Interesting to note on the 5 year time scale, SMT which is a TR share with a tiny yield is the worst performing Trust.

GL

Investment Trust Dividends

Interesting to note on the 5 year time scale, SMT which is a TR share with a tiny yield is the worst performing Trust.

GL

You do not need to take big risks with your Snowball to increase your income but it does help if you are ready to buy after a market downturn.

If you had just simply re-invested your dividends, you would have achieved the holy grail of investing in that you could take out your stake and MRCH would be producing income at a zero, zilch, nothing cost. If you had then re-invested the capital in a long term gilt you could achieve a blended yield of ten percent, with little or nor risk to your hard earned. You would then have 20k of capital invested producing around 1k of income to add to your Snowball.

A £10k lump sum in this dividend share portfolio could help Stocks and Shares ISA investors enjoy a large long-term income.

Posted by Royston Wild

Published 10 August

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Pleasingly for local income investors, the UK stock market has a strong culture when it comes to paying dividends. This means people holding products like a Stocks and Shares ISA have a wide range of shares to choose from when targeting a robust and reliable passive income.

The FTSE 100 and FTSE 250 are loaded with companies boasting market-leading positions, diverse revenue streams, and rich balance sheets. Many of these operate in mature industries with limited growth potential, too: this means they’re more likely to return surplus cash to shareholders than invest it for future growth.

This rich selection means investors can create income-generating portfolios that are closely tailored to their specific investment goals and appetite for risk. It also allows for terrific diversification that can generate a strong second income at all points of the economic cycle.

Here’s what a well-diversified ISA portfolio could look like today:

| Dividend share | Sector | Years of continued dividend growth | Forward dividend yield |

