Supermarket Income REIT plc (LSE: SUPR), the real estate investment trust with secure, inflation-linked, long-dated income from grocery property, has today declared an interim dividend in respect of the period from 1 July 2024 to 30 September 2024 of 1.53 pence per ordinary share (the “First Quarterly Dividend”).

The First Quarterly Dividend will be paid on or around 15 November 2024 as a Property Income Distribution (“PID”) in respect of the Company’s tax-exempt property rental business to shareholders on the register as of 11 October 2024. The ex-dividend date will be 10 October 2024.

£3k to invest? 2 UK REITs I’d buy in an ISA this month

I’ve been looking for the top UK REITs to add to my ISA. Here are two stocks that I think have terrific long-term passive income potential.

Zaven Boyrazian, MSc❯

Published 2 October

been looking for the top UK REITs to add to my ISA. Here are two stocks that I think have terrific long-term passive income potential.

Zaven Boyrazian, MSc❯

Published 2 October

Image source: Getty Images

FSFL UKW

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

The UK stock market’s filled with awesome real estate investment trusts (REITs). By capitalising on these unique financial vehicles, investors can indirectly own a small piece of lucrative assets that are often prohibitively expensive as a direct investment.

Most REITs own and operate a commercial or residential real estate portfolio. However, some focus on alternative assets, such as renewable energy infrastructure.

While fossil fuels aren’t likely to disappear any time soon, the rising threat of climate change is sparking a lot of investment in renewables. And even the new British government’s targeting the creation of 650,000 clean energy jobs by 2030.

With that in mind, I’m looking at two REITs that look set to thrive under a renewable-friendly government, Greencoat UK Wind (LSE:UKW), and Foresight Solar Fund (LSE:FSFL).

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

Wind and solar-powered REITs

Both firms have almost identical business models. They invest in renewable energy infrastructure (wind for Greencoat, solar for Foresight), generate clean electricity, and sell it to energy suppliers.

The constant and rising demand for electricity has enabled both companies to be highly cash-generative. And both significantly benefited from the sharp rise in energy prices over the last few years. As a result, dividends have been hiked nine years in a row, keeping up with inflation and helping shareholders build chunky passive incomes.

This trend should continue, in my opinion. As previously mentioned, energy demand’s climbing thanks to the rising popularity of electric vehicles (EVs) and power-hungry artificial intelligence (AI) models. Needless to say, this could be a lucrative opportunity, attracting investment from the private sector, even if Labour falls short of its targets.

What could go wrong?

Looking across the renewable REIT landscape, these two stocks appear to offer terrific value. While they operate as leveraged businesses, both generate sufficient cash to comfortably meet interest expenses as well as dividends. And to top things off, both trade at a double-digit discount to their net asset value, indicating a potential buying opportunity.

That’s obviously an encouraging trait. So much so that I’ve already added Greencoat to my income portfolio, with plans for Foresight to join the mix once I have more capital at hand. However, these investments, while promising, are far from risk-free.

Like many businesses operating within the energy sector, neither Greencoat nor Foresight have any pricing power. Electricity prices are determined by supply and demand imbalances while being kept in check by regulators like Ofgem. And as a result, energy’s long been a cyclical sector.

When energy prices fall, the earnings of these REITs fall as well. And while the management teams can execute a bit of price hedging with fixed-rate customer contracts, prolonged drops in energy prices could compromise dividends, especially if debt‘s left unchecked in a higher interest rate environment.

Nevertheless, both these businesses are seemingly in a strong position right now. And with a solid track record of navigating fluctuating market conditions, it’s a risk I feel is worth researching, given the long-term passive income that could be unlocked.

Not Naval gazing that’s a completely different topic.

I’ll try to update the dividend information from the Watch shares but it’s best to DYOR before u part with your hard earned and further information released by watch list shares can be found at

During this financial year, the Company declared four interim dividends totalling 5.9pps (2023: 5.7pps), with the total dividends declared for 2023 being 6.045pps, which included 0.345pps relating to monies received following the successful settlement of a historic legal case), which was in line with the previously announced dividend target of 5.9pps (2023: 5.7pps), representing a 3.5% increase on the previous year. I am pleased to report that these dividends were covered by cash earnings.

As set out in Note 8 to the consolidated financial statements, these dividends were covered by the Group’s Adjusted EPS (representing cash) of 5.99pps (2023: 6.43pps). Furthermore. All dividends were paid as Property Income Distributions (‘PIDs’).

Historically the Board has paid dividends in four instalments each financial year. The Board intends to continue with this practice by making dividend payments in November, February, May and August each year. In order to do this, all dividends need to be declared and paid as interim dividends.

