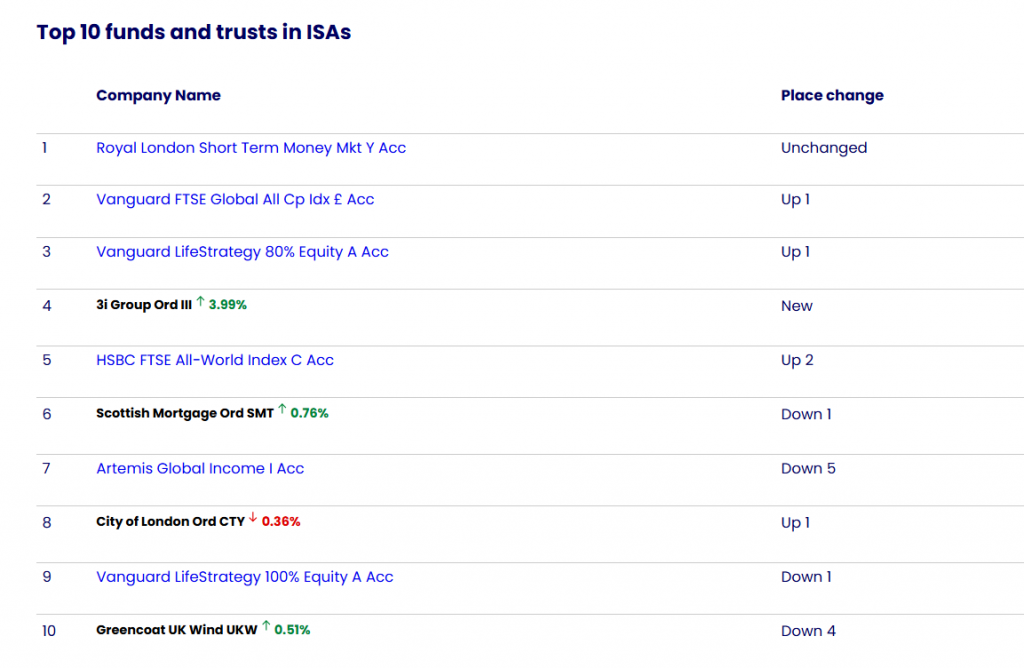

3.99% as a bargain, with the private equity behemoth soaring back into the bestsellers table.

The trust, associated both with its chunky stake in discount retailer Action and the substantial premium on which its shares have tended to trade, initially slipped late last year amid warnings of softening sales growth for its main holding.

The shares tumbled afresh late last week, after an update from Action that outlined plans to expand into the US market appeared to unsettle investors. 3i Group shares have moved to a discount in recent weeks and that has widened markedly in recent days.

Some separate trends otherwise hold firm. Royal London Short Term Money Mkt Y Acc retains its top position, perhaps unsurprising given the continued volatility of markets.

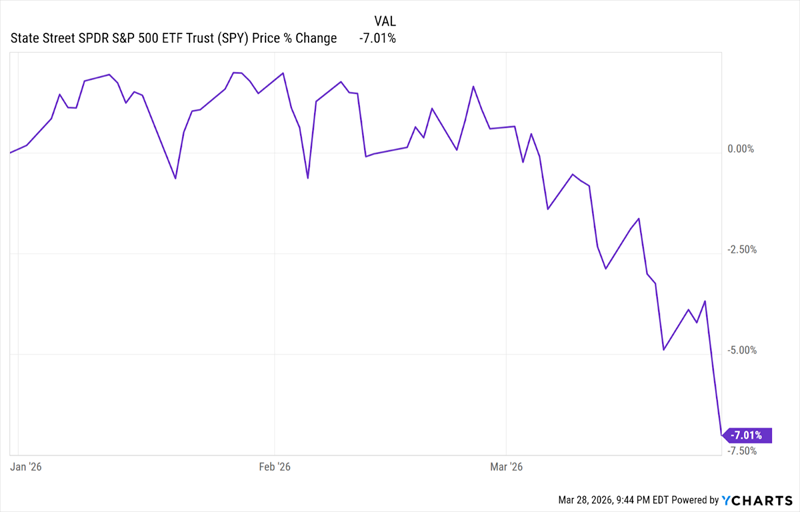

The fund, which has substantial exposure to equity regions most shaken by recent conflict such as Europe and emerging markets, has lost around 9.5% since the onset of hostilities in late February.

