Sequoia Economic Infrastructure Income (SEQI)18 December 2025

Disclaimer

Disclosure – Non-Independent Marketing Communication

This is a non-independent marketing communication commissioned by Sequoia Economic Infrastructure Income (SEQI). The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

SEQI generates an exceptional yield by lending against critical modern infrastructure.

Sequoia Economic Infrastructure Income (SEQI) offers yield high enough to rival most alternative assets or fixed income trusts from an ungeared portfolio of loans to borrowers in the infrastructure sector. The portfolio has a number of defensive properties, being highly diversified by sub-sector, borrower and asset, majority senior secured debt and managed with a conservative approach that has seen very low realised losses in the portfolio.

The infrastructure referred to includes new economy industries and themes like the physical support for artificial intelligence and new and greener energy supply like renewables and nuclear. With loans being made on a three to five-year basis, there is a constant flow of money back into the portfolio allowing the managers to be flexible with their positioning. Having been an early mover in the data centre space and generating attractive returns, they are currently finding lending standards on new loans slip due to the artificial intelligence boom, meaning this allocation has been falling. Instead, the team have been investing further down the chain in the power supply and networks connecting these to the grid, taking advantage of the same trends via loans with better rates and covenants.

SEQI’s Dividendyield of 8.8% reflects the impact of a Discount of 18%. This compares highly favourably to the company’s AIC Infrastructure and AIC Debt – Loans & Bonds peers. The dividend is fully cash covered, and the team report this cover should increase in the coming months as new loans start paying interest. The board has bought back substantial amounts of shares in recent years to tackle the discount, and states that managing the discount remains a priority.

Analyst’s View

We think SEQI is an attractive income product in the current economic environment. The portfolio is invested in defensive, non-cyclical sectors and in crucial infrastructure with strong economic and policy support behind it. The lack of fund-level gearing is notable, as it means that the NAV should be more stable than many other high-yielding options, and that financing costs don’t affect profitability. With the strong focus on new economy infrastructure like data centres, broadband and power networks we think the trust offers a way for income investors to generate a high return from these secular growth themes without taking equity risk.

We think the discount largely reflects the higher interest rate environment since 2022 which has seen capital go into cash and government bonds, and so as rates continue to come down demand for SEQI’s shares should rise. In that light, buying a portfolio of ungeared loans on an 18% discount looks attractive, particularly when considering the board’s commitment to buybacks and the fact the NAV includes a pull-to-par gain of c. 2.8p, or 3%, on loans trading below 100. While falling interest rates should see yields available fall across fixed income sectors, it is notable that SEQI has maintained its portfolio yield and dividend target while rates have fallen between 125bps and 235bps in the major jurisdictions. We think this speaks to the diversity of the opportunity set, which continues to benefit from strong technicals, and the conservative approach of the management team, who have plenty of levers to pull to maintain the yield without massively tramping up risk.

Bull

High dividend yield from ungeared portfolio with relatively low credit risk

Strong technical picture with withdrawal of banks from the sector and few competing funds

Specialist team with many years of experience in this space pre-SEQI launch

Bear

Falling interest rates will create a challenge to maintain the yield

Buybacks have used large amounts of cash which, if continued, would reduce funds available for investment and maintaining yield

Unfamiliar asset class which is less transparent to the average investor

Hello would you mind stating which blog platform you’re using? I’m going to start my own blog soon but I’m having a difficult time making a decision between BlogEngine/Wordpress/B2evolution and Drupal. The reason I ask is because your design and style seems different then most blogs and I’m looking for something unique. P.S Apologies for being off-topic but I had to ask!

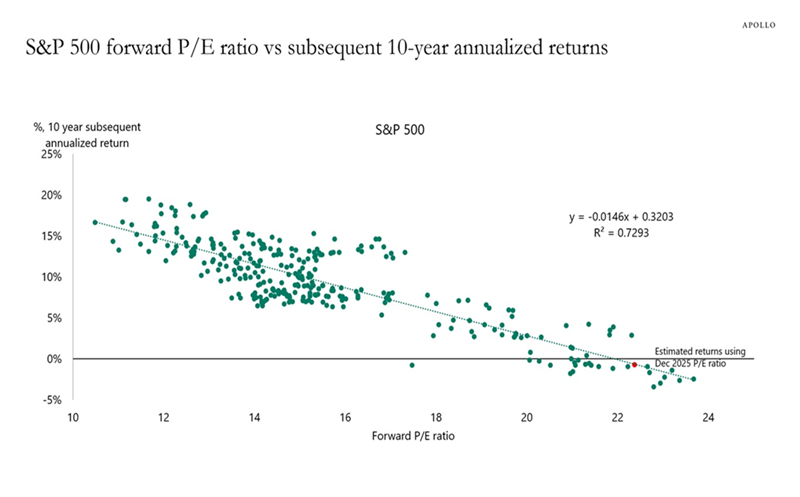

Every year, the stock market has a theme. And I’ve got a pretty good idea of what 2026’s will be.

Simply this: If you buy stocks in the new year, your return will be zilch – at best – for a decade. Maybe more.

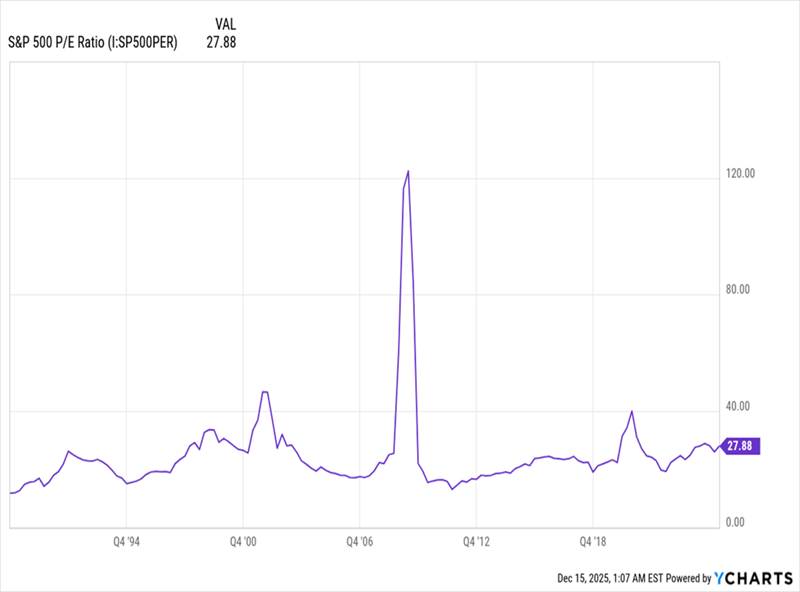

Why do I say that? Because the market’s price-to-earnings (P/E) ratio is high by historical standards.

Trouble is, most people are reading this popular indicator all wrong. That disconnect (and the fear it’s starting to cause, which could get worse in 2026) is setting up a nice short-term buying opportunity for us.

Valuation worries are being amplified by this chart from Apollo Global Management, which could easily become the poster child for fearful investors next year:

It comes from Apollo’s chief economist, Torsten Sløk, who notes that the estimated returns we should expect from the S&P 500 over the next decade are zero. This argument is based on that “high” P/E ratio I just mentioned. In other times where we saw a similar P/E ratio, according to Apollo’s analysis, we saw 10 years of flat to negative returns.

This argument has a logical end point: You may as well sell, because we’re in for a long period of flat returns at best.

Except the argument is wrong, and it’s not as logical as it looks.

The issue in the chart above is with what each of these dots represents. The S&P 500 as an entity has only existed since 1957, and the first ancestor to the index showed up about 100 years ago. So at most, we should have 10 dots here to cover 10 decades. Instead, we have many more than that because Apollo is using monthly reads of the index to fill out the chart and get more data points.

That’s not a small decision. It means that many of these dots are almost identical, just shifted forward a bit. For instance, the dots for November and December 2015 share 119 out of 120 months of the same data, so the chart looks like it has lots of separate data points, but it really doesn’t.

Statisticians call this “autocorrelation,” and it often results in charts that look like they have conclusive results when they really don’t say much at all.

Plus, let’s not forget that P/E ratios can be “high” for different reasons. Consider, for example, the spring of 2009, when the S&P 500’s P/E ratio shot above 120. I think we know how the following years played out.

