Not Naval gazing, that’s a totally different topic for boys and girls.

At 207%, the Warren Buffett indicator says the stock market could crash!

Zaven Boyrazian, CFA

Sun, 10 Aug 2025

The Motley Fool

Billionaire investor Warren Buffett has shared a lot of wisdom throughout his successful career. However, one gem to come off his desk is the Buffett Indicator – a simple comparison of the US stock market’s total value divided by US GDP.

As Buffett puts it, the indicator is “probably the best single measure of where valuations stand at any given moment”. And for value investors, knowing when the stock market is overpriced is a powerful advantage, even when relying only on index funds.

However, looking at the Buffett Indicator today might cause some concern.

US stocks are expensive

Historically, his Indicator has sat between 90% and 135%. This healthy range generally indicates that US stocks are fairly-to-slightly overvalued and presents an ideal window of opportunity to top up on investments. But following the tremendous artificial intelligence (AI)-driven returns of 2023 and 2024, the indicator’s been rising. So much so that it now sits at a whopping 207%!

That’s the highest it’s ever been since records began in the 1970s. And it’s even higher than the 194% peak seen in late 2021, right before US stocks experienced one of the most severe market corrections seen in over a decade.

That would certainly explain why Buffett and his team at investment vehicle Berkshire Hathaway have been busy selling stocks lately. In fact, the firm just marked its 11th consecutive quarter of being a net seller, with positions such as Bank of America, Citigroup, and Capital One all getting trimmed, or outright sold off.

So could another stock market downturn be just around the corner?

Panic isn’t a strategy

The stretched valuation of US stocks definitely creates cause for concern. However, there’s no guarantee a crash or correction will actually materialise. Therefore, panic selling everything today likely isn’t a sensible strategy, and it’s why Buffett, despite higher selling activity, still has plenty of capital invested in the US stock market.

Dividends can be more reliable than share prices as they’re driven by the companies performance itself and not by the whim of investors.

As part of a total return / reinvestment strategy, this income could be reinvested into income assets or back into the equity market depending on the relative valuations.

The emotional benefits of dividend re-investment, in fact, with this investment strategy you can actually welcome falling share prices.

Howdy are using WordPress for your site platform? I’m new to the blog world but I’m trying to get started and create my own. Do you need any coding expertise to make your own blog? Any help would be really appreciated!

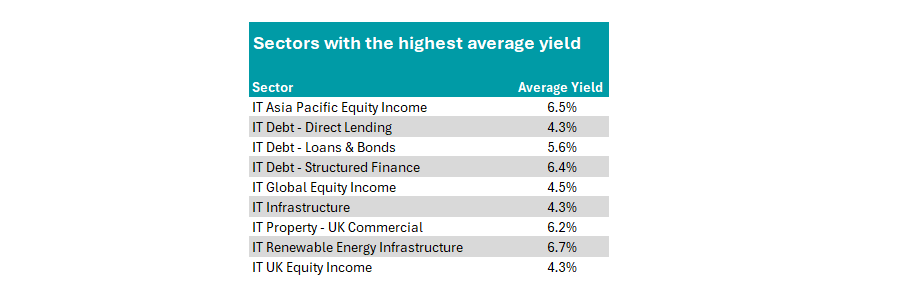

Some 88 investment trusts are paying interest-rate busting dividends, according to research by Trustnet, potentially offering a haven for income-needy savers who are unsure where to put their cash.

Last week the Bank of England cut rates from 4.25% to 4%, a move unlikely to be well received by savers, as it should bring bank and building society savings rates down with it.

This may encourage more people to look to invest their cash, with some investment trusts offering significantly higher yields than the current base rate.

These could be ideal for more adventurous savers during this period of lower rates and higher inflation, and can offer more consistent income than funds thanks to their ability to retain up to 15% of income generated each year in reserve.

Investment trusts in the IT Renewable Energy Infrastructure sector have the highest average yield at 6.7%, closely followed by IT Asia Pacific Equity Income and IT Debt – Structured Finance.

Source: FE Analytics

But which investment trusts across these sectors offer the highest yield? Below we look at the top-yielding trusts from the highest-paying sectors.

The £26.6m trust was launched in 2021 and aims to generate returns – principally in the form of income distributions – by investing in a diversified portfolio of energy efficiency investments.

While the dividend may be enticing, investors should note that a higher yield can signify higher risk. For example, this trust has disappointed against its sector from a total return basis, languishing in the fourth quartile across three months, six months, one year and three years.

The trust’s shares trade at a 37.6% discount to the net asset value (NAV).

In second place is another renewable energy specialist, NextEnergy Solar Fund Limited Trust, with the £435m trust’s dividends representing an 11.2% yield.

Also trading at a discount (28.8% to NAV), the growth-focused trust was launched in 2014 and has an over 80% weighting in the UK, 12.4% in Europe ex UK and 3.5% in international.

It has managed a top-quartile performance over three-, five- and 10-years, delivering a 46.5% total return over a decade. However, it has struggled in the past year, managing a 1.4% return compared to its sector average of 5.9%.

Turning to equities, Henderson Far East Income in the IT Asia Pacific Equity Income sector has the highest payout, with a 10.9% yield.

Managed by Sat Duhra since 2019, the £417m trust is heavily weighted to financials but has some 15% in technology names – unusual for an income portfolio.