|---|---|---|---|

| BAE Systems | Defence | 21 | 1.8% |

| Legal & General Group | Financial services | 4 | 8.4% |

| Coca-Cola HBC | Consumer staples | 12 | 2.5% |

| Sirius Real Estate | Real estate | 11 | 5% |

| Rio Tinto | Mining | 0 | 6.2% |

| Bloomsbury Publishing | Media | 25+ | 3.3% |

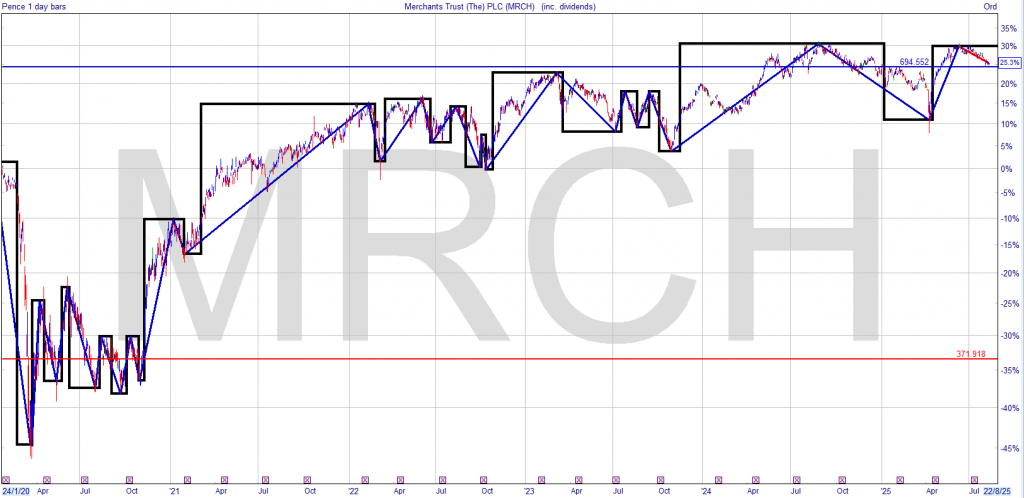

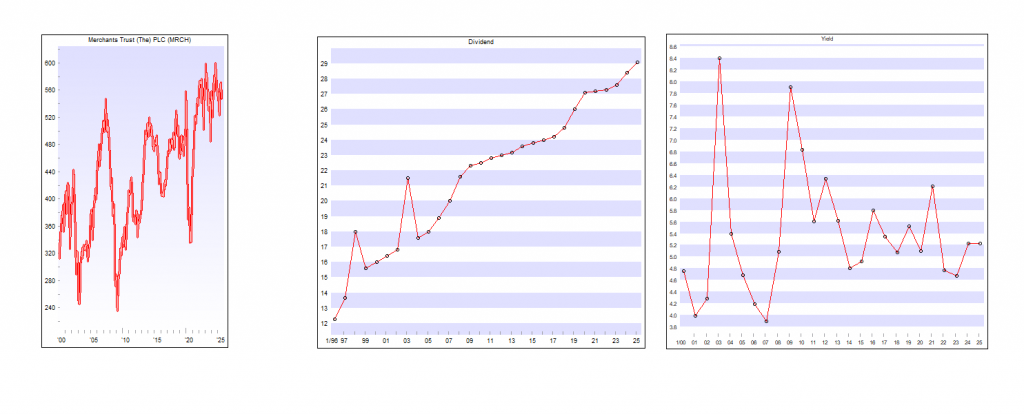

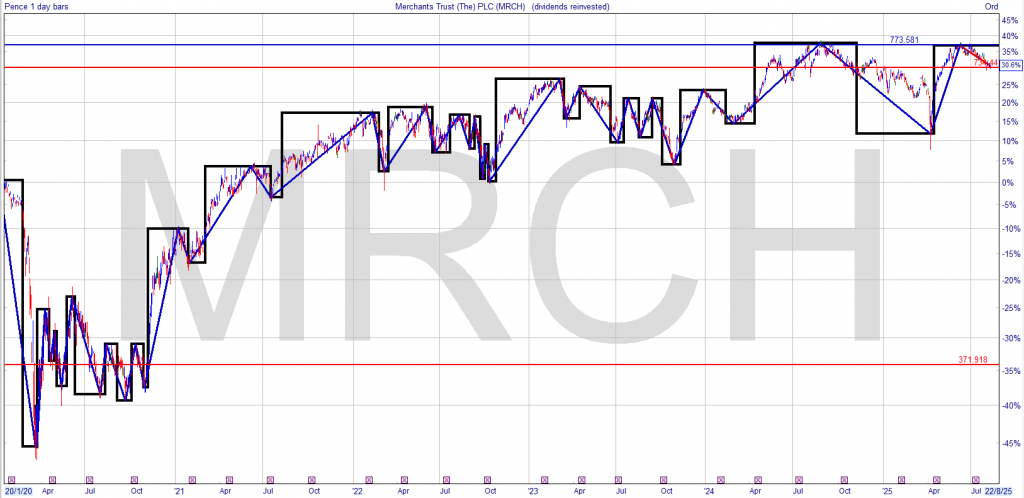

| Merchants Trust (LSE:MRCH) | Investment trusts | 25+ | 5.3% |

| Foresight Solar Fund | Renewable energy | 10 | 9.3% |

| HSBC | Banking | 4 | 5.3% |

| Primary Health Properties | Real estate investment trusts (REITs) | 25+ | 7.4% |

As you can see, this selection of Footsie and FTSE 250 shares covers a range of cyclical and non-cyclical industries. It also includes companies with long records of annual dividend growth. These businesses have helped investors protect their income from inflation by providing consistent, growing payouts year after year.

Finally, many of the dividend stocks here have long histories of paying dividends above the UK share average. For this year, the average dividend yield for this grouping is 5.5%.

Let me explain why investment trusts like Merchants Trust can be powerful tools for targeting passive income. This particular one has grown annual payouts for 43 straight years, and provides a dividend yield far ahead of the FTSE 350 average of 3.3%.

These financial vehicles own a basket of assets, which provides investors’ portfolios with even better diversification. This Allianz-owned one holds shares in 52 different companies, ranging from banking stock Lloyds and pharmaceuticals developer GSK, through to utilities company National Grid.

Merchants Trust is also focused on the more robust companies found on the FTSE 100 and FTSE 250 as well. This provides it with added strength that supports strong and consistent dividend growth.