Those Who Sold This “High” P/E Missed Years of Gains

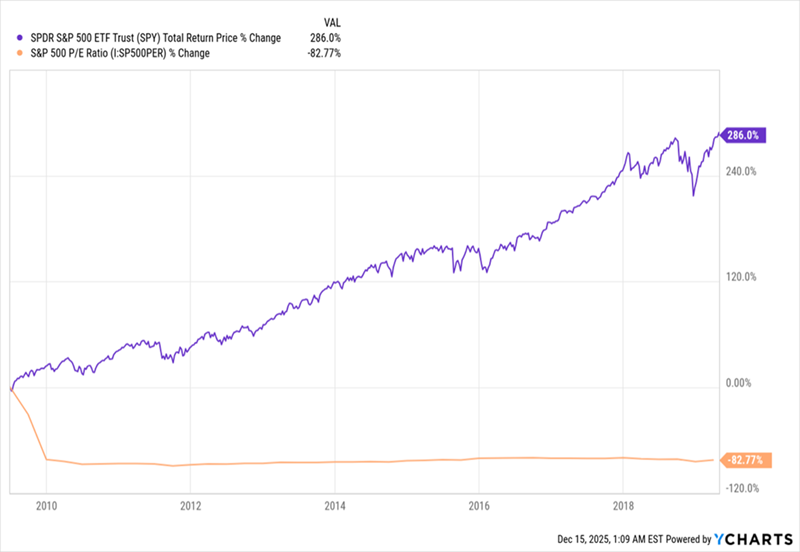

An investor who bought the S&P 500 at its highest P/E in living memory earned a 14.5% total return in the next decade, as the index’s P/E dropped to a more “normal” range.

S&P 500 Returns Soared as Valuations Dropped

In this case, the logic of “Don’t buy stocks when P/E ratios are high” doesn’t work. That’s because – and this is the real takeaway – P/E ratios can jump because prices get too high, sure. But they can also soar when the “E” part of the equation, earnings, slump, as they did in early 2009.

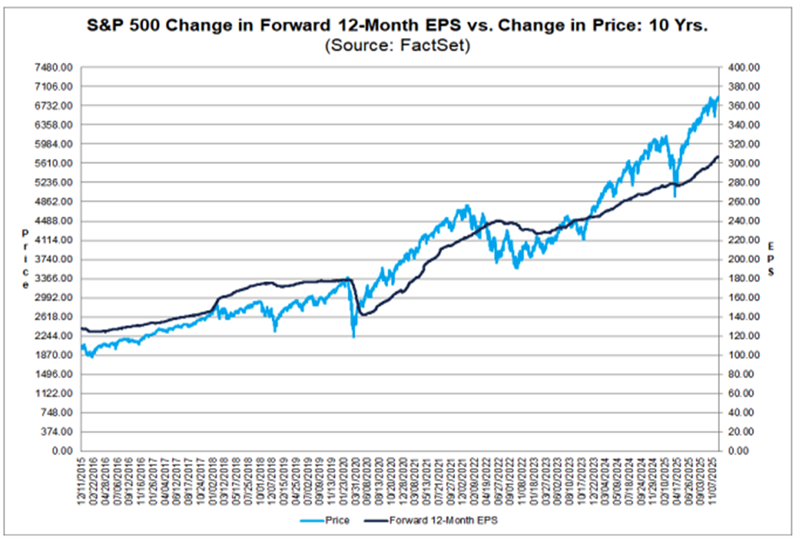

The real question, then, is “Are companies growing profits now?” The answer is yes.

In 2025, US companies saw a 12.1% rise in earnings per share from a year ago. This suggests stock prices should rise at least 12.1% just to maintain the same P/E ratio.

But since earnings growth is surging (an 11% rise in 2024, up from 1.1% in 2023 and 4.1% in 2022), and since revenue growth is unusually high (up 7% for 2025), we should see more than 12.1% yearly gains. That’s exactly what we’re seeing now. It wouldn’t be surprising if we keep seeing this in the future.

Flawed Logic Can Still Crash Markets

Nonetheless, most people put more weight on the “P” than the “E” in “P/E ratio,” so we should expect Apollo’s chart to be replicated, and even take hold in investors’ minds. If that happens, we should be cautious and ready to buy when others sell.

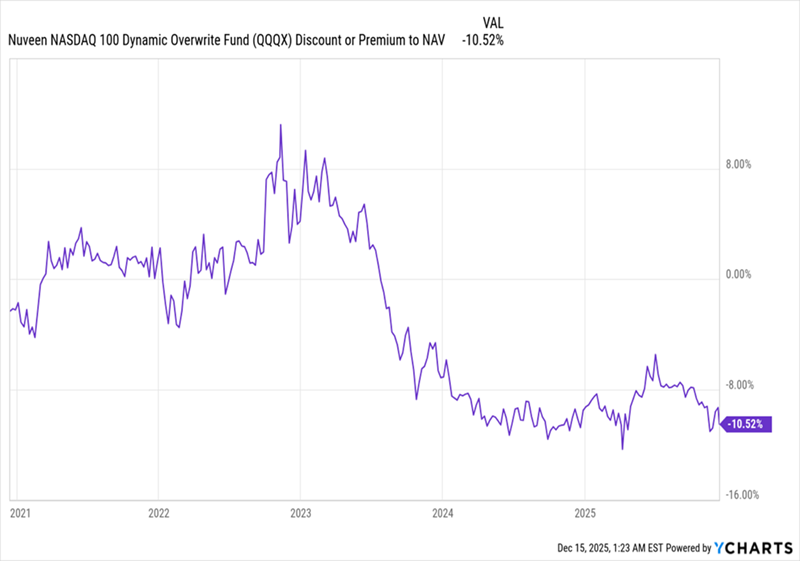

That’s why I’m starting to like funds like the Nuveen NASDAQ 100 Dynamic Overwrite Fund (QQQX). This one is a nice, cheap 8%-paying hedge against uncertainty. It sells covered-call options, or the opportunity to buy its stocks – the tech-focused names in the NASDAQ 100 – at a fixed future price and date.

No matter how these trades play out, QQQX keeps the fee, or “premium,” it charges for this right. Plus, its focus on the big-cap tech stocks of the NASDAQ also means this index tends to have higher volatility when markets get scared, juicing payouts further.

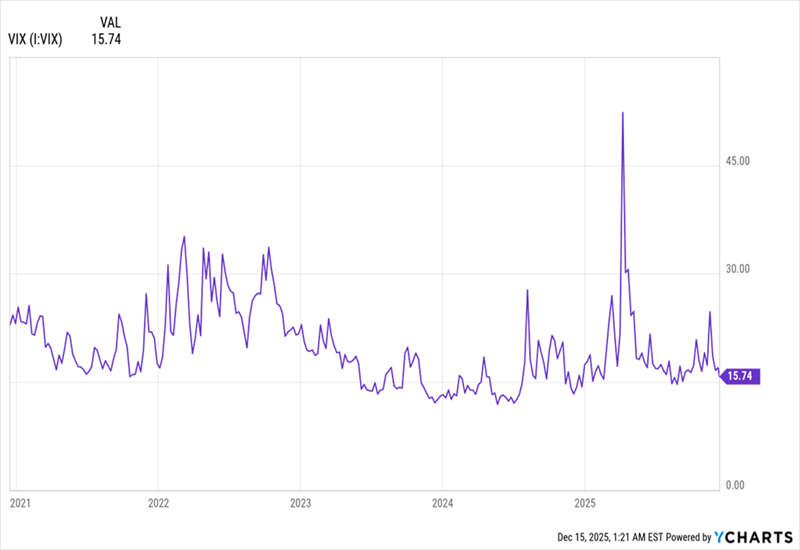

This strategy generates more premium cash in volatile markets. That’s the opposite of what we’re seeing now, as the VIX – the so-called “fear indicator” – remains low.

Market Stays Calm, Despite Investor Fears

In other words, we have a relatively calm market as I write this. That, in turn, means options are selling for cheaper than normal. And unusually cheap options compound the discounts to NAV on option-selling funds like QQQX. Right now, the fund’s discount is at a multi-year low.

Calm Markets Put QQQX on Sale

We saw that discount fade a bit in April, when volatility spiked, only for it to drop back to double-digits as markets remained calm and stocks steadily gained.

But if the narrative behind Apollo’s chart catches on, it could narrow that discount again, driving gains and bolstering QQQX’s 8% dividend. That possibility alone makes the fund a nice hedge against a market panic in 2026.

