnings.

Another diversified REIT

Like the Schroder trust, Alternative Income REIT takes a diversified approach to the property market. If anything, things are even more wild and wonderful — they range from hospitals and petrol stations, through to hotels, gyms, and thermal power plants.

Its rent collection is even higher, at 100%. And its tenants are locked down on ultra-long contracts, providing protection from (if not totally eliminating) cyclical pressures on rent collection. The weighted average unexpired lease term for its 23 tenants sits at 17 years.

With more than 92% of rental income linked to inflation, too, Alternative Income is in great shape to grow shareholder payouts. For 2026, the dividend yield is a brilliant 8.5%.

Double-digit yield

At 10%, Regional REIT is today the highest-yielding property trust on the London stock market. It carries greater risk than the other contenders we’ve looked at, reflecting its narrow exposure to the UK and broader weakness in the office market in which it specialises.

This has caused its share price to slump over the past year (down 10%). But is the bad news now baked into the trust’s share price? I think it might be. As well as having that enormous yield, Regional REIT trades at a 51% discount to its net asset value (NAV).

To my mind, it’s a top recovery share to consider. The REIT retains a high-quality portfolio, and is selling non-core assets to boost occupancy and repair the balance sheet. As for dividends, this year’s predicted payout is covered more than twice over by expected earnings, providing a wide margin of error.

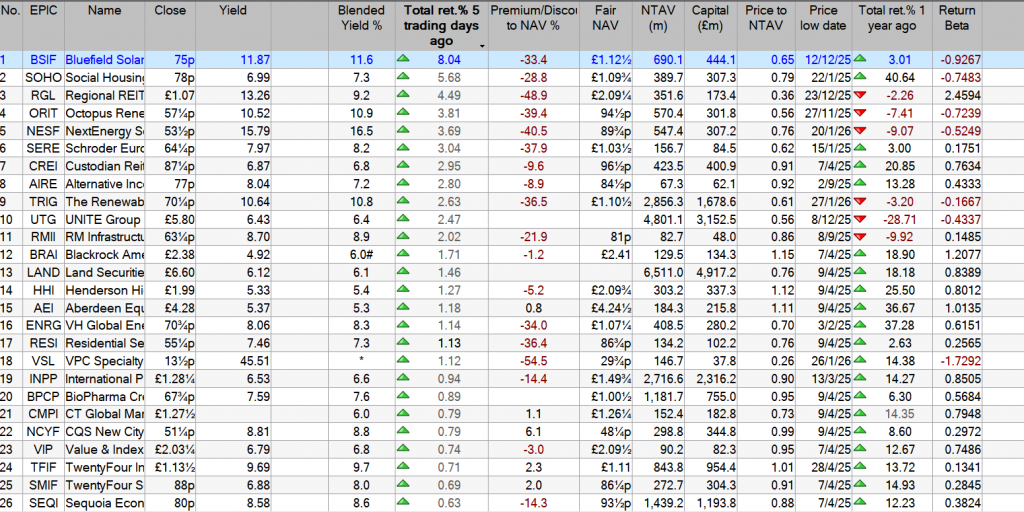

SERE

Schroder European Real Estate Investment Trust PLC – London and Johannesburg-listed property investor – Dutch telecommunications company Koninklijke KPN NV formally terminates its lease at Schroder European Real Estate’s Apeldoorn property. KPN occupies this mixed-use office and data centre property in Netherlands, representing about 19% of the company’s portfolio income and 6% of portfolio value as at September 30, 2025. The lease termination will take effect from December 31, 2026. Early this month, Schroder European Real Estate Investment warned of the risk of maintaining its dividend following the departure of KPN.

Kepler View

As the board notes, alongside broader market factors, two specific factors play a role in Schroder European Real Estate’s (SERE) persistent discount. The largest tenant, KPN, has already provided verbal confirmation and is expected to formally confirm shortly its intention not to renew its lease, which expires in December 2026. We note that this is a large site that, aside from its current use, could be repositioned for residential development. But it’s current mixed use, particularly as a datacentre, are in an area which is seeing strong tenant demand across Europe.

We understand from the manager that there is a strong case to believe that the French tax claim will not be paid, and the board confirms that it has received professional advice on the same basis. Alongside this change, there is now a timetable for when we might expect a resolution, and as the board notes, there is an appeal process should the initial assessment go against SERE.

SERE’s significantly wider than average discount, c. 36% , says to us that the market is taking a wait and see approach on the above issues and while that’s frustrating given that there has been an improvement in sentiment to REITs more generally, with some of SERE’s UK-listed peers turning in very good share price performances over the last year, taking this approach is understandable given the binary nature of both issues. Once the outcome of either or both is known, then SERE’s remaining portfolio, which has maintained a relatively stable valuation and income, could be significantly undervalued by the share price.

to the fact that bargain hunters have seized on the (briefly) wilting premium on 3i Group Ord III

But it also shows us that one particularly battered Association of Investment Companies (AIC) sector, Renewable Energy Infrastructure, continues to draw in buyers after a horrific run of performance.

both sit in the top 10 list for January and seem to be a common addition to portfolios, what with their ultra-high dividend yields and wide share price discounts to net asset value (NAV).