A focus on UK shares leaves the trust more exposed to regional difficulties than more geographically diversified ones. However, this could also pay off over time if the recent rotation into British stocks from US shares continues.

Based on this year’s 5.5% forward dividend yield, our mini ISA portfolio of shares could deliver a £1,100 passive income this year on a £20,000 lump sum investment.

What’s more, if their dividends grow by an average 5% a year over the next 25 years, it could provide a second income of £3,725 at the end of the period.

Dividends are never guaranteed, even with a diversified portfolio. But I’m confident this set of shares could deliver a robust long-term passive income.

Story by Royston Wild

House models and one with REIT – standing for real estate investment trust – written on it.© Provided by The Motley Fool

For my money, the best way to source a long-term second income is to invest in dividend-paying assets. I own a variety of stocks, investment trusts and exchange-traded funds (ETFs) that have a history of paying a large and growing income over time.

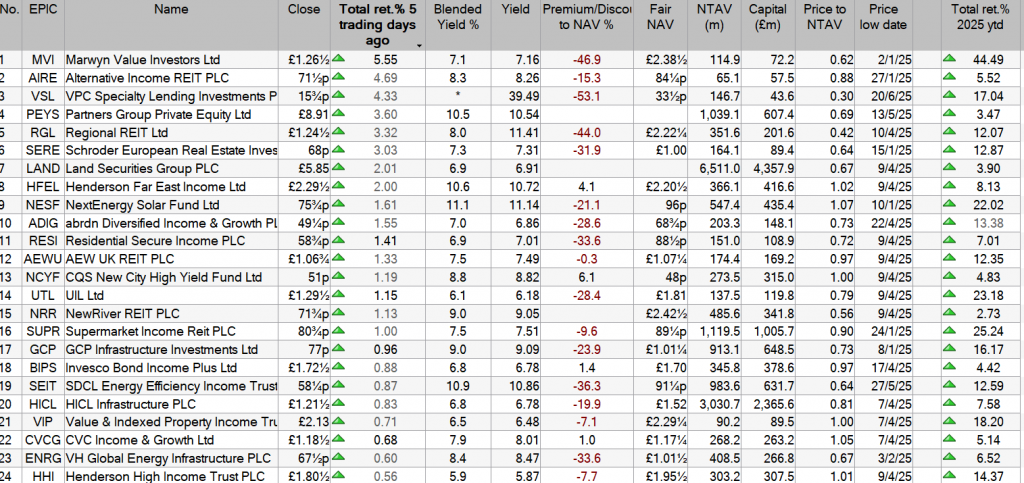

At 11%, Henderson Far East Income (LSE:HFEL) has one of the highest forward dividend yields on the London stock market. This reflects in large part significant share price weakness in recent years that’s inflated the yield.

As its name implies, it provides significant exposure to China and the surrounding regions. Around 27% of its capital is tied up in Chinese equities alone. So amid signs of severe economic cooling there, it’s no shock to see it fall in value.

The trust’s regained much ground in 2025, thanks to signs of improvement in China’s economy. Yet with trade tensions simmering, it’s possible the share price could turn lower again.

The make-up of its portfolio also allows it to weather individual dividend shocks and pay a large and growing dividend. As well