While there are concerns hanging over the region, such as global trade relations souring between the US and China, there are bright spots, according to the manager.

“The outlook for dividends in the region remains robust as positive free cashflow generation alongside the strength of balance sheets – with record cash being held by corporates – provides a strong backdrop across a number of sectors and markets across the region,” he said in the trust’s latest factsheet.

Despite the manager’s optimism, the trust has failed to perform in recent years, languishing as the worst trust in the sector over one-, three-, five- and 10-years.

By contrast, the £772.4m Invesco Asia Dragon Trust has outperformed its sector across one-, three-, five- and 10-years – delivering 188.2% total return over the decade. It offers a slightly lower yield of 5.3% but still beats the Bank’s base rate.

Managed by Ian Hargreaves since 2011 and Fiona Yang since 2022, it aims to grow its NAV in excess of its benchmark index, the MSCI AC Asia ex Japan index. The trust is at a 6.1% discount to NAV.

There were three UK trusts on the list, with Merchants Trust the pick of the trio, sitting in the top quartile of the IA UK Equity Income sector over five and 10 years. It has struggled more recently, however, sat in the bottom quartile over more recent timeframes.

It offers investors a 5.3% dividend yield.

By contrast, the £176.8m Aberdeen Equity Income Trust, which is offering a 6.3% yield, has been on a strong run over the past one-, three- and five-years, but struggled over the decade.

Managed by Thomas Moore, it aims to provide shareholders with an above average income from their equity investment while providing real growth in capital and income. Top holdings include British American Tobacco, HSBC and BP.

Chelverton UK Dividend Trust is the highest-yielding of the trio at 9% but has failed to beat its average peer over one, three, five and 10 years, as well as over shorter time periods.

Your Snowball should be different to the blogs, generally the longer you have to retirement, you can take a higher risk as you have longer to correct any clunkers.

Alternative Income REIT PLC ex-dividend date Aquila European Renewables PLC ex-dividend date Assura PLC ex-dividend date Baillie Gifford UK Growth Trust PLC ex-dividend date Bellevue Healthcare Trust PLC ex-dividend date BlackRock American Income Trust PLC ex-dividend date BlackRock Throgmorton Trust PLC ex-dividend date EJF Investments Ltd ex-dividend date Fair Oaks Income Ltd ex-dividend date Greencoat Renewables PLC ex-dividend date Greencoat UK Wind PLC ex-dividend date ICG Enterprise Trust PLC ex-dividend date Impax Environmental Markets PLC ex-dividend date International Public Partnerships Ltd ex-dividend date Invesco Global Equity Income Trust PLC dividend payment date Majedie Investments PLC ex-dividend date Murray Income Trust PLC ex-dividend date NextEnergy Solar Fund Ltd ex-dividend date Octopus Renewables Infrastructure Trust PLC ex-dividend date Pershing Square Holdings Ltd ex-dividend date PRS REIT PLC ex-dividend date Schroder Real Estate Investment Trust Ltd ex-dividend date Scottish American Investment Co PLC ex-dividend date Starwood European Real Estate Finance Ltd ex-dividend date Target Healthcare REIT PLC ex-dividend date The Renewables Infrastructure Group Ltd ex-dividend date Tritax Big Box REIT PLC ex-dividend date

I’m the Chief Investment Strategist at Contrarian Outlook.

Today I’m going to reveal a simple strategy that could triple many investors’ dividend income in just a few years—without making any high-risk, highly speculative investments you can’t tell your spouse about.

I call it the “Recession-Resistant Retirement Plan.”

Now you might believe that to double or triple your dividend income, you would need to find the next Amazon, Facebook or Google and get in at ground zero.

However, this just isn’t true.

In fact, as you’re about to see, investors who endlessly chase these unicorns tend to lose a lot of money—and lose it fast.

The truth is, these breakthrough companies are one in a million, and trying to fund your retirement with them is the fast track to the poor house.

The same goes with the latest cryptocurrencies (which, although they’ve soared recently, have a long history of cratering overnight), penny stocks, profitless tech startups and every other overhyped stock you hear the so-called gurus telling you to “buy, buy, buy!”

Personally, I don’t see why you would want to gamble on your future.

Especially when there are safe, secure stocks that are nicely positioned to return 15% per year on an annualized basis in the long run, no matter what direction the market goes.

It’s stocks like these that I specialize in finding.

And today I’m going to share my exact process with you. Then I’m going to give you …

5 Recession-Resistant Stocks Set to

Deliver 12% to 20% Returns Per Year

In Both Bull and Bear Markets

But first, let’s get one thing straight.

Do you agree, if you were looking for the perfect retirement portfolio it would:

Pay real, spendable income – not just paper gains.

Be built on safe, secure stocks that are much less volatile than the typical stock.

Continue paying—even if the market crashes.

Be cash-flow rich, free from major debt and profitable.

Pay a generous—and ever-growing—dividend.

Keep growing revenues year after year after year.

Be safe from new competitors.

And most important of all …

Do you agree that your recession-resistant retirement portfolio would be built on the undervalued, overlooked and often-ignored stocks other investors miss? The stocks you can buy for pennies on the dollar and watch soar over time?

As I said, I specialize in uncovering these contrarian stocks …

The plays an intelligent, income-focused investor could use to double or triple their wealth every few years.

