The blog portfolio will have the right to buy 59,100 shares at a cost of £5,910.00

Some of the shares could have been sold, by selling the existing shares, at a gain of around £2,500 and the new shares would then replace the existing shares held at a big loss.

If, which is doubtful, the price was to rise I would sell some shares at an equivalent of around a 75% gain.

The longer term plan is to hold all the shares and receive the diluted dividend and reduce if/when Mr. Market gives me the chance.

Funds for the purchase will/should be provided by ADIG £3,733.00 and the balance from cash £1,443.00 and dividends received before the payment date.

According to Forbes, Warren Buffett is the fourth-richest person on the planet, with an estimated fortune of $121bn. Unlike the three ahead of him — Messrs Musk, Bezos, and Ellison — he’s built his wealth primarily from investing.

I’ve been looking at his career to see how I might go about accumulating significant wealth, without having any savings to start with.

1. Start early

The first thing I’d have to do is begin investing as early as possible. Buffett bought his first stock when he was 11. He’s still investing 82 years later.

Do you like the idea of dividend income?

The prospect of investing in a company just once, then sitting back and watching as it potentially pays a dividend out over and over?

The longer the investment horizon, the more time there is for wealth to grow. And delaying a few years can make a big difference.

The table below shows how much £100 invested today could be worth over different periods. The figures assume an annual growth rate of 7.4% — the average yearly return (with dividends reinvested) of the FTSE 100, from 1984 to 2022.

Period (years)

Final value (£)

5

143

10

204

20

417

30

851

40

1,738

82

34,862

2. Reinvest those dividends

By withdrawing dividends, the FTSE 100 would have delivered growth of ‘only’ 5.3%. With this lower rate, £10 would have been worth £789 after 40 years — over 50% less.

This demonstrates the power of compounding, which has been described as the eighth wonder of the word.

Berkshire Hathaway, Buffett’s own investment company, doesn’t pay dividends. Instead, it reinvests the cash it saves by buying more shares.

This has helped its stock achieve a compound annual growth rate of 19.8%, since 1964. A sum of £1 invested then, would now be worth over £3.7m!

That’s why — as tempting as it might be to spend dividends on a one-off treat — I always reinvest them.

3. Don’t put all your eggs in one basket

Most investors emphasise the advantages of diversification — spreading risk across a number of stocks.

However, Buffett once said: “A lot of great fortunes in the world have been made by owning a single wonderful business. If you understand the business, you don’t need to own very many of them“.

Some have interpreted this as meaning that he doesn’t believe in owning lots of individual shares.

On the contrary, the point he’s making is that most of us don’t have the skills (or time) to undertake the necessary research to consistently pick winners. In fact, he’s a big fan of diversification for the amateur investor.

In 1993, the billionaire said the “know-nothing” investor is likely to out-perform the average fund manager by investing in a tracker fund.

These are a great way of spreading risk across many companies through the ownership of just one investment.

From 1964-2022, a fund tracking the S&P 500 would have returned 24,708%.

Of course, there’s no guarantee that history will be repeated.

4. Be patient

Finally, Buffett is quoted as saying: “It is not necessary to do extraordinary things to get extraordinary results“.

In my view, too many people get caught up trying to find the next ‘big thing’. Remember, slow and steady sometimes wins the race.

Investing small — and often — can be effective. A sum of £50 a month, earning a return of 5%, will grow to nearly £30,000 after 25 years.

I don’t think I’ll ever be a billionaire, but, in my opinion, it’s never too late to follow in the footsteps of Warren Buffett and start building wealth by investing in stocks and shares.

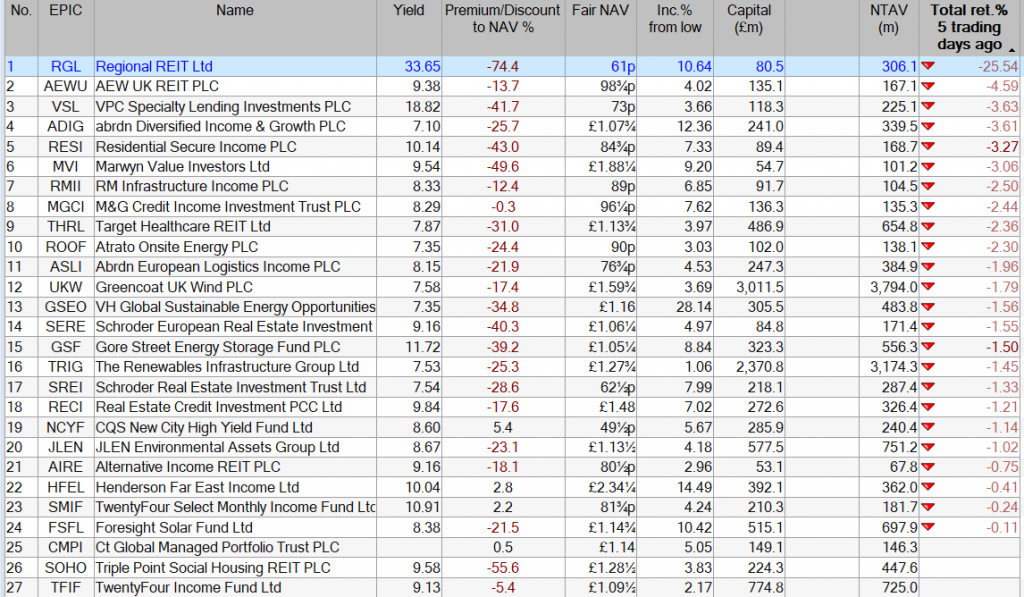

The blog portfolio will subscribe for it’s entitlement for the new shares to be issued at 10p.