Foresight Environmental Infrastructure – Pushing on despite regulatory upheaval

17 December 2025

QuotedData

Richard Williams

Pushing on despite regulatory upheaval

The renewable energy infrastructure sector was dealt a blow last month as the government outlined plans to change the inflation link in existing clean energy incentives from the traditionally-higher RPI to CPI from next year – four years ahead of the planned changeover. The impact on Foresight Environmental Infrastructure (FGEN) would be marginal under this option (0.5% reduction in NAV), due to the diversified nature of its portfolio. However, a more radical second proposal was also put forward that would freeze uplifts until the perceived overpayments are clawed back. This move calls into question the UK government’s reputation as a sound investment partner for private capital and has the potential to damage long-term investment in UK infrastructure.

Meanwhile, FGEN’s portfolio continues to produce robust revenue streams – more than covering its progressive dividend, which currently yields almost 12% – and it will soon benefit as its growth assets become fully operational.

Progressive dividend from investment in environmental infrastructure assets

FGEN aims to provide its shareholders with a sustainable, progressive dividend, and to preserve capital values. It invests in a diversified portfolio of environmental infrastructure technologies, targeting projects characterised by long-term stable cash flows, secured revenues, and inflation linkage. Investment in these assets is driven by the need to address climate change and societal demand for sustainability.

12 months ending

Share price TR (%)

NAV total return (%)

Earnings per share (pence)

Adjusted EPS (pence)

Dividend per share (pence)

31/03/2021

6.9

1.5

1.5

6.7

6.76

31/03/2022

7.3

34.1

30.6

7.0

6.80

31/03/2023

12.2

13.1

14.9

6.7

7.14

31/03/2024

(15.8)

(1.8)

(2.1)

7.5

7.57

31/03/2025

(15.9)

0.6

(0.4)

8.6

7.80

Source: Bloomberg, Marten & Co

Market backdrop

UK government proposes change to inflation measure in existing incentives

Government proposals to change the inflation measure used in existing clean energy incentives have hit share prices across the renewable energy infrastructure sector. The Department of Net Zero and Energy Security launched a consultation in October on changing the inflation indexation calculation used in the renewables obligation (RO) and feed-in-tariffs (FIT) schemes from RPI to CPI.

Two options have been put forward to the industry. Option one is for a simple switch to take effect in 2026; four years before the planned 2030 changeover. Option two is more radical and would involve freezing the subsidy until 2035 to claw back what the government views as historic overpayments to renewable operators.

The impact on FGEN and the wider sector’s NAV of the two proposed outcomes is shown in Figure 1. FGEN’s diversified portfolio means that a lower percentage of its portfolio revenue (around 29%) is subject to RO and FIT incentives than its pure-play renewable peers, and as such, it should be the least impacted.

Figure 1: Estimated NAV impact of proposed change to RO and FIT inflation measure

Company

Option 1 (%)

Option 2 (%)

FGEN

(0.5)

(6.3)

Bluefield Solar

(2.0)

(10.0)

Foresight Solar

(1.6)

(10.2)

Greencoat UK Wind

(1.7)

(7.5)

NextEnergy Solar

(2.0)

(9.0)

Octopus Renewables Infrastructure

(1.1)

(4.0)

The Renewables Infrastructure Group

(0.5)

(2.2)

Source: Company announcements

Option one impact FGEN the least among peers

The manager estimates that option one would reduce FGEN’s NAV by 0.5p per share or 0.5%, while option two would knock 6.6p, or 6.3%, off the NAV. In both scenarios, the manager adds, dividend cover would not be materially impacted in the near-term.

The government is seeking to reduce energy bills and estimates that the changes under option one would see the average household bill for 2026-27 fall by just £4. This increases to £13 under the second option (before any costs such as an increase in the cost of capital).

The proposal follows the Office for National Statistics’s call for RPI to be dropped in favour of its preferred measure of CPIH, which includes housing costs, because RPI has tended to over-estimate inflation, thereby inflating contractual payments linked to it. The government has not commented on why it is not proposing a change to CPIH.

The government said that using CPI to annually adjust the RO and FIT buyout price (which were withdrawn in 2017-2019 but will continue until 2037 for renewable energy operators that built wind and solar farms under the schemes) was “proportionate and fair”, ensuring a stable and predictable return for generators and savings for consumers. It added that this would also prevent the risk of overpayment, as occurred when energy prices and inflation soared after Russia’s invasion of Ukraine in 2022.

QuotedData view

Move could erode investor confidence in UK government

To unilaterally change the terms of its contract with the renewables industry would not only undermine confidence in the sector and create an unwelcome precedent, but would also erode investor confidence in the UK government as a business partner – at a time when private investment in UK infrastructure is critically needed. The short-term saving on consumer bills is very likely to be overshadowed in the long term by a higher return demanded by infrastructure investors and developers to compensate for an unreliable partner. The UK government’s actions echoes a similar move by the Spanish government in the mid-2010s, which retrospectively altered the terms of existing renewable energy projects, replaced FITs with new schemes and levied a tax on electricity producers. Investor confidence was irreparably damaged and led to a wave of legal challenges that is still rumbling on today.

Interim results

FGEN reported a NAV of £652.7m or 104.7p per share at 30 September 2025 – a 1.7% fall over the six-month period. Factoring in dividends of 3.94p, this equated to a 2.0% NAV total return in the period.

Distributions received from projects over the six months was £39.7m (six months to September 2024: £46.6m). This underpinned the dividend with a coverage of 1.22x, and helped fund further share buybacks. The value of the portfolio fell £13.8m over the period, as shown in Figure 2.

Figure 2: FGEN portfolio valuation in £m, as at 30 September 2025

Source: FGEN, Marten & Co

Drivers of portfolio returns

Several factors impacted FGEN’s NAV. We detail these factors and their sensitivities below, beginning with inflation.

Inflation

Short-term RPI inflation assumptions raised 50bps

Inflation assumptions used to value FGEN’s portfolio (based on actual data and independent forecasts) were raised 50bps to 4.0% RPI inflation for 2025 and 3.5% for 2026 and then falling to 3% until 2030 and 2.25% thereafter. This resulted in a £6.1m uplift in NAV.

As mentioned earlier, it is likely that the inflation measure used on RO and FIT contracts will revert to CPI next year. FGEN’s CPI inflation assumptions are 2.75% in 2025 and 2.25% thereafter. CPI was at 3.6% at the end of October 2025. Figure 3 shows RPI and CPI inflation over the past five years.

Figure 3: UK RPI and CPI year-on-year (%)

Source: ONS, Marten & Co

Power prices

Power prices have fallen slightly over the six months, as shown in Figure 4, and a marginal change in forecasts for future electricity and gas prices compared to forecasts at 31 March 2025 resulted in a £6.5m reduction in FGEN’s NAV.

Figure 4: UK power prices

Source: Bloomberg – UK baseload

Fixed prices secured on the majority of portfolio

FGEN looks to fix the prices for most of its output, in an attempt to de-risk its exposure to volatile market prices. At 30 September 2025, the portfolio had price fixes secured at 63% for the Winter 2025/26 season, 24% for Summer 2026 season, and 25% for Winter 2026/27.

Over the life of the asset, an increase in electricity and gas prices of 10% would add £33.8m (or 5.4p) to NAV and a 10% fall in power prices would take off £33.1m (or 5.3p).

FGEN’s manager states that in the event that electricity prices fall to £40/MWh (they are currently at around £70/MWh) and gas prices fall by a corresponding amount, the company would maintain a resilient dividend cover for the next three financial years.

Discount rates

Figure 5: Long-term (10-year and 30-year) UK gilt yields

Source: Bloomberg, Marten & Co

The weighted average discount rate now sits at 10.1%

Despite a slight fall over recent months, UK gilt yields remain at elevated levels, as shown in Figure 5. The discount rates used to value FGEN’s portfolio remained unchanged. However, FGEN’s weighted average discount rate moved out slightly to 10.1% (from 9.7%), primarily due to ongoing investment into growth assets and increases in their values. There was no change to NAV resulting from changes to the discount rate.

A reduction in the discount rate of 0.5% would result in an uplift in value of £19.4m (or 3.1p per share), while a downward movement in the portfolio valuation of £18.2m (2.9p per share) would occur if discount rates were increased by the same amount.

Asset allocation

FGEN has one of the most diversified portfolios among its renewable energy infrastructure peers, with it currently invested in 10 sectors across 39 projects. The manager splits the portfolio into three key environmental infrastructure pillars: renewable energy generation (71% of the portfolio – wind, solar, AD, biomass, energy from waste, and hydropower); other energy infrastructure (11% – battery energy storage and low carbon transport assets); and sustainable resource management (18% – waste and water management assets and controlled environment assets).