The investments that are designed to protect against wild market swings so you can enjoy a stress-free, secure retirement.

The stocks that can be held for years without the “can’t-sleep-at-night” worries.

So, if you’re retired or you’re looking to retire soon, this may be the most important investment advice you ever read.

Bold claim, I know.

But please bear with me for just a couple minutes …

Because I’m going to show you, step-by-step, how to find the stocks best positioned to deliver double-digit annualized returns—through boom, bust, inflation, deflation, you name it

Better yet, I’m going to show you how to do this without making any highly speculative, high-risk bets. Everything you’ll discover is focused on buying reliable stocks with rock-solid fundamentals, strong cash flow and terrific long-term prospects.

So while other investors lose their shirts chasing the latest unicorn …

You could be quietly doubling—even tripling—your retirement income by investing in what I call the “Hidden Yields.”

In just a moment, I’ll tell you how to build a recession-resistant retirement plan with these Hidden Yield stocks, and I’ll tell you about 5 specific names to buy now.

But first, let me tell you a little bit more about myself …

Today I’m writing to you from sunny Sacramento, where the tech industry is still growing, thanks to massive investments in AI. But tech execs are also growing more worried about the trade war, and what it might mean for the vast amounts of revenue they pull in from outside the US.

You may have seen me on CNBC, Yahoo Finance or NASDAQ, where I’ve been called on to share my methodology for collecting consistent, predictable and reliable retirement income without making any wild, speculative bets that keep you up at night.

You see, I take a strategically contrarian approach to the markets.

And for the past several years, I’ve helped thousands of readers fund their retirement thanks to what I call “Hidden Yield stocks.”

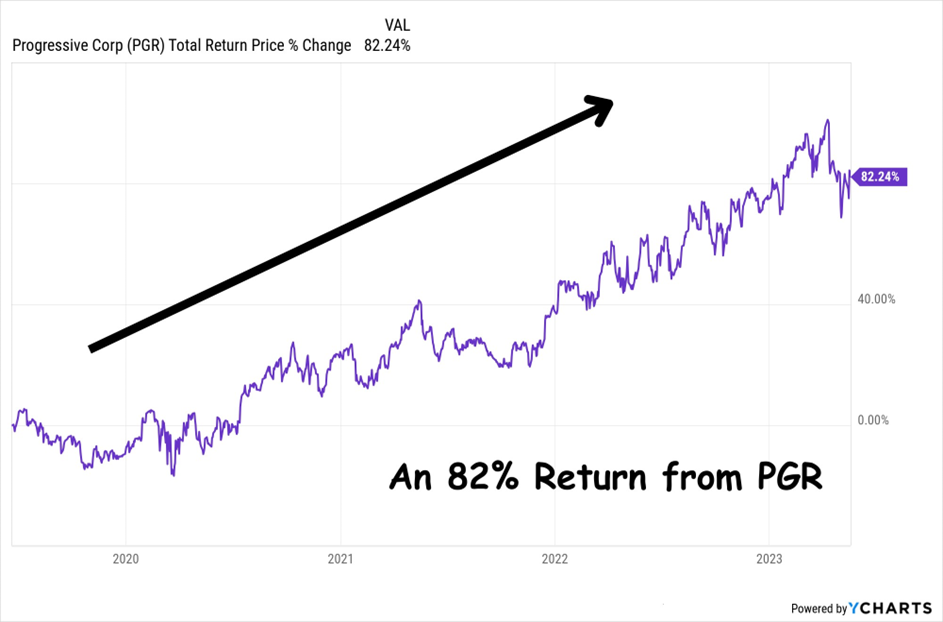

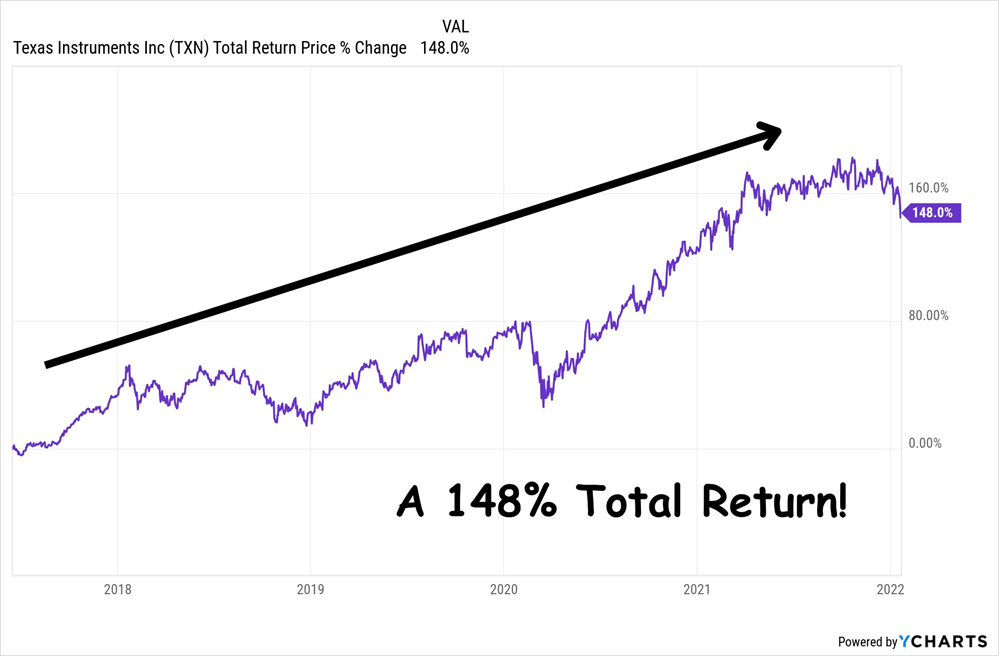

For example:

82% on Progressive Corp. in Just Under 3 years

22% on Microsoft in just 3 months

83% on Synnex Corp. in 24 Months

148% on Texas Instruments in just over 4 years

Now, I know these aren’t the huge 500% … 1,000% … or 5,000% overnight gains you hear other gurus CLAIMING they can get you.

But—as you’ll see in just a moment—outrageous claims like these are nothing more than overhyped promises designed to separate YOU from your money.

And to be clear, not all recommendations play out as well as the four examples above. Investing in the stock market is inherently risky, and some recommendations have lost money.

So we level-headed contrarians don’t chase unicorns.

We don’t listen to smiling swindlers.

We don’t put our family’s futures in jeopardy.

Instead, my readers and I focus on …

Doubling Our Money Every 5 Years with

15% Total Returns Per Year on Little-Known

“Hidden Yield Stocks”

However, this is just one small part of what I do.

My real aim is to help investors safeguard their retirement from recessions with low-volatility—but highly lucrative—investments that consistently pay you, whatever direction the market goes.

This method lies very close to my heart and ethics.

You see, my first experience in the markets was brutal …

It was 2003, and I’d recently graduated from Cornell University and was designing computer systems for Fortune 500 companies. For the first time in my life, I was making money. So I decided to hire a broker to help grow my savings.

This guy had countless credentials and certifications, years of experience, and he talked a great game.

Without hesitation, I hired him.

The result?

Just one year later, this so-called expert had literally lost nearly ALL my money. Everything. Years of saving and investing, gone.

As you can imagine, I was furious. However, thanks to this experience, I came to a huge breakthrough. I realized that nobody is EVER going to care about MY money, MY future, MY retirement and MY family as much as I do.

And, I realized, if I wanted to retire rich, I needed to take control of my money.

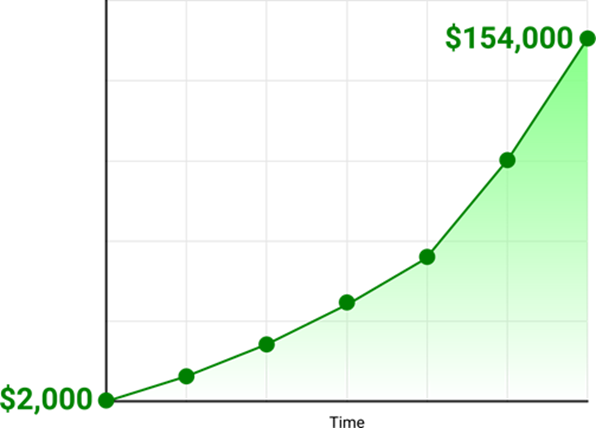

Anyway, with this realization, I decided to learn everything I could about investing. I was absolutely relentless. And after a few bumps in the road, it paid off, starting with a measly $2,000 that I turned into $154,000 in just 48 months!

Obviously, this sort of performance doesn’t go unnoticed …

Shortly afterward, I was invited to join a famous financial publication as an editor.

At first it was great. We helped our readers take home huge profits, exponentially grow their portfolios and finally create the financial freedom they’d been chasing their whole life.

However, as time passed, things started to change …

Instead of focusing on secure, safe stocks with huge upside, they started recommending all sorts of highly speculative, high-risk “investments” like obscure cryptocurrencies, volatile penny stocks and many other questionable opportunities.

Anyway, this didn’t sit well with me.

I believe financial analysts like me have an ethical and moral duty to help our readers safely grow their money—not recklessly gamble it away on some pie-in-the-sky idea.

Which is why I decided to set up my own research firm—Contrarian Outlook.

Since inception, the goal of Contrarian Outlook has been simple:

All without making any highly speculative bets you can’t tell your spouse about … without trying to time the markets … without the can’t-sleep-at-night worries … and without putting your retirement at risk!

Today I want to share five of my recession-resistant “Hidden Yield Stocks” with you.