Source: Janus Henderson

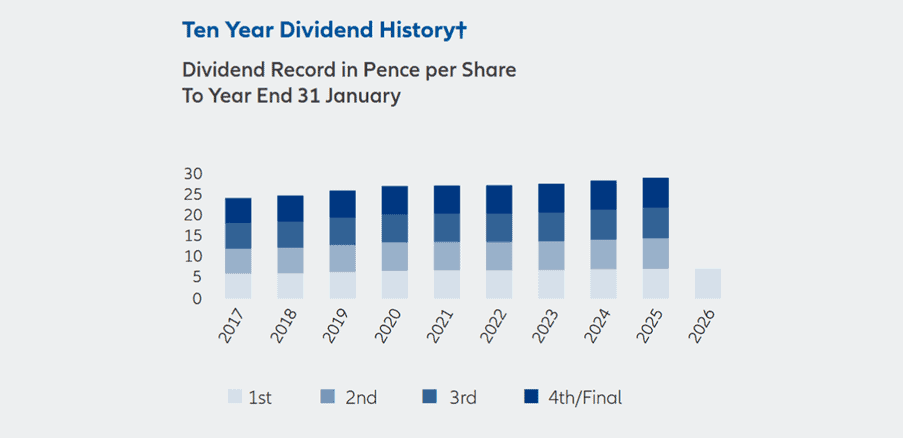

As you can see, annual dividends have kept steadily rising, even in spite of troubles in the key Chinese market. In fact, they’ve grown for 17 years on the bounce.

TR Property Investment Trust (LSE:TRY) doesn’t have such a knockout near-term dividend yield. For 2025, it sits at a still-market-beating (but not double-digit) figure of 5%.

What it does have however, is a similarly excellent record of unbroken dividend growth. Shareholder rewards have risen almost each year for around 20 years.

Source: TR Property

Many of these trusts focus on cyclical sectors like retail, leisure and industrials. And so rental collection and building occupancy are highly sensitive to economic conditions.

But strong diversification across sectors helps limit such damage on overall returns. Healthcare, residential and food retail are also among the industries it has exposure to through the 48 REITs it holds.

Today, the trust trades an a near-8% discount to its net asset value (NAV) per share of 352p. Combined with that large dividend yield, I think it’s a great value investment trust to consider.

The post 2 investment trusts I’d consider for long-term passive income appeared first on The Motley Fool UK.

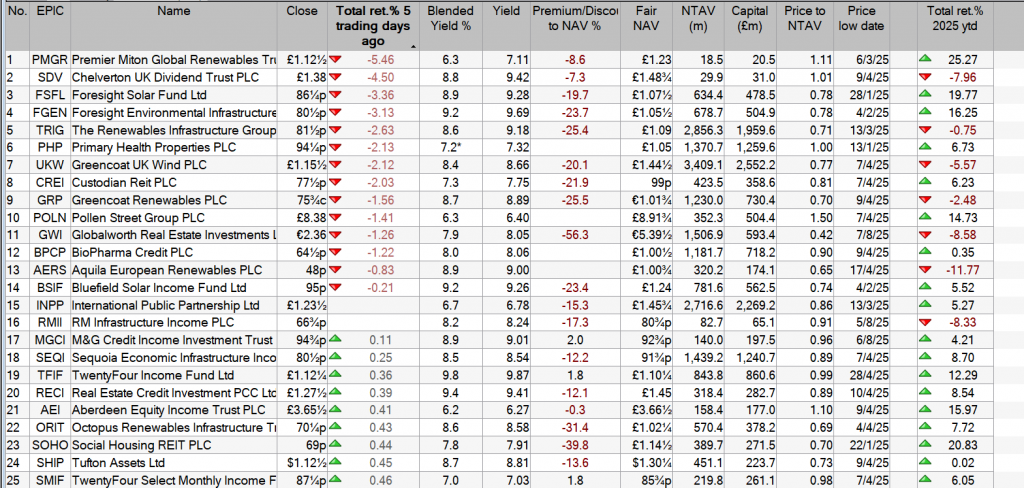

Greencoat UK Wind on the rise as institutions clamour for renewables

Last updated: 02 Aug 2025

Greencoat UK Wind PLC is the leading listed renewable infrastructure fund, invested in operating UK wind farms.

The fund is a constituent of the FTSE 250 and has a market capitalisation of approximately c.£3.2bn.

02 Aug 2025

Greencoat UK Wind PLC’s (LSE:UKW) Matt Ridley talked with Proactive about the company’s interim results and strategic direction in a challenging macro environment.

Ridley highlighted that this marks the twelfth consecutive year of paying an RPI-linked progressive dividend, amounting to £1.3 billion in total distributions. “We generated about £1 billion of cash to reinvest in the business,” he noted, emphasising the importance of maintaining net asset value in real terms.