Figure 6: Portfolio value split by sector, as at 30 September 2025

Figure 7: Portfolio split by remaining asset life as at 30 September 2025

Source: FGEN, Marten & Co

Source: FGEN, Marten & Co

Figure 6 displays FGEN’s portfolio by project type, as at 30 September 2025. The weighted average remaining asset life of the portfolio was 16.2 years, although the manager feels it is being conservative in this area, especially in its AD portfolio.

Potential Life extensions for AD assets could result in a substantial valuation uplift

These are currently conservatively valued over the life of the renewable heat incentive subsidy (RHI) that they receive. The manager says that there is growing evidence, including several market transactions, pointing to valuing these AD facilities beyond the end of the tariffs and possibly into perpetuity. It has modelled extension scenarios for its AD portfolio, including revenues being derived from corporate offtakes, green certificates and/or a lower level of government support mechanisms. It has modelled that this would result in a substantial valuation uplift of between £10m and £20m (1.6p to 3.2p) and significantly extend the weighted average life of the portfolio.

Some clarity is required on the position that biomethane will take in the wider net zero and energy transition plans in the UK, with the government currently developing a biomethane policy framework, which the manager expects to be released next year.

The majority of its portfolio (88%) is located in the UK, with the 12% outside the UK accounted for by FGEN’s Italian and Norwegian investments.

Figure 8: Portfolio split by operational status as at 30 September 2025

Figure 9: Net present value of future revenues by type as at 30 September 2025

Source: FGEN, Marten & Co

Source: FGEN, Marten & Co

FGEN’s construction exposure has reduced to 3%, with the Rjukan asset transferring to early-stage operations (detailed below).

The top 10 largest assets make up 54% of the total portfolio value. Figure 10 details the assets in FGEN’s portfolio, at 30 September 2025. The company has low exposure to individual assets, with no asset accounting for more than 10% of the portfolio.

Figure 10: FGEN portfolio1 of projects by type, as at 30 September 2025

Asset

Location

Type

Ownership

Capacity(MW)

Commercial operations date

Renewable energy generation

Bilsthorpe

UK (Eng)

Wind

100%

10.2

Mar 2013

Burton Wold Extension

UK (Eng)

Wind

100%

14.4

Sep 2014

Carscreugh

UK (Scot)

Wind

100%

15.3

Jun 2014

Castle Pill

UK (Wal)

Wind

100%

3.2

Oct 2009

Dungavel

UK (Scot)

Wind

100%

26.0

Oct 2015

Ferndale

UK (Wal)

Wind

100%

6.4

Sep 2011

Hall Farm

UK (Eng)

Wind

100%

24.6

Apr 2013

Llynfi Afan

UK (Wal)

Wind

100%

24.0

Mar 2017

Moel Moelogan

UK (Wal)

Wind

100%

14.3

Jan 2003 & Sep 2008

New Albion

UK (Eng)

Wind

100%

14.4

Jan 2016

Wear Point

UK (Wal)

Wind

100%

8.2

Jun 2014

Biogas Meden

UK (Eng)

Anaerobic digestion

49%

5.0

Mar 2016

Egmere Energy

UK (Eng)

Anaerobic digestion

49%

5.0

Nov 2014

Grange Farm

UK (Eng)

Anaerobic digestion

49%

5.0

Sep 2014

Icknield Farm

UK (Eng)

Anaerobic digestion

53%

5.0

Dec 2014

Merlin Renewables

UK (Eng)

Anaerobic digestion

49%

5.0

Dec 2013

Peacehill Farm

UK (Scot)

Anaerobic digestion

49%

5.0

Dec 2015

Rainworth Energy

UK (Eng)

Anaerobic digestion

100%

5.0

Sep 2016

Vulcan Renewables

UK (Eng)

Anaerobic digestion

49%

5.0

Oct 2013

Warren Energy

UK (Eng)

Anaerobic digestion

49%

5.0

Dec 2015

Amber

UK (Eng)

Solar

100%

9.8

Jul 2012

Branden

UK (Eng)

Solar

100%

14.7

Jul 2013

CSGH

UK (Eng)

Solar

100%

33.5

Mar 2014 & Mar 2015

Monksham

UK (Eng)

Solar

100%

10.7

Mar 2014

Pylle Southern

UK (Eng)

Solar

100%

5.0

Dec 2015

Codford Biogas

UK (Eng)

Waste anaerobic digestion

100%

3.8

2014

Bio Collectors

UK (Eng)

Waste anaerobic digestion

100%

11.7

Dec 2013

Cramlington Renewable Energy Developments

UK (Eng)

Biomass combined heat and power

100%

32.0

2018

Energie Tecnologie Ambiente (ETA)

Italy

Energy-from-waste

45%

16.8

2012

Northern Hydropower

UK (Eng)

Hydropower

100%

2.0

Oct 2011 & Oct 2017

Yorkshire Hydropower

UK (Eng)

Hydropower

100%

1.8

Oct 2015 & Nov 2016

Other energy infrastructure

West Gourdie

UK (Scot)

Battery storage

100%

n/a

May 2023

Clayfords

UK (Scot)

Battery storage

50%

n/a

Pre-construction

Sandridge

UK (Eng)

Battery storage

50%

n/a

Under construction

Asset

Location

Type

Ownership

Capacity(MW)

Commercial operations date

CNG Fuels

UK (Eng)

Low carbon transport

Minority2

n/a

Various

Sustainable resource management

Glasshouse

UK (Eng)

Controlled environment

10%

n/a

Mar 2025

Rjukan

Norway

Controlled environment

25%

n/a

Early stage operations

ELWA

UK (Eng)

Waste management

80%

n/a

2006

Tay

UK (Scot)

Wastewater treatment

33%

n/a

Nov 2001

Source: FGEN, Marten & Co. Note 1) excludes projects in FEIP’s portfolio. Note 2) FGEN holds 25% of CNG Foresight Holdings Ltd, which owns 60% of the shares in CNG Fuels Ltd (FGEN look-through interest 15%) and holds £150.15m in 10% preferred return investments issued by CNG Fuels (FGEN interest £37.5m).

As part of FGEN’s re-focus on core environmental assets, its three growth assets – the two controlled environment projects (the Glasshouse and Rjukan) and the CNG portfolio – will be sold over the medium term once operations have ramped up and their valuation uplifts booked. We profiled all three in our previous note, a link to which can be found on page 16.

The valuation of Rjukan asset rose as it transitions from construction to operational

All three assets have progressed in line with the manager’s expectations. The value of the Rjukan land-based trout farm in Norway rose as it transitioned from construction to early-stage operational, with the first harvest and sales in the summer. As such, it moved from being valued at cost to DCF method, and increased in value by £2.9m over six months. FGEN’s manager says the valuation will increase further as operations are ramped up.

Operations at CNG Fuels also grew, with volumes of gas dispensed (+15%), truck numbers (+18%) and pricing (+21%) all up significantly over the year. This contributed to a £2.2m uplift in value for the asset.

Meanwhile, the Glasshouse secured further sales and market penetration, with customers now including six of the eight largest clinics in the UK. The business target is being cash flow break-even in the new year, ahead of a full ramp-up by 2026/27.

Portfolio activity

FGEN sold its stake in a BESS project and is considering options on another BESS asset

There has been very little activity in the way of acquisitions and disposals since our last note in July. However, FGEN did sell its 50% stake in its Lunanhead battery energy storage (BESS) project for £1.25m, in line with book value, in August. The sale was made in preference to making a follow-on investment in the project. The manager says that it is continuing to explore options for the Clayfords BESS asset, in which it owns a 50% stake.

The company made several follow-on investments over the six months totalling £7.9m, including into the CNG platform and into Vulcan Renewables.

FGEN’s solar assets exceeded generation targets by 6.2% in the period, but was offset by disappointing performance of its wind assets, which was 6.5% below target. FGEN’s largest asset, the Cramlington biomass scheme (which accounts for 9% of portfolio value), generated 44.3% below target in the six months to the end of September, due to a six-week extension of a planned outage in July. FGEN’s manager has advanced a liquidated damages claim with the O&M contractor and expects the shortfall to reduce to 9.5% once the minimum expected compensations are received.

Performance

FGEN’s NAV returns over the past three years have been flat, despite substantial headwinds that it and the renewable energy infrastructure sector have faced over the period contributing to portfolio valuation declines. Robust portfolio revenues have allowed for a progressive dividend distribution, which has offset the fall in asset value.

