Keen for early retirement with a second income from dividends? Here’s how much you might need to invest.

Ditching the office job early is a dream of many, but without a second income, is it possible ? Here’s how investors could aim to make that happen.

Posted by Mark Hartley

Published 13 December

Image source: Getty Images

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

When I was young, my father would spend hours on the phone to brokers discussing share investing. I thought it sounded terribly boring but little did I know he was working towards a critical goal: building a second income.

Now, years later, I see the fruits of his labour — he lives a comfortable retirement, traveling regularly with seemingly no financial worries.

It’s a popular goal among UK investors — purchase shares in dividend-paying companies and watch the regular income flow in. For many people, this is seen as a way to supplement their pension so they don’t need to keep working past retirement age.

But how easy is it to actually make that happen? Let’s break down how much money is needed to retire early and a possible method to get there.

Realistic targets

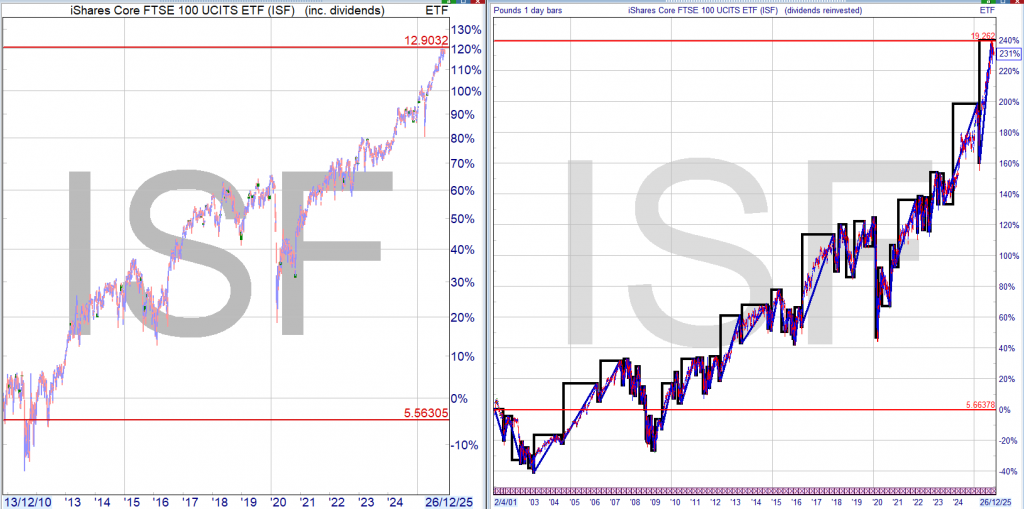

Since dividends are paid as a percentage of money invested, the first thing is to work out how much is needed. For example, 5% of 500,000 is 25,000. So a £500,000 portfolio of shares with an average yield of 5% would pay out £25,000 a year.