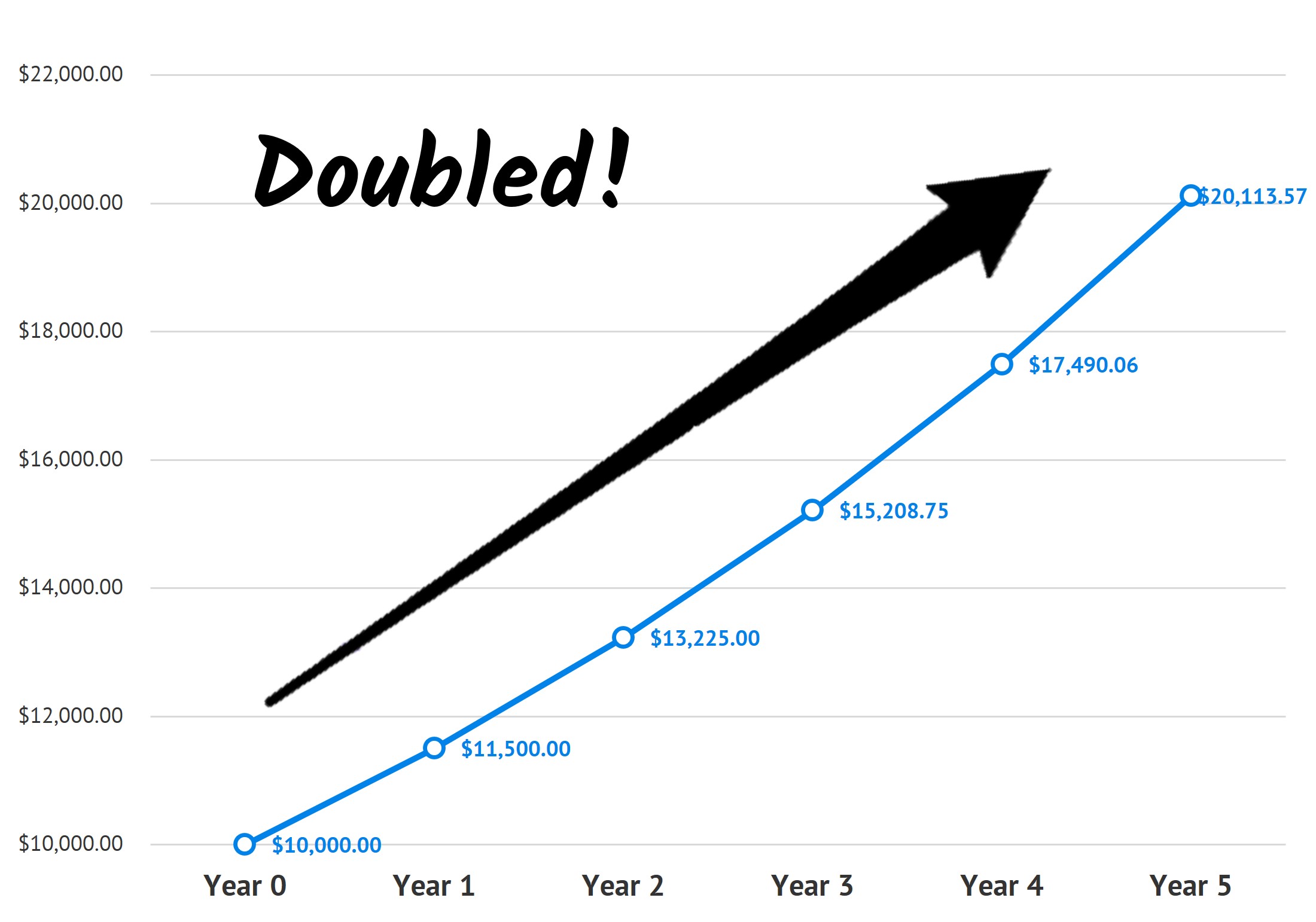

My research indicates each of these investments could deliver 15% total returns per year – even as we stumble towards a recession.

As you can see in the chart below, that’s enough to double your money every 5 years!

15% Average Annual Return on $10,000 Compounded Over 5 Years

Still skeptical?

Good. I would be, too.

Which is why I don’t expect you to just take my word for this.

Instead, I’m going to prove everything to you.

I’ll walk you through my investment approach. I’ll show you how to identify these “Hidden Yield Stocks.” And I’ll give you the cold-hard evidence that proves you can double—even triple—your portfolio without taking on any unnecessary high-risk bets.

Then I’ll give you 5 of my favorite recession-resistant “Hidden Yield Stocks” to buy now.

Here’s the Time-Tested Way to Make

15% Per Year From Stocks

There’s an untapped portion of the market few people know about …

It’s filled with stocks that seem “boring” to the uninformed investor…

Companies that rarely get coverage from the mainstream media …

Contrarian investments that are hiding their true potential …

However, if you look below the surface and read between the lines, these “Hidden Yield Stocks” offer intelligent investors the opportunity to deliver 15% total returns per year—no matter what the wider market does.

How?

Well, the answer lies in what I call “The Three Pillars.”

Pillar #1 – Consistent Dividend Hikes

Pillar #2 – Lagging Stock Price

Pillar #3 – Stock Buybacks

Together, these three pillars allow us to identify the stocks that are undervalued … overlooked … recession-resistant … and primed for major growth.

And by investing exclusively in these “Hidden Yield Stocks,” we can enjoy massive upside with very little downside … plus collect regular, reliable income through healthy dividend payouts!

As I said, today, I want to give you 5 of my favorite “Hidden Yield Stocks.”

But first, let me briefly explain each of the Three Pillars and show you how it helps to predict—with pinpoint accuracy—the direction a stock is going to take.

Pillar #1 – Consistent Dividend Hikes

Most investors approach dividend paying stocks backward.

Here’s how it usually works …

An investor will scan the markets looking for stocks paying a high dividend. After all, if a company is currently paying a high yield, it’s a great investment, right?

Dead wrong!

In fact, looking at the CURRENT yield is one of the slowest ways to grow your money.