A few other favourites retain their presence in the table, from future trends play Scottish Mortgage Ord

Forget Oil Stocks: This 7.7% Dividend Is a Smart Contrarian Buy Now

Michael Foster, Investment Strategist Updated: April 2, 2026

Iran War volatility has tossed finance stocks “out with the bathwater.” It’s giving us a nice “second chance to buy” my favorite finance-focused dividend.

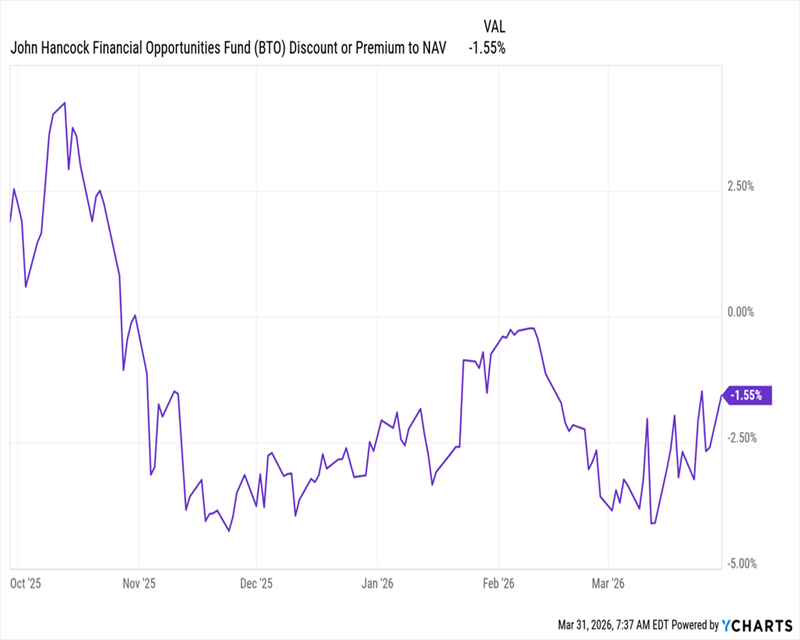

That would be the John Hancock Financial Opportunities Fund (BTO), which yields 7.7% today and, as we’ll see, trades at a discount that’s double what most investors think it is.

Why April 2026 Could Be April 2025 Redux (But With a Faster Rebound)

To see why I think the market is making a mistake when it comes to finance stocks, let’s rewind to last year, when stocks sold off on the so-called “Liberation Day” tariffs.

From the Spring 2025 Selloff …

That selloff has actually looked a lot like this one so far, with a similar depth:

… to Its 2026 “Twin”

