2k to be invested into QYLP. The current plan is to reduce the risk into the QYLP trade by re-investing future dividends into a lower risk trade.

Every time you put on a trade on, you must ask yourself. What is the worst possible thing that can happen to this trade in between now and me being right. Is this realistic ? Am I lying to myself ? Take your worst case scenario and double it.

If you want to buy a high yielding Trust/Etf but are concerned about the risk, one way of lowering the risk is to pair trade the purchase.

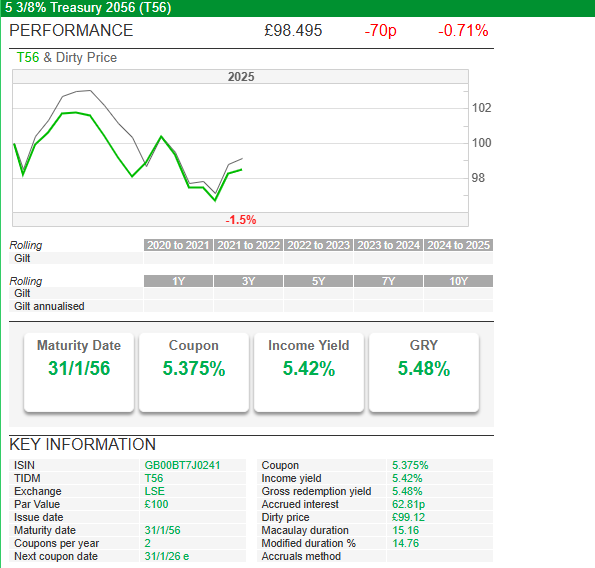

The income yield is 5.42%, the income is paid twice a year, better if held in a tax free account.

It’s likely that over the time period that you could make a capital loss but only if you sell and as you only want the income to re-invest it matters little. If/when interest rates rise above 5.42% you could simply re-invest your income into a money market account. To double your income in ten years the target is re-investing for a blended yield of 7% plus.

Brett Owens, Chief Investment Strategist Updated: September 10, 2025

Last Friday’s jobs report confirmed what we contrarians have been discussing for months now—thanks to AI, employers no longer need to hire more employees to grow.

Bosses simply need to implement AI tools to grow their businesses. The machines are a managerial dream. Once trained they are, in many cases, better, faster and cheaper than people.

Robots always report for work. They will grind all the time. And they are never sick or hungover!

Two years ago, my current software company engaged about 15 contractors in various capacities. Today, thanks to AI, we have only two-and-a-half. Yet even with only one-sixth the “manpower,” sales are climbing, and the bottom line has never looked better!

This “growth without headcount” revolution is happening throughout the economy. The US added only 22,000 new jobs in August and 107,000 jobs over the last four months. Meanwhile, it’s estimated that 100,000 fresh gigs are needed every month to keep up with population growth—which means we are 70,000 short per month of that target.

Bad news for job seekers (such as new college grads) but bullish for business owners.

This is the reason that small businesses are increasingly cheerful. The rise of machines solves a tough business problem—hiring and managing employees. No wonder the Small Business Optimism Index just hit a five-month high.

Let’s talk about an 11% dividend that is directly benefiting.

FS Credit Opportunities (FSCO) is a small-business lender quietly cashing in on this generational shift. The team at FS Credit rewarded investors with another 5.1% dividend raise earlier this summer. FSCO now yields 11%, paid monthly!

The firm benefits from an uptick in M&A under Trump 2.0. As a business development company in a “fund wrapper,” FSCO presents us with the best of all possible worlds—a reliable income strategy via value-based lending that gets dished to us as a generous monthly dividend.

We were “early adopters” of FSCO in my Contrarian Income Report, and we have been rewarded with 24% gains in just 11 months. We bought the fund at a 10% discount to its net asset value, a deal that was “too good to be true” as this fund now trades at fair value. Still, it is tough to argue with a fair price for a secure 11% monthly dividend.

FSCO’s Fat Monthly Dividend

Small company bosses aren’t the only ones trimming their human payrolls. Big companies are also going big on AI. Microsoft (MSFT) laid off 15,000 employees a few months back. Yet Microsoft isn’t downsizing. It’s upsizing efficiency by rolling out robot-powered sales, marketing and support teams.

Meanwhile, if you need to get a hold of a person at Amazon (AMZN) about your latest package, good luck. CEO Andy Jassy openly acknowledged that Amazon’s workforce will shrink over the next few years. Today is likely “peak human headcount” for the online retailer because it has found a way to grow without hiring.

We are seeing these patterns all over the “Magnificent 7”— tech companies are eating their own AI dogfood to replace expensive humans with cheaper machines. Profits are booming.