You see, if you’re focused on current yields, you’re too late to the party. All the major gains have already been made. You’ll need to settle for earning a paltry 4%, 5%, maybe 6% per year … with minimal stock-price appreciation, too.

Sure, chasing high current yields will provide you with instant gratification, but it won’t give you the recession-resistant income … or the 15% year on year returns we want.

Instead, you need to focus on consistent dividend hikes.

In my opinion, selecting companies with a proven track of increasing their dividend payments is one of the safest, most reliable ways to get rich in the stock market. You see, every time a company raises its dividend, you start earning more from your original investment.

For example:

On a $1,000 initial investment, $30 in dividends equals a 3% return. Later, if the dividends go up to $40 a year, you are effectively earning 4% on your initial $1,000 investment.

As this trend continues, you could easily be earning 10%, 15%, even 20% per year just from rising dividends, as your initial investment never changes.

However, this ever-growing income from dividend hikes is just ONE part of the puzzle. To engineer real growth and quickly double an initial investment, we must combine Pillar #1 with the next two pillars of “Hidden Yield Stocks.”

Pillar #2 – Lagging Stock Price

After years of active investing, I’ve only ever found one surefire way to predict whether a stock will go up or down.

I call it the “Dividend Magnet,” and here’s how it works …

After you’ve identified stocks that are built on the foundations of Pillar #1 (consistently hiking their dividends), you want to narrow your search to companies whose share price LAGS behind the rate of dividend increase.

Why? Well, it’s simple really …

Share prices almost always increase as dividends increase.

This is because as a company hikes its dividend, mainstream investors tend to flock to the stock, chasing the new, higher yields. And this inevitably bids up the share price.

Let me give you a few examples where the dividend acts like a floor to keep bumping the share price higher:

UnitedHealth Group: Dividend Up 460% Share Price Gains 510%

Mastercard: Dividend Up 500%, Share Price Gains 532%

Cisco Systems: Dividend Up 111%, Share Price Gains 113%

As you can see in these examples, the stock price lags behind the dividend increases at some point in time …

However, as more investors notice the company’s soaring dividend and buy in, the price lag closes—sending the share price soaring.

So, by investing in the right companies whose share prices have fallen behind despite consistent dividend hikes, you can buy the stock, safe in the knowledge the Dividend Magnet will eventually pull the price up.

Now, investing with Pillar No. 1 and No. 2 alone would stand you in great stead.

However, there’s one final Pillar of a “Hidden Yield Stock” that can rapidly accelerate both the share price and dividend payouts …

Pillar #3 – Stock Buybacks

Uncovering companies that are buying back their stocks is one of the fastest ways to accelerate your gains.

You see, when a company buys back its stock, it is improving every single “per share” metric investors watch (earnings, free cash flow, book value, etc.).

After all, if a company reduces the number of its shares by 50%, its earnings per share will automatically DOUBLE without any actual increase in profits. And I probably don’t need to tell you what will happen next …

Investors quickly bid up the stock’s price to bring it back in line with the value it was trading at before. Indeed, my research shows that simply investing in stocks that are reducing their share counts can help you beat the broader market’s performance.

And it’s important to bear in mind that S&P 500 companies are sitting on huge piles of CASH (more than $1 trillion in all!). They’re rolling out fresh buybacks amid continued economic growth post-pandemic, and they’re getting a nice upside kick in return.

You can see this just by looking at the shares of Union Pacific (UNP), which took an impressive 31% of its stock off the market in 10 years, helping drive a 100% gain in the share price!

And that’s just one example. By targeting cash-rich companies that either continue to buy back shares now or have a long record of doing so (even if they’re holding off today), you can set yourself up for HUGE price gains.

In short …

Combine the Three Pillars … Buybacks,

Dividend Hikes and Price Lags, and Your

Yearly Returns Can Be Absolutely Astounding

For example, in April 2020, as the world was shutting down, I recommended food maker Mondelez International (MDLZ) because it looked cheap … was consistently growing its dividend payments … and management was aggressively buying back shares.

These three pillars told me the stock would skyrocket. And just take a look at what happened …

Over the next three years, Mondelez reduced its share count by 4.6% (orange line in the chart above) while raising its dividend a whopping 35% (blue line).

The market quickly responded, and the stock delivered a 39% price gain (purple line) by the time I recommended selling in April 2023.

Put it all together and that’s a 48% total return (green line) in just 3 years from a relatively boring (at the time!) company.

Of course not all of my recommendations work out exactly like this one … some better, some worse… and I’m no longer recommending MDLZ today.

But this example shows you that you don’t always need to take big risks or invest in things you don’t understand. All you need to do is sniff out these “Hidden Yield” stocks before the mainstream crowd catches on.

With These 3 Pillars, Uncovering Safe,

Secure Stocks Set to Return 15% Per Year

Is Like Shooting Fish in a Barrel

However, it still takes a lot of work …

You see, although these three pillars can help you beat the market, double your portfolio and enjoy true security in your retirement, you also need to analyze these “Hidden Yield Stocks” in excruciating detail before investing.

Not a prospect too many people look forward to …

Fortunately for you, I love this sort of in-depth financial research!

And, right now, I want to tell you about …

5 Hidden Yield Stocks to Buy Now

My research shows they will not only pay a healthy—and continually growing—dividend, but their stock prices are primed for major increases over the coming years.