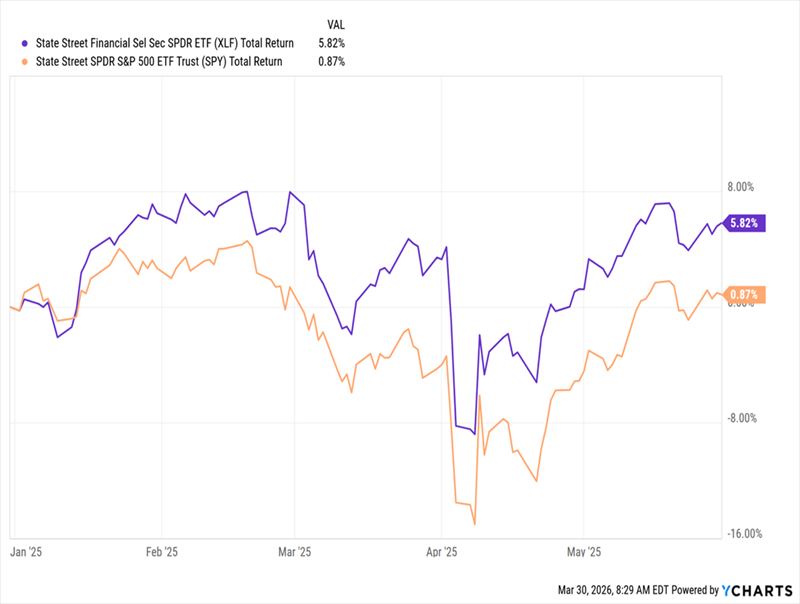

Here’s what I really want to draw your attention to: In 2025, the finance sector—shown by its benchmark ETF in purple below, didn’t fall as hard as the rest of the market, and soared on the other side:

Finance Beat the S&P 500 in the 2025 Plunge …

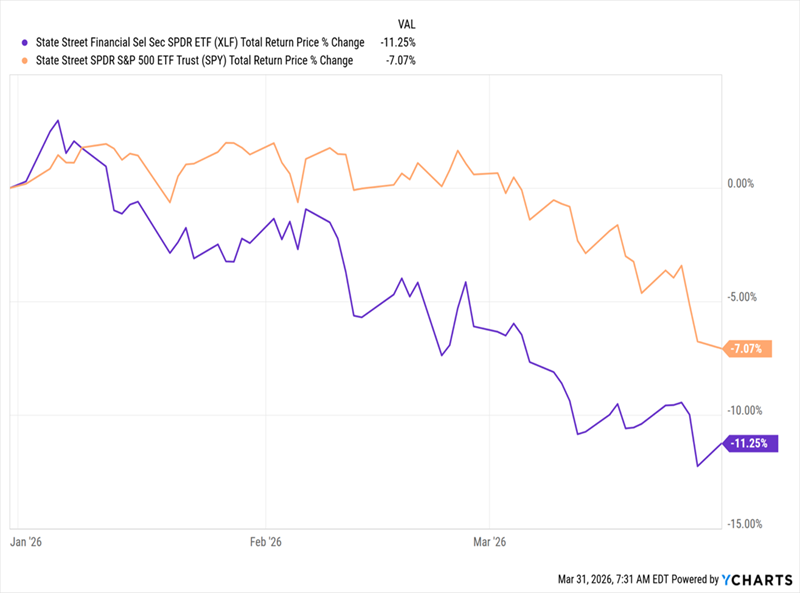

Fast-forward to this year, and finance stocks are being hit harder in the Iran War fallout, falling much further than the market since the start of the year.

… And Looks Like a Coiled Spring This Time Around

That’s excessive, in my view, and positions the sector for a stronger rebound this year. That’s because, at their core, both of these selloffs are about one thing: inflation. Last year, the driver was thought to be tariffs. This year, it’s oil prices.

And last year, it was hard to tell which sectors could win as the administration brought in tariffs on everything from lumber to car parts. This year, it’s easier to peg a winner: oil stocks, which have already surged.

That ship, of course, has already sailed for us, and we never chase trades at CEF Insider. But finance is setting up to be our still-discounted play here, as it’s poised to benefit from two trends stemming directly from the oil-price surge.

First, continued oil-price volatility—almost certain, no matter when the war ends—will drive higher commodities-trading revenue for banks. And if higher oil becomes a “new normal,” oil producers (most of whom are generally cautious about committing to higher production) will eventually expand output—and will of course look for financing to do so.

And then there’s a third angle few investors have even thought of.

Airline-Fuel Hedging Could Be Set for a Comeback

Years ago, airlines used derivative contracts on oil to hedge their exposure to energy prices. Intermediaries (banks, in other words) took a fee for this, alongside other players, like hedge funds. But these programs were expensive to run, so most airlines have wound down their hedging programs over the last decade or so.

“US airlines abandoned the practice of hedging against fuel costs long ago. With oil prices surging following US-Israel strikes ?on Iran, they could be looking at a big bite out of their bottom line in the event of a lengthy conflict that keeps prices elevated for months.”

This March 6 report from Reuters tells us that there may be more demand for options in the future, which is good news for the financial sector broadly.

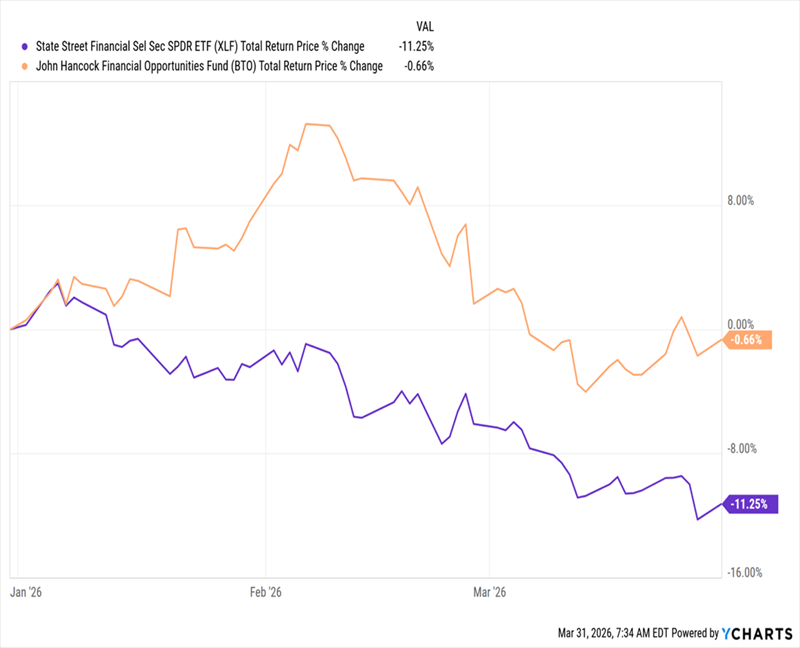

Which brings me back to BTO, which is roughly flat this year (shown in orange below), on a total-return basis as of this writing, compared to the more than 11% decline we’ve seen from the financial sector as a whole:

BTO Falls Less Than Finance …

That’s the kind of resilience we want to see from a CEF in this environment.

And here’s where things get interesting: Even though it’s held up better than the sector, BTO has remained a bargain by another key metric: the discount to net asset value (NAV, or the value of its underlying portfolio).

… While Keeping Its Discount

As you can see above, the fund now trades at a bit less than a 2% discount. And that discount is actually much larger in real terms, because BTO’s valuation is normally well above par, averaging a 3.9% premium over the last five years. Indeed, you can see in the chart above that it’s fallen from around that level just six months ago.

BTO is also notable in that it holds mainly regional banks, and while they may not be as exposed to things like airline fuel hedging, they stand to gain on improving prospects across the sector as a whole. Those in energy-producing areas are likely to do better, like Hancock Whitney (HWC), BTO’s No. 7 holding, based in Gulfport, Mississippi.

Moreover, regionals let us better diversify across the sector, while keeping our focus on the US, the world’s largest oil producer, which accounts for 95% of BTO’s portfolio.

The fact that regionals have been caught in the downdraft that’s affected the whole sector is an opportunity for us to get BTO at a 7.7% yield and that “larger-than-it-looks” discount. This way, we’re setting ourselves up for higher income and potential gains as that markdown moves back to a premium, where it belongs.

In times like these, a growing 7.7% dividend can bring us a lot of peace of mind. But the beauty of CEFs is we can get dividends that are even higher—and pay us every month, too.

That’s right in line with our monthly bills, of course. And if you want to reinvest, great ! Monthly payouts let you do so even faster.

This is not substantive investment research or a research recommendation, as it does not constitute substantive research or analysis. This material should be considered as general market commentary.

Octopus Renewables Infrastructure’s (ORIT) annual results to 31/12/2025 show a NAV total return of -2.8% (2024: +2.5%). At an operational level, ORIT’s power generation and revenues grew by 5% (2024: 7% and 12%), and EBITDA by 3% (2024: 16%). Total shareholder return was -1.5%.

ORIT met its dividend target of 6.17p, 1.14x covered by operating portfolio cash flows (2024: 6.02p, 1.24x). The dividend was an increase of 2.5% over 2024, in line with UK CPI for a fourth consecutive year. The target dividend for the year ending 31/12/2026 is an increase of 1% to 6.23p and is expected to be fully covered. At the current share price (as at 30/03/2026) the yield is c. 10.9%.

The NAV per share was 93.8p (2024: 102.6p), a c. 9% decline. The main components of the fall were adjustments for power prices and green certificates (-4.2p), RoC indexation adjustments (-0.9p), adjustments to developer valuations (-1.4p) and changes in discount rates (-0.7p).

ORIT’s weighted average discount rate, in local currency terms, increased to 7.8% (2024: 7.4%). ORIT’s discount rate is calculated on operational assets, and factoring in the developer company assets as well as impacts of FX and the RCF, the expected portfolio return is 8.2%.

Fixed revenues rose from 84% to 88% (forward fixed for two years), reducing ORIT’s exposure to short-term power price fluctuations. In addition, about half of revenues are inflation-linked over ten years.

ORIT was geared 45% LTV or 82% as a percentage of NAV (2024: 45%), although the level of debt was reduced in absolute terms, with c. £56m paid down over the year. 75% of debt is fixed rate with an average cost of 3.3% and an average remaining term of ten years. The medium-term goal is to reduce gearing to 40% although the managers note this level could fluctuate on a short-term basis.

ORIT defines itself as an impact fund with a core impact objective of accelerating the transition to net zero through its investments and is classified under Article 9 of SFDR. The impact highlight from the financial year is 1,304 GWh of renewable energy generated (2024: 1,240 GWh), with the portfolio having the potential to avoid 344k tCO2. A detailed breakdown including the cumulative impact over five years is in the annual report.

Capital allocation policy update:

Disposals totaling £74.3m brought the total under the policy implemented in 2023 to £235m, achieved at a weighted average uplift of 9%.

£26m of the £30m share buyback now executed.

ORIT 2030. In September 2025, the board announced its ‘ORIT 2030’ strategy, which sets out its four priorities for the next five years.

Grow: Invest for NAV growth, deploying capital into higher growth investments, including an increased 20% target allocation to construction assets, maintaining the current 5% allocation to developers. There will also be a greater focus on asset improvement and disciplined capital recycling.

Scale: Target £1 billion net asset value by 2030, to create a more liquid and investable company. Alongside investment growth, this could include corporate M&A.

Return: Target medium-to-long-term total returns of 9-11% through a combination of capital growth and income, maintaining the progressive dividend policy, while preserving full cover and targeting medium-term gearing below 40%, although this level may fluctuate in short-term periods as mentioned above. Retain diversification across core technologies and geographies.

Impact: Aim to build approximately 100 MW of new renewable capacity per annum (on average over the five-year plan).

As part of the ORIT 2030 strategy, the board is also recommending that the continuation vote moves to a cycle of every three years, from the current five. The change will be put to a vote at the 2026 AGM, with the next continuation vote then held at the 2028 AGM.

Chair Phil Austin said: “The ORIT 2030 strategic framework provides a clear structure for capital allocation and portfolio development over the medium term. The actions taken during FY 2025, particularly in relation to capital recycling, operational optimisation and capital structure discipline, are consistent with the early execution of this strategy.”

Kepler view

Once again, at an operational level, ORIT delivered good performance, with an increase in power generation and revenues. The ORIT management team also note that at a technical level, the portfolio performed well, with less downtime than expected. And diversification played an important role, with lower wind speeds offset by strong performance from solar assets, particularly in the UK.

Further, ORIT completed its fourth consecutive year of dividend growth, essentially increasing its dividend in every full operational year since its IPO. The target for the FYE 31/12/2026 is a further increase, albeit at a lower rate of 1%. Whereas the dividend policy has never explicitly targeted matching inflation, in the past ORIT’s dividend increases have been in line with UK CPI inflation. As ORIT shifts to its ORIT 2030 strategy, which targets higher returns through more investment in construction assets, and strategic recycling of operational assets, the goal remains to target a progressive dividend, but as the strategy evolves clearly a greater exposure to non-yielding construction assets will make it harder to increase dividends in line with inflation. Overall, though, the anticipated result of this shift is an increase in annual returns of 9-11%, up from the 7-8% envisaged at IPO.

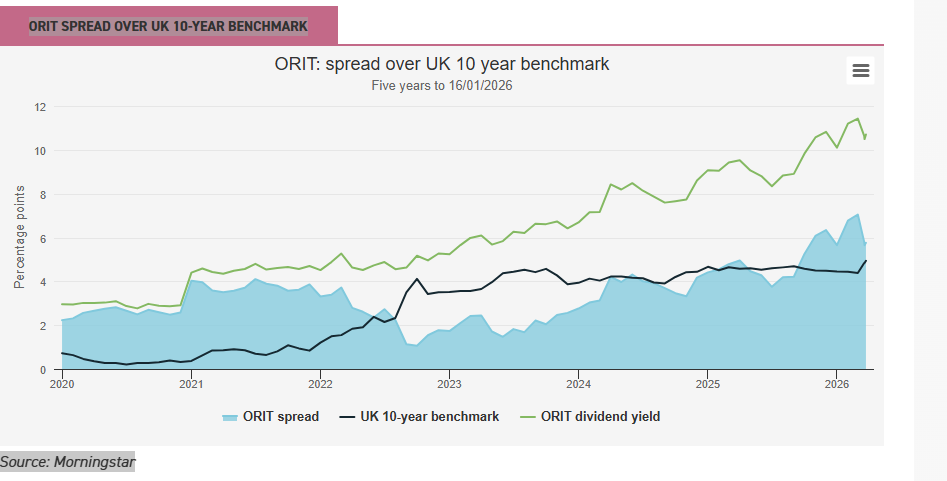

Clearly though, the macro backdrop remains challenging, with ORIT’s peer group of renewable energy infrastructure trusts all trading at wide discounts and, in many cases at dividend yields of 10% or more. This is an interest-rate sensitive asset class, and current events in the Persian Gulf are taking their toll on government bond yields, with the UK 10-year benchmark bond yield briefly touching 5% in recent days. ORIT’s near-term power prices are 88% fixed (for two years) so a short-term spike in energy prices will have little impact, although if longer-term futures rise, there may be opportunities to fix at higher rates further out. Rising interest rates will have an impact, but given these are likely to be a response to higher inflation, and half of ORIT’s portfolio is inflation-linked, revenues would rise, providing partial protection. So, there are push and pull factors that investors need to consider. But in considering the chart below, which shows ORIT’s dividend yield as a spread over the above mentioned 10-year benchmark, it’s worth reflecting that this lifetime-high gap comes at a time when, once again, the UK and other European countries are under pressure to evolve their energy security policy. Notwithstanding the uncertainty around bond yields and inflation, the valuation of assets that generate power without any reliance on global hydrocarbon supply chains seems like an anomaly investors should be paying more attention to.

I’m extremely impressed with your writing talents and also with the layout for your weblog. Is this a paid topic or did you customize it your self ? Anyway keep up the nice quality writing, it is rare to look a nice blog like this one these days..

All my own customizing, with a big help from Copilot for the Graphics.

The current fcast for the first quarter is income of £2,903.00, which is comparable to the yearly fcast of £10,500

The figures includes the next dividend for NESF which after it’s paid will be trimmed but as the dividends are re-invested that will make up the shortfall.

After the long weekend, the SNOWBALL starts again with an empty pot.

The fcast is to earn £10,500 of income, all of which is to be re-invested back into the SNOWBALL to earn more income.

The plan is shown below, if you don’t have a plan with and end destination, you are unlikely to achieve your goals.

The SNOWBALL is in year 4 of the above plan, so if the fcast of £10,500 is achieved the SNOWBALL will be 3 years ahead of plan. The SNOWBALL has outperformed the fcast every year and the intention is to do so again this financial year but the fcast remains unchanged.

Option One

The SNOWBALL has a comparator share VWRP where the current value is

£151,249. Using the 4% rule that would provide a ‘pension’ of £6,051, if you ignore the requirement to have a recommended 3 year cash fund.

Option 2

Use your hardearned to buy an annuity, currently around 7% depending on age etc., so income £10,587. You have to surrender all your hardearned, so not an option, unless you have a fund of a million, then take out an annuity and concentrate soley on spending your income.

Option 3

A dividend re-investment scheme or part option 1 and option 3.

April and therefore every 3 months is a weak month for dividends to be received but remember

Mr. Market is going to present you with some wonderful opportunities.

The SNOWBALL has booked a ‘profit’ of £180 from the recent purchase in MRCH. If the SNOWBALL had bought a full position the ‘profit’ would have been £360 but it didn’t, so it isn’t.

The intention is to buy back the shares that have been sold plus others at a higher or lower price.

Why have bonds not protected investors during the Middle East crisis?

Wednesday, April 1, 2026

Martin Gamble

Shares and Markets Writer

Bonds have historically provided shelter and ballast to portfolios during times of market uncertainty because of their stable fixed income.

That has not happened over the last month because the shock to stock markets has come from rising energy prices. Something which is likely to lead to higher inflation.

The worry is that central banks might be forced to hike interest rates to bring inflation back down, in an echo of what happened coming out of the pandemic.

Inflation is the enemy of bond investors because it reduces future spending power. For example, if inflation were to average 5% over the next 20 years it would shrink the value of £1,000 today to around £375.

These concerns have pushed up bond yields (prices move inversely to yields) since the end of February with UK 10-year gilt yields rising from 4.3% in late February to 4.9% in late March.

Two-year yields which more closely mirror expectations for the direction of Bank of England base rate have increased by almost one full percentage point, reversing prior expectations for interest rates to fall in 2026.

The reason bond prices fall is because new government debt will be issued with higher, prevailing yields which make existing bonds less attractive.

What has been the impact on bond portfolios?

Bonds are sensitive to changes in interest rates and as a rule of thumb, longer-dated bonds are more sensitive than shorter-dated issues.

For example, 10-year bonds have seen a price fall of around 5% over the last month, while two-year bonds have lost around 2% of their value.

This means that investors holding a diversified UK gilts fund, could have experienced losses of between 2% and 5% depending on the composition of bonds held.

Remember that no capital losses are incurred when government bonds are held until maturity, because they expire at the same price they were issued.

The corporate bond market has also been impacted by rising yields with UK investment grade (the highest quality part of the market) bond yields rising by around 0.5% to 5.4%.

This is reflected by diversified investment grade bond portfolios dropping by around 3.5% since the end of February. Corporate bonds typically have higher yields than government bonds to reflect the higher risk of default.

It is also worth emphasising that Bank of England policy makers have urged caution and recognise that aggressively hiking interest rates into an energy shock could do serious harm to the economy.

Even so, it could be a close call with market prices implying a 50% chance of a rate hike at the April or May meeting, which is a big change from the 80% chance of a rate cut priced into markets just four weeks ago.

What could happen if current mediation hopes falter?

Recent events indicate US-Iranian talks are finding some traction, implying the conflict is likely to be short lived. This scenario is the base case for most economists although the range of outcomes remains wide.

This view is supported by the state of the oil market which has been in deep contango (meaning oil derivatives are trading at levels that imply prices will be lower in a few months) since the war began.

However, the longer the supply of oil from the Strait of Hormuz remains blocked, the greater the potential damage to the global economy. It is useful here to think of higher energy costs as a tax hike.

It means consumers have less to spend on other things and given consumer expenditures represent two thirds of the economy, this is important.

In other words, at some point a sustained rise in energy costs will start to impact economic growth and potentially lead to interest rate cuts as central banks look to stimulate the economy.

Remember that no capital losses are incurred when government bonds are held until maturity, because they expire at the same price they were issued.

If you buy above the issue price of £100, you will make a capital loss.

If you buy a long dated gilt and you have to sell you could make quite a large loss if the market moves against you.