Despite facing some of the lowest wind speeds in the first half of the year, Greencoat UK Wind still achieved a 1.4x dividend cover. Ridley said this demonstrates the resilience of the portfolio. However, net asset value declined, impacted by lower-than-expected generation and softer power prices.

To support capital allocation efforts, the company has now completed £222 million in asset disposals over eight months, including four new disposals announced with the interim results. These were completed at prevailing NAV, reinforcing the disconnect between the share price and private market valuations.

Greencoat UK Wind PLC (LSE:UKW) has agreed to sell partial stakes in three of its wind farms, raising a total of £181 million and bringing its cumulative disposals over the past year to £222 million.

The London-listed renewables investment group said on Wednesday that it will dispose of 32.65% interests in each of the Andershaw and Bishopthorpe onshore wind farms for £42.6 million.

The income yield is 5.35%, the gross redemption yield is 5.42% but we will not dwell on that for long as the redemption date is 2056. Next income payment date 31 Jan.

If you have twenty years to retirement you will receive all you capital back as income. If you have thirty years to retirement you will achieve the holy grail of investing in that for ten years you will have in your Snowball a position that pays you income at zero, zilch, nothing cost.

Now 5.35% isn’t 7%, so you could pair trade it with a higher yielder.

If not, as you re-invest the income the blended yield will grow to above 7%.

On a 10k investment, after twenty years you will receive income of £535.00

The income re-invested at 7% would produce income of £700.00.

A blended yield of 12.35%

If you are lucky enough to have thirty years to invest, you can work out the return you will receive in the last ten years. Also if/when interest rates rise again you may be able to re-invest your income back into the gilt at a better rate. Income is taxable, so best if held in a tax free wrapper.

You have to allow for inflation and also that you could/will make a capital loss until the maturity date.

Let’s look ahead using 100k of capital, you will most probably haven’t got 100k but it’s easier to make a pro rata comparison.

Option one: A Snowball which invested in a portfolio of Investment Trusts/Etfs compounding at 7%

Option two buy a passive tracker we will use VWRP that fluctuates with the market but compounds at 7%.

After ten years

Snowball Income 14k

Tracker using the 4% rule 8k

After twenty years

Snowball Income 28k

Tracker using the 4% Rule 16k

If you are lucky enough to have 30 years

Snowball Income 56k

Tracker 32k

So what looked liked the high risk strategy wasn’t at all.

If you can keep your head when all about you are losing theirs and blaming it on you:

If you can trust yourself when all men doubt you:

But make allowance for their doubting too:

If you can wait and not be tired by waiting:

GL

Story by Christopher Ruane

Senior woman potting plant in garden at home© Provided by The Motley Fool

Put money into a Stocks and Shares ISA, buy a range of high-quality dividend shares, monitor the portfolio from time to time.

Can earning sizeable passive income streams really be as simple as that? Yes it can!

I ought to explain immediately that this is no overnight scheme. Rather, it is an example of how a long-term approach to investing can hopefully pay rewards in future.

If the £20k is compounded at 8% annually, after 32 years the Stocks and Shares ISA should be worth over £234k. An 8% dividend yield on that would amount to over £18k a year in passive income – without touching the capital.

With more than £20k, the timeline could be reduced — or the goal could be targeted with less than £20k, but taking more years to reach it. Another variable is the compound annual growth rate and later, dividend yield achieved. The higher that is, the quicker the goal could be hit — but it is important to stay realistic. Too much risk could mean what seems like a quicker approach ends up being a slower one after all.

That helps explain why I think the savvy investor will take time to construct a carefully selected, diversified portfolio of high-quality shares.

Another element that could eat into the compound annual growth is fees, charges, commissions, taxes and the like. So choosing the most suitable Stocks and Shares ISA is also wise in my view.

I think an 8% target is realistic in today’s market. The current FTSE 100 average dividend yield is 3.3%. Some individual shares offer much higher yields – and the compound annual growth rate takes share price movement into account too.

© 2026 Passive Income Live

Theme by Anders Noren — Up ↑