With the cash from IDIG, dividends payable and current cash, there will enough cash, with no need to sell anything.

RGL intends to continue to pay dividends to keep its REIT status but they will be diluted by the new shares being issued.

When the new shares are issued the blog portfolio will be overweight with RGL so the intention is to sell some into the market if the price is favourable.

I thank you for reading the thread and posting a comment but sadly I can’t approve any post I can’t understand as that could lead to a very slippery slope. GL anyway.

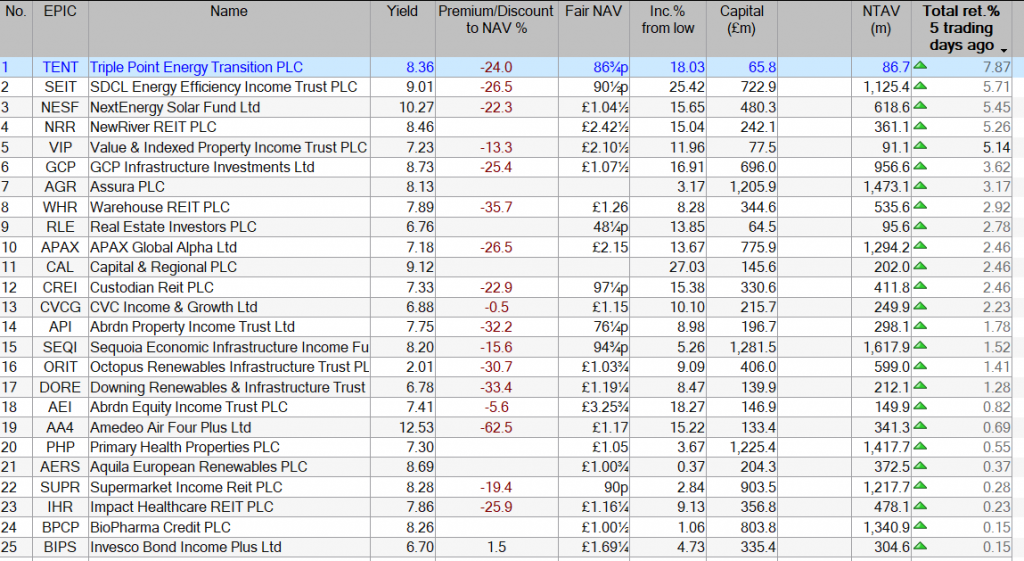

Perusing the FTSE 250, one dividend stock in particular stands out to me for its eye-popping yield. That’s NextEnergy Solar Fund (LSE: NESF), which has a huge 10.7% yield.

However, this renewable energy fund recently raised its payout for the 11th consecutive year. And the future still looks very bright, despite a big drop in the share price over the past few years.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

How it generates revenue

NextEnergy Solar is a specialist investor in solar assets and energy storage. At the end of March, its portfolio had 103 operating assets, enough to power the equivalent of 301,000 homes for one year.

A significant portion of the fund’s revenues comes from government-backed subsidies and power purchase agreements (PPAs). These are often indexed to inflation. This means that as inflation rises, the payments it receives also increase, providing a natural hedge.

Why is the share price in the doldrums?

The share price has fallen from 126p at the start of 2020 to just 78p today. The chief culprit for this is higher interest rates. They’ve impacted the entire renewables sector by increasing the cost of financing for both existing and new debt.

At the end of March, the company’s financial debt was £338m. Of this, 32% was on a floating rate (not fixed), so the high-rate environment is an ongoing risk here.

To reduce debt, the company has embarked on a capital recycling programme. It recently sold a 35.2MW solar farm in Lincoln for £27m. This transaction represented a 14% premium to the March holding value, which is very encouraging to see.

Proceeds from this will be used to reduce the company’s debt. Three other assets are still up for sale.

Massive discount

Higher rates also tend to negatively impact the value of assets, including solar farms. Currently, the fund is trading at a whopping 26% discount to net asset value (NAV).

Chairwoman Helen Mahy said: “NextEnergy Solar Fund continues to maintain a strong financial platform in a challenging environment… [We] view the current size of the company’s discount to NAV as unjustified.”

Big passive income potential

I agree and think that when the Bank of England starts to cut interest rates, the share price could be set for a nice rebound. Longer term, I remain bullish on the clean energy sector and this fund in particular.

Meanwhile, there is that massive 10.7% dividend yield. At the current price, I’d need to buy 11,987 shares to aim for £1,000 in annual passive income. This would set me back £9,350.

While no payout is guaranteed, I reckon the chance to lock in such high-yield passive income is well worth the risk here. So I’m looking to buy this stock myself.

How to become an ISA millionaire Investing is a long-term game so don’t expect to get rich quick with an ISA.

Performance can be volatile but by staying invested you benefit from the power of compounding.

If you can invest the full £20,000 annual ISA allowance each tax year and get a 5% return before fees, you could hit the million-pound mark in 25 years with a pot worth £1,002,269.08.

An annual return of 7% could get you to the million-pound target within 22 years, while a more conservative 3% would take 31 years.

“Starting your ISA investing early is a key component to joining the ISA millionaire club,” adds Hasler.

“Other important steps to getting the best returns and seeing that money grow are using your ISA allowance every year, investing wisely and regularly, then leaving the money there.”