Figure 11: FGEN NAV TR over five years to 30 September 2025

Source: Bloomberg, Marten & Co

Figure 12: FGEN cumulative performance to 30 September 2025

3 months (%)

6 months (%)

1 year (%)

3 years (%)

5 years (%)

FGEN NAV total return

2.0

2.1

2.7

1.9

52.4

FGEN share price total return

(10.5)

2.7

(14.6)

(24.8)

(14.8)

Source: Bloomberg, Marten & Co

Peer group

Figure 13: AIC renewable energy infrastructure sector comparison table, as at 15 December 2025

Market cap (£m)

Premium/(discount) (%)

Yield(%)

Ongoing charge (%)

FGEN

422

(35.3)

11.8

1.24

Aquila Energy Efficiency

20

(46.1)

0.0

3.80

Aquila European Renewables Income

121

(38.3)

14.1

1.10

Bluefield Solar Income

401

(41.1)

13.2

1.02

Ecofin US Renewables Infrastructure

21

(50.3)

2.3

2.30

Foresight Solar

358

(38.7)

12.5

1.17

Gore Street Energy Storage Fund

272

(40.2)

13.0

1.38

Greencoat Renewables

683

(30.4)

9.7

1.18

Greencoat UK Wind

2,106

(31.5)

10.6

0.95

Gresham House Energy Storage

461

(30.4)

6.8

1.29

Hydrogen Capital Growth

19

(59.0)

0.0

2.53

NextEnergy Solar

291

(42.9)

16.7

1.18

Octopus Renewables Infrastructure

314

(39.8)

10.4

1.21

SDCL Efficiency Income

572

(40.9)

12.0

1.16

The Renewables Infrastructure Group

1,651

(36.9)

10.8

1.04

US Solar Fund

79

(45.2)

10.1

1.54

VH Global Energy Infrastructure

249

(41.4)

9.2

1.50

Peer group median

314

(40.2)

10.6

1.21

FGEN rank

6/17

4/17

7/17

10/17

Source: QuotedData website

You can access up-to-date information on FGEN and its peers on the QuotedData website.

FGEN has one of the broadest remits of the 17 companies that comprise the members of the AIC’s renewable energy sector. Most of these funds are focused on solar or wind or some combination of the two. Two of these funds are focused solely on energy storage. There is variation of geographic exposure within the peer group too, with a number of funds that are heavily exposed to the North American market (which has a different risk/reward structure).

The sector has been shrinking over the past 12 months through a combination of private acquisitions (taking advantage of the wide discounts in the sector) or through managed wind-downs. We have lost Downing Renewables & Infrastructure since our last note, while Aquila Energy Efficiency and Hydrogen Capital Growth are in a managed wind-down. Meanwhile, Bluefield Solar Income put itself up for sale in November after shareholders voted against a proposal for it to merge with its manager, Bluefield Partners.

The proposed merger of The Renewables Infrastructure Group (TRIG) and infrastructure trust HICL Infrastructure (which are both managed by InfraRed Capital) was abandoned in early December after a HICL shareholder revolt. TRIG is facing a continuation vote in 2026.

FGEN is one of the larger funds within this peer group. Whilst its discount is narrower than most, the whole sector derated following the government proposals on bringing forward a change in the inflation measure on ROs and FITs. Wide discounts have distorted yields across the sector. Nevertheless, FGEN’s yield is highly attractive, with coverage of 1.22x. Its ongoing charges ratio ranks middle of the pack, but is expected to fall when the impact of a reduction in the management fee is felt.

Figure 14: AIC renewable energy infrastructure sector NAV total return performance comparison table, as at 1 December 2025

1 year(%)

3 years(%)

5 years(%)

10 years(%)

FGEN

2.7

0.6

8.8

7.3

Aquila Energy Efficiency

(19.3)

(7.1)

–

–

Aquila European Renewables Income

(28.3)

(14.5)

(5.7)

–

Bluefield Solar Income

(2.8)

(0.5)

6.8

7.8

Ecofin US Renewables Infrastructure

(39.9)

(25.1)

–

–

Foresight Solar

(2.4)

(0.5)

8.3

7.1

Gore Street Energy Storage Fund

(6.0)

(0.7)

4.7

–

Greencoat Renewables

3.6

4.2

5.9

–

Greencoat UK Wind

(5.0)

9.3

9.7

9.4

Gresham House Energy Storage

6.1

(6.7)

6.7

–

Hydrogen Capital Growth

(59.1)

(24.4)

–

–

NextEnergy Solar

(0.7)

(2.9)

5.3

5.6

Octopus Renewables Infrastructure

0.8

1.8

5.5

–

SDCL Efficiency Income

1.9

(0.4)

2.8

–

The Renewables Infrastructure Group

(3.7)

(0.9)

5.4

7.4

US Solar Fund

(16.5)

(11.2)

(3.0)

–

VH Global Energy Infrastructure

1.5

3.5

–

–

Peer group median

(2.8)

(0.7)

5.5

7.3

FGEN rank

3/17

5/17

2/13

4/6

Source: QuotedData website

Premium/(discount)

FGEN’s discount had been narrowing from all-time lows at the start of this year; however, the government proposals to bring forward the change in the inflation measure for incentives saw the discount widen (along with the wider peer group).

Over the year to 30 September 2025, FGEN’s shares traded in range of a 17.4% and a 38.8% discount to NAV, and averaged a discount of 28.6%. FGEN’s discount at 15 December 2025 was wider than its 12-month average at 35.3%.

Figure 15: FGEN premium/(discount) (%) over five years to 30 September 2025

FGEN invests in a diversified portfolio of private infrastructure assets that deliver stable returns, long-term predictable income, and opportunities for growth while supporting the drive towards decarbonisation and sustainable resource management.

FGEN invests in three core areas of environmental infrastructure: renewable energy generation, other energy infrastructure, and sustainable resource management. Renewable energy generation investments include wind, solar, AD, biomass, energy from waste, and hydropower. Other energy infrastructure assets include battery energy storage and low carbon transport. Sustainable resource management includes wastewater, waste processing, and sustainable solutions for food production such as agri- and aquaculture-controlled environment projects.

FGEN’s portfolio is diversified across complementary sectors, technologies and geographies which substantially de-risks it from exposure to fluctuations in weather patterns and helps differentiate the company from its peers.

FGEN’s mandate allows it to invest in emerging areas of environmental infrastructure, provided that they are sufficiently mature and display strong infrastructure characteristics.

FGEN’s AIFM is Foresight Group LLP (Foresight). Foresight is one of the best-resourced investors in renewable infrastructure assets, with £13.6bn of AUM at 30 September 2025. This includes Foresight Solar Fund, which sits in FGEN’s peer group. Foresight has a highly experienced and well-resourced global infrastructure team with 185 infrastructure professionals managing around 5.0GW of energy infrastructure. It is a global business, with offices in seven countries. The co-lead managers for FGEN are Chris Tanner, Edward Mountney and Charlie Wright.

SWOT analysis and bull vs bear case

Figure 16: SWOT analysis for FGEN

Strengths

Weaknesses

Continued robust revenues from core portfolio

Sensitive to market sentiment and interest rate volatility

Progressive dividends, with comfortable coverage by income

Opportunities

Threats

Valuation uplifts from growth assets moving to fully operational

Potential discount widening with Option 2 of government proposal

35%+ discount to NAV could narrow if sentiment improves and interest rates fall

Source: Marten & Co

Figure 17: Bull vs bear case for FGEN

Aspect

Bull case

Bear case

Performance

Capital appreciation of growth assets as operations ramp up. Core portfolio continues to produce strong cash flows

Growth assets take longer than anticipated to become fully operational. Energy prices dive, impacting income streams

Dividends

Strong track record of increases, which the board are committed to continuing

Increases potentially not sustainable if conditions change

Outlook

Structural increase in renewable energy demand looks set to continue

Government scales back climate commitments

Discount

FGEN’s wide discount could narrow as interest rates subside and sentiment towards the sector turns positive

The discount could widen further due to detrimental government proposals

Source: Marten & Co

IMPORTANT INFORMATION

This marketing communication has been prepared for Foresight Environmental Infrastructure Plc by Marten & Co (which is authorised and regulated by the Financial Conduct Authority) and is non-independent research as defined under Article 36 of the Commission Delegated Regulation (EU) 2017/565 of 25 April 2016