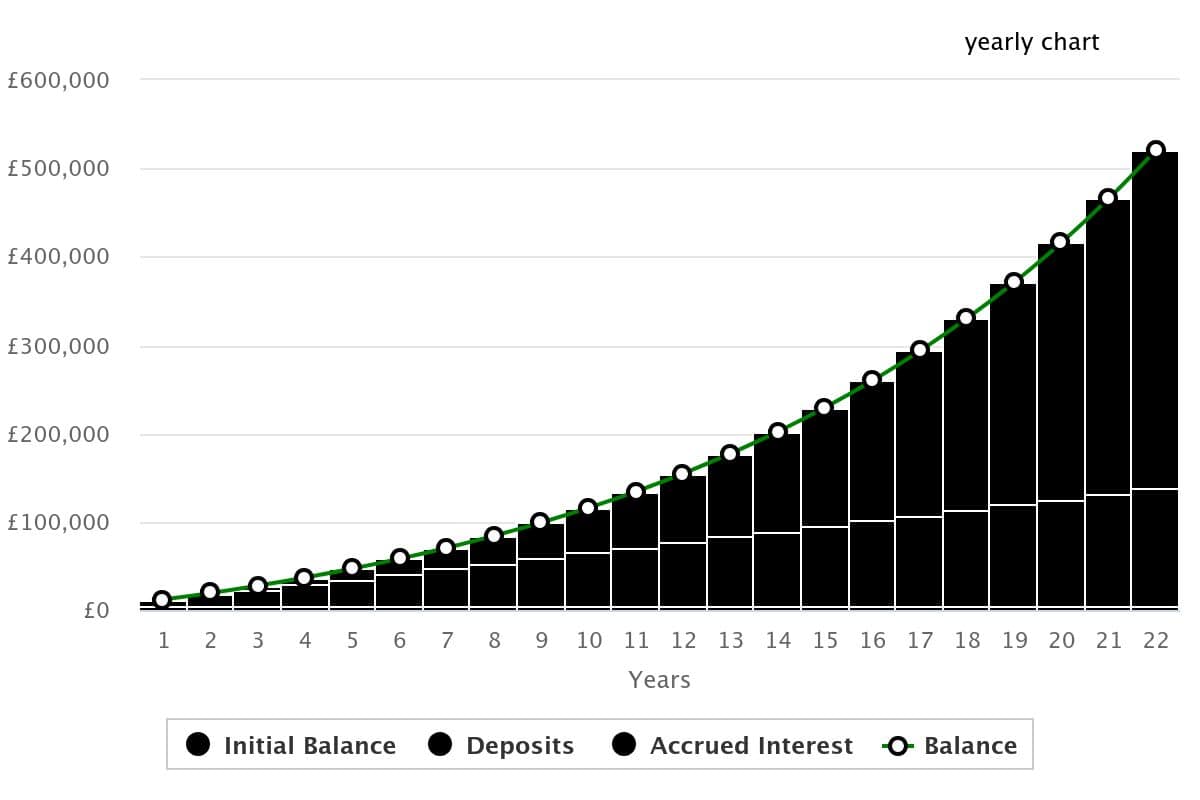

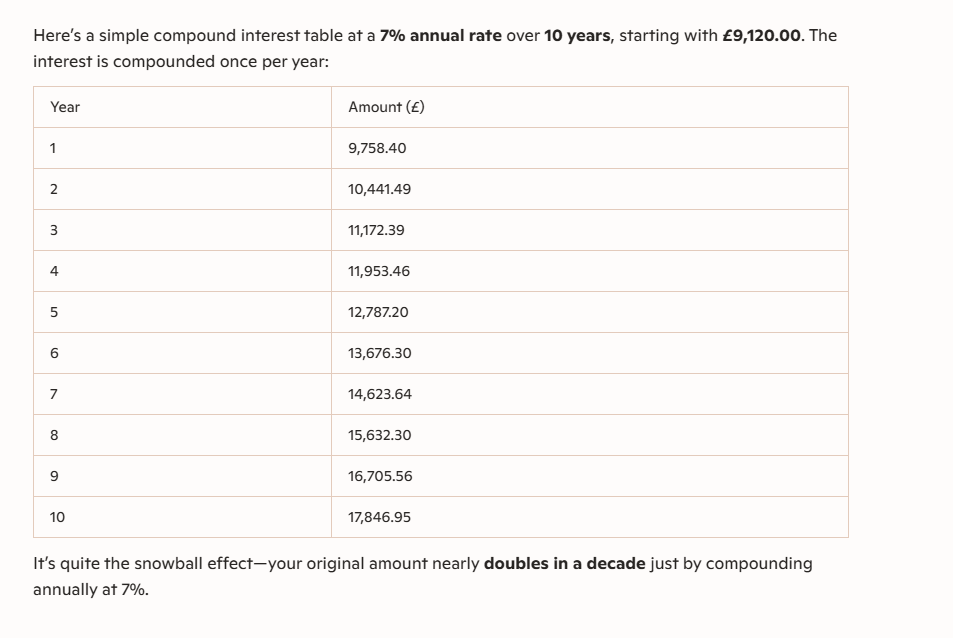

Working on those averages, how long would it take to save £500,000? Even saving £500 every month would take 1,000 months, or 83 year! Fortunately, the miracle of compounding returns would drastically reduce that timeline.

Smart investors with a well-balanced portfolio typically achieve an average return of around 10% a year. With a £5,000 initial investment and £500 monthly contributions, it would take less than 22 years to reach £500,000.

Now that’s more like it!

Created on the thecalculatorsite.com

3 starter shares to consider

Over time, I’ve rebalanced my income portfolio several times but three shares that remain permanent fixtures are Unilever, Legal & General and HSBC (LSE: HSBA). Together, they offer a mix of defensiveness, high yield and global exposure.

As a multinational bank with a £182.4bn market-cap and 4.7% yield, HSBC embodies all three of these characteristics. Lately, Lloyds has been outshining HSBC in both growth and dividends, but the long-term outlook paints a different picture.

With well over two decades of uninterrupted payments, its dividend track record beats most rivals. And despite weak performance this year, its 10-year growth outpaces Lloyds, Barclays and NatWest.

That’s the kind of reliability I’m looking for when thinking of retirement income.

Still, past performance doesn’t guarantee anything and HSBC still faces notable risks. The key being its recent attempts to divide East and West operations — a costly effort that could cause disruption. Execution is critical here as the move has already irked investors and any profit miss could risk a negative market reaction.

But for now, things look good and I’m optimistic about the eventual outcome.

Final thoughts

When building an income portfolio, don’t just aim for the highest yields. It pays to have a foundation of defensive shares in industries that maintain demand even during market downturns.

Diversification is equally as important to reduce the risk of localised losses in one sector or region. These three companies are good examples of stocks worth considering for a beginner’s portfolio.

They can serve as a starting point to finding companies with similar characteristics, with the aim to build up a portfolio of 10-20 stocks.

Could a 10%+ yielding dividend share like this make sense for a retirement portfolio?

With a double-digit percentage yield, could this FTSE 250 share be worth considering for a retirement portfolio? Our writer weighs some risks and rewards.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

What makes for a good retirement portfolio?

The answer will be different for each investor. From timeframe to risk tolerance, different people have their own idea of how they want to prepare themselves financially for their retirement.

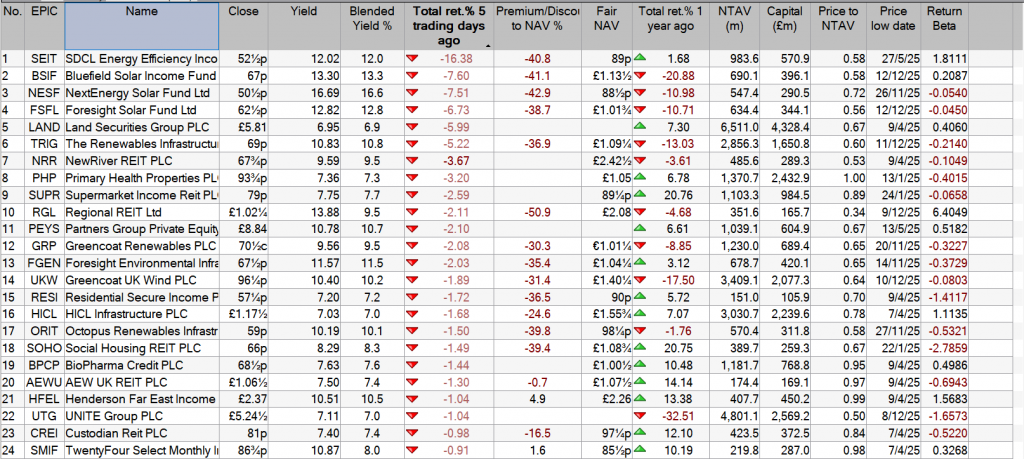

Should you buy Greencoat UK Wind shares today?

One thing a lot of people like is shares they reckon can give them generous dividends.

But dividends are never guaranteed to last. When salivating over a high yield (or any yield, come to that), an investor always ought to ask themselves how likely it is to last.

10%+ yields in the FTSE 250

As an example, a number of FTSE 250 shares connected to renewable energy currently offer double-digit percentage yields.

For example, Greencoat UK Wind (LSE: UKW) currently yields 10.7%.

As if that is not enough, the dividend per share has grown annually in recent years.

So, what is going on with these high-yield renewables shares?

Each share needs to be viewed on its own merits

The fact that multiple renewable energy shares offer high yields right now points to concerns some investors have about the sector.

There is a risk that uncompetitive production costs could mean the business model becomes less attractive, especially if fossil fuel prices fall. Potentially lower selling prices are also a concern.

But while a high-level view can be useful when assessing a possible area for investment, it is always important to consider each individual share on its own merits too.

A well-constructed retirement portfolio is diversified not only across multiple shares, but different business areas too. It also ought to involve a long-term view. After all, retirement can last for decades.

So, no matter what a dividend may be today, an investor will also want to consider how sustainable it might be for the future.

Dividend is well covered

In the first half, Greencoat UK Wind’s net cash generation covered its dividend costs around 1.4 times over.

Its net asset value at the end of June was around £1.43 per share – but its share price is currently in pennies.

With proven cash generation potential and a generous dividend, I reckon that the share has some things going for it. But its price suggests that at least some investors have questions about whether the dividends can keep flowing. After all, a double-digit percentage yield is unusual.

The company has been actively buying back its own shares. Given the gap between its most recently reported net asset value and the current share price, that could create value for shareholders.

However, that net asset value is based in part on power prices. If forecast power prices fall, the value of power generation assets is also reduced. That is a risk that I think could continue to weigh on Greencoat UK Wind’s net asset value – and share price.

Still, although there are risks, I also see the potential for rewards here. Getting the balance between risks and rewards matters for any investor and certainly when it comes to a retirement portfolio.

All things considered, I do see this as a share for investors to consider.

Dividends yield can fall by:

1. The company cuts it dividend or holds it dividend at the previous level and you suffer a modest real time fall from inflation.

2. As the price rises the comparative yield falls, although you will receive the same buying price yield. If the price rises and the yield falls you may be able to re-invest into another high yielding share.

The Schwab US Dividend Equity ETF has lagged far behind the market and the Vanguard Dividend Appreciation ETF this year. (Justin Sullivan/Getty Images)

Key Points

About This Summary

The stock market has returned more than 18% this year. Many dividend funds haven’t kept up.

The Vanguard Dividend Appreciation ETF is up 16% this year, while the Schwab US Dividend Equity ETF returned 5.3%.

Vanguard’s fund focuses on dividend growth, so it invests heavily in tech, while Schwab’s targets companies with strong fundamentals in areas such as consumer staples and energy.

America has a K-shaped economy. The performance of dividend funds is similar.

The stock market has returned more than 18% so far this year, including dividends. The fact that the rally is led by fast-growing tech companies makes it hard for dividend stocks, dedicated to handing cash back to investors, to keep up.

VIG ETF, the market’s largest dividend exchange-traded fund. It’s up 16% this year. By contrast, one of its main rivals, the $72 billion Schwab US Dividend EquitySCHD ETF, has returned just 5.3%.

What gives? The two funds’ approaches to dividends aren’t so different from the current socioeconomic split between two Americas.

One group of people in the U.S. is thriving, with wealth rising like the upper arm of a letter K. It is benefiting from the extraordinary excitement around artificial intelligence that is lifting the prices of tech stocks and swelling the bank accounts of those that own them.

Another segment of U.S. represents the K’s lower arm. The majority of consumers are struggling with tepid wage growth and stubborn inflation.

The realm of dividend funds shows the same kind of divergence. Vanguard Dividend Appreciation focuses on companies that grow their dividends, giving it a tech-first portfolio, with top holdings that include Broadcom, Microsoft, and Apple.

Schwab U.S. Dividend Equity ETF takes a more traditional approach, targeting stocks with strong fundamentals and sustainable payouts. Its top holdings include companies like Coca-Cola, ConocoPhillips

COP, and ChevronCVX. It is heavily invested in consumer staples and energy, two sectors that have badly lagged behind the market in 2025.

Schwab U.S. Dividend Equity has some strong points. It yields 3.8%, compared with 1.6% for the Vanguard fund, an important consideration for dividend investors who want income. And its portfolio is arguably undervalued as a result of the market’s obsession with growth. Shares in its portfolio trade at an average of 14 times forward earnings, compared with 21 times for the Vanguard fund.

That means that if the market really is in an artificial-intelligence bubble, and that bubble pops. the ETFs’ fortunes could quickly reverse. The tech stocks that have boosted the Vanguard fund would slide, while companies like Coca-Cola could rise as investors reallocate their cash.

That said, investors in Schwab U.S. Dividend Equity will have to be patient. With stubborn inflation and a weakening job market, consumer stocks don’t seem likely to rebound soon.

And the picture for energy stocks is even gloomier. Oil prices tumbled about 20% in 2025. With oil companies still pumping at a breakneck rate, they look set to fall further in 2026.

The upshot is that as long as the market rally giving the economy its K shape continues, these funds will remain the dividend world’s haves and have-nots.

Looking for High-Yield Dividend Stocks ? Citizens JMP Suggests 2 Names — One Offers a Massive 13% Yield

Sat, December 13, 2025

As we head into 2026, it’s only natural to want to set up the best possible portfolio for the new year. The key here is returns – we’ve seen bullish markets for several years now, and investors want to keep up that momentum. Dividend stocks can make a clear contribution.

Among the higher-yield corners of the market, business development companies (BDCs) stand out. These firms provide financing to small- and medium-sized businesses that often fall outside the traditional banking system, and like REITs, they benefit from favourable tax treatment when they distribute a large share of earnings to shareholders. That leads to high and usually reliable dividends.

Covering the BDC space for Citizens JMP, analyst Brian McKenna notes that despite recent underperformance, the fundamentals remain intact.

“Both the Alts and BDCs have underperformed over the past several months, although as we have written about at length, underlying fundamentals remain generally healthy for many (vs. perceptions across the marketplace today),” McKenna said. “We think the recent underperformance across the industry is largely unwarranted, specifically as the broader markets continue to trade at/near all-time highs, and we see (yet again) another compelling longer-term buying opportunity in these stocks.”

For investors seeking out high-yield dividend payers, this is exactly what is needed: an attractive point of entry and strong dividend.

Trinity Capital(TRIN)

The first company on our list, Trinity Capital, is an alternative asset manager that is structured for business purposes as an internally managed BDC. The company aims to provide its client firms with access to the credit market, and its investors with stable and consistent returns. Trinity invests its capital in a wide range of target firms, across several categories: tech, equipment, life sciences, sponsor finance, and asset-based lending. Since its founding in 2008, Trinity has poured some $5.1 billion into its investments. The company is based in Phoenix and operates in the US and Europe.

Trinity currently has $2.6 billion in assets under management, and boasts a market cap of $1.15 billion. The company makes careful vetting of its investment targets, keeping in mind its constant goal of maintaining a sound return for investors. This is usually returned via dividend distributions, and as of September this year Trinity has returned a cumulative $411 million through those payments.

How Trinity’s Seventh Straight Dividend Raise Will Impact Trinity Industries (TRN) InvestorsSimply Wall St Sun, December 7, 2025

Trinity Industries recently increased its quarterly dividend to US$0.31 per share, its seventh consecutive annual raise and the 247th straight quarterly payout, with the latest dividend paid on January 30, 2026 to shareholders of record on January 15, 2026.This extended record of dividend growth highlights Trinity’s emphasis on consistent shareholder returns and reinforces its reputation for disciplined capital allocation in the rail sector. We’ll now explore how this latest dividend increase shapes Trinity’s investment narrative, particularly its balance between income stability and future growth.

Trinity Industries Investment Narrative Recap. To own Trinity Industries, you have to believe in the long-term need for North American railcar leasing and manufacturing, supported by stable demand for freight-by-rail. The latest US$0.31 dividend increase reinforces Trinity’s income appeal, but does not materially change the near term picture, where the key catalyst remains a healthier railcar order environment and the main risk is that cyclical end markets and delayed customer capex continue to weigh on volumes and cash. The dividend hike follows Trinity’s October 2025 move to tighten and raise its full year 2025 EPS guidance to US$1.55 to US$1.70, which helped frame the payout within recently updated earnings expectations. Together, these announcements point to a management team signalling confidence in the business while still operating against a backdrop of softer recent sales, high leverage and interest costs that are not comfortably covered by earnings. Yet behind the steady dividend record, investors should also be aware of Trinity’s high leverage and relatively weak interest coverage…

Trinity Industries’ narrative projects $2.6 billion revenue and $207.4 million earnings by 2028. This requires 1.3% yearly revenue growth and about a $98.8 million earnings increase from $108.6 million today.

Exploring Other PerspectivesTRN Earnings & Revenue Growth as at Dec 2025The Simply Wall St Community’s two fair value estimates for Trinity span roughly US$16.32 to US$25.50, underlining how far apart individual views can be. Some of these investors focus on the risk that Trinity’s exposure to cyclical energy and agriculture demand could slow new railcar orders and weigh on longer term performance, so it is worth comparing several viewpoints before forming your own stance.

A great starting point for your Trinity Industries research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Our free Trinity Industries research report provides a comprehensive fundamental analysis summarized in a single visual – the Snowflake – making it easy to evaluate Trinity Industries’ overall financial health at a glance.

Blue Owl Technology Finance (OTF)

Next on our list, Blue Owl Technology Finance, is a large, tech-focused BDC that was formed to provide credit to tech-related firms. The company originates and makes loans and makes equity investments in its target firms, and aims mainly at enterprise software companies. Blue Owl Tech Finance is externally managed by an affiliate of the larger Blue Owl Capital. This link to a larger asset manager gives the BDC access to solid backing.

The BDC focuses on US-based upper middle-market tech firms. Its investment strategy prioritizes senior secured or unsecured loans, subordinated loans or mezzanine loans, and also equity-related securities. Blue Owl Tech Finance aims to prioritize long-term credit performance for maximum returns. This includes setting a diversified portfolio and weighting it toward defensive industries that are non-cyclical.

Blue Owl Tech’s portfolio currently stands at $12.9 billion in fair value, with 77% of it being in first-lien senior secured loans. The portfolio features 97% floating-rate debt investments and 3% fixed-rate. Nearly three quarters (74%) is located in three US regions: West, South, Northeast. Systems software makes up 20% of the portfolio.

In its last reported financial quarter, 3Q25, Blue Owl Tech reported two key metrics: the company reported a GAAP net investment income of 28 cents per share and an adjusted net investment income of 32 cents per share. This quarter marked the company’s first full quarter as a publicly listed firm. Blue Owl Tech declared a dividend of 35 cents per share to be paid on January 15. In addition, the company has declared five special dividends of 5 cents each, with the next one scheduled for payment on January 7. The total dividend to be paid in January, 40 cents per common share, annualizes to $1.60 and gives a forward yield of 11%.

McKenna, in following this BDC, lays out a course that he sees it following, one that will lead to continued success.

“Given the strong trajectory of NII over the next year (i.e., NII per share will be growing vs. the 2H25 quarterly level, not declining), we think the company will be roughly earning the regular quarterly dividend ($0.35 per share) exiting 2026, with even greater dividend coverage beyond that as leverage and the size of investment portfolio inevitably normalize to the longer-term targets, a clear outlier within the publicly-traded BDC sector. We also highlight that the company has a healthy track record of delivering unrealized/realized gains across the portfolio (specifically tied to equity investments), so any incremental GAAP earnings above and beyond NII will be accretive to GAAP NI ROEs, as well as NAV,” McKenna noted.

Summing up, the Citizens analyst says of Blue Owl Tech: “Bottom line, as leverage and the size of the investment portfolio normalize over time, we anticipate the company will generate ~10%+ ROEs through the cycle (both on an NII and GAAP net income basis), potentially even above that depending on the level of appreciation/upside that occurs within the equity portfolio, which we think will be the biggest driver of OTF’s valuation multiple over time… We believe OTF is an excellent way to gain exposure to the asset class, specifically some of the largest and most innovative companies in the private ecosystem.”

Quantifying his stance on OTF, McKenna rates the stock as Outperform (i.e., Buy), with a $17 price target that suggests an upside of 20% by this time next year. The one-year return can hit 31% when the dividend yield is added in.

Overall, Blue Owl Tech’s Moderate Buy consensus rating is supported by 9 analyst reviews that include 4 Buys and 5 Holds. The shares are priced at $14.21, and the $15.78 average price target implies a 12-month gain of 11%. (See OTF stock forecast)

Remember if you buy a tracker and can decide when to sell you will not lose any of your hard earned. As in the chart above, you may have to wait several years to be proved correct, better if there is a dividend, so you can add more shares without risking any more of your capital.

Lower risk but you have to old thru thick and thin, there will always be plenty of thin.

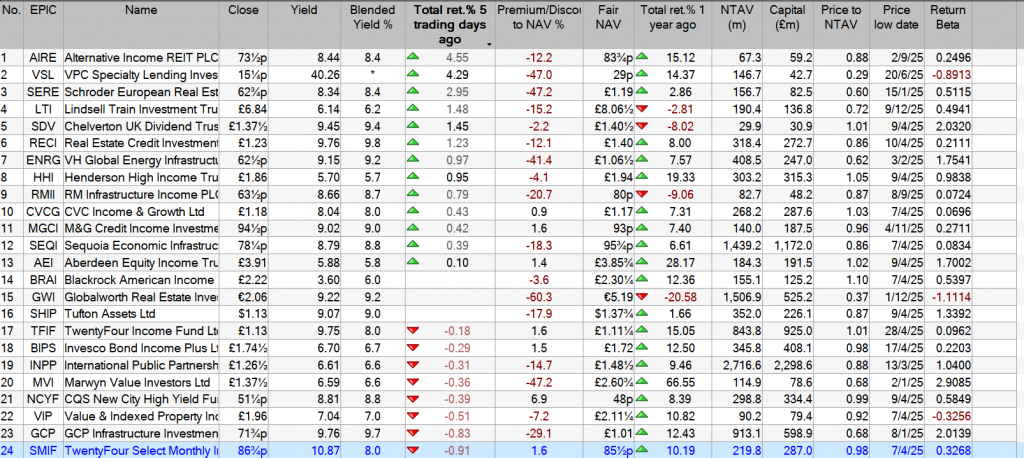

The Snowball has beaten the 2025 fcast and target, so it’s now history.

The Snowball, on all the known unknowns should at least better the year one 2026 target of 10k, especially as there is already a buffer built in for January.

Remember the Snowball doesn’t add any capital, so if you can add to your Snowball, even modestly you should be able to improve the yield in the table above, especially thanks to Mr. Market you can currently re-invest all dividends at above 7%, or pair trade with a blended yield of 7%.

Pair trading is best if you are not near to you retirement date as you have time to correct any unfavourable trading choices.

Also if you can only add a modest amount, compound interest takes several years before the big money is made, which should encourage you to start saving. Can you cut one coffee a day and save the cash ?

Your Snowball should be different from the blog Snowball as it should reflect on your risk profile, which depends mainly on how many years it is before you want to spend your hard earned. Join us on the journey, where there are bound to be many twists and turns as we journey thru the year.

Dividends can be more reliable than share prices as they’re driven by the companies performance itself and not by the whim of investors.

As part of a total return / reinvestment strategy, this income could be reinvested into income assets or back into the equity market depending on the relative valuations.

The emotional benefits of dividend re-investment. In fact, with this investment strategy you can actually welcome falling share prices.