Of course, no one has a crystal ball or can claim 100% certainty that any of their recommendations will play out exactly as they say, so let me explain why I’m so bullish on these stocks, even in these uncertain times …

But first, let me explain why I’m so bullish on these stocks, even in these uncertain times …

Hidden Yield Stock #1

201% Dividend Growth and Massive Upside

Our first stock is a biotech cash cow boasting 61% gross profit margins and a dividend that’s soared 201% over the past decade. The share price? It’s followed the payout higher, like a loyal puppy dog.

This firm generates so much cash that raising its dividend barely dents its cash flow. The company also buys back shares when they’re cheap. Over the past decade, management has taken 29% of its “float” off the market:

Pick No. 1’s Steady Share Buybacks

In recent years, this firm has been buying other firms specializing in treatments for rare diseases. There are more than 10,000 of these conditions identified today, but only 5% have approved medicines. As an established biotech, it has the R&D and manufacturing know-how to bring these drugs to market.

Since 2020, the drug maker has boosted rare-disease product sales from $2.2 billion to $4.2 billion. Yet the stock still hasn’t caught the media’s attention. Let’s jump in now, before it does.

Hidden Yield Stock #2

Death, Taxes and…

Death, taxes and the cyclical nature of natural gas are the only three rules of life. Natural gas has fallen due to trade war worries as I write this, but it always bounces back. The cure for low prices is, after all, low prices.

And that means Stock #2 is set to soar.

The reason for this is simply supply and demand. When natural gas prices are low, producers stop producing. Which means less supply.

Natural gas companies can cut (“shut in”) production quickly. They do it out of self-preservation—to save money so that they can live to see another “up cycle” in prices.

Of course they all cut at once! Which crimps supply. Which ensures rising prices that eventually test the ceiling, because it takes years to bring back higher supply. These firms cut quickly and ramp slowly.

When natural gas is low and due to rally, Stock #2 is my “go to” stock.

It’s sitting on nearly 4,000 drilling locations on proven reserves, literally decades of inventory!

This one is cheap now, and management is calling for a continued rise in demand (and by extension prices) as consumption of liquefied natural gas (LNG) doubles by 2050, driven by heightened demand from Europe.

The vast energy appetite of artificial intelligence is another growth driver here.

We could easily double our money because its stock price is due to climb. For months and even a few years, tickers can meander independently of their dividends. But eventually, they follow their payouts higher:

This Dividend Magnet Is Due

Let’s listen to this cash cow, which is imploring us to buy it—before Wall Street catches on.

Hidden Yield Stock #3

A “Dead Money” Play That’s Returned

Nearly 2,000%

This is my “go to” manufacturer and distributor for agricultural, construction and forestry equipment. In recent years, the company has expanded into financial services and solutions for its own equipment and technology as well as other ag projects.

And what a winner! Over the last 20 years, it has returned nearly 2,000% to its shareholders. This is one great company to buy and sock away for a long time.

But it’s best to buy on the dips when wheat is down. Troughs in wheat tend to mark lows in profits—and its price follows:

Buy When Wheat Bottoms (and Sell Tops)

Over the last 20 years, wheat and grain prices have rallied and reversed several times. But there’s been one consistency, which is the lynchpin for big returns—returning cash to shareholders.

Most of this manufacturer’s cash—about 63%—has been returned to shareholders through dividends and buybacks:

Divvie Up 170%, Share Count Down 19%

Fewer shares mean fewer dividends to pay, creating more cash for the firm to raise its divvie for those who hold on. This virtuous cycle is outstanding for shareholders.

Plus, management knows how to deal with corn and wheat prices: control costs, keep generating cash and be ready for that next boom.

Ag prices will take off again soon. It’s a matter of when, not if. They are scraping the basement floor right now. Stock #3, meanwhile, is reasonably priced for a blue chip at just 18-times earnings—depressed earnings.

This is “dead money” to Wall Street, which means now is the time to start grazing before the herd catches on.

It’s very unlikely you have a million in cash to invest and if you did have it’s doubtful you would take the risk on investing for dividends until you DYOR.

But the sooner you start, the sooner you will finish.

Investing can be the key to unlocking life milestones that allude so many younger people (Photo: Richard Drury/Getty)

My entry to the world of work in August 2016 coincided with the Bank of England lowering its base rate to 0.25 per cent – the lowest level on record (until 2020 at least).

Throughout the following seven years as the base rate – and therefore savings rates – fell further, these low-paying accounts were where I funnelled any hard-earned cash I had left over after paying my rent, bills and other costs each m

Inflation throughout that period regularly topped 2 per cent, and therefore in effect, I was haemorrhaging money left, right and centre.

In that period between 2016 and 2023, if I’d put my money in investments I could have had returns of more than 100 per cent on my original deposit, instead of the less than 15 per cent I made on cash.

That’s not the case. I could have had this return simply by putting the cash into a fund that tracked the performance of 500 of the biggest companies listed on stock markets in the US – an S&P 500 tracker – and forgetting about it for seven years.

Granted, US stock market performance has been particularly strong over the past decade – and I’d have had no way of knowing nine years ago that this would be the case – but it serves to illustrate how much harder your money can work in investments, as opposed to cash.

So why didn’t I make the move back in 2016? And what do I wish I’d have known back then, that I do now?

It’s not as hard as it seems

You don’t. If you’re not comfortable buying individual equities, a simple option is to invest in exchange-traded funds (ETFs). These expose your money to a basket of different investments, which could include stocks, but also currencies and other commodities like gold.

In the most simple case, you can invest in ETFs which simply passively track the performance of major stock markets. One option being the likes of an S&P 500 tracker or an All-World tracker – which exposes you to thousands of stocks in countries across the globe.

But if even doing this feels too much, an alternative option is to get a managed investment account, where someone manages your money for you.

Although this can be a good entry point into investing, remember that you will be charged a fee for this, and there’s no guarantee your return will actually be better than if you do it yourself.

Understanding the ‘risk’ factor

The second point I wish I’d known is the level of risk you are encountering with investing. With cash, your money can of course only go upwards. When investing, there is a risk that you lose money, as well as gain it, we are often told.

Of course, though the above is true, it needs to be put into context. Though stock markets do dip from time to time – think the Covid pandemic or the aftermath of Donald Trump’s tariff blitz in April – they tend to recover and grow over the longer term.

Even the FTSE 100, which tracks the biggest UK stocks, has grown 30 per cent over the past decade despite multiple dips.

Your risk of losing money is also less if you put your money in a range of diverse investments, like an ETF, rather than buying large amounts of individual stocks.

The downside of cash savings

Finally, I wish I’d better understood that having your money in cash is not risk-free.

Although you can’t lose money in cash terms – you’ll always end up with a higher total sum than you started with – if your savings are languishing in accounts that pay interest of below the inflation rate – currently 3.6 per cent – you are really losing money in real-terms.

If this happens repeatedly over time, you are compounding your losses, when an alternative exists.

Ultimately, more and more young people are starting to slowly learn that investing is the best way to grow their wealth.

Industry figures show that in February 2020, 19 per cent of 18- to 34-year-olds had investments, but by May 2022 this proportion had increased to 29 per cent.

Investing can be the key to unlocking life milestones that elude so many younger people.

It’s never too late, but the earlier you begin, the better.

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

Earning £10,000 a month in passive income is a financial milestone that many UK investors aspire to. Whether it’s to fund an early retirement, achieve financial independence, or simply provide peace of mind, reaching this level of income is possible.

However, it requires careful planning and a well executed strategy. And, of course, it makes sense to do this through a tax-efficient Stocks and Shares ISA.

With its exemption from income and capital gains tax, the ISA’s a powerful tool for UK investors. But generating £120,000 a year in passive income from an ISA alone is a tall order. To reach that level of cash flow without drawing down capital would need a substantial portfolio. What’s more, investors would need an asset allocation designed to yield reliably.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

So how much?

So how much is “substantial”? The answer depends on several variables. Chief among them is the average yield of the investments held within the ISA.

A portfolio yielding 4% annually would require a value of £3m to produce £120,000 a year in income. At a 6% yield, the required capital falls to £2m. Of course, higher yields often come with greater risks, including income volatility as well as capital erosion.

Now, many readers may have zoned out at £2m or £3m. However, for those starting early enough, reaching these figures is very possible.

Take the case of investing £500 a month over 40 years with 10% annualised returns. In the first decade, progress can feel modest. After 10 years, the portfolio’s worth just over £100,000.

Source: thecalculatorsite.com

But compounding begins to accelerate. By year 20, the balance grows to around £380,000, and by year 30 it passes £1.1m. In the final 10 years, growth becomes dramatic: the portfolio adds over £2m, ending above £3.1m by year 40.

Despite contributing just £240,000 in total, over £2.9m comes purely from reinvested gains. This is the exponential nature of compounding. It starts slow, then surges.

Of course, it’s not all plain sailing. There are risks involved with investing, and we can lose as well as gain money. What’s more, 10% may prove to be a challenging target for some investors.

An investment for the long run?

Investors typically want to strive for diversification. One way to do that is by investing in 20-30 individual stocks, another is to focus on in a handful of investment trusts or funds.

Scottish Mortgage Investment Trust (LSE:SMT) offers investors exposure to a high-conviction portfolio of innovative, growth-oriented global companies. Its top holdings include SpaceX (7.4%), Mercadolibre (6.5%), Amazon, Meta, and Nvidia.

These are firms at the forefront of e-commerce, artificial intelligence (AI), and digital infrastructure. The trust actively targets transformational businesses, often before they’re fully recognised by the wider market, and includes private companies such as Bytedance.

However, this strategy comes with risks. The trust employs gearing (borrowing) to enhance returns, which can magnify losses during market downturns. Moreover, its growth bias can lead to volatility, particularly in rising interest rate environments.

For long-term investors with a decent tolerance for risk, it remains an opportunity worth considering. It has a place across my own portfolios.

Should you invest, the value of your investment may rise or fall and your capital is at risk. Before investing, your individual circumstances should be assessed. Consider taking independent financial advice.

James Fox has positions in Nvidia and Scottish Mortgage Investment Trust Plc. The Motley Fool UK has recommended Amazon, MercadoLibre, Meta Platforms, and Nvidia. Views expressed on the companies mentioned in this article are those of the writer and therefore may differ from the official recommendations we make in our subscription services such as Share Advisor, Hidden Winners and Pro. Here at The Motley Fool we believe that considering a diverse range of insights makes us better investors.