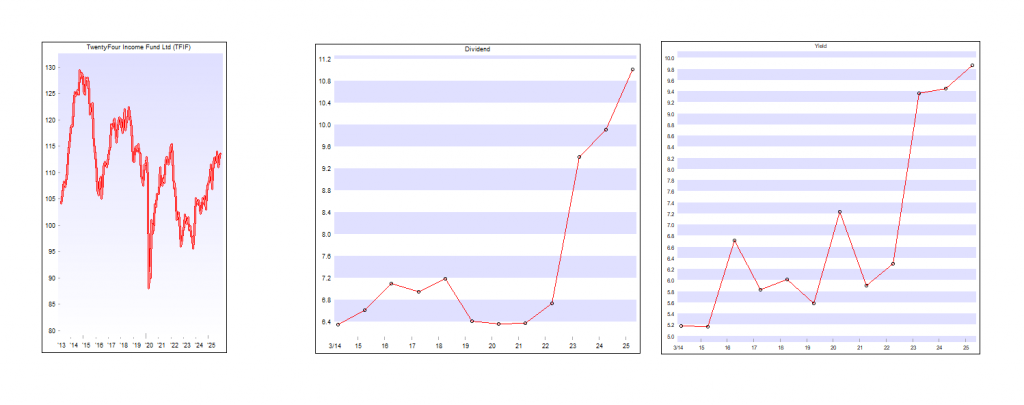

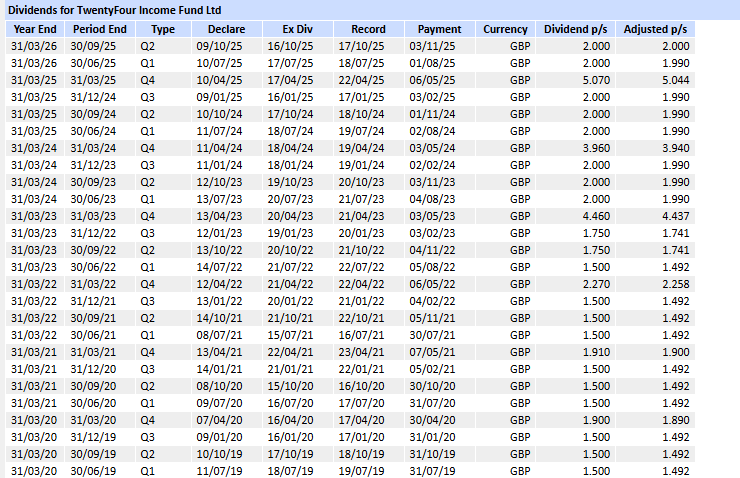

I’ve bought back for the Snowball 8802 shares in TFIF Twenty Four Income Fund for 10k.

With the UK stock market closing over the Xmas and New Year period, I would prefer to be making a small contribution to the Snowball rather than the cash sitting in the account earning nothing. All baby steps.

Current yield 8% which could be enhanced if they pay a higher dividend in April, trading at a small premium to their NAV.

2026 is shaping up to be the best year for bond investors in many years. Washington wants rates down, housing up and borrowing cheap again.

This wish list is wildly bullish for bonds.

Fed Chair Jay Powell has delivered two rate cuts to end the year, with more to follow. Whether or not Powell personally delivers them doesn’t matter to us. Powell is on his way out. But the Fed show will go on, with a ringmaster ready to roll.

President Trump has confirmed his shortlist for the next Fed Chair is down to “The Two Kevins”: Kevin Hassett and Kevin Warsh.

The implication for bond investors is the same, regardless of which Kevin gets the nod:

Kevin Hassett, the “cut early, cut often” candidate, has spent 20 years arguing the Fed moves too slowly. He knows the assignment: Cut!

Kevin Warsh, a historic hawk, has aligned himself with Trump’s mandate. He told the President personally that borrowing costs must come down.

Whichever Kevin gets the job, the result is already in the cards. More cuts are coming.

This “Kevin accommodation” is the catalyst our bond funds have been waiting for. PIMCO and DoubleLine don’t just buy bonds for their closed-end funds (CEFs)—they borrow money to buy more bonds.

This is called leverage. For the last three years, high rates made leverage a dead weight on these funds. In 2026, falling rates will burn that weight like rocket fuel. Every quarter-point cut lowers the funds’ borrowing bill and widens the spread between what they pay and what their portfolios earn.

The “pure plays” on lower borrowing costs are PIMCO Dynamic Income (PDI) and PIMCO Dynamic Income Opportunities (PDO). With more leverage than your typical bond fund, PDI and PDO have felt high rates more acutely than their peers.

They will be happy to see either Kevin in action and experience the relief of falling rates. PDI and PDO have been paying 5-6% on their credit lines. Cutting back towards 3-4% restores the profitability these funds enjoyed in their late 2010s bull run.

PIMCO is the 800-pound gorilla when it comes to bond trading. They don’t just buy bonds; they bully the market. PDI yields a massive 14.9% and uses 32% leverage. Yes, it has been paying the price for high rates, but now it is ready to run, thanks to Fed cuts. Its younger sibling PDO, meanwhile, employs 35% leverage and yields 11%. Not shabby!

If PIMCO is the bond bully, then Jeffrey Gundlach is the fixed-income sniper. The “Bond God” isn’t afraid to buy “unloved” assets for DoubleLine Income Solutions (DSL). His edge is simple: when emerging-market debt gets dumped, he buys it at 60-70 cents on the dollar and clips big yields while he waits for appreciation.

As the US dollar softens further from falling rates, these global bonds are positioned to bounce. They act as a high-yield hedge to greenback weakness. DSL yields 11.7% while its more conservative sister fund DoubleLine Yield Opportunities Fund (DLY) pays 9.6%. They use 22% and 15% leverage respectively—conservative numbers.

Speaking of a softer dollar, AllianceBernstein Global High Income (AWF) is a direct play on it. The fund owns high-income debt from around the world. In a falling-rate environment, the dollar typically weakens—making AWF’s foreign-bond income worth more when converted back into dollars. It’s a nice currency kicker on top of a 7.3% yield.

Finally, Muni Bondland is the place for leverage. Safe muni bonds take advantage of the security in their sector by borrowing to buy more. The leverage ratio for Nuveen Municipal Credit Income (NZF) is 41%, so this fund is about to save big time:

Plus, that 7.5% yield from NZF gets a tax “hall pass” from Uncle Sam. For a top-bracket taxpayer, that 7.5% tax-free income is worth 12.6% in taxable terms. It’s essentially an S&P-beating return from safe muni bonds.

With 12% to 14.9% yields in hand, we don’t need to chase AI moonshots or sweat over quarterly earnings reports. Retirement is no longer a spreadsheet problem. We just need to buy the right bonds before vanilla investors realize the leverage game has flipped.

When we can lock in 14.9% yields, our retirement math gets very simple.

The Retirement Strategy That’s Failing Millions—Even the Ones Who “Did Everything Right”

In this exclusive briefing, you’ll discover:

Why “safe” income strategies are failing right now

How inflation, fluctuating yields and policy chaos are gutting retirement plans

The hidden risk that quietly drains retirement accounts (and how to avoid it)

A contrarian dividend blueprint yielding up to 11%—without touching principal

How to turn $500K into a stable income stream that could last decades

Dear Reader,

You saved. You invested. You followed the “rules.”

And yet here you are—uneasy.

Wondering if you really can afford to retire. Or stay retired.

And who could blame you?

One minute, inflation’s the threat. The next, it’s recession.

A new headline from Washington sends markets whipsawing the very same day.

And the broader economy? It’s bloated with debt and only getting worse.

We touch new all-time highs, then the market zigzags like a drunk squirrel—making it feel impossible to plan, let alone sleep at night.

So you start looking for stability. Maybe trim a position here. Tap a bit of principal there. Just for now.

But that’s exactly how it begins.

And once you start selling shares to supplement your income, you’re on a slippery slope.

A slow-motion wealth drain most retirees don’t realize they’re in—until it’s too late.

I call it…

The Share Selling “Death Spiral”

Some financial advisors (who are not retired themselves, by the way) say that you can safely withdraw and spend, say, 4% of your retirement portfolio every year. Or whatever percentage they manipulate their spreadsheet to say.

Problem is, in reality, every few years you’re faced with a chart that looks like this.

Apple’s Dividend Was Fine – Its Stock Wasn’t

As you can see, the dividend (orange line above) is fine — growing, even — but you’re selling at a 25% loss!