Discount

The discount of the share price to NAV at 30 June 2024 narrowed to 18.4% from 23.1% at the previous year end. The Board monitors the discount level throughout the year and has the authority to both issue and buy back shares. Although these powers have not been used to date, the Board believes these authorities are important powers for it to have available, if required, and therefore recommends that shareholders vote in favour of their continuance at the forthcoming AGM.

£££££££££££

Current share price 72.8p dividend 5.99p a yield of 8%

hujantoto Hello there! Would you mind if I share your blog with my twitter group? There’s a lot of folks that I think would really appreciate your content. Please let me know. Cheers

££££££££££

Yep, no problem with that. If the content is from another source it would be polite to include their name.

The Company’s aim remains to provide investors with an attractive and sustainable dividend that increases in line with RPI while preserving capital on a real basis. In each of the first 10 years since listing, the Company increased its dividend target by RPI and for 2024, the 11th year, the Company increased its target significantly above RPI to 10 pence per share. The Company paid an underlying 2.5 pence per share with respect to Q1 2024 and has declared a dividend of the same amount per share with respect to Q2 2024, giving a total of 5 pence per share for the period. The Company also paid an additional £29 million of dividends to shareholders in February, increasing the total dividend to 10 pence per share for 2023.

In line with the current higher interest rate environment, the Company forecasts a 10 per cent return to investors on NAV (net of all costs). This includes reinvestment of excess cash generation (dividend cover) in addition to the dividend yield. Since listing, the Company has reinvested £935 million of excess cash generation and paid £1,074 million of dividends.

£££££££££££

Price was 165p dividend 10p yield 6% Price now to buy 142p yield 7% Now a belt and braces Trust. As always timing and then time in. 7% compounded doubles your hard earned in ten years.

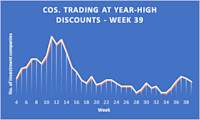

The number of investment companies trading at 52-week high discounts fell to just nine. It wasn’t a good week all round though, one sector saw all five of its constituents set new discount highs for the year.

By Frank Buhagiar• 30 Sep

We estimate there to be nine investment companies that saw their share prices trade at 52-week high discounts over the course of the week ended Friday 27 September 2024 – two less than the previous week’s 11.

It’s not often all funds in one sector see their share prices set new 52-week high discounts to net assets on the very same day. But that’s what happened with the five-strong Japan sector. True, the share prices of the five investment companies – Baillie Gifford Japan (BGFD), CC Japan Income & Growth (CCJI), Fidelity Japan (FJV), JPMorgan Japanese (JFJ), Schroder Japan (SJG) – had been bobbling close to the year-high marks for some time now, but all saw their discounts set new highs for the year on Friday 27 September 2024.

Of the five, only SJG released results this week but a +21% NAV total return for the full year hardly cause for concern, more like celebration. The reason for the sector-wide discount doldrums have a political driver. After Japan’s markets closed on Friday, former defence minister, Shigeru Ishiba, narrowly defeated Economic Security Minister, Sanae Takaichi, in the Liberal Democratic Party’s leadership contest. That means Ishiba becomes Japan’s next prime minister.

With Ishiba considered to be on the hawkish side when it comes to monetary policy, expectations are that he will likely not stand in the way of further interest rate hikes as the Bank of Japan looks to normalise monetary policy after years of tackling deflation. Cue the election result causing the yen to gain more than 1% against the dollar and stock futures to sink, indicating a selloff in equities lies ahead when markets reopen on Monday. But with UK markets still open, the share prices of all five Japan-focused investment companies were always likely to come under pressure, and so it proved.

Fidelity Japan FJV19.53%JapanSchroder Japan SJG14.69%JapanBaillie Gifford Japan BGFD16.79%JapanCC Japan Income & Growth CCJI11.87%JapanJPMorgan Japanese JFJ14.50%Japan

Defensive sectors come to the fore even as investors celebrate Fed rate cut

Russ Mould Thursday, September 26

“Investors continue to welcome the first interest rate cut from the US Federal Reserve in four years, and a big one at that, in the view that the central bank is doing its best to keep American economic growth firmly on track,” says AJ Bell investment director Russ Mould.

“However, the need for a half-point cut may be tempering enthusiasm slightly, as it does suggest the Fed is concerned about the risk of a greater-than-expected slowdown, and this may be why defensive sectors are doing so well Stateside so far in 2024.

“The S&P 500 has gained just 1.6% since 10 July, which does not entirely smack of an imminent inflationary boom, and it may pay to dig beneath the headlines to see what investors are really thinking.

“The market may not always be right, but its views must be respected and so it is always worth paying attention to what the market is saying, and there will be many adherents to the view that ‘a bad stock in a good sector will outperform a good stock in a bad sector,’ at least in the near term.