But shareholders have been through the wars: rising interest rates (and bond yields) did huge damage to share prices across the sector in 2022.

All manner of problems, from a backlash against renewable energy to low wind speeds in the first half of 2025 and a broader crisis for the investment trust universe, have continued to hurt returns in the following years.

The government confirmed its decision to go ahead with this option last week, although the news did in fact prompt the sector to rally. It’s worth asking what triggered this – and what bargain hunters buying the likes of UKW shares now need to understand.

Lesser evils – and the funds feeling the most pain

The sector rallied because the switch from RPI to CPI from April, while unwelcome, seemingly represented the lesser of two evils. The government had also considered temporarily freezing the subsidy level to make way for “a gradual realignment with the CPI”.

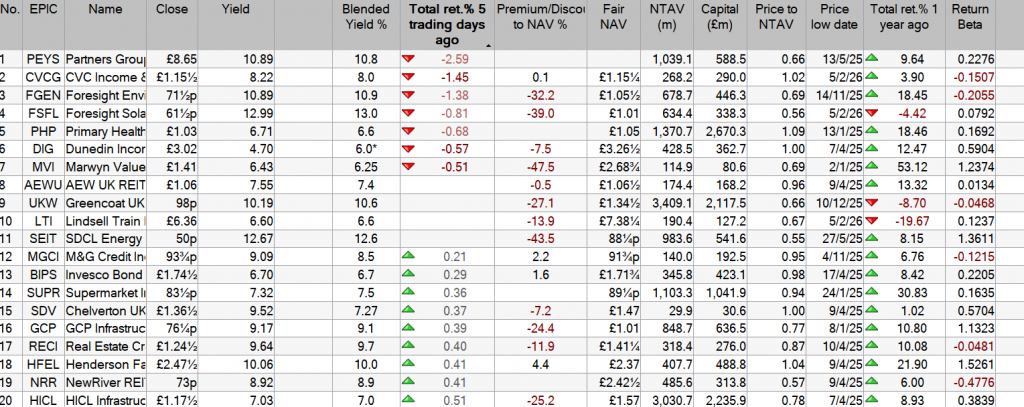

As the table below shows, some of the renewable trusts have substantial exposure to certain subsidy schemes and would see their NAV fall on the back of either change.

But the first option (now chosen by the government) is less harmful, with modest hits to NAV. While the damage is lessened, it’s the solar funds that are expected to take the biggest hit.

Estimated NAV impact of switching from RPI to CPI now vs a temporary freeze

Trust

Estimate of revenues from affected subsidies (%)

NAV change (%) from switching now

NAV change (%) from a temporary freeze

Bluefield Solar Income

50

-1.9

-9.9

Foresight Environmental Infrastructure

20

-0.3

-1.7

Foresight Solar

49

-2.2

-10.9

Greencoat UK Wind

40

-1.7

-6.1

NextEnergy Solar

45

-2.9

-10.3

The Renewables Infrastructure Group

15

-0.7

-2.5

Source: JPMorgan.

Buy or avoid?

As mentioned, there’s plenty to draw a bargain hunter in, from wide discounts to high yields.

In theory, we now have plenty of catalysts for a recovery: interest rates have been on a downward trend, high dividend yields mean investors are “paid to wait”, while such payouts are in most cases fully covered by earnings, and corporate action could also drive improvements. That could range from asset sales to mergers and buyouts.

Note, for example, that names such as Harmony Energy Income and Downing Renewables saw bids at decent premiums to share prices in the last year. That could prompt a recovery from depressed valuations.

It’s worth pointing out that not all specialists are keen on the sector at all, with Charles Murphy, senior research analyst at Singer Capital Markets, arguing that the underlying assets could ultimately prove hard to value in future, undermining the investment case.

Meanwhile, investors are seemingly overwhelmed with factors that complicate the picture, from shifts in power prices to bond yield moves and a political environment that looks increasingly hostile to the subsector.

As Hawksmoor’s Dan Cartridge adds, Reform UK is leading in the polls. “They have extreme negative views on the renewables sector,” he says. “That’s an ongoing reason for caution, although the next general election is still quite a long way off.”

Such considerations might understandably put off a potential investor. There are much simpler ways to bag a good yield, be it via a “core” infrastructure trust such as HICL Infrastructure PLC Ord HICL

(on roughly 7%), via equity income or via a UK government bond, whose 10-year instrument offers 4.5%.

Which trusts are the analysts favouring?

With the caveat that some may simply avoid a headache by not investing in the sector at all, trust brokers and analysts did pick out a few names they viewed as appealing.

as an interesting fund thanks to the fact that it’s so heavily diversified.

At the mid-point of 2025, the fund had a 27% allocation to wind power, with 14% in anaerobic crop digestion (where organic materials such as grass are broken down by microorganisms to produce renewable energy), 12% in solar power, 10% in biomass and smaller allocations to areas such as low-carbon transport and energy storage. The trust can have an eclectic mix of assets, with these including a fish farm in Norway.

Hawksmoor’s Cartridge is also a fan of Foresight’s diversification, while pointing to other trusts which have a good spread of assets and “where overall cash-flow profiles are more defensive” – for example with strong solar power generation last year to offset the falls suffered in wind generation. Here, he points to Octopus Renewables Infrastructure Ord ORIT

To briefly linger on these names, ORIT unveiled something of a turnaround plan in September where it promised to continue and extend its share buyback programme, look to reduce its debt, sell down some assets and make selective new investments.

TRIG sought to roll into stablemate HICL last year, a plan that ultimately fell apart after it caused a stink among HICL investors. However, this drama may have alerted investors to the existence of TRIG as a possible takeover target.

The case for Greencoat UK Wind

Meanwhile, Greencoat UK Wind remains popular with the professionals, much as it does with ii customers.

Cartridge notes that it has “a unique funding model that has been successful over a long time”, while Peel Hunt’s Markuz Jaffe adds: “We like Greencoat UK Wind for the pure-play domestic strategy. It remains simple and is perhaps most exposed to the subsidy amendment but is linking [dividends] to inflation even if that’s now CPI rather than RPI.

“It has been a leader in trying to address the discount, via buybacks, changes to management fees and recycling capital to reduce gearing.”

The Peel Hunt team also has an eye on Bluefield Solar Income as a tactical opportunity, with a focus on how its sale process and strategic review is progressing. The trust is expected to give an update when it publishes its interim results in March. Jaffe notes that its peer, Foresight Solar, also looks interesting because of this.

“The portfolio is quite vanilla, it’s on a wide discount and its closest peer is going through a sale process, so there’s reason to expect a catalyst for a material rerating in the shares,” he says.

Not all rosy

An improving environment does not guarantee a recovery. Note, for example, that interest rates have already been falling over the last year, with no discernible rebound for most of the trusts in this sector. And investors may want to tread carefully.

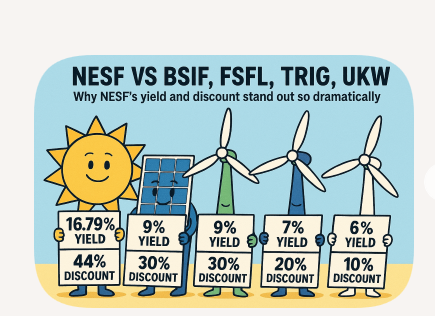

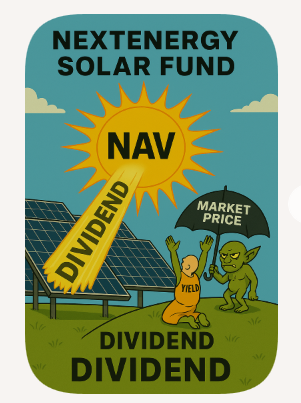

Cartridge notes some caution on certain specialist names, for example. He points to ii customer favourite NextEnergy Solar, noting that the dividend yield at the NAV level is “higher than the discount rate, pointing to it being unsustainable” and Bluefield Solar.

When it comes to NESF, it does have one of the highest yields in its sector.

However, the board has been in the midst of a strategic review “exploring all options to close the current discount”. Options discussed include exploring “opportunities to enhance shareholder returns” and upping the level of capital recycling. The findings of the strategic review are due out this year.

As ever, specialist funds tend to carry greater volatility than generalist options and can reward and punish adventurous investors in equal measure.

How much do I need in a Stocks and Shares ISA to earn a £300 monthly passive income?

James Beard considers the passive income potential of a Stocks and Shares ISA

Posted by James Beard

Published 7 February

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

It’s estimated that approximately 15% of UK adults have a Stocks and Shares ISA. Many of these individuals will be using them to buy dividend shares to help provide a second income. As an added bonus, this cash can be enjoyed tax-free.

So without having to work for it, how much would someone need in an ISA to earn an extra £300 a month ? Let’s take a closer look.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

What’s achievable?

The answer to this question depends on the level of return achieved. For example, the FTSE 100 currently (5 February) has a historic yield of 3.1%. With a return like this, an ISA would have to be worth £116,129 to meet our £300 a month target.

But I reckon it’s possible to achieve a higher return by carefully choosing a diversified selection of high-yielding stocks. The 10 highest on the index are currently offering 6.4%, meaning our portfolio would need to be worth £56,250 to achieve our objective.

Of course, dividends cannot be guaranteed. However, there are plenty of stocks that have a long history of steadily increasing their payouts and offering above-average returns