In other words, you’re forced to sell more shares to supplement your income when they’re depressed.

Remember the benefits of dollar-cost averaging that built your portfolio? You bought regularly, and were able to buy more shares when prices were low?

In this case, you’re forced to sell more shares when prices are low.

When shares rebound, you need an even bigger gain just to get back to your original value.

The Only Reliable Retirement Solution

Instead of ever selling your stocks, you should instead make sure you live on dividends alone so that you never have to touch your capital.

This is easier said than done, and obviously the more money you have, the better off you are. But with yields still pretty low, even rich folks are having a tough time living off of interest today.

And you can actually live better than they can off of a (much) more modest nest egg if you know where to look for lesser-known, meaningful and secure yield.

I’m talking about annual income of 8%, 9% or even 10%+ so that you’re banking $50,000 (and potentially more) each year for every $500,000 you invest.

You and I both know an income stream like that is a very nice head start to a well-funded retirement.

And it’s totally scalable: Got more? Great!

We’ll keep building up your income stream, right along with your additional capital.

And you’ll never have to touch your nest egg capital – which means you won’t have to worry about or running out of money in retirement, or even the day-to-day ups and downs of the stock market.

The only thing you need to concern yourself with is the security of your dividends.

As long as your payouts are safe, who cares if your stock prices swing up or down on a given day?

Most investors know this is the right approach to retirement.

Problem is, they don’t know how to find 8%, and 10% yields to fund their lives.

And when they do find high yields, they’re not sure if these payouts are safe. Will the company or fund have enough cash flow to pay the dividends into the future?

And how sensitive are these payouts to the latest headline, Fed policy change or unrest on the other side of the globe?

We’ll talk specific stocks, funds and yields in a moment.

But first, a bit about myself.

My name is Brett Owens. I first started trading stocks in college, between classes at Cornell.

I graduated cum laude with an industrial engineering degree — which is actually pretty popular with Wall Street recruiters.

But I couldn’t stand the thought of grinding it out in a cubicle for 80 hours a week. So I moved to San Francisco and got into the tech scene.

A buddy and I started up two software companies that serve more than 26,000 business users.

The result was a nice chunk of change coming in … and I had to decide what to do with my money.

I had seen plenty of young “techies” come into sudden cash and burn through their windfall in a year, ending up right back where they started.

That was NOT going to be me. I already had dreams of living off my wealth one day, decades before I retired.

I got plenty of cold calls from brokers wanting to “help” me. But I knew that nobody would care as much about my money as me.

So I went out on my own and invested my startup profits in dividend-paying stocks.

I’ve been hunting down safe, stable and generous yields ever since, growing my wealth with vehicles paying me 8%, 9%, even 10%+ dividends.

Over the past 10+ years, I’ve been writing about the methods I use to generate these high levels of income.

Today I serve as chief investment strategist for Contrarian Income Report — a publication that uncovers secure, high-yielding investments for thousands of investors.

Since inception, my subscribers have enjoyed dividends 5 times (and much more!) the S&P 500 average, plus big annualized gains!

And that brings me to a crucial piece of advice…

The ONE Thing You Must Remember

If I could leave you with just one nugget of investing wisdom today, it would be to NEVER overlook the incredible wealth-building power of dividends.

Few investors realize how important these unglamorous workhorses actually are.

Here’s a perfect example…

If you put $1,000 in the dividend-paying stocks of the S&P 500 back in 1973, you would have had $96,970 by 2023, or 97x your money.

But the same $1,000 in the non-dividend payers would have grown to just $8,990 — 91% less.

That’s why I’m a dividend fan.

The stock market is a fantastic wealth-building machine, but it doesn’t always go straight up!

There have been plenty of 10-year periods where the only money investors made was in dividends.

And that’s what gives us dividend investors such an edge.

When you lock in an 8%+ yield, you’re booking an income stream that’s bigger than the stock market’s long-term average return right off the bat.

Of course you can’t just buy every ticker symbol out there with a flashy yield, or you’ll get burned pretty fast.

So let’s wipe the false promises of mainstream finance from our minds and start thinking the “No Withdrawal” way…

Step 1: Forget “Buy and Hope” Investing

Most half-million-dollar stashes are piled into “America’s ticker” SPY.

The SPDR S&P 500 ETF (SPY) is the most popular symbol in the land. For many 401(K)’s, this is all there is.

And that’s sad for two reasons.

First, SPY yields just 1.1%. That’s $5,500 per year on $500K invested… poverty level stuff.

Second, consider 2022 for a moment (and only a moment, I promise!).

SPY was down nearly 20% that year. That is no bueno, because that $500K would have been reduced to $400K.

The last thing we want to do is lose the money we’re getting in dividends (or more) to losses in the share price. Which is why we must protect our capital at all costs.

Step 2: Ditch 60/40, Too

The 60/40 portfolio has been exposed as senseless.

Retirees were sold a bill of goods when promised that a 60% slice of stocks and 40% of bonds would somehow be a “safe mix” that would not drop together.

Oops.

Inflation — plus an aggressive Federal Reserve, plus a (thus far) persistently steady economy — drop-kicked equities and fixed income before they went on a serious bull run in 2023, 2024 and into 2025 (with a brief interruption for the April “tariff tantrum.”)

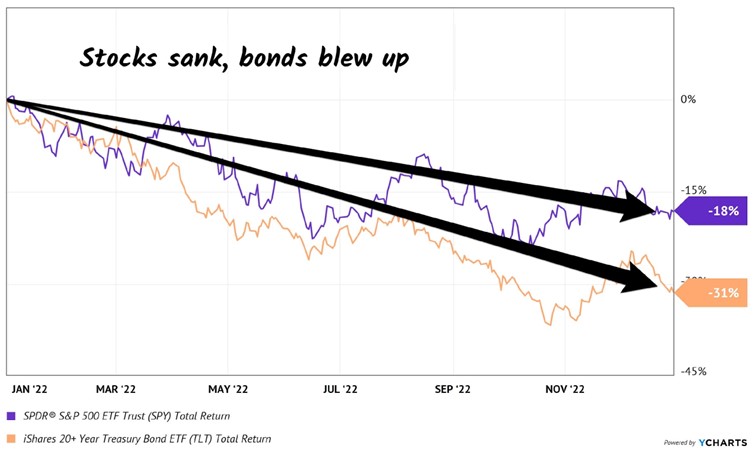

It just goes to show that bonds are not the haven guaranteed by the 60/40 high priests. They could easily plunge just as hard (or harder) than stocks in the next economic crisis.

Just like they did in 2022 (sorry, we’re only going to spend one more second on that disaster of a year). US Treasuries plunged, which resulted in the iShares 20+ Year Treasury Bond ETF (TLT) getting tagged.

Sure, it still paid its dividend. But even including payouts, the fund was down 31% — worse than the S&P 500. Ouch!

When stocks and bonds are dicey, where do we turn? To a better bet.

A strategy to retire on dividends alone that leaves that beautiful pile of cash untouched.

My colleague Tom Jacobs and I literally wrote the book on a dividend-powered retirement.

In How to Retire on Dividends: Earn a Safe 8%, Leave Your Principal Intact, we outline our “no withdrawal” approach to retirement:

Save a bunch of money. (“Check.”)

Buy safe dividend stocks with big yields

Enjoy the income while keeping the original principal intact.

To make that nest egg last, and our working life worthwhile, we really need yields in the 7% to 10% range. We typically don’t see these stocks touted on Bloomberg or CNBC, but they are around.

Of course, there are plenty of landmines in the high-yield space. Some of these stocks are cheap for a reason. Which is why we need to be contrarian when looking for income.

We must identify why a yield is incorrectly allowed to be so high. (In other words, we need to figure out why the stock is priced so cheaply!)

As I write, the top 10 payers in my Contrarian Income Report portfolio yield about 10.6% on average.

On every million dollars invested, this dividend collection is spinning off an incredible $106,000 every single year!

And you don’t have to be a millionaire to take advantage of this strategy.

A $750k nest egg will generate $79,500 annually…

$500K could hand you $53,000…

You get the idea.

The important thing is that these yields are safe, which creates stability for the stock (and fund) prices attached to them.

We want our income, with our principal intact.

It’s really the only way to retire comfortably, without having to stare at stock tickers all day, every day.

Now, many blue-chip yields are reliable. They just need to hit the gym and bulk up a bit. Here’s how we take perfectly good, yet modest, dividends and make them into braggarts.