“In this context, the US stock market’s response to the long-awaited reduction in interest rates from the Federal Reserve on Wednesday 18 September has been fairly textbook. Cyclical sectors such as Consumer Discretionary, Materials and Industrials have done well, as have so-called ‘bond proxies’ such as Telecoms and Utilities, as their yields become relatively more attractive as returns on cash and bond yields recede. Defensives such as Consumer Staples and Health Care have done less well, although pharmaceutical firms’ traditional role as a pre-presidential election punch bag for vote-hungry candidates could be an additional reason for the latter sector’s muted showing.

Source: LSEG Refinitiv data, as of 25 September 2024, based on S&P 500 sectors

“Tech stocks have continued to do well, and they remain the best performer in the year to date, buoyed by enthusiasm for the Magnificent Seven and all things related to artificial intelligence.

“However, the next best performer is Utilities, with Telecoms close behind.

Source: LSEG Refinitiv data, as of 25 September 2024, based on S&P 500 sectors

“This could be down to the possible boost to demand for electricity from data centres that run the Large Language Models behind artificial intelligence and store vast swathes of digitised information and content. It could be because utilities are seen as so-called ‘bond proxies,’ and a sector that usually does well when interest rates (and bond yields) are falling, as this makes the yield on utility stocks seem more attractive on a relative basis.

And it could be because investors are subtly looking for a haven, and industries where demand is relatively predictable and not too sensitive to the wider economy, just in case an unexpected slowdown is coming around the corner in the US.

“The long-term chart for Utilities’ performance relative to the S&P 500 remains ugly, but it is worth noting how the sector’s defensive, economically insensitive characteristics enabled it to outperform during 1990-92, 2000-02 and 2007-08, just as the US entered a recession or encountered some form of financial market meltdown, or both.

Source: LSEG Refinitiv data

“The presence of Financials among the leaders offers some reassurance, as does how every US sector is still in positive territory this year, but the presence of Utilities and Telecoms in the top five is not necessarily what you would expect to see if investors were truly confident in America’s economic outlook. Weakness in Energy and Materials may not be a good sign, either, although China’s efforts to reflate could yet give them a boost, especially if the US does enjoy a soft landing, or even avoid a slowdown altogether.

“According to the official data from the Office for National Statistics, the UK is emerging from the shallow recession suffered in the second half of 2023, and this may be helping cyclical sectors like Industrials and Consumer Discretionary, even if Energy and Materials are the laggards, just as they are in the USA, thanks to commodity price weakness that could speak of nerves regarding the wider, global economic outlook.

Source: LSEG Refinitiv data, as of 10 September 2024, based on the FTSE UK sectors

“That said, Materials is the best performer in the UK since the Fed cut, perhaps boosted by monetary stimulus in America, the world’s largest economy, and the application of a fiscal boost in China, its second biggest.

“Utilities have fared less well on this side of the Atlantic, and that could be down to uncertainty over the new AMP8 regulatory cycle for water companies that begins in April 2025, especially as water and waste treatment services providers are still the subject of much public opprobrium over the quality of their services, the prices they charge and the bonuses they pay. Utilities were also the subject of windfall taxes when Tony Blair’s Labour government took over in 1997 and investors may have taken some evasive action with this year’s general election in mind.

“These trends could yet prove ephemeral, and sentiment could switch again – technology for one is unlikely to go down without a fight. If indeed summer’s ructions are the first signs of a top in the sector which, for the moment at least, peaked in mid-July there may be many attempted rallies before the bull market cracks, just as there were in 2000 when the tech bubble burst. The telling indicator back then was each rally failed to reach the prior peaks and that may be a trend to note this time around, too, although investors are unlikely to be too keen to ‘fight the Fed’ for too long, unless the monetary medicine is not enough to stave off a US slowdown and the American market’s above-trend valuation multiples prove difficult to sustain (which was exactly what happened during the downturns of 2001-03 and 2007-09, when growth and thus corporate earnings both disappointed).”

City of London Investment Group PLC ex-dividend date CT Private Equity Trust PLC ex-dividend date European Assets Trust PLC ex-dividend date F&C Investment Trust PLC ex-dividend date Finsbury Growth & Income Trust PLC ex-dividend date Life Science REIT PLC ex-dividend date Manchester & London Investment Trust PLC ex-dividend date Murray International Trust PLC ex-dividend date Pantheon Infrastructure PLC ex-dividend date Real Estate Investors PLC ex-dividend date RIT Capital Partners PLC ex-dividend date Schroder European Real Estate Investment Trust PLC ex-dividend date Schroder Income Growth Fund PLC ex-dividend date Shires Income PLC ex-dividend date