Global X S&P 500 Covered Call ETF (XYLD) is a savvy dividend play on this megatrend. XYLD holds a substantial 40% tech allocation, capturing the automation-driven profitability boom.

XYLD implements a covered call strategy that buys stocks and then sells (“writes”) call options to other investors. XYLD owners earn income from the premiums collected, paid upfront.

It’s a lucrative payout boost: XYLD dishes a 9.7% dividend, payable each month. The fund’s showered us with 31% annualized gains since we added it to the CIR portfolio in April, and more profits are likely as the Mag 7 continues to impress.

So, we have booming corporate profits alongside a sleepy jobs market. The latter means the Federal Reserve will almost certainly cut short-term interest rates.

Long rates are on the way down, too. Partly as a reaction to unemployment numbers, but really thanks to major “help” from the US Treasury.

The Treasury is dusting off its bond buyback machine to keep a lid on long rates. Here’s how it works. The Treasury raises cash in the short end (by selling more lower-yielding bills, two years or less) and uses those funds to repurchase longer-dated notes and bonds (“retiring” their higher yields and higher cost to Treasury) in the secondary market.

It’s a recycling program for Uncle Sam’s outstanding debt. The effect of these Treasury buybacks? Even fewer long-duration bonds are available to investors.

Treasury Secretary Bessent doesn’t even have to announce a formal cap on the 10-year yield. He simply pulls supply out of the market, which causes long-dated yields to drift down (with more demand, Seller Sam can “name his price”—he doesn’t have to pay higher yields to attract lenders).

Result? The 10-year Treasury yield has dropped to 4% from 4.8% this year.

Treasury bond prices and interest rates have an inverse relationship. Thus, 11.3%-yielding iShares 20+ Year Treasury Bond BuyWrite Strategy ETF (TLTW) has a rock-solid floor beneath it.

TLTW buys the iShares 20+ Year Treasury Bond ETF (TLT) and then writes covered calls on its shares for extra income. There are many covered call funds for stocks, but TLTW is unique in using this strategy to boost bond yields. With the US Treasury having TLT’s back, TLTW’s assets are well supported while they generate its big monthly dividend.

3 popular UK income stocks I won’t touch with a bargepole right now

Investors are rushing to buy these three income stocks, but Zaven Boyrazian has spotted some critical weaknesses that make him sceptical.

Posted by

Zaven Boyrazian, CFA

Published 13 September

Image source: Getty Images

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.Read More

The content of this article is provided for information purposes only and is not intended to be, nor does it constitute, any form of personal advice. Investments in a currency other than sterling are exposed to currency exchange risk. Currency exchange rates are constantly changing, which may affect the value of the investment in sterling terms. You could lose money in sterling even if the stock price rises in the currency of origin. Stocks listed on overseas exchanges may be subject to additional dealing and exchange rate charges, and may have other tax implications, and may not provide the same, or any, regulatory protection as in the UK.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

The FTSE 100 is packed with a wide range of income stocks, some of which are offering pretty tasty-looking yields right now. Sadly, not all of these dividend-paying shares will be winning investments. And after taking a look at some of the most popular picks among investors over the last month, there are three that I’m personally steering clear of.

The shifting insurance landscape

According to AJ Bell, Legal & General (LSE:LGEN) and Aviva (LSE:AV.) are both among the most popular income stocks to buy right now. And it’s not too difficult to understand why.

Should you buy Aviva plc shares today?

These insurance giants currently offer a 9.2% and 5.6% dividend yield. Looking at their latest results, both have delivered higher operating profits across their increasingly diversified portfolios of financial products. And since that has, in turn, generated recurring cash flows, both businesses are on a bit of a dividend hiking streak of four and five years, respectively.

But as every experienced investor knows, past performance does not guarantee future results. And the shifting macroeconomic landscape in the UK is starting to create headwinds that could potentially compromise dividends.

My top concern is the state of UK gilts. Both insurance groups have large portions of their investment portfolios tied up in government bonds. As such, they’re highly sensitive to sudden movements in gilt yields, which have recently spiked to multi-decade highs on the back of growing fiscal policy concerns.

Rising gilt yields mean falling bond prices, which can create enormous problems for liability-driven investing strategies and pension risk transfers – something that both Legal & General and Aviva use to generate earnings. Put simply, if yields continue to be volatile, these firms may face a sudden wave of margin calls, triggering balance sheet and liquidity challenges.

That’s why, despite the high dividend yields, the risk surrounding these income stocks is just too high for my tastes.

Homebuilding opportunity?

Another popular pick right now is Taylor Wimpey (LSE:TW.). And again, it’s easy to see why investors are rushing to buy. Despite issues with affordability, housing demand in Britain remains exceptionally strong due to shortages. And with over 76,000 plots in the firm’s landbank, the company has ample untapped growth.

Looking at its latest results, Taylor Wimpey has even managed to accelerate its homebuilding efforts by double-digits. As such, home completions are on track to reach between 10,400 and 10,800 by the end of 2025.

So, what’s the problem? Despite operational improvements, the company continues to see its profit margins squeezed. Build cost inflation surrounding raw materials as well as labour continues to be a pest. And when throwing in unpredictable cladding remediation and regulatory settlements, Taylor Wimpey’s profits recently swung firmly into the red.

With fewer profits to spare, dividends are no longer covered by earnings. That’s fine if profits are able to rebound in the short term. But if not, management may be forced to cut shareholder payouts. And with mortgage rates ticking back up due to the previously mentioned fiscal and economic environment, Taylor Wimpey may struggle to find buyers for all its newly completed homes.

That’s why, despite the tempting 9.6% dividend yield, I’m not tempted to buy this popular income stock.

Let’s assume you bought some shares when it was 100p. You could have booked some profit with the intention of buying back if the share price fell but for this analysis we will assume you just held and re-invested the dividends back into your Snowball. Your one share would be worth 65p a loss of capital of 35p and you need to allow for inflation. Your analysis of the share has turned out to be wrong.

But you have earned dividends of 62p, the current dividend is

Dividend:

· Total dividends declared of 2.10p per Ordinary Share for the Q1 period ended 30 June 2025 (30 June 2024: 2.10p), in line with full-year dividend target.

· Full-year dividend target guidance for the year ending 31 March 2026 remains at 8.43p per Ordinary Share (31 March 2025: 8.43p).

· The full year dividend target per Ordinary Share is forecast to be covered in a range of 1.1x – 1.3x by earnings post-debt amortisation.

· Since inception the Company has declared total Ordinary Share dividends of £407m.

· As at 20 August 2025, the Company offers an attractive dividend yield of c.11%.

In 5 years time you will have achieved the holy grail of investing that you will have a share providing income at a zero, zilch, cost. Also you have re-invested the income back into your portfolio which is earning you more income to re-invest into your Snowball.

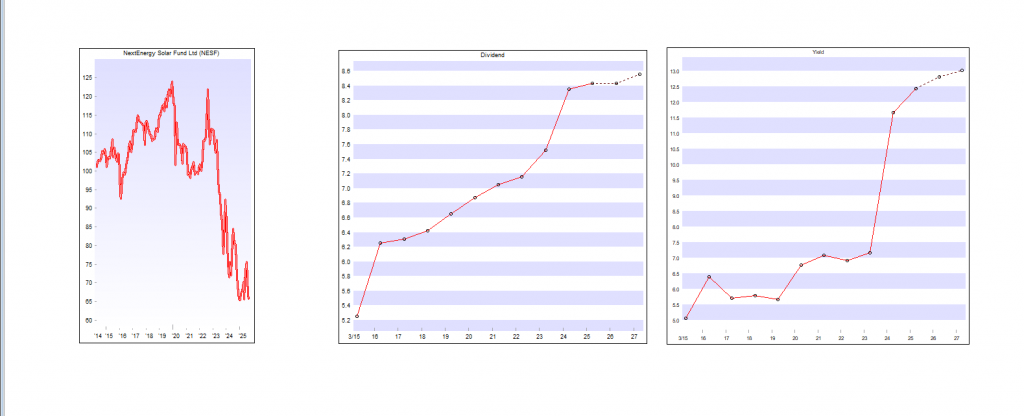

Firms to exit the FTSE 250 are online retailer Asos, auction market operator Auction Technology Group, Bloomsbury Publishing and housebuilder Crest Nicholson Holdings. Solar investor NextEnergy Solar Fund

Even though your analysis turned out to be wrong but by trading a belt and braces strategy you are still growing your retirement Snowball.

The Board of Value and Indexed Property Income Trust PLC (“the Company”) declares a first quarterly dividend of 3.6p per Ordinary Share in respect of the year to 31 March 2026, payable on 31 October 2025 to Shareholders on the register at close of business on 3 October 2025. The ex-dividend date is 2 October 2025. This dividend will be designated as a Property Income Distribution (PID).

The Board will announce in due course the proposed further quarterly dividend payments for the year to 31 March 2026, which will be paid on or around 30 January 2026, 24 April 2026 and 31 July 2026.

£££££££££££££££££££££

RGL

Resilient operations underpinning fully covered dividend; Total Shareholder Return +9.6%

· Dividend declared of 5.0p (H1 24: 3.4p*) fully covered

· EPRA EPS 5.2pps (H1 24: restated 13.5 pps*)

*On 19 July 2024 the shares in issue increased by 1,105,149,821 shares to 1,620,886,404. On 29 July 2024 the shares were consolidated on a 1 for 10 share basis.

£££££££££££££££££££££££

SDV Chelverton UK Dividend Trust plc

Declaration of Interim Dividend

The Company has today declared a first interim dividend in respect of the year 1 May 2025 to 30 April 2026 of 2.5p per share (2024: 3.25p).

This dividend will be paid on 10 October 2025 to the holders of Ordinary shares on the register at 26 September 2025, with an ex-dividend date of 25 September 2025.

It is the Board’s intention that this payment will be the first of four equal core dividend payments of 2.5p each, being a total of 10.00p, for the year ending 30 April 2026.

£££££££££££££££££££££

SEIT

SDCL Efficiency Income Trust plc

(“SEIT” or the “Company”) Interim Dividend Declaration

SDCL Efficiency Income Trust plc is pleased to announce the first quarterly interim dividend in respect of the year ending 31 March 2026 of 1.59 pence per Ordinary Share, covered by net operational cash received from investments.

The shares will go ex-dividend on 11 September 2025 and the dividend will be paid on 29 September 2025 to shareholders on the register as at the close of business on 12 September 2025.

£££££££££££££££££

RMII

RM Infrastructure Income Plc

Dividend Declaration

The Directors of the Company, an investment trust specialising in secured debt investments, have declared an interim dividend of 0.625 pence per ordinary share in respect of the period from 1 January 2025 to 30 June 2025:

Ex-Dividend Date – 11 September 2025

Record Date -12 September 2025

Payment Date – 26 September 2025

The Company has elected to designate the interim dividend for the period as an interest distribution to its ordinary shareholders.

As an update to previous disclosures relating to the ongoing discussions with the French Tax authority, the Group has received a payment demand from the French Tax Authority amounting to c.€14.2 million, including interest and penalties. The Group considers that this amount is not due and intends to file an appeal against the decision. Nevertheless, the Board considers it prudent to ring-fence the amount demanded from its other cash reserves, and is considering its options, including making a payment of tax on account in line with French judicial procedures. Having taken professional advice, the Board remains of the opinion that the Group’s position is ultimately more likely than not to prevail, such that a net outflow is not probable, and hence no tax provision has been recognised.

Interim dividend

Announcement of a third quarterly interim dividend of 1.48 euro cps, which is 90% covered by adjusted EPRA earnings, reflecting the sale of the Frankfurt DIY asset in the previous quarter and higher than normal exceptional items. Annualising the dividend provides investors with a dividend yield of c.7.6%, based on the share price as at 10 September 2025(1).

Total dividends declared relating to the nine months of the current financial year are 4.44 euro cps, 96% covered by adjusted EPRA earnings.

The interim dividend payment will be made on Friday 7 November 2025 to shareholders on the register on the record date of Friday 3 October 2025. In South Africa, the last day to trade will be Tuesday 30 September 2025 and the ex-dividend date will be Wednesday 1 October 2025. In the UK, the last day to trade will be Wednesday 1 October 2025 and the ex-dividend date will be Thursday 2 October 2025.

The Company has a total of 133,734,686 shares in issue on the date of this announcement (including those held in treasury). The dividend will be distributed by the Company (UK tax registration number 21696 04839) and is regarded as a foreign dividend for shareholders on the South African register. In respect of South African shareholders, dividend tax will be withheld from the amount of the dividend noted above at the rate of 20% unless the shareholder qualifies for the exemption. Further dividend tax information for South African shareholders will be included in the exchange rate announcement to be made on Tuesday 30 September 2025.

Property portfolio

The direct property portfolio was independently valued at €193.9 million (30 June 2024 €196.5 million on a like-for-like basis), reflecting stable values across the period. Robust valuations within the industrial portfolio, along with a positive revaluation of the Berlin asset, helped to offset declines in other sectors, which were primarily driven by shortening lease terms.

During the period a new 12-year lease extension with Hornbach, at the Berlin investment, was successfully agreed, resulting in a €1 million valuation increase. This transaction has further strengthened both the portfolio’s income security and the weighted average lease expiry, which has risen by approximately 1.3 years.

Management is also actively advancing discussions regarding lease re-gears in Stuttgart, Rumilly, Nantes, and Cannes. Completion of these initiatives will positively impact the portfolio value and income and the weighted average unexpired lease term.

KPN is still expected to vacate the Apeldoorn asset at the end of December 2026. As a result, we are assessing options including sourcing a replacement tenant, or securing planning approval for alternative uses. Should KPN vacate as expected, and as previously announced, there may be an impact on the Company’s ability to maintain its current dividend level. However, management is taking steps to mitigate any potential effects.