Step 4: Supersize Those Yields

Mastercard (MA) is a near-perfect dividend stock. Its payout is always climbing, having nearly doubled over the last five years. (MA shareholders, you can thank every business that accepts Mastercard for your “pennies on every dollar” rake.)

Tap, tap, tap. Remember cash? Me neither. Another 2020 casualty, with Mastercard making a few dimes or dollars on every plastic transaction.

The cashless trend has been in motion for years. But international growth prospects remain huge. Just a few years ago, 80%+ of transactions in Spain, Italy and even tech-savvy Japan were in cash.

We expect more dividend hikes as more cash turns to plastic. Or skips plastic entirely and goes straight to e-transfers. Mastercard and close cousin Visa (V) nab a nice piece of that action, too.

The only chink in MA’s armor? Everyone knows it is a dynamic dividend stock. So it only yields 0.5%. Investors keep bidding it higher, knowing that the next dividend raise is just around the corner.

So, the compounding of those hikes makes MA a great stock for our kids and grandkids. You and I, however, don’t have the time to wait for 0.5% to grow. And $2,500 on a $500K investment simply won’t get it done.

Let’s instead consider top-notch closed-end fund (CEF) Gabelli Dividend & Income Trust (GDV), managed by legendary value investor Mario Gabelli.

Mastercard is one of Gabelli’s largest holdings. But we income investors would prefer GDV because it boasts a healthy dividend right around 6.4%, paid monthly, nearly 13 times what Mastercard pays (and this is low in CEF-land; other funds, like the next one we’ll talk about, pay nearly double that).

And as I write this, thanks to the conservative folks who buy CEFs, we have a rare opportunity to buy Mario’s portfolio for just 89 cents on the dollar.

Yup, GDV trades at an 11% discount to its net asset value, or NAV. It’s a way to boost MA’s payout and snag a discount, too.

Where does this discount come from?

CEFs are like their mutual fund cousins, with one exception: they have fixed pools of shares, so they can (and do) trade higher and lower than their NAVs, or “fair” values (the value of their holdings minus any debt).

As contrarians, we can step in when they are temporarily out of favor, like after a pullback, when liquidity is low, and buy them at generous discounts.

GDV holds more blue-chip dividend payers alongside MA, such as American Express (AXP), Microsoft (MSFT) and JPMorgan Chase & Co. (JPM). And with GDV, we have an opportunity to purchase them at an 11% discount.

These high-quality stocks wouldn’t normally qualify for our “retire on $500K” portfolio because everyone in the world knows they are strong long-term investments.

Even though these companies are constantly raising their dividends, constant demand for their shares keeps their prices high (and current yields low). So they never meet our current-yield requirement.

GDV does. The fund pays a monthly dividend that adds up to a nice 6.4% annual yield.

Let me give you one more idea (and this is where that much larger payout comes in): the Eaton Vance Tax-Managed Global Diversified Equity (EXG) is another CEF with a similar blue-chip dividend portfolio.

But EXG generates even more income than GDV by selling covered calls on the shares it owns.

More cash flow means a bigger dividend — and EXG pays an already terrific 8.9%!

So we buy and hold EXG and GDV forever, collecting their monthly dividends merrily along the way? Not quite.

In bull markets, these funds are great. But in bear markets, they’ll chew you up.

Step 5: Protect That Principal!

My CIR readers will fondly recall the 15 months we held GDV and EXG together, collecting monthly dividends plus price gains that added up to 43% total returns.

What was happening in that period, from October 2020 until February 2022? The Federal Reserve was printing money like crazy. Not only did the Fed stoke inflation, but we also enjoyed an asset-price lift.

Starting in 2022, we had the opposite situation. The stock market was topping, and we didn’t want to fight the Fed. We sold high, and by late 2022, both funds were down sharply:

We Sold EXG and GDV Just Before They Plunged

For whatever reason, “market timing” is a taboo phrase among long-term investors. That’s a shame because it is quite important.

By aligning our dividends with the market backdrop, we can protect our principal from bear markets.

Step 6: Start Here to Retire on $500K

So if the “tried and true” money advice — like the 60/40 portfolio and the 4% rule — has been properly exposed as broken…

Where do we go from here?

Well, imagine your portfolio in just a few days or weeks from now spinning off 8%, 9% and even double-digit dividends with the reliability of a Swiss watch… with many of my recommendations paying every single month no less!

No more worrying how much is coming in next month.

No more worrying about the Fed’s next move. Or the next inflation or jobs report.

No more worrying about outliving your nest egg.

Let me tell you more about my solution — what I call the 11% “No-Withdrawal Portfolio.”

Better yet, I want to give you the names of my favorite stocks and funds to buy right now…

Yields Up to 11%, With Upside

To make it easy to transition into this new way of investing… where you are buying “bird in the hand” cash flows… instead of stocks that you just hope will go up… I’ve prepared two in-depth guides that hone in on the strategies I mentioned above…

Special Report #1:

Monthly Dividend Superstars: Yields Up to 11%, With Double-Digit Upside

This is where you’ll find the bargains that investors are leaving on the table in their misplaced fear of the Fed.

Inside you’ll find the ticker symbol, my buy-up-to price and in-depth backstory on my three favorite CEFs:

A well-hedged 11% payer in one of the most in-demand sectors right now,

The brainchild of one of the top fund managers on the planet, throwing off an amazing 9.2% yield,

And a rock-steady 7.1% dividend whose managers have guided it to an astonishing 1,500% total return since inception.

Special Report #2:

The Perfect Income Portfolio

In this guide, you’ll get all the details of what I call the “Perfect Income Portfolio.”

Step-by-step, I’ll show you exactly how to set up your portfolio for maximum income without taking on additional unnecessary risk.

And, if you follow the simple steps laid out, I’m confident you’ll be able to enjoy an income stream that far exceeds what most folks who buy the typical S&P 500 stock earn.

This report includes investments that have passed my strict due-diligence process—including one of the best ways I’ve ever seen to invest in utilities (which I’ve picked for strong gains as interest rates move lower).

This fund pays a rich 7% today, holds some of the strongest electrical utilities in the country and trades at a bargain valuation (even though most investors don’t realize it). Its bargain status won’t last as rates inevitably tilt lower, pulling more investors toward its healthy payout!

I’ll walk you through each recommendation, giving you a clear, concise and easy-to-understand breakdown of exactly why I see these as “perfect” income plays.

How to Get Both Reports Absolutely Free

To access both reports, Monthly Dividend Superstars and The Perfect Income Portfolio, at no cost whatsoever, I simply ask that you take a risk-free trial of my research service, Contrarian Income Report.

I created Contrarian Income Report to help investors uncover overlooked and underappreciated income plays before Wall Street and the mainstream herd bid them up.

People often ask me, “I get the income part, but where does ‘contrarian’ fit in?”

My answer is simple: You’ll never beat the market by following the herd.

If you buy the same investments as everyone else, you’re going to have the same results as other people — which are always mediocre. This is why my advisory is defiantly contrarian.

It all boils down to one simple principle: If you want to make money, really big money, do what nobody else is doing.

Contrarian investing is probably the simplest, sanest, most powerful and reliable money-making technique ever devised to buy low and sell high. It works in any market, from stocks and bonds to gold and real estate — because human nature is the same everywhere.

You don’t need special training. All you need is an independent mind, a bit of patience and an ounce of courage.

If you want to buy low and sell high, you must force yourself to buy when everybody, including yourself, is feeling discouraged — when the news is bad. That’s likely to be the bottom. And you should sell when everybody is excited and the news is good, because that’s likely to be the top.

Right now, we’re holding a diverse collection of these high-yielding stocks and funds, and you’ll get instant access to each one the moment your no-risk trial starts.

And every new investment you get in Contrarian Income Report comes with a simple goal: it will pay a reliable 5% dividend — or better.

In fact, some holdings in our portfolio go way further than that, delivering 12%+ income right now.

So just by “swapping out” your anemic blue chips for these cash cows, you could double, triple — or even quadruple — your income. And you could do it TODAY!

That sort of money can upgrade your lifestyle in a hurry.

My name is Brett Owens. I first started trading stocks in college, between classes at Cornell.

My name is Brett Owens. I first started trading stocks in college, between classes at Cornell.

Inside you’ll find the ticker symbol, my buy-up-to price and in-depth backstory on my three favorite CEFs:

Inside you’ll find the ticker symbol, my buy-up-to price and in-depth backstory on my three favorite CEFs: